China chip stocks fall as US considers allowing Nvidia H200 sales

Introduction & Market Context

Scatec (OL:SCATC) reported a strong start to 2025, with doubled revenues and significant debt reduction according to the company’s Q1 2025 presentation delivered on May 8, 2025. The renewable energy developer and producer, currently trading at NOK 81 per share, emphasized its strengthened financial position and ambitious growth plans across its global portfolio of solar, hydro, and battery storage projects.

CEO Terje Pilskog highlighted the company’s strategy to double its operating capacity through near-term growth initiatives while simultaneously reducing corporate debt through strategic asset rotation.

Quarterly Performance Highlights

Scatec’s Q1 2025 results showed substantial year-over-year improvement across key metrics. Proportionate revenues doubled to NOK 2.4 million compared to NOK 1.2 million in Q1 2024, while proportionate EBITDA increased 75% to NOK 1.4 million from NOK 0.8 million in the prior-year period.

Power production reached 979 GWh in Q1 2025, an 8.7% increase from 901 GWh in Q1 2024, driving a 72% revenue increase in the company’s power production segment.

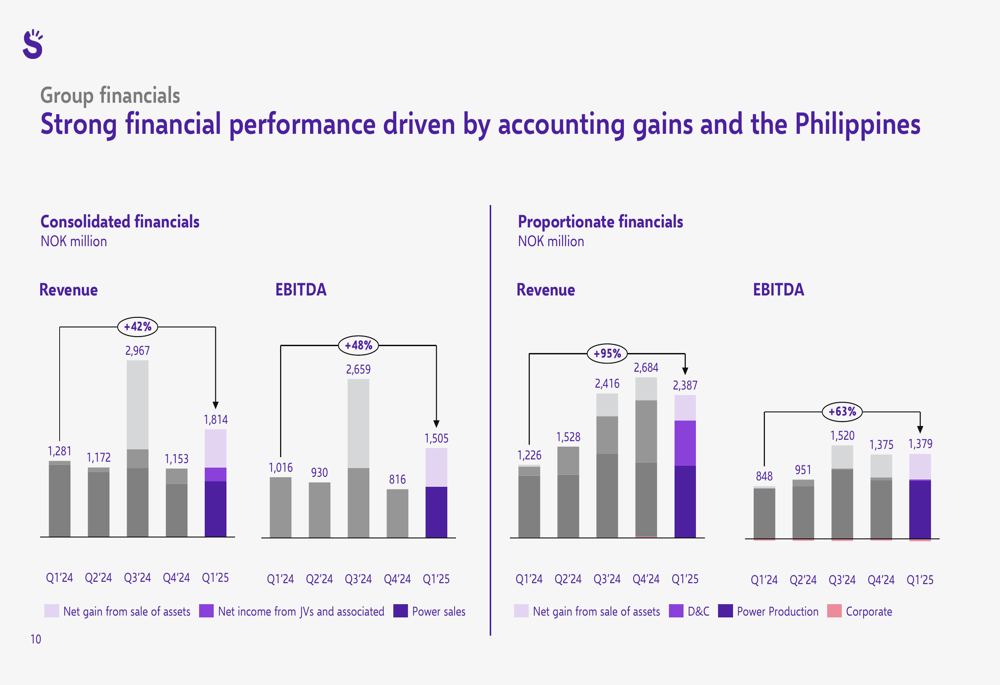

As shown in the following chart of quarterly financial performance:

The company’s consolidated revenues increased 42% while EBITDA rose 48% compared to the same period last year. On a proportionate basis, which reflects Scatec’s economic interest in its projects, the results were even stronger with 95% revenue growth and 63% EBITDA growth.

