S&P500 rises as Nvidia lifts tech, Fed minutes points to more rate cuts ahead

Introduction & Market Context

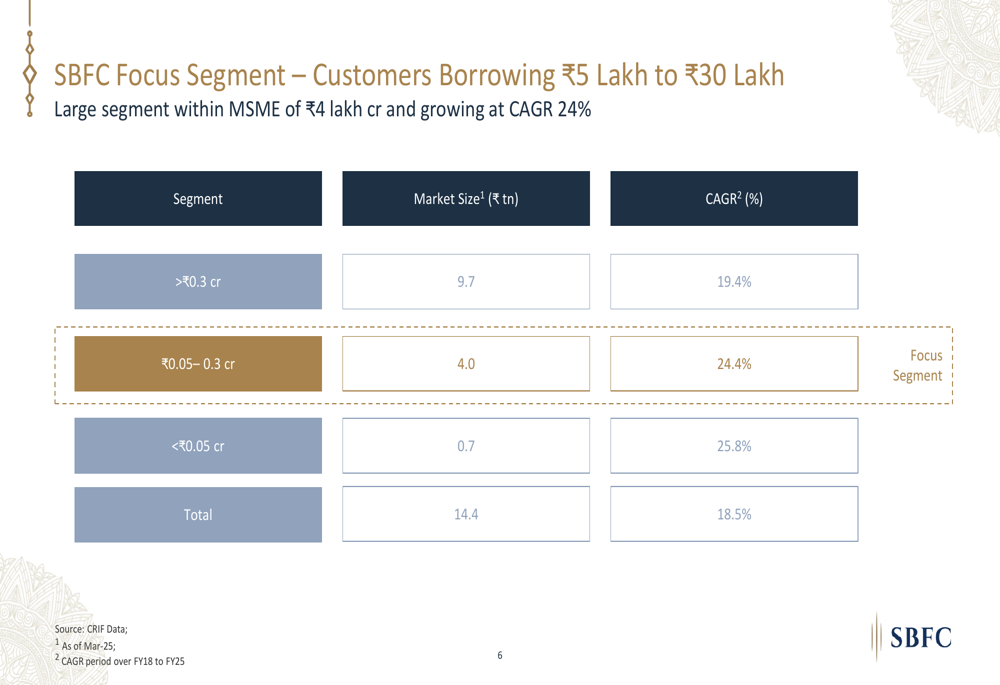

SBFC Finance Ltd (NSE:SBFC) presented its Q1 FY26 financial results on July 26, 2025, showcasing continued growth momentum in its core secured MSME lending business. The company, which focuses on providing loans in the ₹5 lakh to ₹30 lakh segment, operates in a market estimated at ₹41 lakh crore that is growing at a 24% CAGR (FY18-FY25).

SBFC has established a pan-India footprint with 215 branches across 16 states and 2 union territories, positioning itself to capitalize on the significant opportunity in small business financing. The company’s focus on secured lending with rigorous credit underwriting has enabled it to maintain strong growth while managing risk.

