TSX gains after CPI shows US inflation rose 3%

Introduction & Market Context

Sensata Technologies (NYSE:ST) reported its second quarter 2025 financial results on July 29, 2025, demonstrating operational resilience despite ongoing market challenges. The sensor and control solutions provider faced headwinds in key markets, particularly in heavy vehicle and off-road segments, while showing strength in its Sensing Solutions business.

The company operates in a challenging global environment with flat automotive production year-over-year, North America truck production down 24%, and industrial markets showing only early signs of stabilization. Despite these headwinds, Sensata managed to exceed its financial guidance across key metrics.

Quarterly Performance Highlights

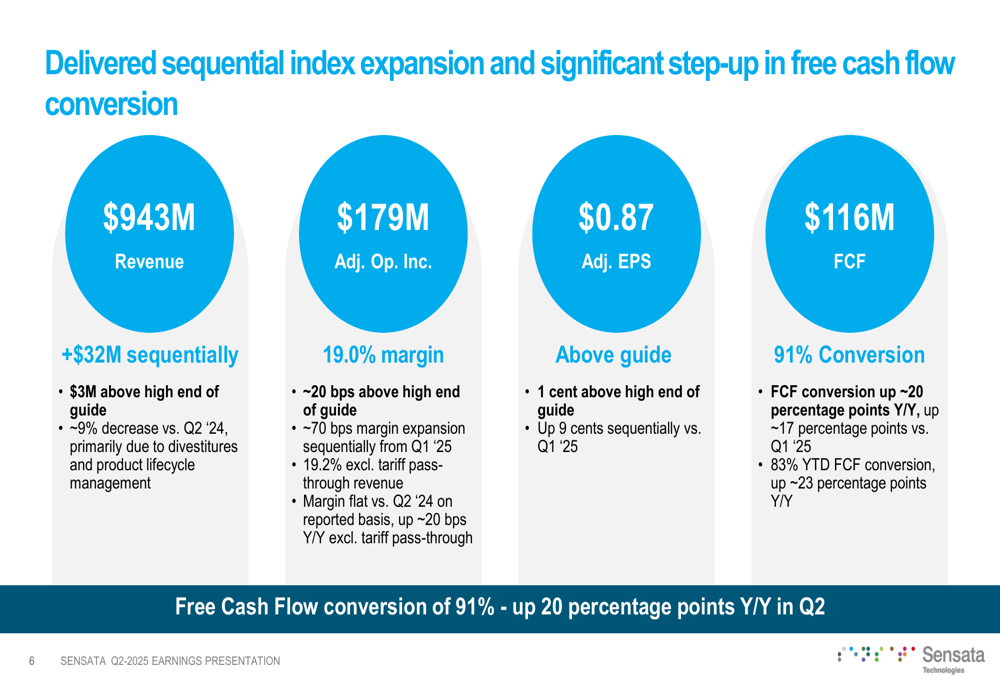

Sensata reported Q2 2025 revenue of $943 million, representing a 9% year-over-year decline but a $32 million sequential improvement from Q1. The company exceeded expectations across its key financial metrics, with adjusted operating income of $179 million (19.0% margin) and adjusted earnings per share of $0.87, both above the high end of guidance.

As shown in the following financial results summary:

Free cash flow performance was particularly strong at $116 million with a 91% conversion rate, representing an improvement of approximately 20 percentage points year-over-year and 17 percentage points sequentially. This cash generation strength reflects the company’s operational discipline and working capital management.

CEO Stephan von Schuckmann highlighted the company’s progress: "Our back-to-basics approach continues to deliver. We are building resiliency in our business and we are pleased to report a strong second quarter where we exceeded our revenue and earnings commitments and significantly improved our free cash flow."

