September looms as a risk month for stocks, Yardeni says

Introduction & Market Context

State Bank of India (NSE:SBI) (NSE:SBIN), India’s largest public sector bank, reported a 12.48% year-over-year increase in net profit for the first quarter of fiscal year 2026, despite facing margin pressure. The bank presented its quarterly results on August 8, 2025, highlighting strong business growth across segments and continued improvement in asset quality metrics.

SBI’s stock closed at ₹704.83 on the day of the presentation, down 0.93% amid broader market volatility, even as the bank reported robust performance across most key metrics.

Executive Summary

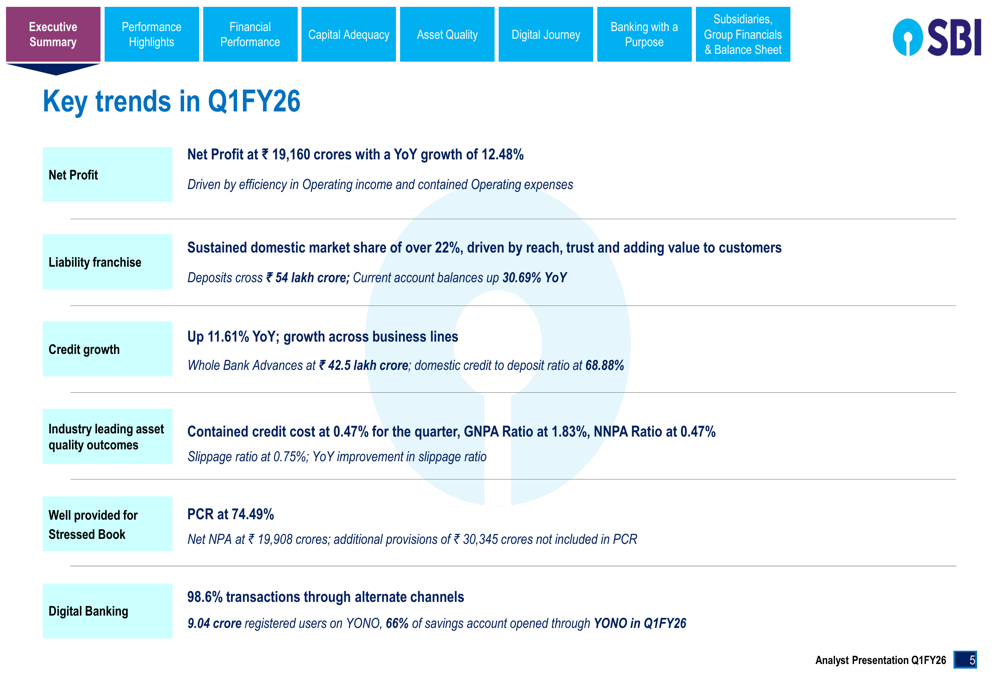

SBI delivered a net profit of ₹19,160 crores for Q1 FY26, representing a 12.48% increase compared to the same period last year. This growth was achieved despite net interest margin (NIM) compression, with whole bank NIM declining 32 basis points year-over-year to 2.90%.

The bank’s operating profit crossed the ₹30,000 crore mark, reaching ₹30,544 crores, a significant 15.49% increase from Q1 FY25. This performance was driven by efficiency in operating income and contained operating expenses.

As shown in the following key trends summary from the presentation:

Quarterly Performance Highlights

SBI’s liability franchise maintained a domestic market share of over 22%, with total deposits crossing ₹54 lakh crore, representing an 11.66% year-over-year growth. Notably, current account balances surged by 30.69% compared to the previous year, strengthening the bank’s low-cost deposit base.

On the lending side, whole bank advances reached ₹42.5 lakh crore, growing at 11.61% year-over-year. The domestic credit-to-deposit ratio stood at 68.88%, indicating a balanced approach to lending against the deposit base.

