SoFi shares rise as record revenue, member growth drive strong Q3 results

Introduction & Market Context

Scatec Solar OL (OB:SCATC) reported strong Q2 2025 results on August 19, highlighting continued growth momentum across its renewable energy portfolio. The company’s stock closed at 103.2 NOK on August 18, up 3.46% ahead of the earnings presentation, and has been trading near its 52-week high of 106.6 NOK, reflecting positive market sentiment toward the company’s expansion strategy.

The renewable energy developer continues to strengthen its position in key markets while maintaining disciplined financial management, with CEO Terje Pilskog and CFO Hans Jakob Hegge emphasizing the company’s focus on sustainable growth and debt reduction.

Quarterly Performance Highlights

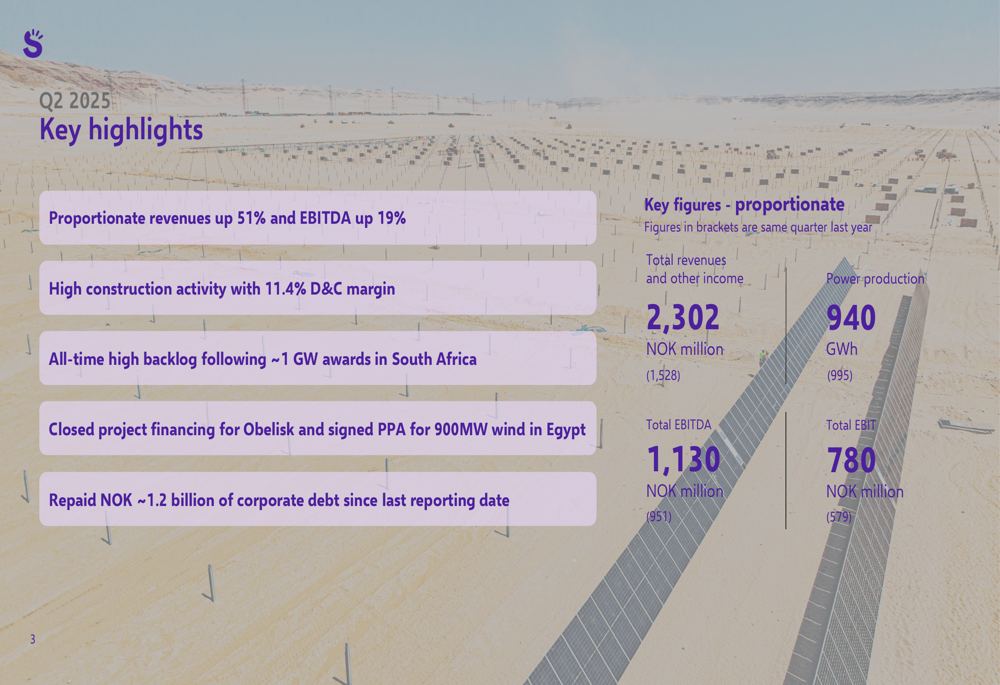

Scatec delivered impressive financial results in Q2 2025, with proportionate revenues increasing 51% year-over-year to NOK 2,302 million, while proportionate EBITDA grew 19% to NOK 1,130 million. The company’s EBIT also showed strong improvement, reaching NOK 780 million, up from NOK 579 million in the same quarter last year.

As shown in the following key highlights from the quarter:

Despite a slight decrease in power production to 940 GWh from 995 GWh in Q2 2024, revenue growth was substantial, primarily driven by strong performance in the Philippines and high construction activity. The company maintained a healthy 11.4% development and construction margin while continuing to expand its project pipeline.

