S&P500 rises as Nvidia lifts tech, Fed minutes points to more rate cuts ahead

Introduction & Market Context

SBC Medical Group Holdings Inc. (NASDAQ:SBC) presented its first quarter 2025 financial results on May 15, 2025, revealing a mixed performance characterized by revenue declines but improved profitability metrics. The medical aesthetics company, currently trading at $4.35, has seen its stock price fall significantly from its 52-week high of $12.50, reflecting ongoing market concerns about its business transformation.

The Q1 results come against a backdrop of strategic restructuring that would later lead to more pronounced challenges in Q2, when the company would report a significant earnings miss. However, the Q1 presentation highlighted the company’s strong franchise clinic expansion and robust balance sheet as positive indicators amid the transition.

Quarterly Performance Highlights

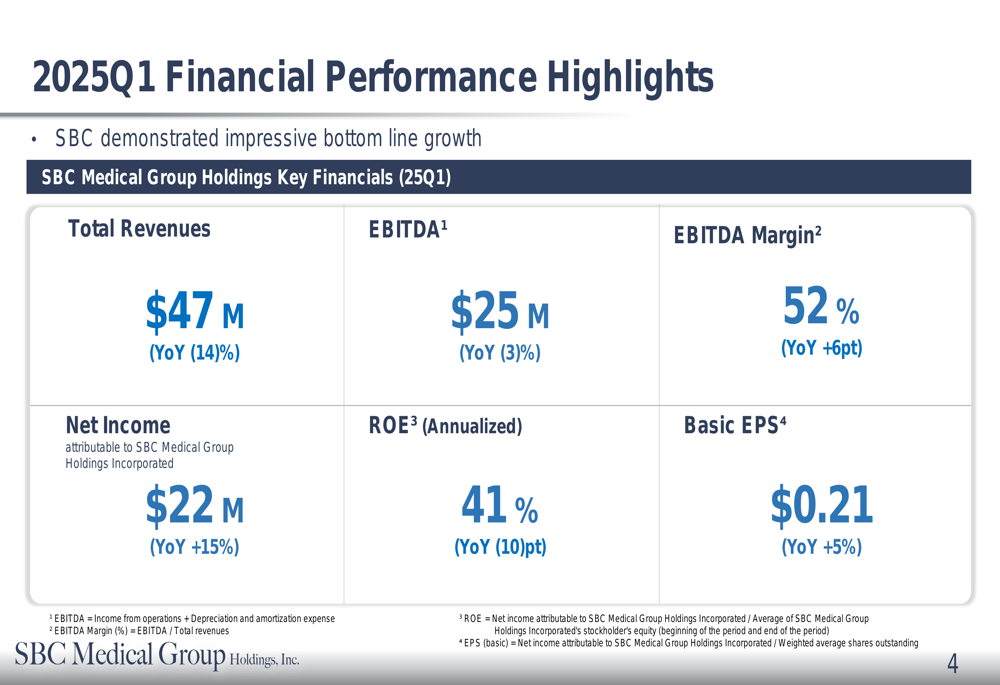

SBC Medical reported total consolidated revenue of $47 million for Q1 2025, representing a 14% year-over-year decline. However, the company emphasized that this decrease was largely attributable to the deconsolidation of SNA and Kijimadaira operations and the termination of its temporary staffing business.

Despite the revenue decline, net income attributable to SBC Medical increased by 15% year-over-year to $22 million, while basic earnings per share rose 5% to $0.21. The company also reported an EBITDA of $25 million with an improved margin of 52%, representing a 6 percentage point increase year-over-year.