Detailed Financial Analysis

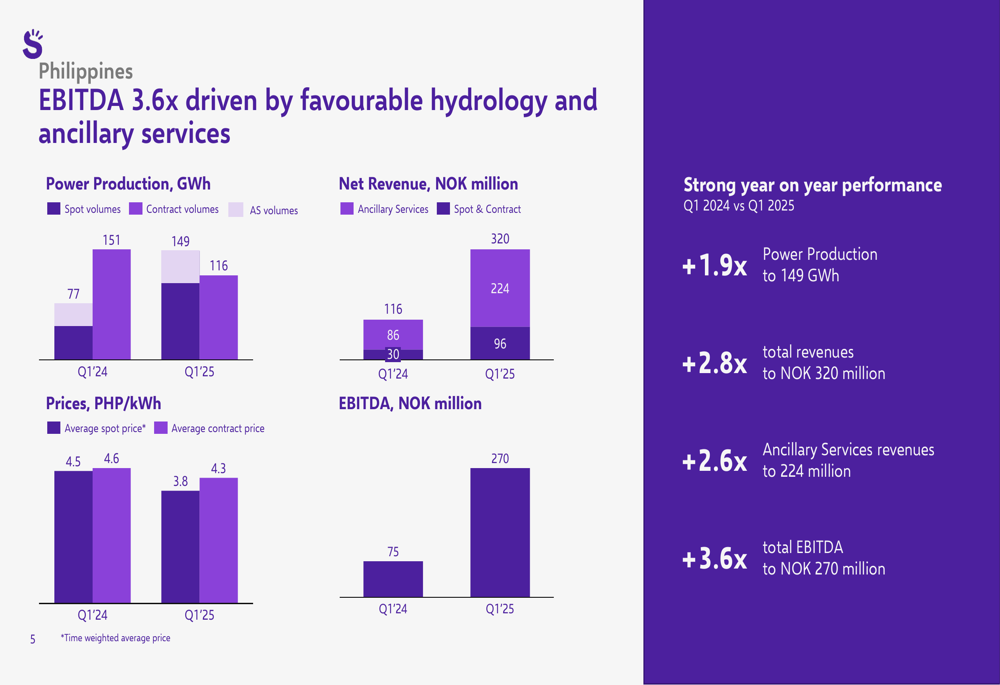

The standout performer in Scatec’s portfolio was its Philippines operations, which delivered exceptional results driven by favorable hydrology conditions and increased ancillary services. Philippines EBITDA surged 3.6 times compared to Q1 2024, with total revenues increasing 2.8 times and power production nearly doubling.

The following chart illustrates the dramatic improvement in the Philippines performance:

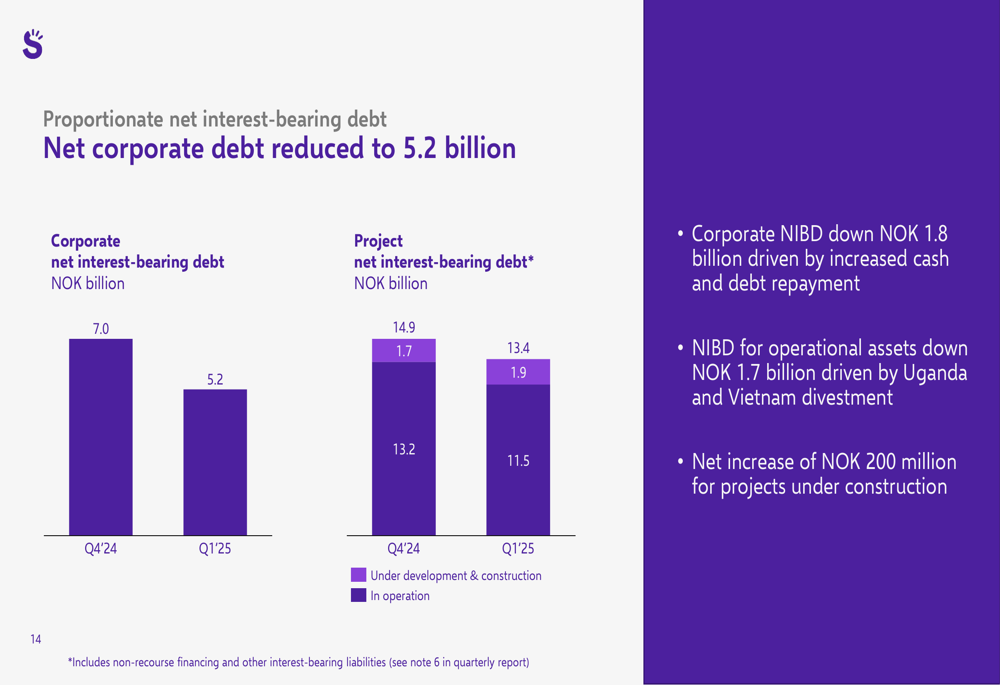

Scatec has also made significant progress in strengthening its balance sheet. Corporate net interest-bearing debt was reduced to NOK 5.2 billion in Q1 2025, down from NOK 7.0 billion at the end of 2024 and NOK 8.4 billion in Q2 2024. This represents a 38% reduction in corporate debt over the past three quarters.

