Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

Scholastic Corporation (NASDAQ:SCHL) presented its first quarter fiscal 2026 results on Thursday, September 18, 2025, reporting a quarterly loss that aligns with the company’s typical seasonal pattern. The children’s publishing and education company saw its stock rise 4.37% in aftermarket trading to $28.40, following a 1.62% gain during regular trading hours.

The first quarter traditionally represents Scholastic’s weakest period due to the summer break in the school calendar, with the company typically generating losses before rebounding in subsequent quarters. Despite a 5% year-over-year revenue decline, management maintained its full-year guidance, signaling confidence in the company’s ability to deliver on its annual targets.

Quarterly Performance Highlights

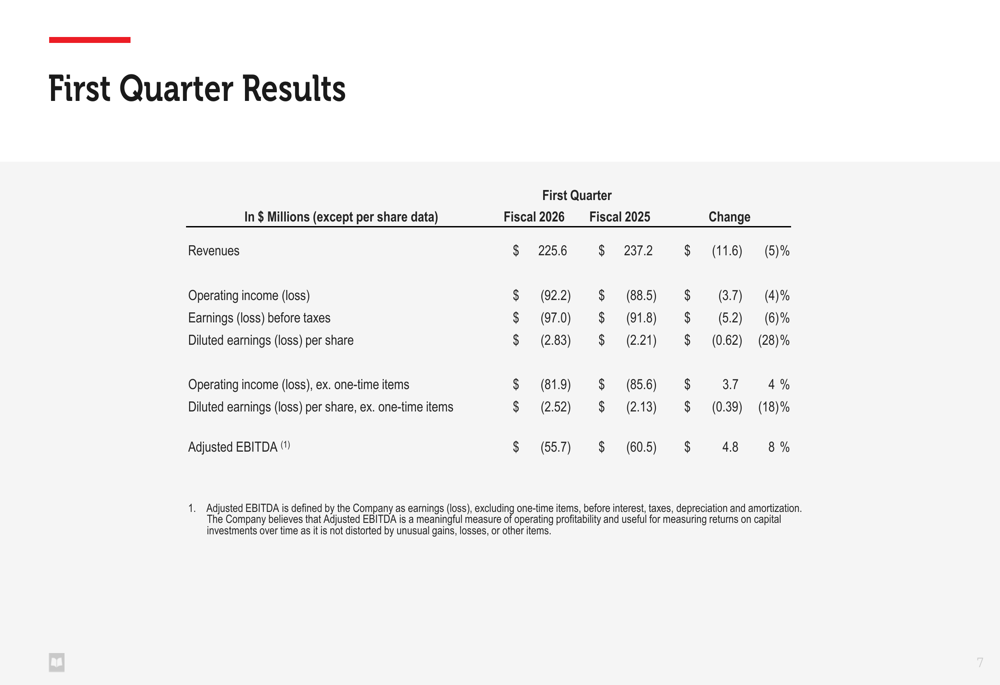

Scholastic reported first quarter revenues of $225.6 million, down 5% from $237.2 million in the same period last year. The company posted an operating loss of $92.2 million, slightly worse than the $88.5 million loss recorded in Q1 2025. However, adjusted EBITDA improved by 8% to $(55.7) million from $(60.5) million in the prior year, suggesting progress in the company’s cost control initiatives.

As shown in the following comprehensive financial results table:

Diluted loss per share increased to $(2.83) from $(2.21) in the prior-year period, representing a 28% decline. However, when excluding one-time items, the adjusted loss per share was $(2.52), compared to $(2.13) in the first quarter of fiscal 2025.