As shown in the following financial performance highlights, the company maintained strong profitability metrics despite revenue challenges:

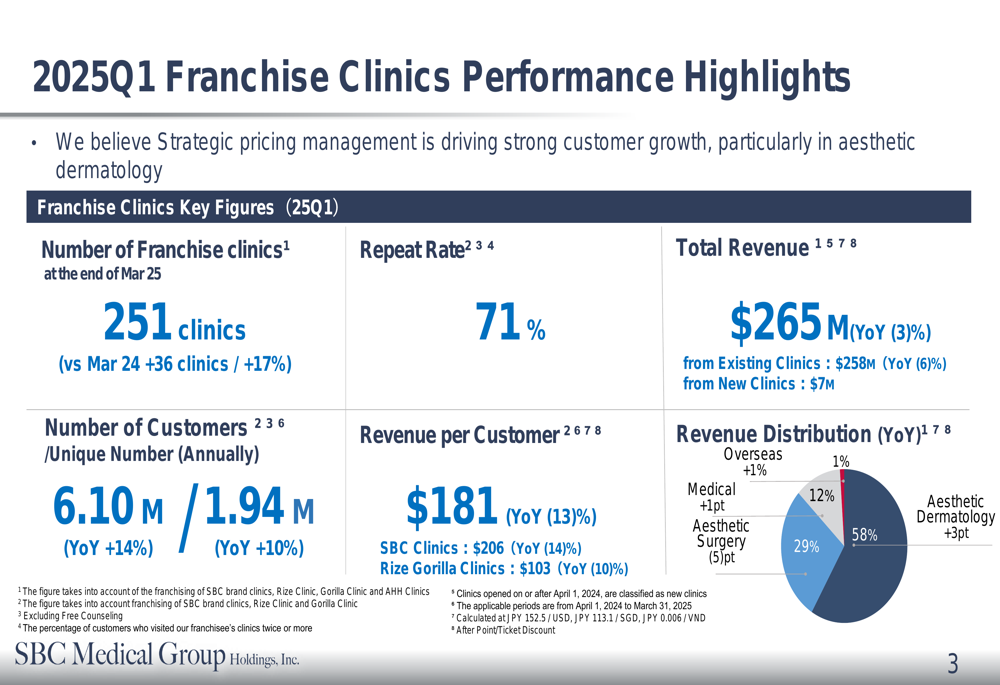

On the operational front, SBC Medical continued to expand its franchise clinic network, which grew to 251 locations, representing a 17% increase (36 additional clinics) compared to March 2024. The company served 6.10 million customers (up 14% year-over-year) with 1.94 million unique customers (up 10%). The customer repeat rate stood at a healthy 71%, though revenue per customer declined by 13% to $181.

The following chart illustrates the franchise clinic performance highlights:

Detailed Financial Analysis

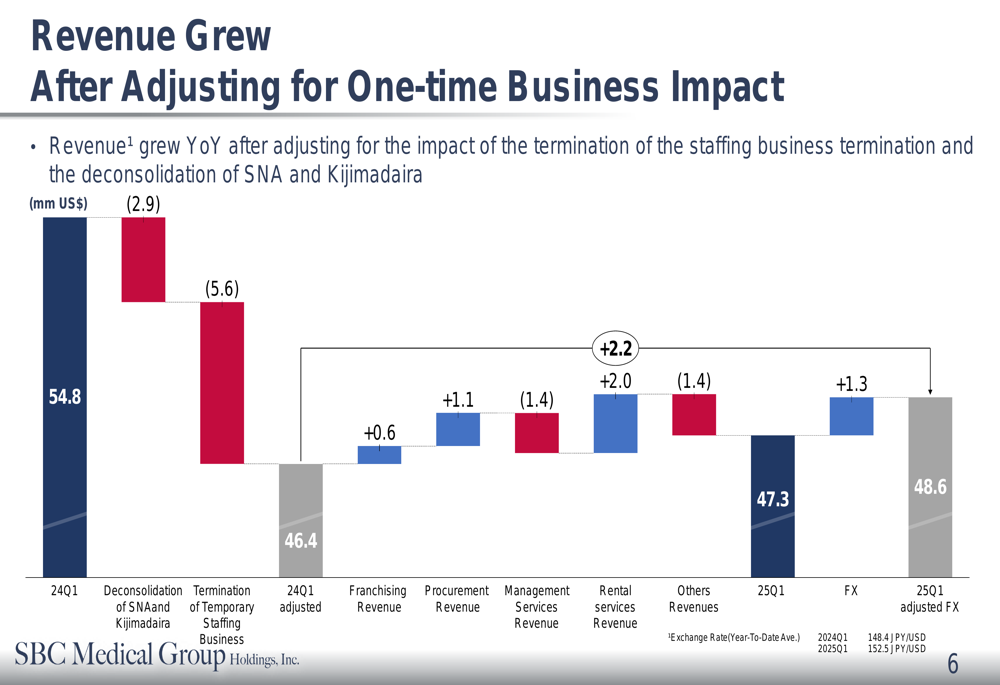

A closer examination of SBC Medical’s revenue components reveals varying performance across business segments. Franchising revenue increased by 4% year-over-year to $16 million, while procurement services grew 9% to $14 million. However, management services revenue declined significantly by 44% to $9 million, and rental services increased by 56% to $6 million.

The company provided a detailed waterfall chart breaking down the revenue changes between Q1 2024 and Q1 2025, illustrating how the 14% headline decline was influenced by various factors:

As shown above, after adjusting for the deconsolidation of certain operations ($2.9 million impact) and the termination of the temporary staffing business ($5.6 million impact), the adjusted revenue actually showed modest growth from $46.4 million to $47.3 million, or $48.6 million when adjusted for foreign exchange effects.

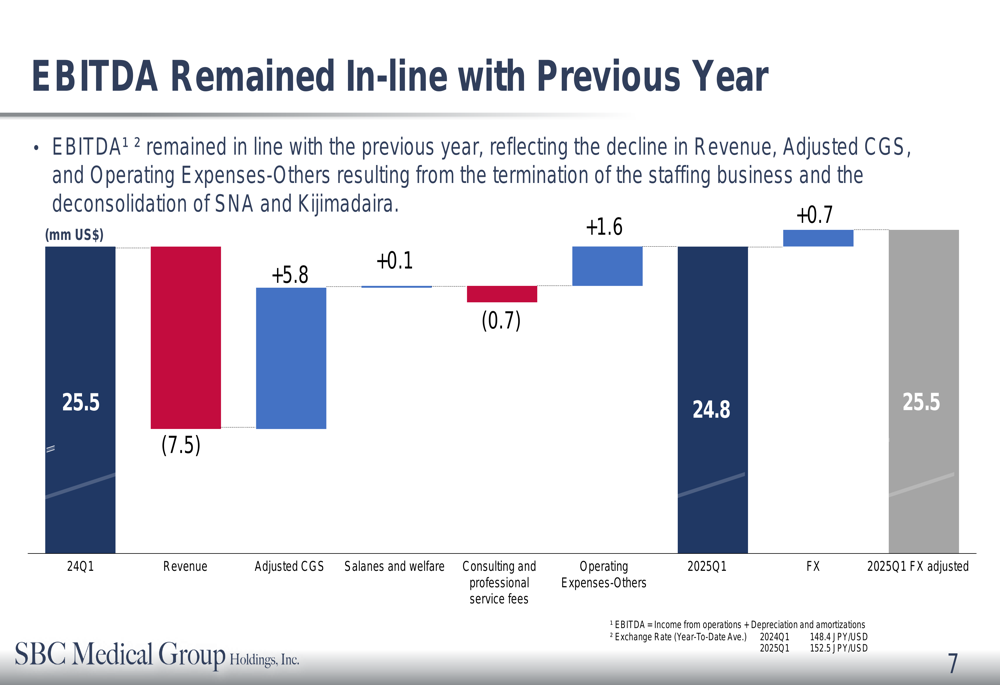

Similarly, EBITDA remained stable year-over-year at $24.8 million, or $25.5 million when adjusted for foreign exchange, as illustrated in this breakdown:

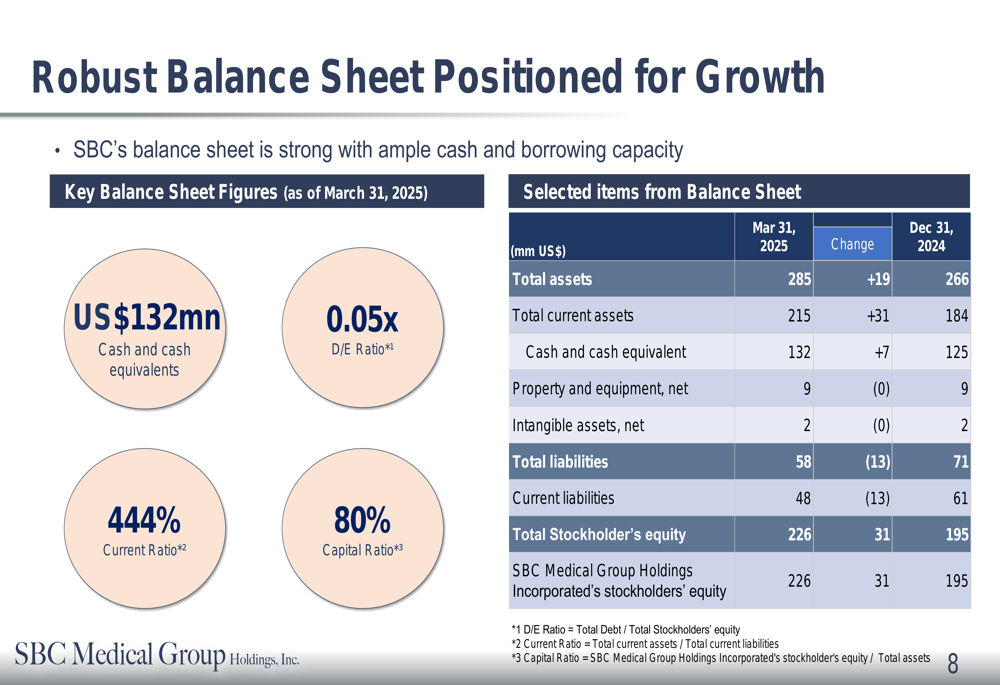

The company maintained a strong balance sheet with $132 million in cash and cash equivalents, a very low debt-to-equity ratio of 0.05x, and an impressive current ratio of 444%. Total assets increased to $285 million as of March 31, 2025, compared to $266 million at the end of 2024.

Strategic Initiatives

In a significant announcement, SBC Medical revealed plans for a $5 million share buyback program running from May 20, 2025, to May 20, 2026. Management stated this decision was based on their belief that the current share price undervalues the company’s performance and growth potential.

Notably, the company also announced the cancellation of a previously planned Bitcoin purchase, indicating a shift in capital allocation strategy toward returning value to shareholders and focusing on core operations.

The revenue distribution chart showed that aesthetic dermatology remains the company’s primary focus, accounting for 58% of total revenue, followed by aesthetic surgery at 29%, medical services at 12%, and overseas operations at just 1%.

Forward-Looking Statements

While the Q1 2025 presentation painted a picture of strategic transformation with stable underlying performance, subsequent events have cast doubt on the sustainability of this trajectory. According to recent earnings reports, SBC Medical’s Q2 2025 results showed a significant deterioration, with EPS plummeting to $0.02 (versus an expected $0.14) and revenue further declining to $43 million, representing an 18% year-over-year drop.

The company continues to pursue ambitious growth plans, targeting 1,000 clinics within the next decade and exploring merger and acquisition opportunities in North America and Asia. SBC Medical is also focusing on expanding into high-growth, high-margin areas such as orthopedics and AGA (androgenetic alopecia) treatment.

Despite these challenges, CEO Mr. Aikawa has emphasized the company’s resilience, stating, "Our strength is the spirit of never give up," and highlighting SBC Medical’s customer-centric approach: "We would like to provide the treatment that matches the customer needs."

The contrast between the relatively stable Q1 2025 performance and the subsequent Q2 decline suggests that investors should closely monitor the company’s ability to execute its strategic transformation while maintaining financial stability. With the stock trading significantly below its 52-week high, the announced share buyback program may provide some support for the share price, but the fundamental business performance will ultimately determine the company’s trajectory.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.