Segment Performance

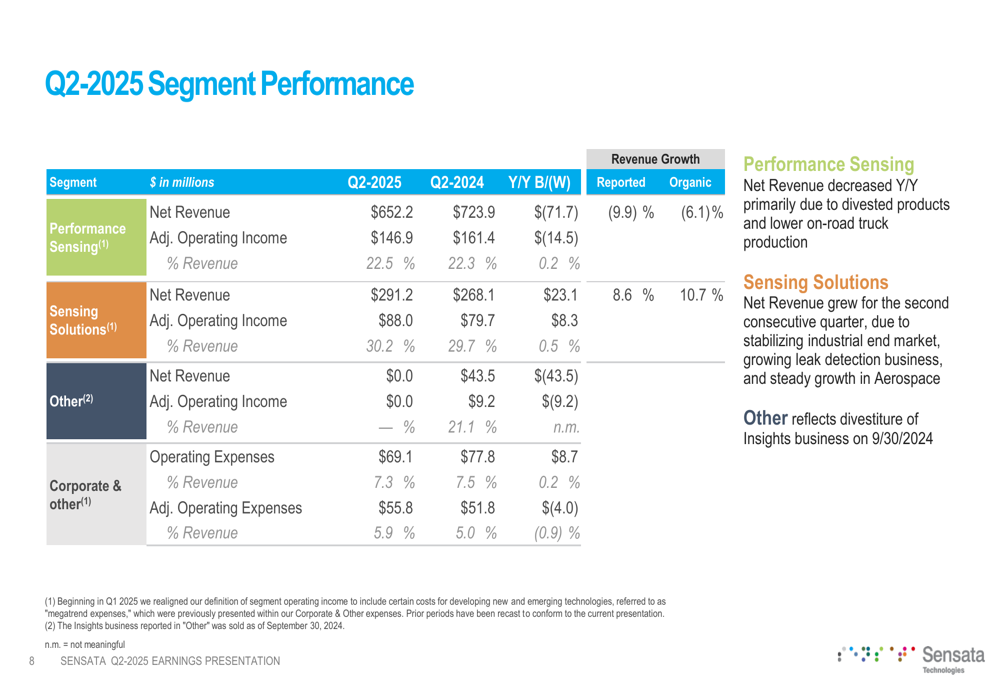

Sensata’s business segments showed divergent performance in Q2 2025. The Performance Sensing segment, which represents approximately 69% of total revenue, experienced a 9.9% year-over-year decline to $652.2 million. This decline was primarily attributed to divested products and lower on-road truck production.

In contrast, the Sensing Solutions segment delivered its second consecutive quarter of strong growth, with revenue increasing 8.6% year-over-year to $291.2 million. This growth was bolstered by new products ramping up production.

The detailed segment breakdown reveals the contrasting performance:

Despite the revenue decline in Performance Sensing, the segment maintained a healthy adjusted operating margin of 22.5%, slightly improving from 22.3% in the prior year. Similarly, Sensing Solutions improved its margin to 30.2% from 29.7%, demonstrating the company’s ability to maintain profitability even in challenging market conditions.