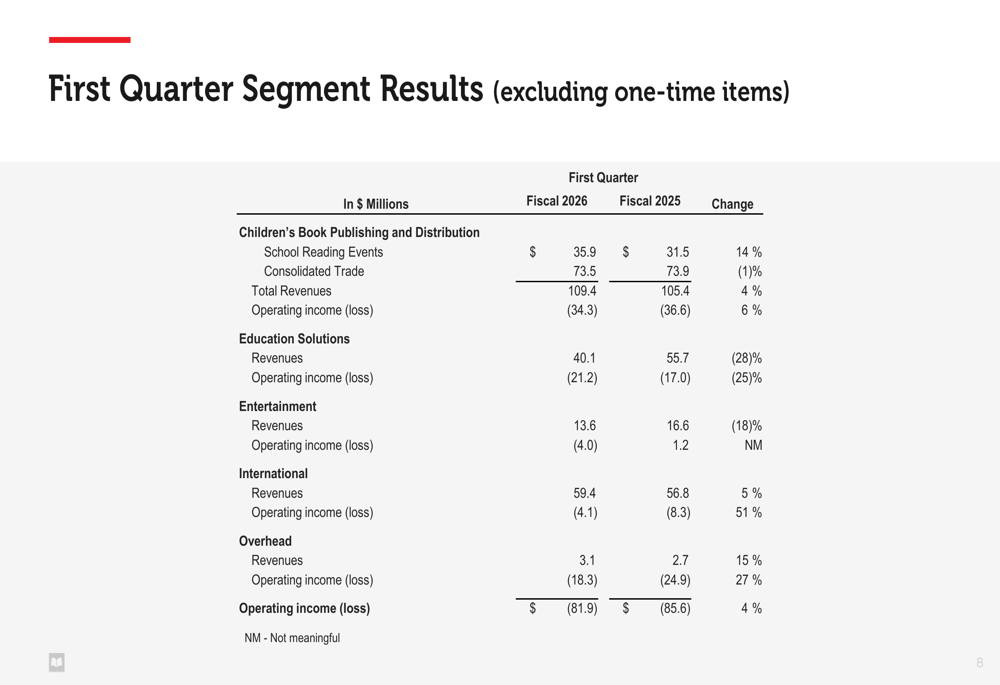

Performance across Scholastic’s business segments showed mixed results, with two segments growing while two others faced challenges:

The Children’s Book Publishing and Distribution segment, Scholastic’s largest revenue generator, showed resilience with a 4% revenue increase to $109.4 million, driven by a strong 14% growth in School Reading Events. The International segment also performed well, with revenues up 5% to $59.4 million and a significantly improved operating loss that narrowed by 51%.

Conversely, the Education Solutions segment faced substantial headwinds, with revenues declining 28% to $40.1 million amid what the company described as a "volatile funding environment." The Entertainment segment also struggled, with revenues falling 18% to $13.6 million.

