Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

SGS SA (SIX:SGSN) presented its H1 2025 results on July 25, 2025, revealing solid organic growth across all business lines and announcing a major acquisition to accelerate its North American expansion strategy. The testing, inspection, and certification giant reported 5.3% organic sales growth, with adjusted operating income margin improving by 80 basis points to 14.9%.

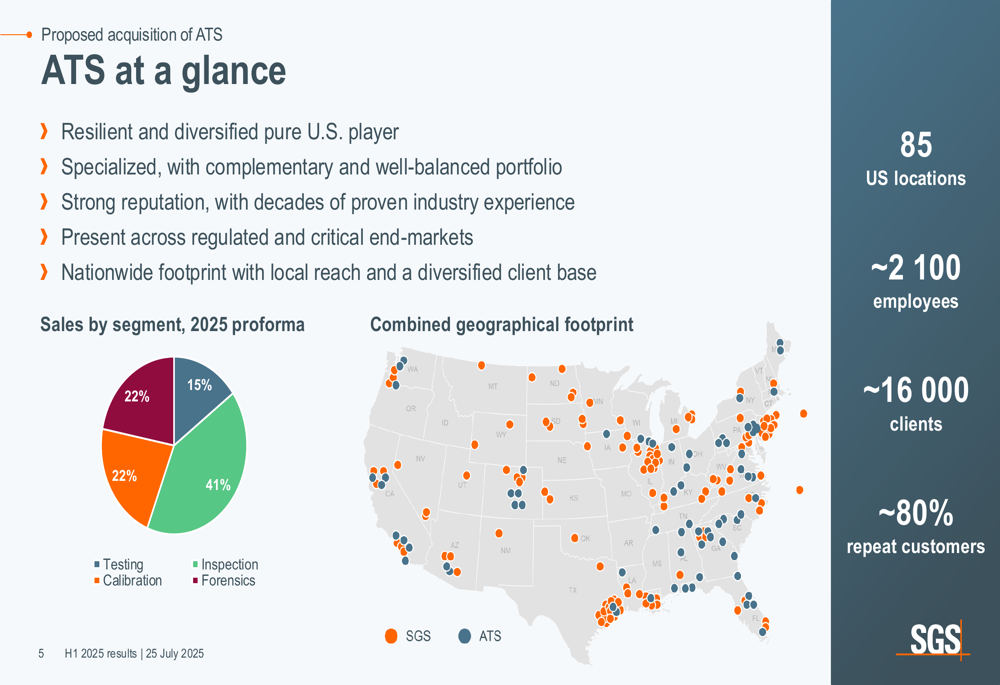

The most significant announcement was SGS’s planned acquisition of Applied Technical Services (ATS), a specialized U.S. testing and inspection provider, for USD 1.325 billion. This strategic move will nearly double SGS’s North American sales compared to 2023 levels.

CEO Géraldine Picaud emphasized that the company is on track to meet its full-year guidance, with strong performance in sustainability services and digital trust sectors driving growth.