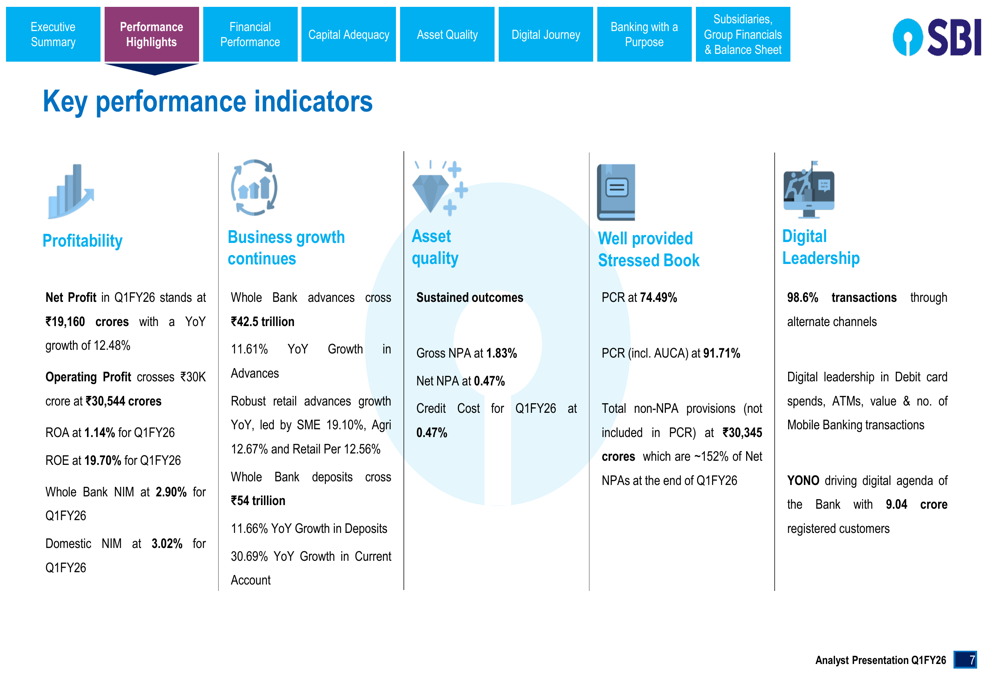

The bank’s key performance indicators demonstrate strong growth across multiple metrics as illustrated in this comprehensive overview:

Detailed Financial Analysis

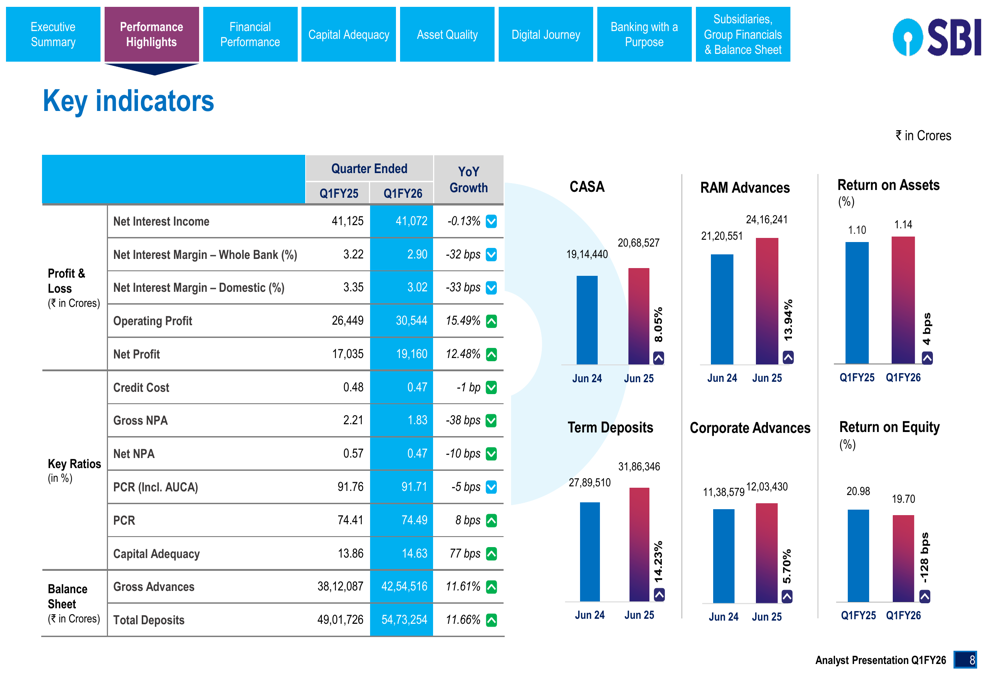

While SBI’s net interest income remained relatively flat at ₹41,072 crores compared to ₹41,125 crores in Q1 FY25, the bank managed to deliver strong profit growth through operational efficiency. Return on Assets (ROA) improved to 1.14% from 1.10% a year ago, although Return on Equity (ROE) declined to 19.70% from 20.98%.

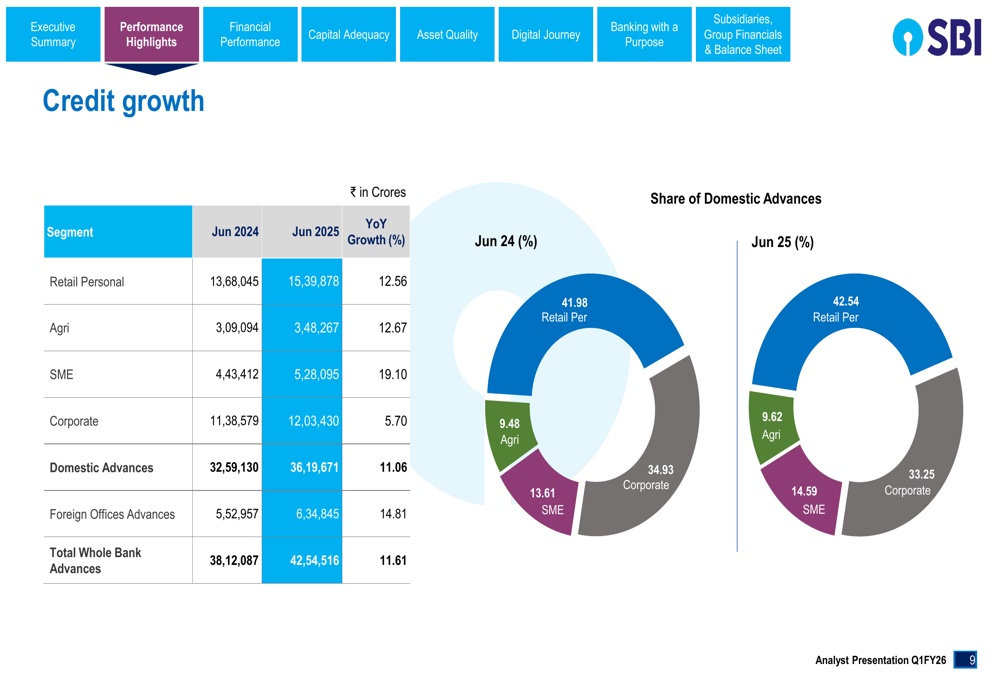

The bank’s credit growth was broad-based, with particularly strong performance in the SME segment, which grew by 19.10% year-over-year. The retail personal segment and agricultural loans also showed robust growth of 12.56% and 12.67% respectively, while corporate advances grew at a more modest 5.70%.

The following table provides a comprehensive view of SBI’s key financial metrics:

The bank’s loan portfolio remains well-diversified across sectors, with home loans constituting the largest segment at 23.51% of domestic advances. SBI maintains a dominant market position in retail lending, with a 27.7% market share in home loans and 19.3% in auto loans.

The credit growth breakdown across different segments demonstrates the bank’s balanced approach to lending:

Asset Quality & Capital Position

SBI continued to demonstrate improvement in asset quality metrics, with the Gross Non-Performing Asset (GNPA) ratio declining by 38 basis points year-over-year to 1.83%. Similarly, the Net NPA ratio improved by 10 basis points to 0.47%. The slippage ratio for the quarter stood at 0.75%, reflecting effective risk management.

The bank’s provision coverage ratio (PCR) improved slightly to 74.49% from 74.41% a year ago. Including amounts under Advance Under Collection Account (AUCA), the PCR stood at a robust 91.71%. SBI reported additional provisions of ₹30,345 crores not included in the PCR calculation, providing further cushion against potential stress.