Detailed Financial Analysis

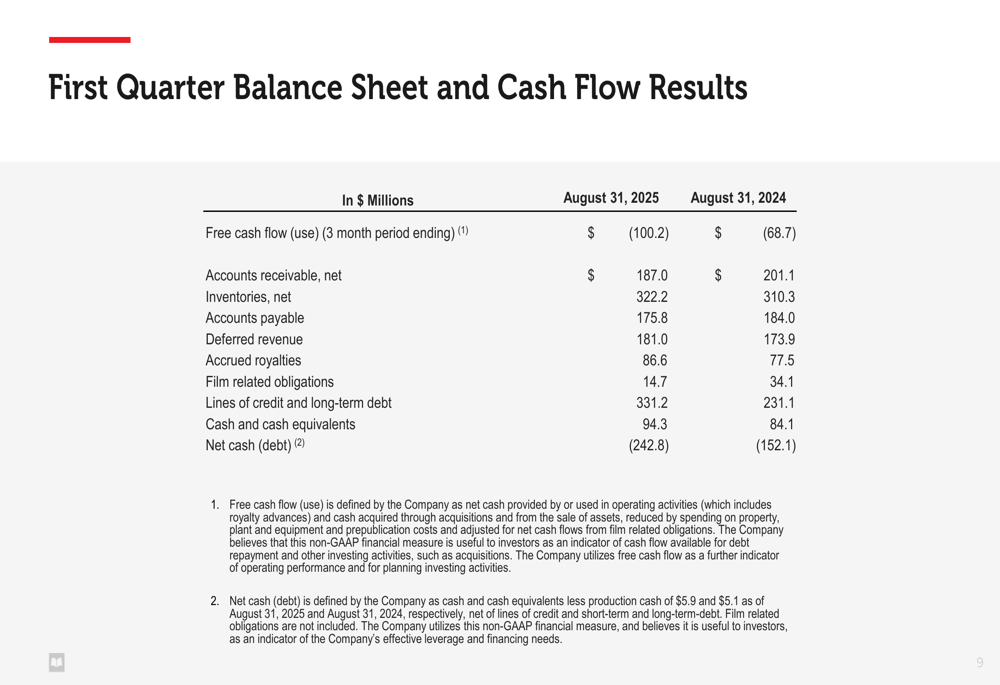

Scholastic’s balance sheet showed some concerning trends, particularly regarding cash flow and debt levels. Free cash flow usage increased to $(100.2) million compared to $(68.7) million in the prior-year period. Net debt position worsened significantly to $(242.8) million from $(152.1) million a year earlier, reflecting increased borrowing and ongoing operational cash needs during the seasonally weak quarter.

The following table provides a detailed look at the company’s balance sheet and cash flow metrics:

Inventory levels increased year-over-year, rising to $322.2 million from $310.3 million, potentially indicating preparation for anticipated higher sales in coming quarters. Meanwhile, accounts receivable decreased to $187.0 million from $201.1 million in the prior year.

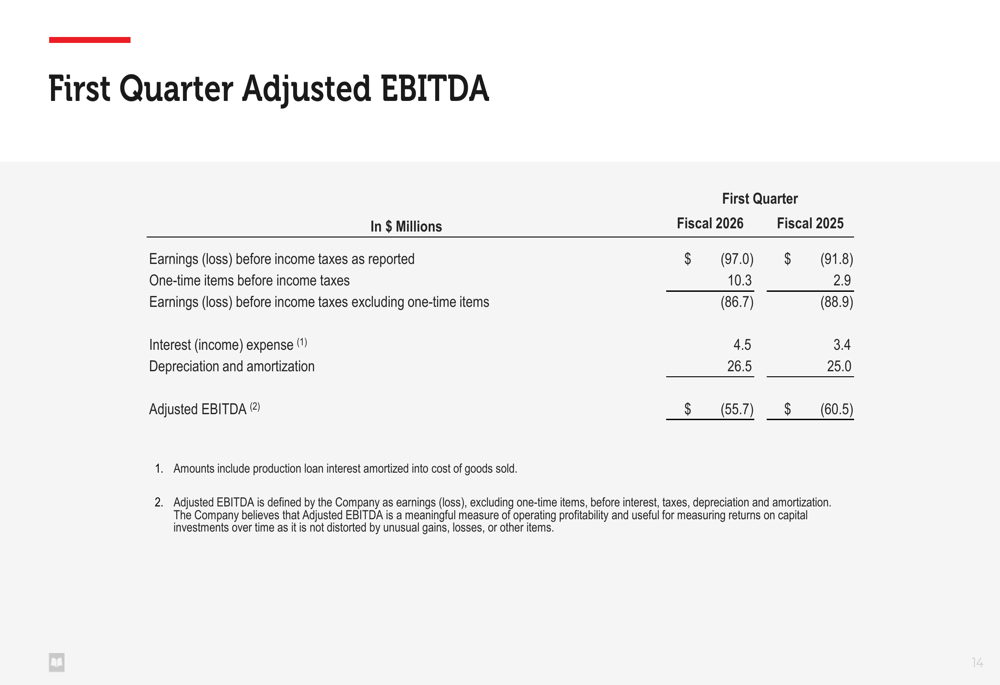

The company’s Adjusted EBITDA calculation shows the impact of one-time items and provides insight into the underlying operational performance:

This reconciliation reveals that despite the reported loss increasing year-over-year, the company’s core operations actually showed improvement when excluding one-time charges of $10.3 million in the current quarter compared to $2.9 million in the prior-year period.