Capital Allocation and Balance Sheet Strength

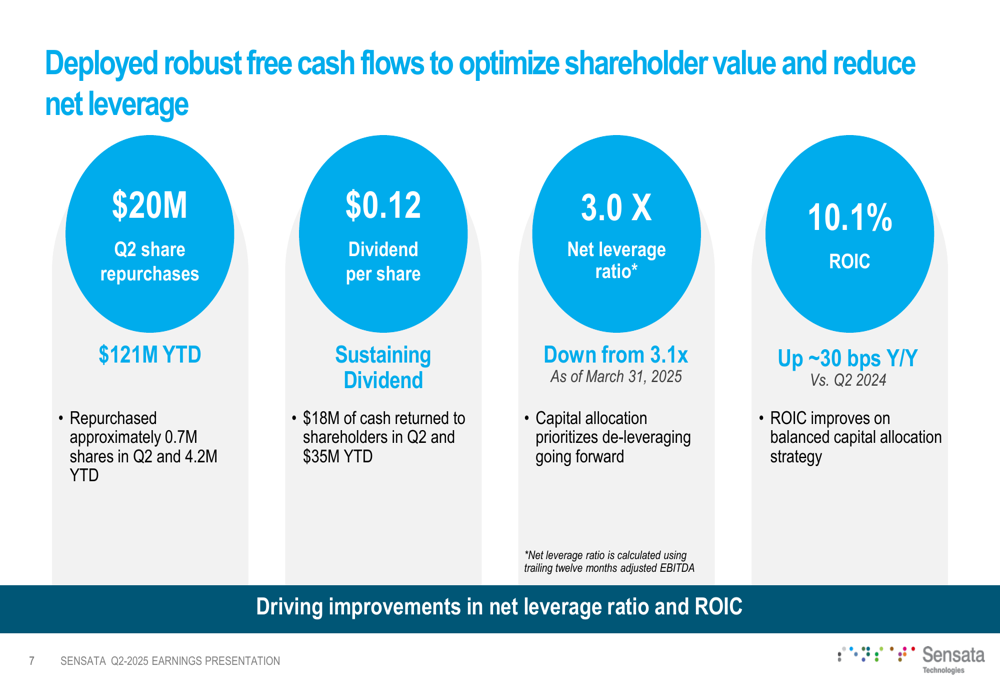

Sensata continued to balance shareholder returns with debt reduction in its capital allocation strategy. During Q2, the company repurchased $20 million worth of shares (approximately 0.7 million shares) and paid a $0.12 per share dividend, returning a total of $18 million to shareholders.

The company’s net leverage ratio improved to 3.0x from 3.1x as of March 31, 2025, reflecting its commitment to deleveraging. Return on invested capital (ROIC) also improved to 10.1%, up approximately 30 basis points year-over-year.

Global Footprint and Tariff Strategy

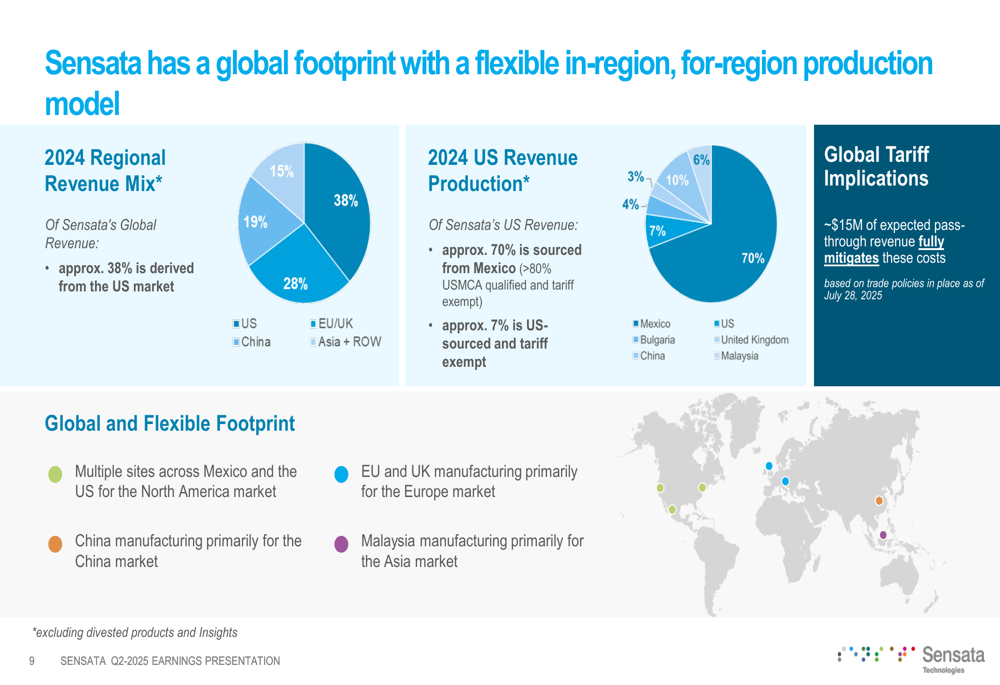

Sensata’s global manufacturing footprint provides strategic advantages in navigating trade policies and tariffs. The company derives approximately 38% of its global revenue from China, 19% from the US, 15% from EU/UK, and 28% from Asia and the rest of the world.

For its US revenue, approximately 70% is sourced from Mexico, with over 80% qualifying for USMCA tariff exemptions. This positioning helps mitigate the impact of tariffs, with the company expecting approximately $15 million of pass-through revenue to fully offset tariff costs based on trade policies in place as of July 28, 2025.