The debt reduction is visualized in the following chart:

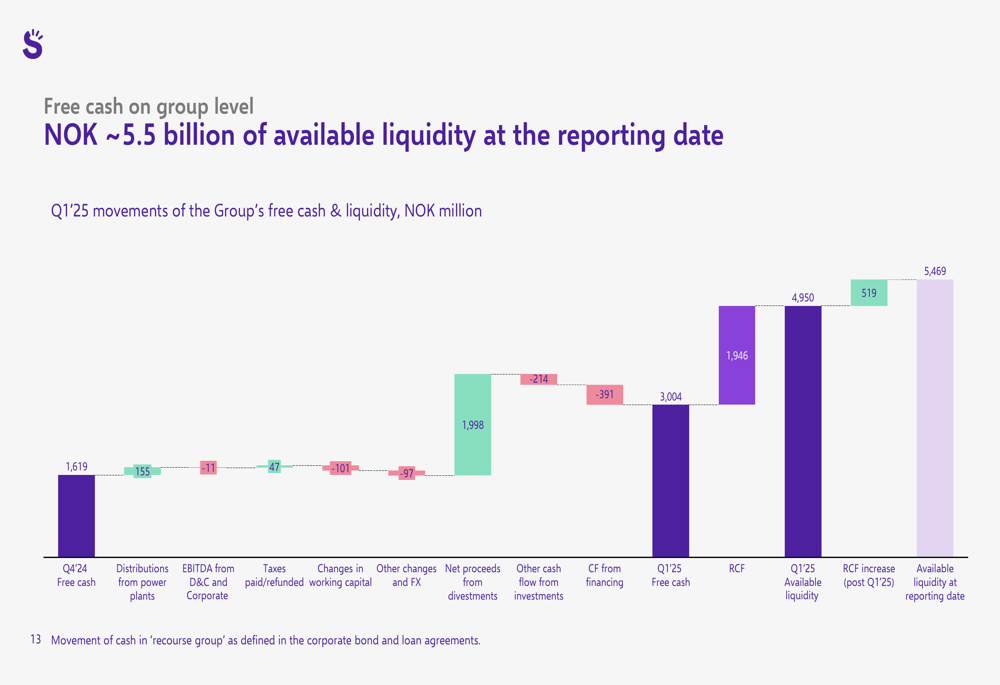

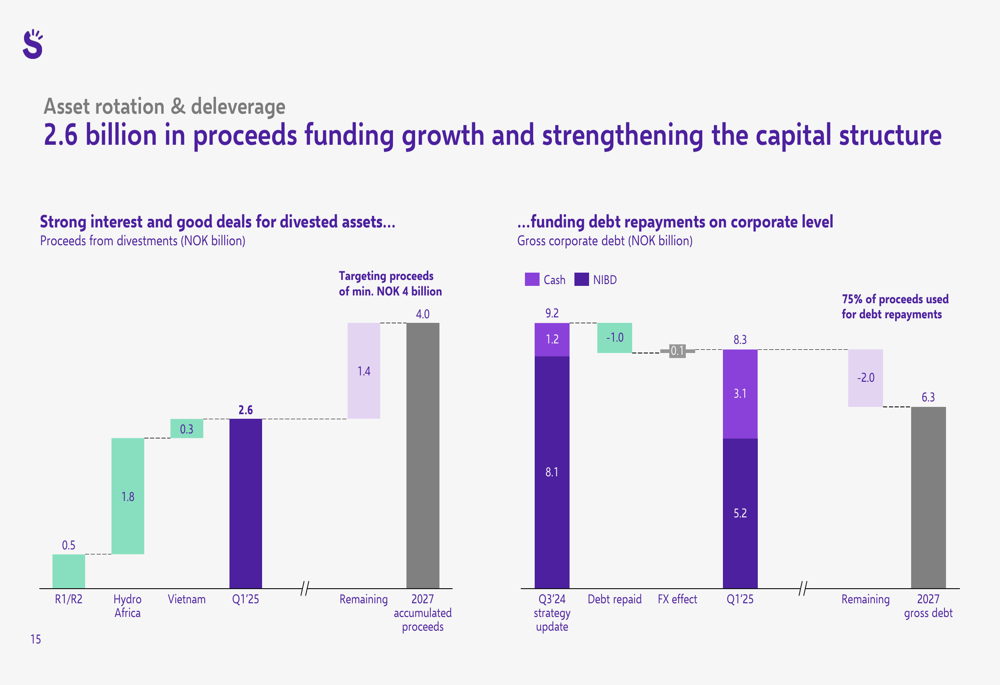

The company’s liquidity position has also improved substantially, with approximately NOK 5.5 billion of available liquidity at the reporting date. This increase was primarily driven by NOK 2.6 billion in proceeds from asset divestments, which are funding both growth initiatives and debt reduction.