Quarterly Performance Highlights

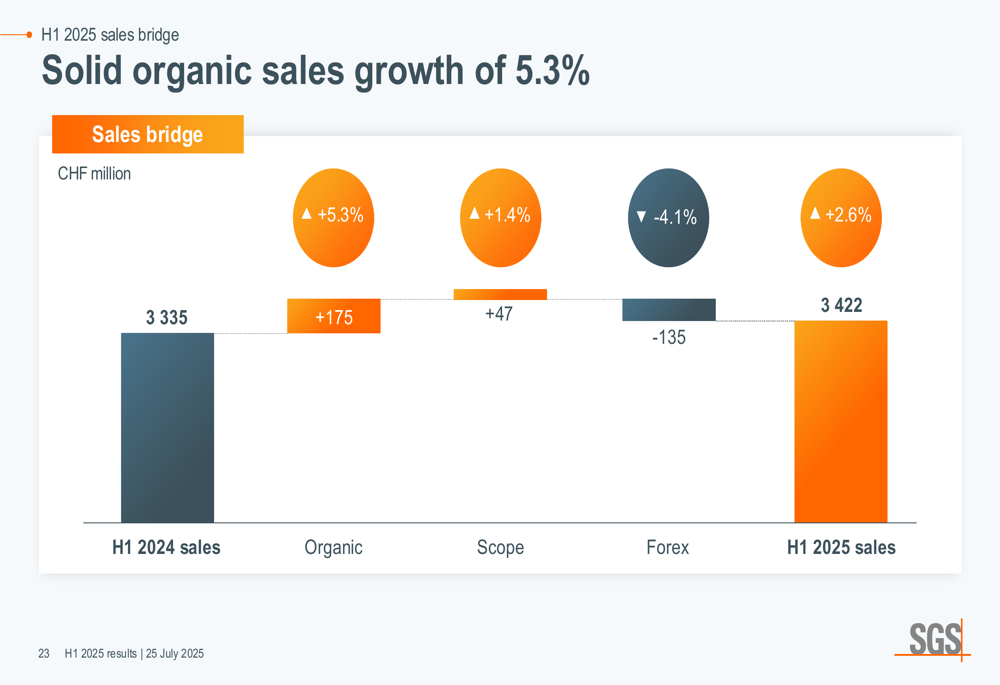

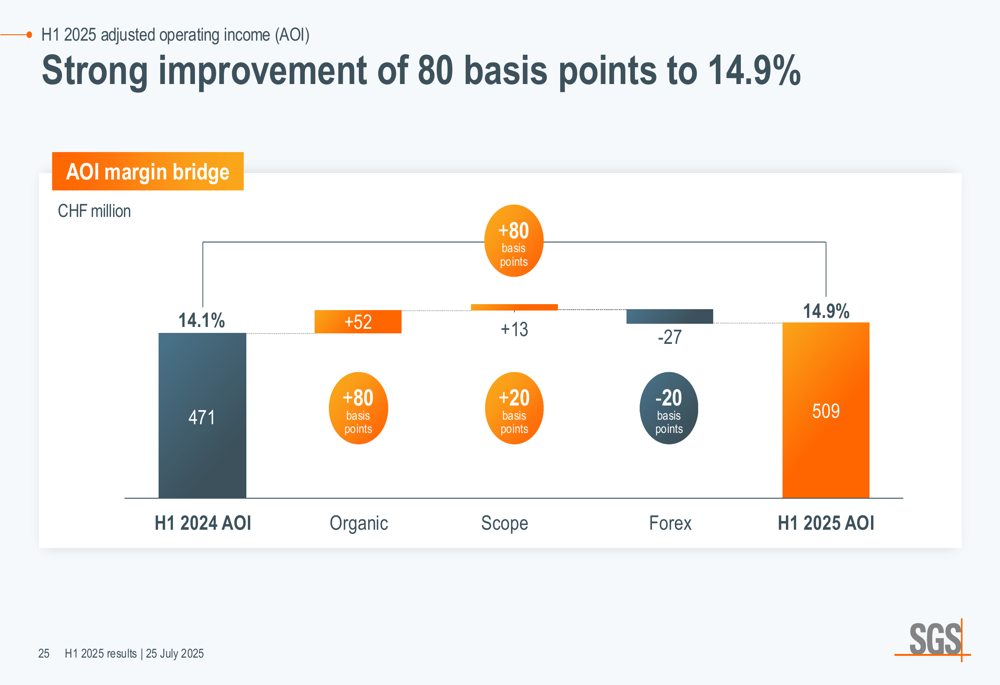

SGS reported H1 2025 sales of CHF 3,422 million, representing a 2.6% increase on a reported basis and 5.3% organic growth. The company achieved an adjusted operating income of CHF 509 million, with margin improvement to 14.9% from 14.1% in the prior year period.

As shown in the following sales bridge chart, organic growth contributed CHF 175 million, while acquisitions added CHF 47 million. However, negative currency effects of CHF 135 million partially offset these gains:

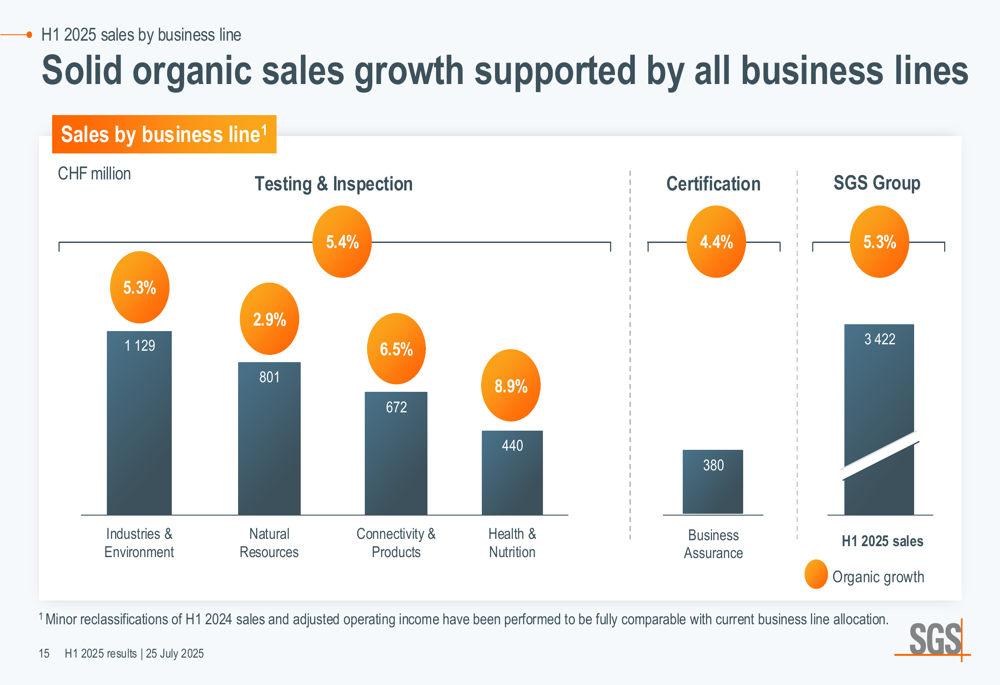

All business lines delivered positive organic growth, with Health & Nutrition leading at 8.9%, followed by Connectivity & Products at 6.5%. Industries & Environment and Business Assurance grew at 5.3% and 4.4% respectively, while Natural Resources showed more modest growth at 2.9%.

The following chart illustrates the solid organic sales growth across all business lines:

Geographically, Latin America led with 13.4% organic growth, followed by Eastern Europe, Middle East & Africa at 8.4%, and Asia Pacific at 6.5%. North America grew by 4.7%, while Europe showed the slowest growth at 1.1%.

Strategic Initiatives

The centerpiece of SGS’s strategic announcements was the proposed acquisition of Applied Technical Services (ATS), a specialized provider of testing, inspection, calibration, and forensics solutions in North America. With expected 2026 sales of USD 460 million and EBITDA of USD 95 million, ATS represents a significant expansion of SGS’s U.S. presence.

The following slide provides a snapshot of ATS’s operations and geographical footprint:

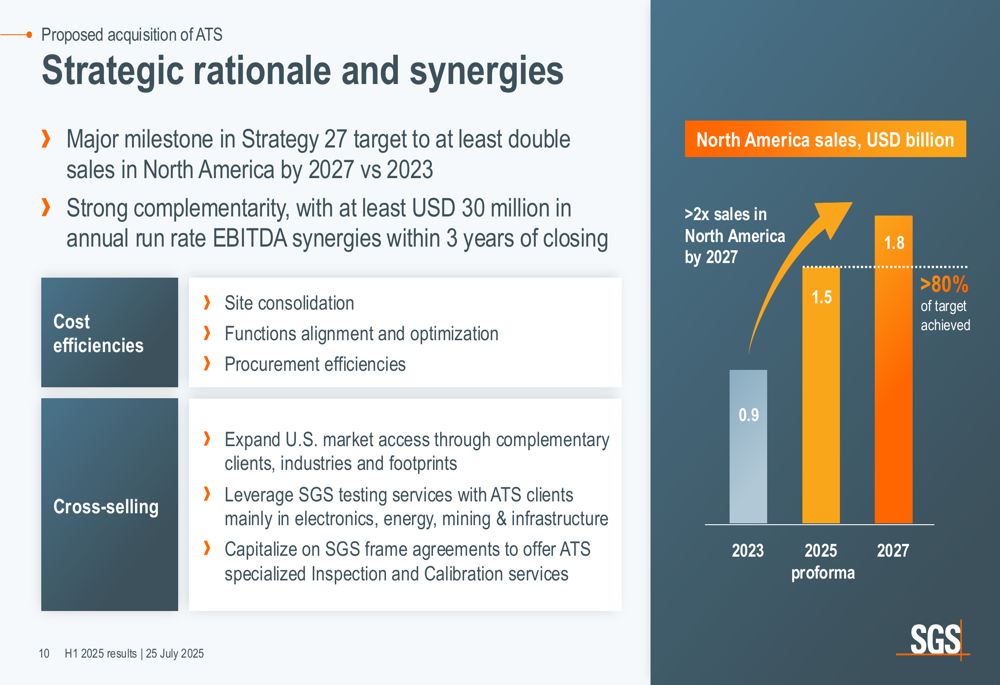

The acquisition, valued at USD 1.325 billion (representing 11.2x 2026 EBITDA including synergies), will be primarily financed through cash and debt. SGS expects to realize EBITDA synergies of at least USD 30 million annually within three years of closing through cost efficiencies and cross-selling opportunities.

This acquisition represents a major milestone in SGS’s Strategy 27, which targets at least doubling North American sales by 2027 compared to 2023 levels. As illustrated in the following chart, the ATS acquisition will achieve more than 80% of this target:

Beyond the ATS acquisition, SGS has been active in smaller bolt-on acquisitions, announcing 12 deals in 2025 representing total annual sales of more than CHF 90 million. The company also reported strong growth in its strategic focus areas, with sustainability services up 19% and digital trust services up 20% compared to H1 2024.