Credit cost for the quarter remained well-controlled at 0.47%, marginally better than the 0.48% reported in Q1 FY25. The bank’s capital adequacy ratio strengthened significantly to 14.63%, up 77 basis points year-over-year, providing ample headroom for future growth.

Digital Banking Initiatives

SBI’s digital transformation continues to gain momentum, with 98.6% of transactions now conducted through alternate channels. The bank’s flagship digital platform, YONO (You Only Need One), has reached 9.04 crore registered users, underlining its widespread adoption.

The digital platform has become a significant acquisition channel, with 66% of savings accounts opened through YONO in Q1 FY26. This digital focus has helped SBI improve operational efficiency while enhancing customer experience.

International Operations

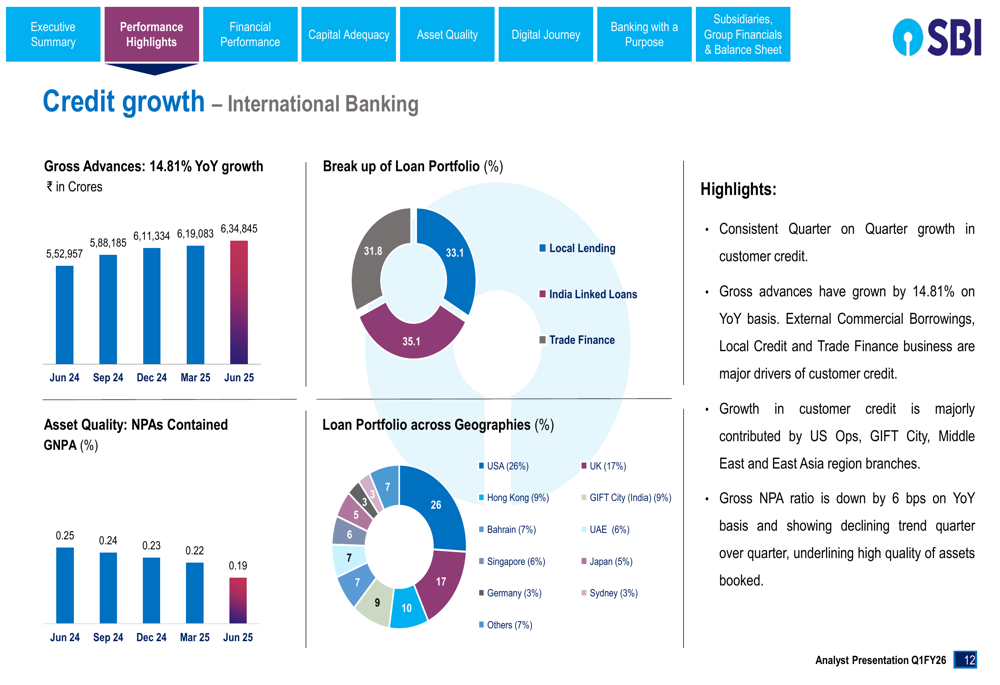

SBI’s international banking operations demonstrated strong growth, with foreign office advances increasing by 14.81% year-over-year to ₹6,34,845 crores. This growth was primarily driven by operations in the US, GIFT City, Middle East, and East Asia regions.

The international loan portfolio is diversified across local lending, India-linked loans, and trade finance. The bank highlighted that its international Gross NPA ratio declined by 6 basis points year-over-year, indicating improving asset quality in overseas operations.

The following chart details the performance of SBI’s international banking segment:

Forward-Looking Statements

While SBI did not provide specific guidance for the remainder of FY26, the strong Q1 performance positions the bank well for continued growth. The bank’s focus on digital transformation, improving asset quality, and diversified loan growth across segments suggests a balanced approach to navigating the current economic environment.

The margin pressure observed in Q1 will be a key area to watch in upcoming quarters, as will the bank’s ability to maintain its strong deposit growth and asset quality metrics. With its robust capital position and improving operational efficiency, SBI appears well-positioned to capitalize on growth opportunities in the Indian banking sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.