As shown in the following cash flow breakdown:

Strategic Initiatives

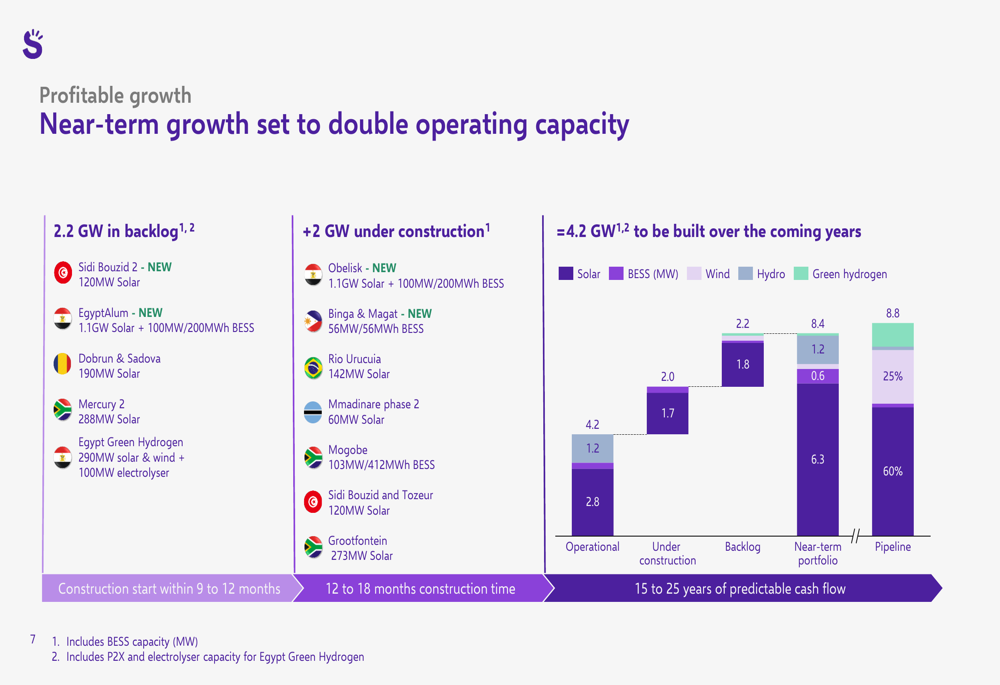

Scatec’s near-term growth strategy aims to double its operating capacity through a combination of projects under construction and backlog developments. The company currently has 2.2 GW of operational capacity, with 2.0 GW under construction and 4.2 GW in backlog.

The following chart illustrates Scatec’s growth portfolio:

Construction activity is robust, with 1,988 MW currently under development across multiple countries including South Africa, Tunisia, Botswana, Brazil, Philippines, and Egypt. These projects span solar, battery energy storage systems (BESS), and hybrid installations, with commercial operation dates ranging from H1 2025 to H2 2026.

The company’s asset rotation strategy has generated NOK 2.6 billion in proceeds to date, with a target of at least NOK 4 billion by 2027. These funds are being used to both finance growth and reduce corporate debt, as illustrated in the following chart:

Forward-Looking Statements

Looking ahead, Scatec provided guidance for full-year 2025, projecting power production of 4,100-4,500 GWh and EBITDA of NOK 4,150-4,450 million. For Q2 2025, the company expects power production of 900-1,000 GWh with Philippines EBITDA estimated at NOK 180-220 million.

The Development & Construction segment has a remaining contract value of NOK 6.7 billion, with estimated gross margins of 10-12% for projects under construction and in backlog. This segment is expected to generate negative EBITDA of NOK 115-125 million for FY 2025 as the company continues to invest in growth.

CFO Hans Jakob Hegge emphasized the company’s extended debt maturity profile, which now stretches to 2029 following the issuance of a new green bond of NOK 1,250 million. This restructuring provides Scatec with greater financial flexibility to execute its growth strategy while maintaining a strengthened balance sheet.

As Scatec continues its transition from a pure solar developer to a diversified renewable energy producer with solar, hydro, and battery storage assets, the company appears well-positioned to capitalize on global demand for clean energy infrastructure while delivering improved financial results for shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.