Quarterly Performance Highlights

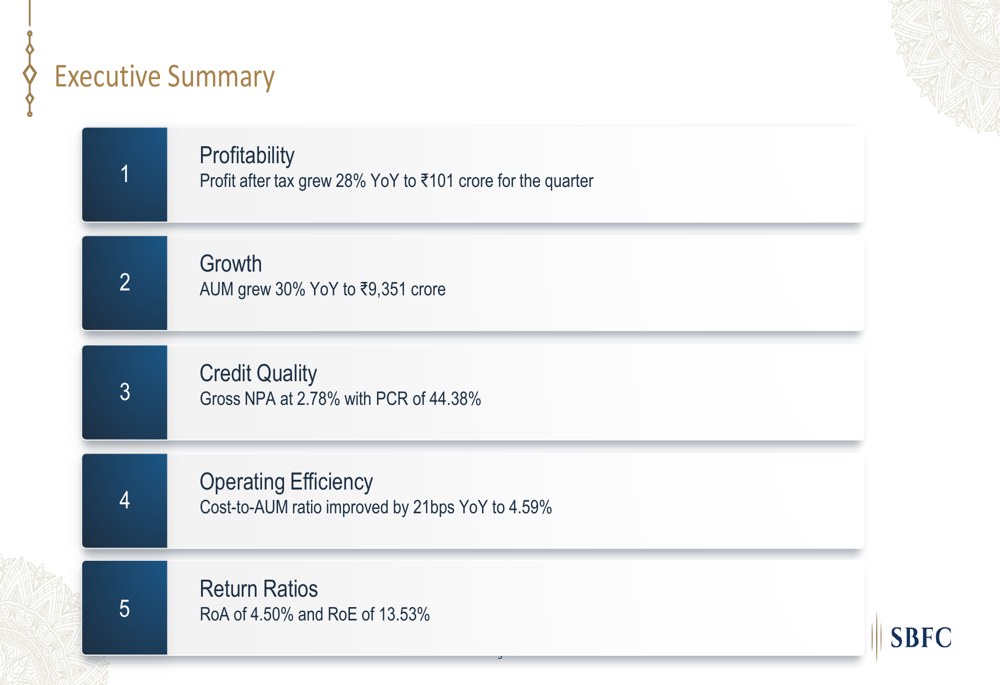

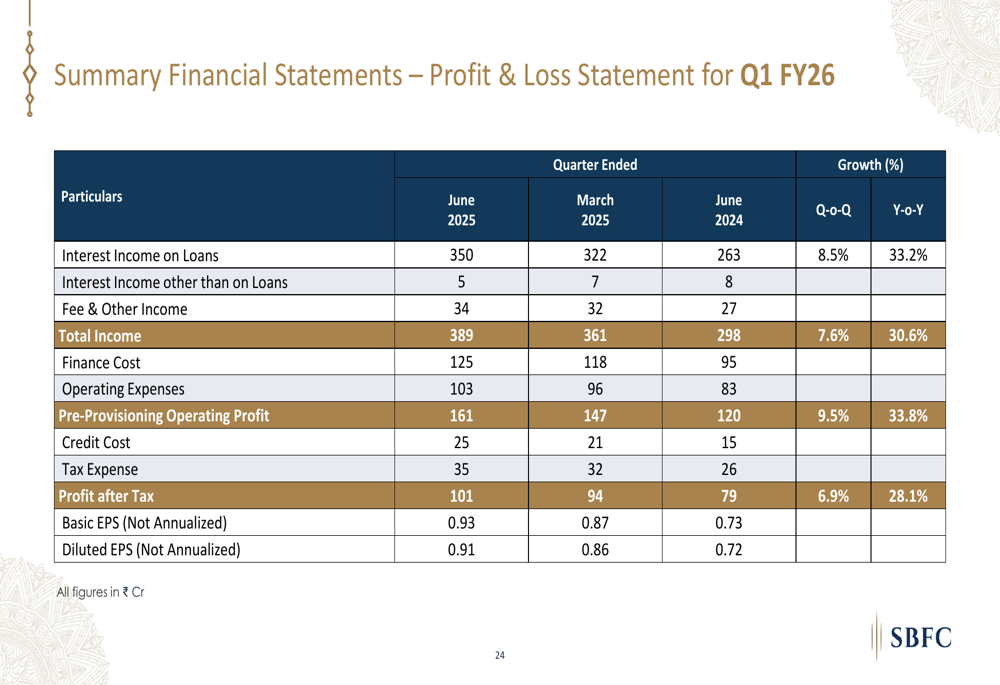

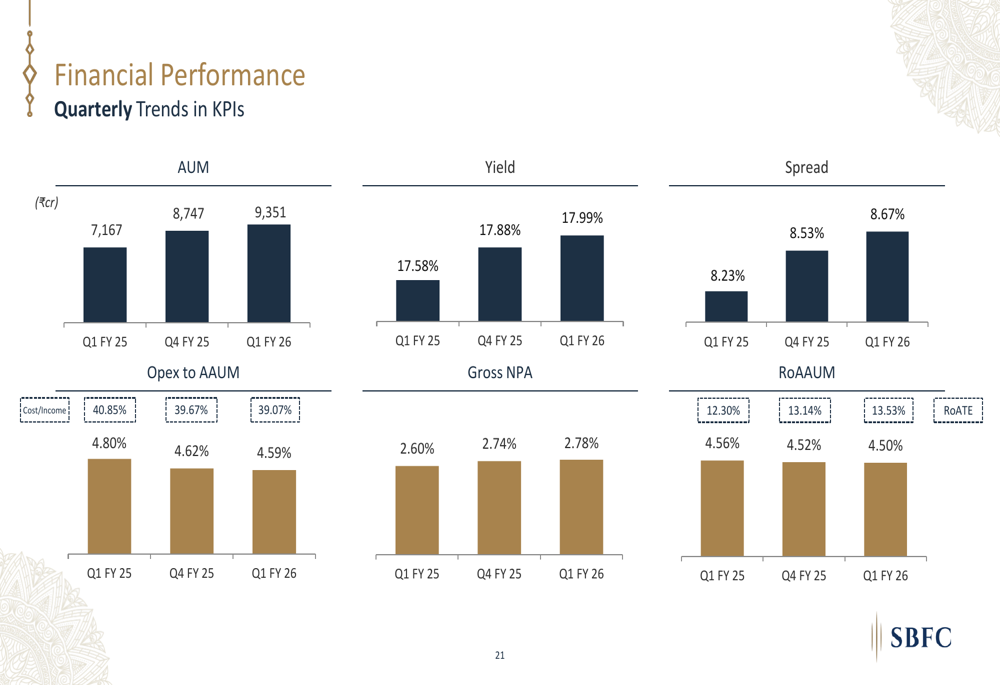

SBFC Finance reported a profit after tax of ₹101 crore for Q1 FY26, representing a 28% year-over-year increase. This marks the first quarter where the company’s PAT has crossed the ₹100 crore milestone. Assets under management (AUM) grew to ₹9,351 crore, up 30% year-over-year and 7% quarter-over-quarter.

As shown in the following comprehensive performance snapshot, the company maintained strong metrics across multiple dimensions:

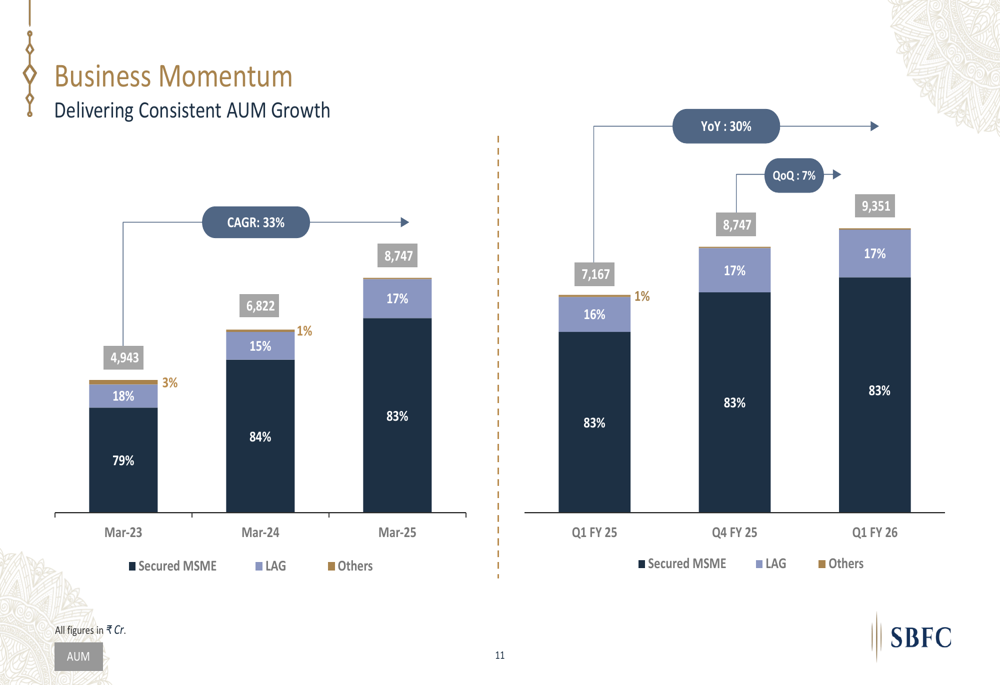

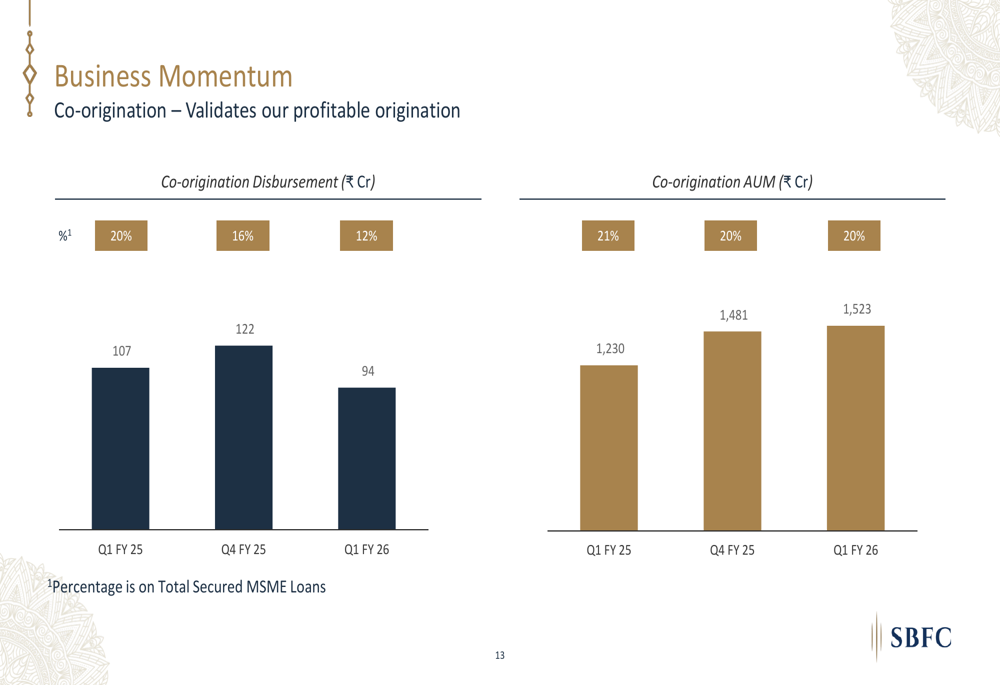

The company’s core secured MSME segment, which constitutes 83% of the total AUM at ₹7,744 crore, also grew by 30% year-over-year. Disbursement value in this segment increased by 51% year-over-year to ₹809 crore, while disbursement volume grew by 48% to ₹8,619 crore.

The following chart illustrates the momentum in SBFC’s secured MSME business:

Detailed Financial Analysis

SBFC’s financial performance showed improvement in several key metrics. The yield on loans increased to 17.99%, up 41 basis points year-over-year, while the spread widened to 8.67%, an improvement of 44 basis points compared to the same period last year. The cost of borrowing remained stable at 9.32%, decreasing by 3 basis points year-over-year.

The company’s profit and loss statement highlights the strong growth in both income and profitability:

Operational efficiency continued to improve, with the cost-to-AUM ratio decreasing by 21 basis points year-over-year to 4.59%. This contributed to a pre-provisioning operating profit of ₹161 crore, up 33.8% from the previous year.

Return ratios remained robust, with return on average assets (RoA) at 4.50% and return on average tangible equity (RoATE) at 13.53%. The following breakdown provides insight into the components driving SBFC’s return metrics:

Asset Quality and Risk Management

While SBFC maintained strong growth, there was a slight deterioration in asset quality metrics. Gross non-performing assets (GNPA) increased to 2.78%, up 18 basis points year-over-year and 4 basis points quarter-over-quarter. Net NPA also rose to 1.57%, up 6 basis points both year-over-year and quarter-over-quarter.

The following chart illustrates the trend in key credit quality indicators:

The 1+ days past due (DPD) metric increased from 6.37% to 8.12%, while collection efficiency decreased slightly from 97.89% to 97.24%. Despite these challenges, the company’s focus on secured lending (100% of the portfolio) and strong credit underwriting practices helps mitigate risk.