Geographic Growth Drivers

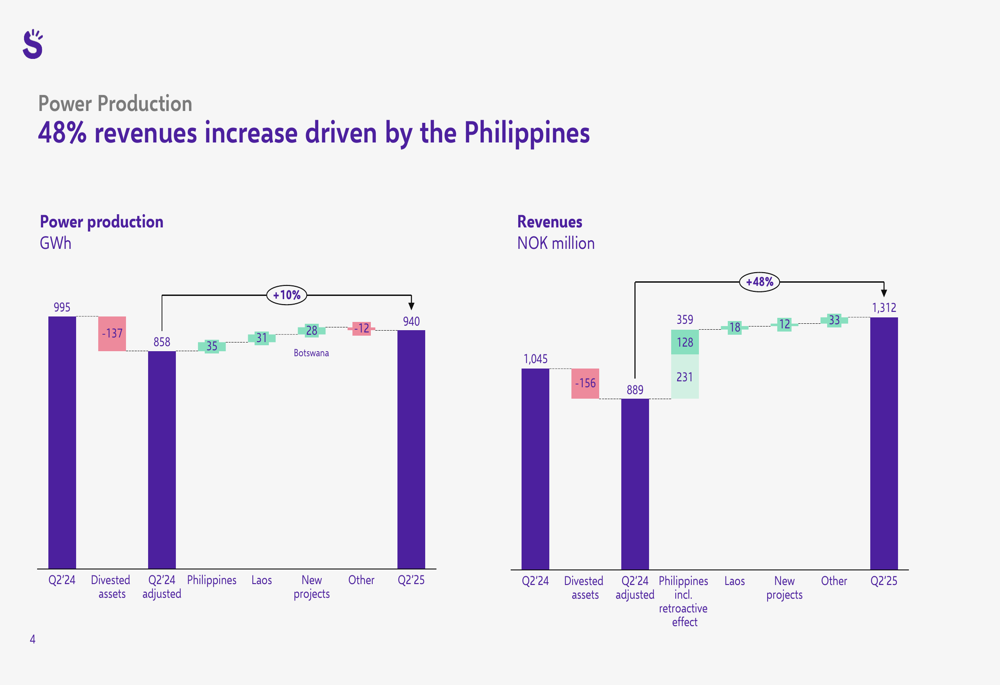

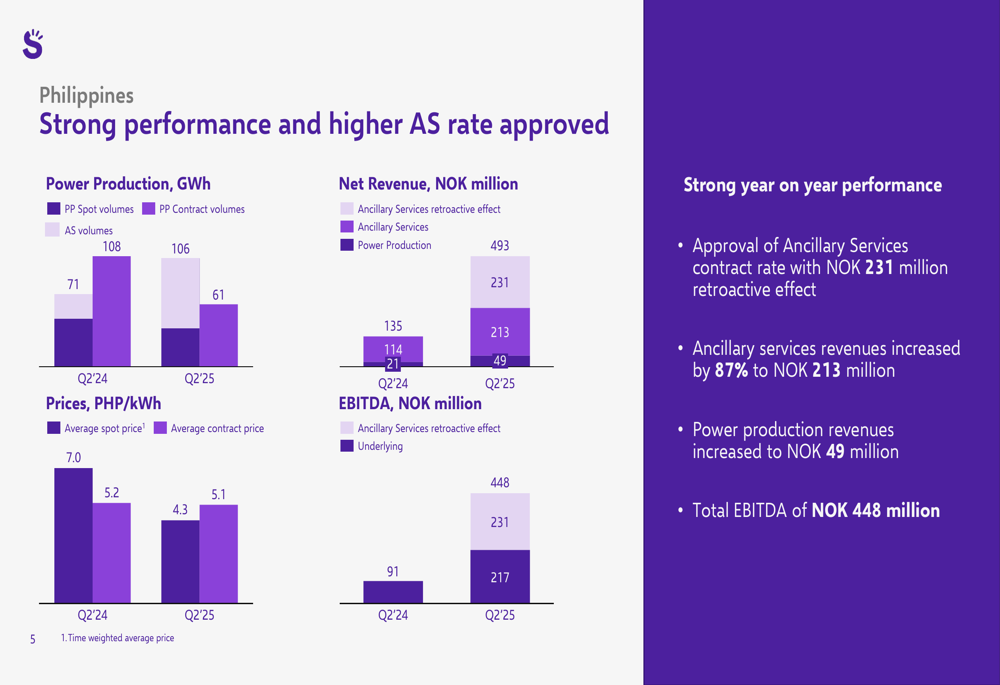

The Philippines emerged as a key growth driver for Scatec in Q2 2025, with revenues increasing by 48% year-over-year. This growth was primarily attributed to the approval of a higher Ancillary Services (AS) rate, which generated a NOK 231 million retroactive effect. Ancillary services revenues increased by 87% to NOK 213 million, while power production revenues rose to NOK 49 million.