Strategic Initiatives

During the presentation, CEO Peter Warwick highlighted several strategic priorities for fiscal 2026, including progress on real estate monetization efforts and a continued focus on financial discipline. These initiatives align with statements made during the previous quarter’s earnings call, where management emphasized cost-saving strategies targeting non-revenue generating functions.

The company’s international segment results "reflected continued portfolio rationalization," suggesting ongoing efforts to streamline operations and focus on more profitable markets. This approach appears to be yielding results, as evidenced by the 51% improvement in the segment’s operating loss despite modest revenue growth.

In the Entertainment segment, Scholastic positioned itself for "renewed growth" following what appears to be a transitional period. The company mentioned the integration of YouTube channels as part of its strategy in this area, indicating efforts to expand its digital presence and reach younger audiences through contemporary platforms.

Forward-Looking Statements

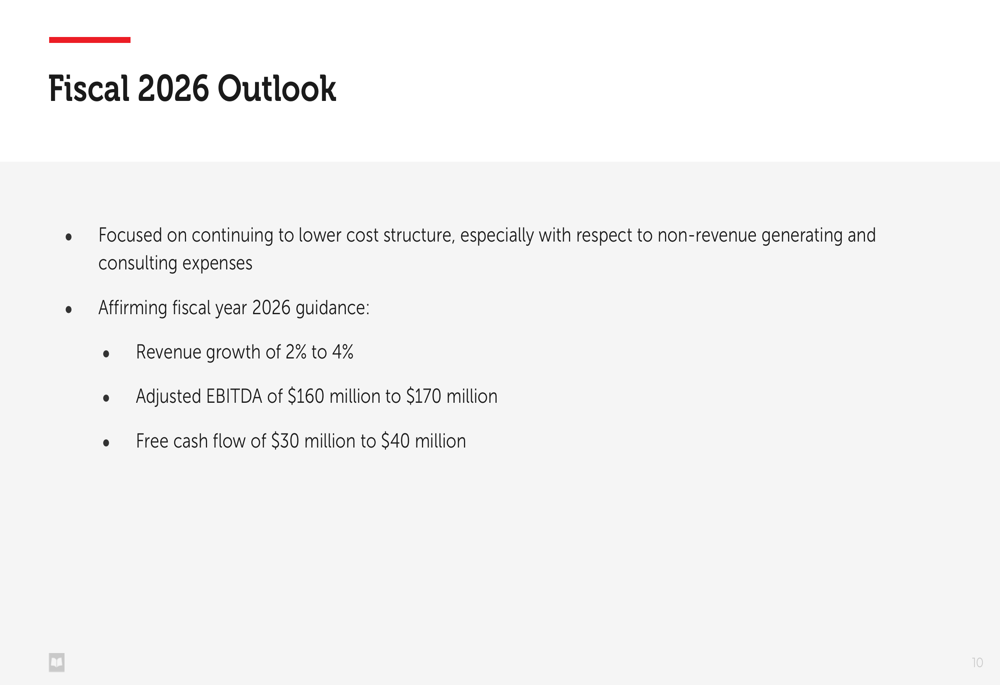

Despite the seasonal first-quarter loss, Scholastic reaffirmed its full-year fiscal 2026 guidance, projecting:

The company’s revenue growth target of 2-4% and Adjusted EBITDA range of $160-170 million remain unchanged from the guidance provided in the previous quarter. This consistency suggests management remains confident in the company’s ability to overcome the challenges faced in the Education Solutions segment and capitalize on strengths in Children’s Book Publishing and International markets.

The projected free cash flow of $30-40 million would represent a significant improvement from the current quarter’s cash usage, reflecting the highly seasonal nature of Scholastic’s business model.

Management emphasized its focus on "continuing to lower cost structure," indicating that operational efficiency remains a priority. This approach aligns with statements from the previous quarter’s earnings call, where CFO Haji Glover noted that cost-saving actions would "more than offset the impact of current tariffs and inflation."

As Scholastic moves into its traditionally stronger quarters, investors will be watching closely to see if the company can deliver on its full-year promises despite the mixed start to the fiscal year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.