The following chart illustrates Sensata’s global manufacturing strategy:

Forward-Looking Statements

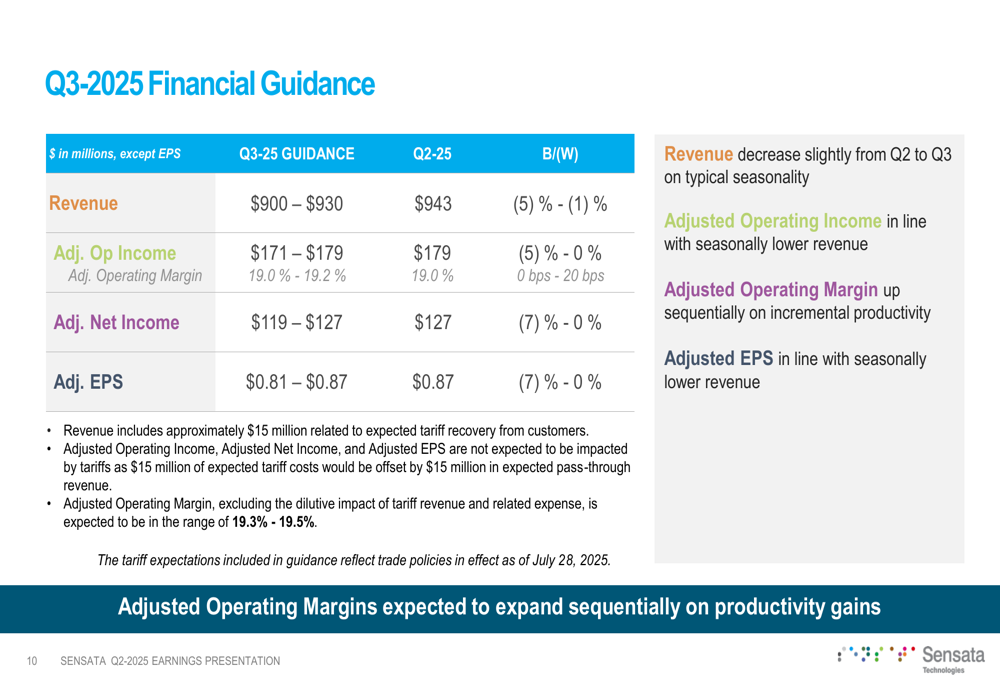

Looking ahead to Q3 2025, Sensata provided guidance for revenue between $900 million and $930 million, representing a sequential decline of 1-5% from Q2 due to typical seasonality. Adjusted operating income is expected to be between $171 million and $179 million, with adjusted operating margin improving slightly to 19.0-19.2%.

Adjusted earnings per share guidance for Q3 2025 is set at $0.81-$0.87, consistent with the seasonally lower revenue expectations.

The company noted that its guidance includes approximately $15 million related to expected tariff recovery from customers, reflecting trade policies in effect as of July 28, 2025. Despite the challenging market environment, Sensata expects to maintain margin stability through productivity improvements.

End Market Outlook

Sensata provided insights into its key end markets, with mixed outlooks across segments. In automotive, S&P estimates global production to be approximately flat year-over-year, with the first half up low single digits, Q3 flat, and Q4 down mid-single digits. North America and Europe markets are projected to decline 3-4% in 2025, offset by growth in China.

The heavy vehicle and off-road (HVOR) market faces more significant challenges, with North America truck production down 24% year-over-year. European on-road markets are expected to stabilize in the second half after a weak first half, while global off-road markets are projected to decline 2% for the full year after growing in the first half.

In the industrial sector, Sensata sees early signs of stabilization but maintains a cautious outlook due to the slow housing market and potential tariff escalation. The aerospace segment continues to show strength, with commercial and defense markets growing at low to mid-single digits, supported by strong backlogs at key customers.

Conclusion

Sensata’s Q2 2025 results demonstrate the company’s operational resilience in a challenging market environment. Despite the 9% year-over-year revenue decline, the company exceeded financial expectations, delivered strong free cash flow, and maintained healthy margins. The divergent performance between segments highlights both challenges and opportunities, with Sensing Solutions showing promising growth momentum.

The company’s strategic global footprint positions it well to navigate trade complexities, while its focus on productivity and operational efficiency supports margin stability. As Sensata continues its "back-to-basics" approach, investors will be watching for continued execution against guidance and progress in growing its higher-margin Sensing Solutions business in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.