Efficiency Plans and Margin Improvement

SGS’s adjusted operating income margin improved by 80 basis points to 14.9%, driven by organic growth and efficiency initiatives. The following margin bridge illustrates the key contributors to this improvement:

The company’s efficiency plans are progressing well, with CHF 46 million in savings realized in H1 2025. These savings come from two main initiatives: a leaner operating model (CHF 100 million target) and procurement optimization (CHF 50 million target). The leaner operating model has been fully executed as of H1 2025, while 70% of procurement savings have been secured.

SGS expects to fully implement its CHF 150 million efficiency plan by the end of 2025, with CHF 96 million in total savings expected by 2026.

Financial Analysis

SGS reported earnings per share of CHF 1.64, a 13.9% increase from CHF 1.44 in H1 2024. Net profit attributable to shareholders rose to CHF 314 million from CHF 267 million in the prior year period.

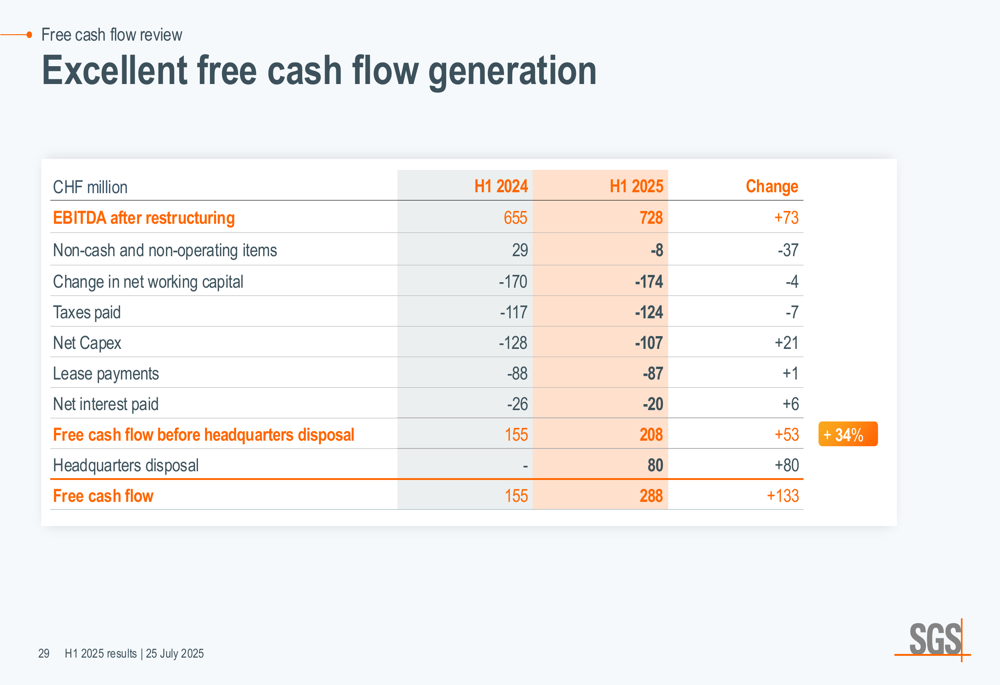

The company demonstrated excellent free cash flow generation, with free cash flow excluding headquarters disposal increasing by 34% to CHF 208 million. Including the CHF 80 million headquarters disposal, total free cash flow reached CHF 288 million.

The following table provides a detailed breakdown of the free cash flow components:

The company’s financial performance was negatively impacted by currency effects, with the Swiss franc appreciation reducing reported sales by 4.1% and adjusted operating income by 5.7%.

Forward-Looking Statements

SGS confirmed its outlook for 2025, projecting:

- 5% to 7% organic sales growth

- 1% to 2% bolt-on contribution to annual sales growth

- At least 30 basis points improvement in adjusted operating income margin on sales

- Strong free cash flow generation

The ATS acquisition is expected to close by late 2025 or early 2026, subject to customary closing conditions. The transaction will be EPS accretive from year one and is expected to enhance SGS’s organic growth and margin profile.

Looking ahead, SGS will continue to focus on its Strategy 27 initiatives, with particular emphasis on sustainability services, digital trust, and expanding its North American presence. The company’s financial calendar indicates that its Q3 2025 sales update will be released on October 23, 2025.

Based on the recent Q4 2025 earnings report, SGS appears to be maintaining its growth trajectory, with Q4 sales showing 5.6% organic growth, in line with the guidance provided in this H1 presentation. However, investors should note potential headwinds from currency fluctuations and trade tariffs, which could impact margins and supply chains in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.