The following chart illustrates the significant contribution of the Philippines to overall revenue growth:

A closer look at the Philippines operation reveals the substantial impact of the higher AS rate approval:

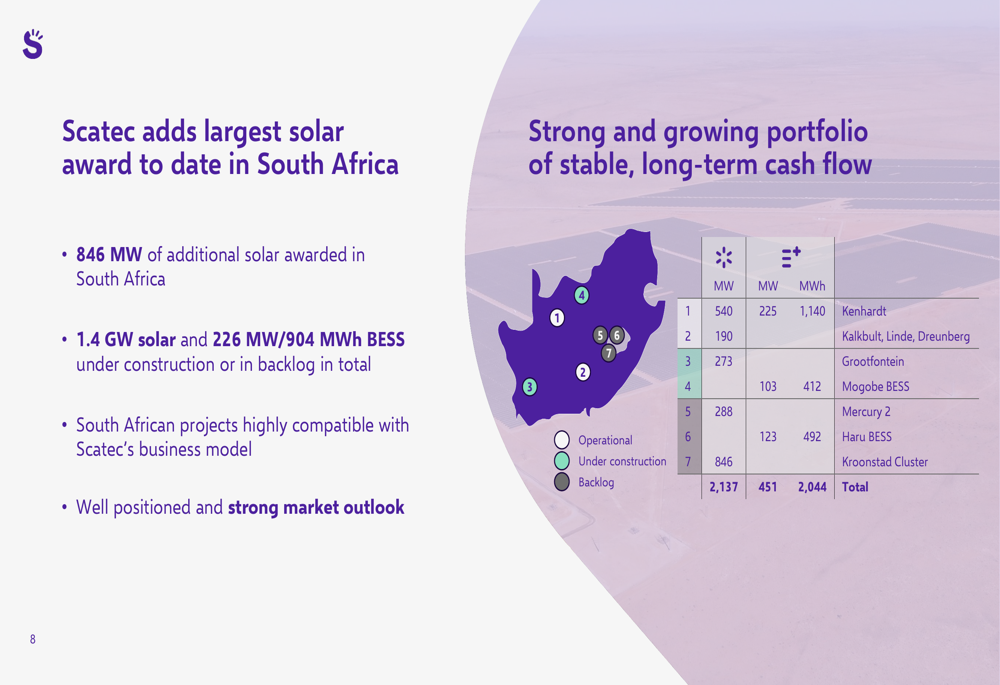

Meanwhile, Scatec significantly strengthened its position in South Africa, securing its largest solar award to date with 846 MW of additional capacity. The company now has 1.4 GW of solar and 226 MW/904 MWh of battery energy storage systems (BESS) either under construction or in backlog in South Africa, positioning it as a major player in the region’s renewable energy transition.

The following slide details Scatec’s expanding footprint in South Africa:

Construction and Project Pipeline

Scatec reported record construction activity with 1,979 MW currently under development across multiple countries. The company’s project portfolio includes solar installations in South Africa, Tunisia, Botswana, Brazil, and Egypt, as well as battery energy storage systems in the Philippines and South Africa.

The company’s construction portfolio is detailed below:

Beyond active construction, Scatec maintains a robust growth pipeline totaling 5.2 GW, with 3.2 GW in backlog and 2 GW under construction. This includes the recently awarded Kroonstad Cluster (846 MW solar) in South Africa and the Haru BESS project (123 MW/492 MWh), among others.

The company’s overall asset portfolio now includes 4,221 MW of operational capacity (with 50% economic interest) and 1,979 MW under construction (with 86% economic interest), along with a 7,700 MW project pipeline where Scatec maintains 100% ownership share.