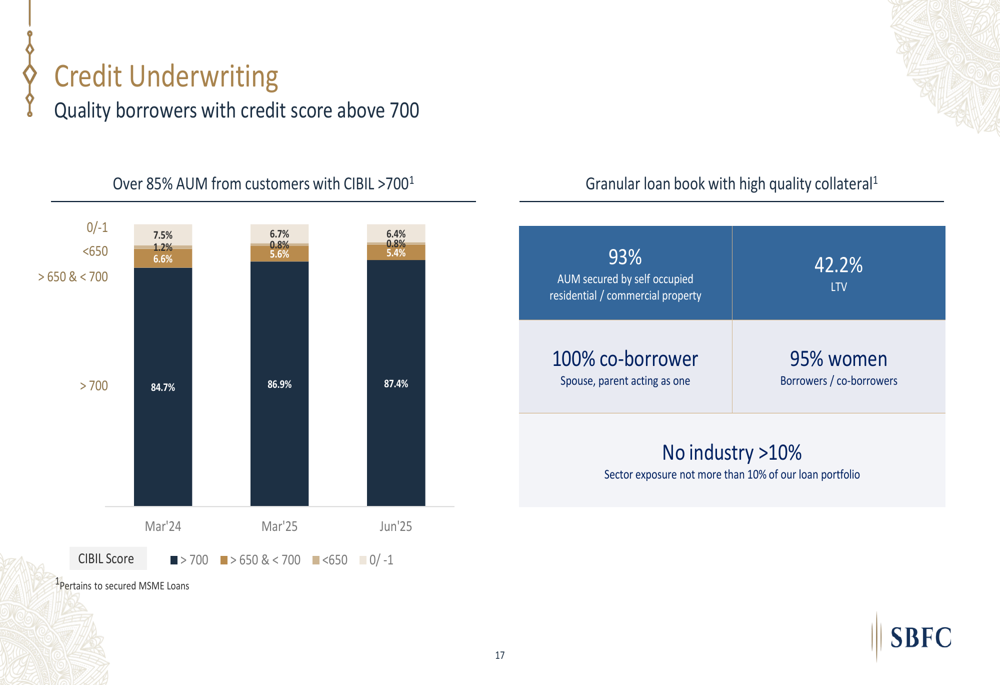

SBFC’s loan portfolio demonstrates strong credit quality, with 85% of AUM coming from customers with credit scores above 700. Additionally, 93% of the AUM is secured by property, and the company maintains a diversified portfolio with no single industry representing more than 10% of the business.

Growth Strategy and Outlook

SBFC Finance has demonstrated consistent growth since its inception, as illustrated in the following chart showing the company’s journey:

The company’s growth strategy includes geographic diversification, with a presence across India. Nearly 70% of SBFC’s branches have been operational for more than 36 months, providing a stable foundation for continued expansion.

SBFC also maintains a diversified funding profile, with access to multiple sources of borrowing including bank loans, external commercial borrowings (ECBs), securitization, and non-convertible debentures (NCDs). This diversification helps the company manage its cost of funds and ensure adequate liquidity.

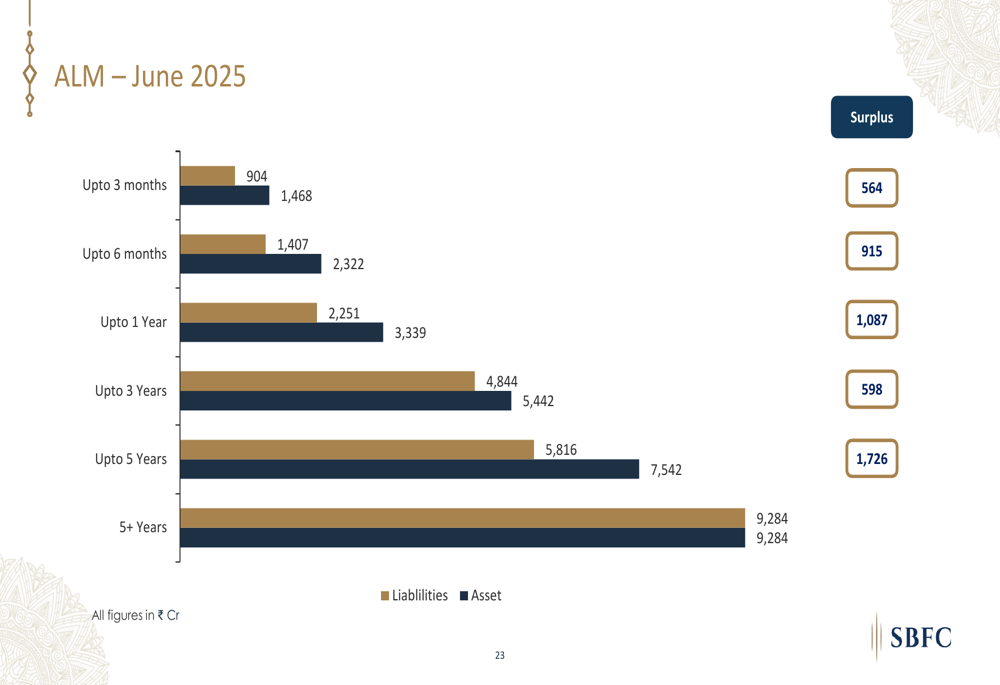

The company’s asset-liability management (ALM) remains healthy, with positive cumulative surpluses across all time buckets. This provides SBFC with financial flexibility to support its growth plans while managing liquidity risk.

Looking ahead, SBFC Finance appears well-positioned to continue its growth trajectory, leveraging its established branch network, robust credit underwriting capabilities, and focus on the underserved MSME segment. However, investors should monitor the slight deterioration in asset quality metrics, which could impact profitability if the trend continues.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.