Financial Position and Debt Reduction

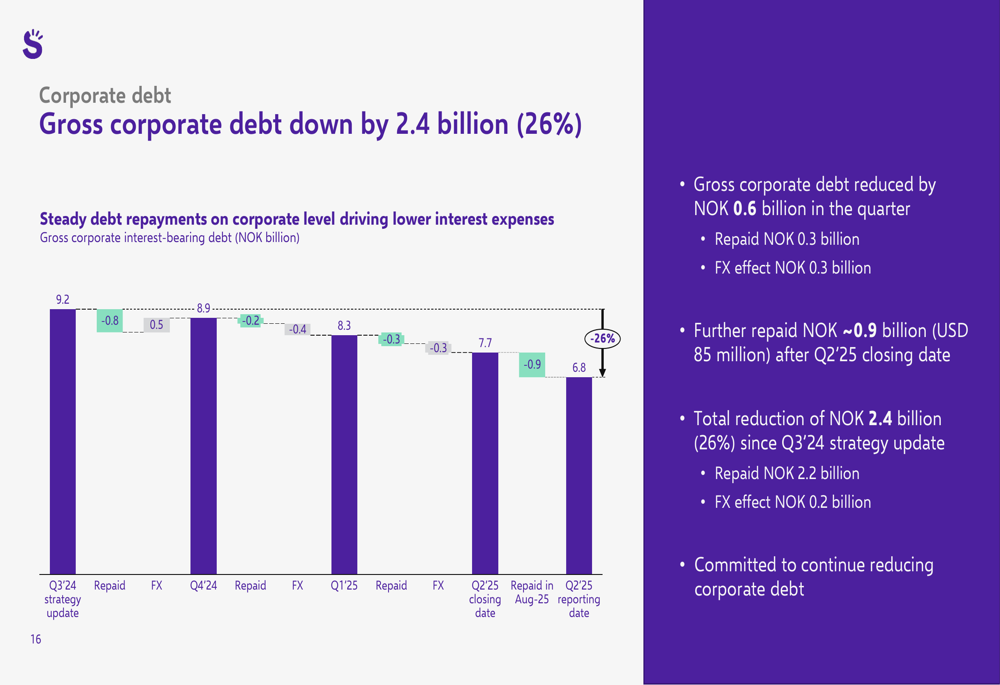

Scatec continues to strengthen its balance sheet, reducing gross corporate debt by NOK 2.4 billion (26%) since its Q3 2024 strategy update. In Q2 2025 alone, the company repaid NOK 0.3 billion and benefited from a favorable FX effect of NOK 0.3 billion. After the Q2 closing date, Scatec further repaid approximately NOK 0.9 billion (USD 85 million).

The company’s debt reduction progress is illustrated in the following chart:

Despite significant investments in construction activities, Scatec maintained a strong liquidity position of NOK 4.4 billion, including NOK 2 billion in free cash and NOK 2.4 billion in undrawn revolving credit facilities. This financial flexibility supports the company’s ambitious growth plans while ensuring operational stability.

Forward Outlook

Looking ahead, Scatec provided guidance for full-year 2025, projecting power production of 4,000-4,300 GWh and EBITDA of NOK 4,150-4,450 million. For Q3 2025, the company expects power production of 1,100-1,200 GWh, with Philippines EBITDA estimated at NOK 280-380 million.

The Development & Construction segment maintains a remaining contract value of NOK 6.0 billion with estimated gross margins of 10-12% for projects under construction. Corporate EBITDA for FY 2025 is projected at NOK -115 to -125 million.

Management emphasized three key takeaways from the quarter: strong financial performance, continued growth momentum, and an ongoing commitment to reducing corporate debt. These strategic priorities align with Scatec’s long-term vision of expanding its renewable energy portfolio while maintaining financial discipline.

As renewable energy continues to gain traction globally, Scatec appears well-positioned to capitalize on growing demand across its diverse geographic footprint, with particularly strong momentum in the Philippines and South Africa markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.