Nvidia among investors in xAI’s $20bn capital raise - Bloomberg News

Introduction & Market Context

Sika AG (SIX:SIKA) reported modest growth of 1.6% in local currencies for the first half of 2025, according to the company’s presentation released on July 29, 2025. Despite challenging market conditions and significant foreign exchange headwinds, the Swiss specialty chemicals company managed to expand its EBITDA margin to 18.9%, up from 18.7% in the same period last year.

The results reflect a notable slowdown from the company’s stronger performance in previous years, with the Q4 2023 period having delivered 7.4% growth in local currencies. However, Sika continues to execute its strategic plan focused on margin improvement and targeted investments in growth areas.

Quarterly Performance Highlights

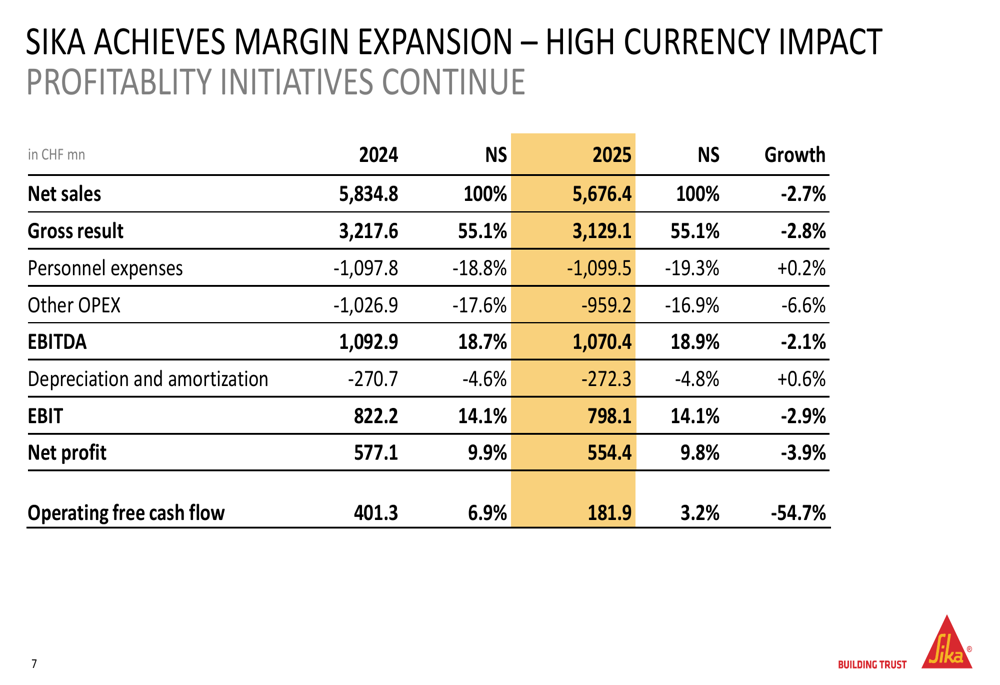

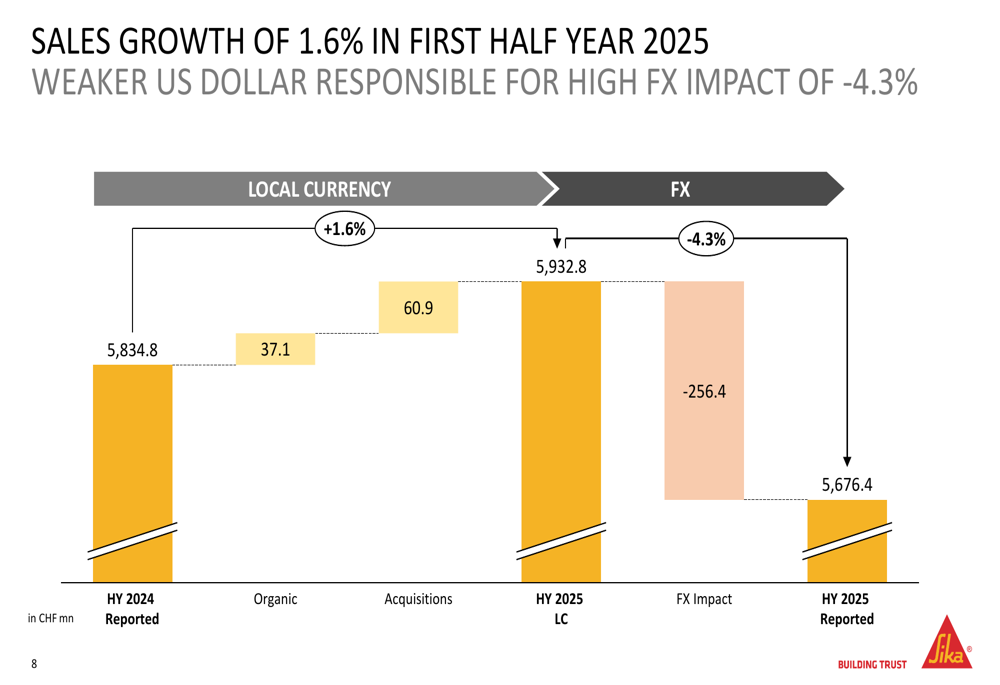

Sika reported sales of CHF 5,676.4 million for H1 2025, representing a 2.7% decrease from CHF 5,834.8 million in H1 2024. This decline was primarily due to a significant negative foreign exchange impact of 4.3%, which offset the 1.6% growth achieved in local currencies.

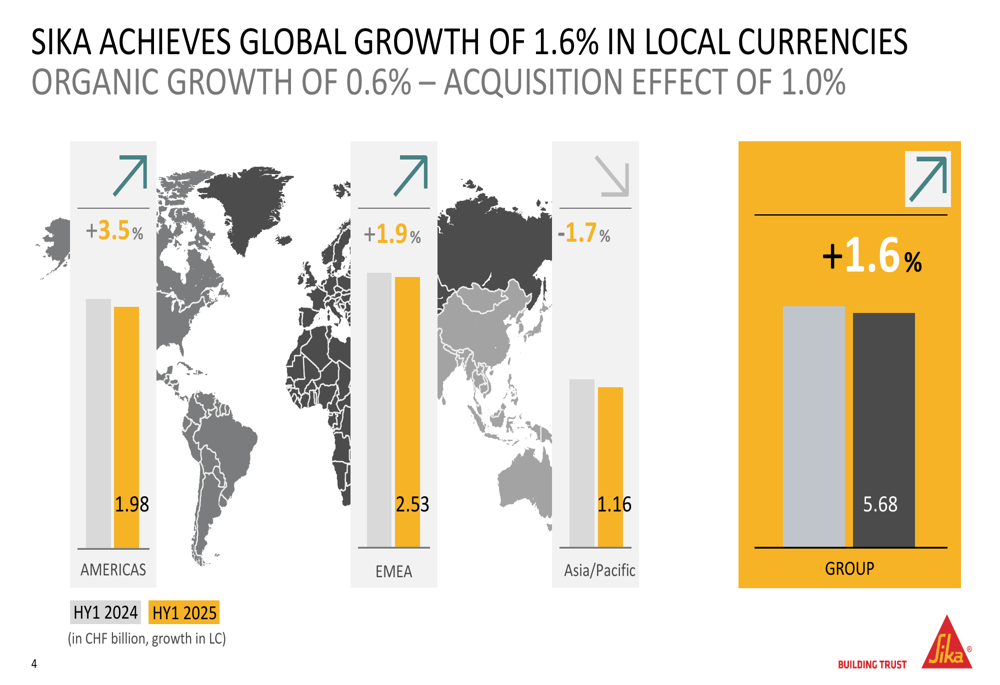

The company’s organic growth slowed to 0.6%, with acquisitions contributing an additional 1.0% to overall growth. Despite the sales decrease, Sika maintained its material margin at 55.1% and improved its EBITDA margin to 18.9%.

As shown in the following financial performance breakdown:

Net profit declined by 3.9% to CHF 554.4 million, representing 9.8% of net sales compared to 9.9% in the previous year. More significantly, operating free cash flow decreased by 54.7% to CHF 181.9 million, dropping from 6.9% to 3.2% of net sales.

The waterfall chart below illustrates how foreign exchange impacts affected Sika’s sales performance:

Regional Performance Analysis

Sika’s performance varied significantly across regions, with the Americas and EMEA showing growth while Asia/Pacific experienced a decline. The Americas region led with 3.5% growth, followed by EMEA at 1.9%, while Asia/Pacific contracted by 1.7%.

The following map highlights these regional variations in growth:

The company’s balanced business mix across different market segments has helped maintain stability despite regional fluctuations. Sika’s portfolio is distributed across residential (20%), infrastructure (30%), commercial (35%), and automotive & industry (15%) sectors, providing diversification against market-specific downturns.

Strategic Initiatives & Acquisitions

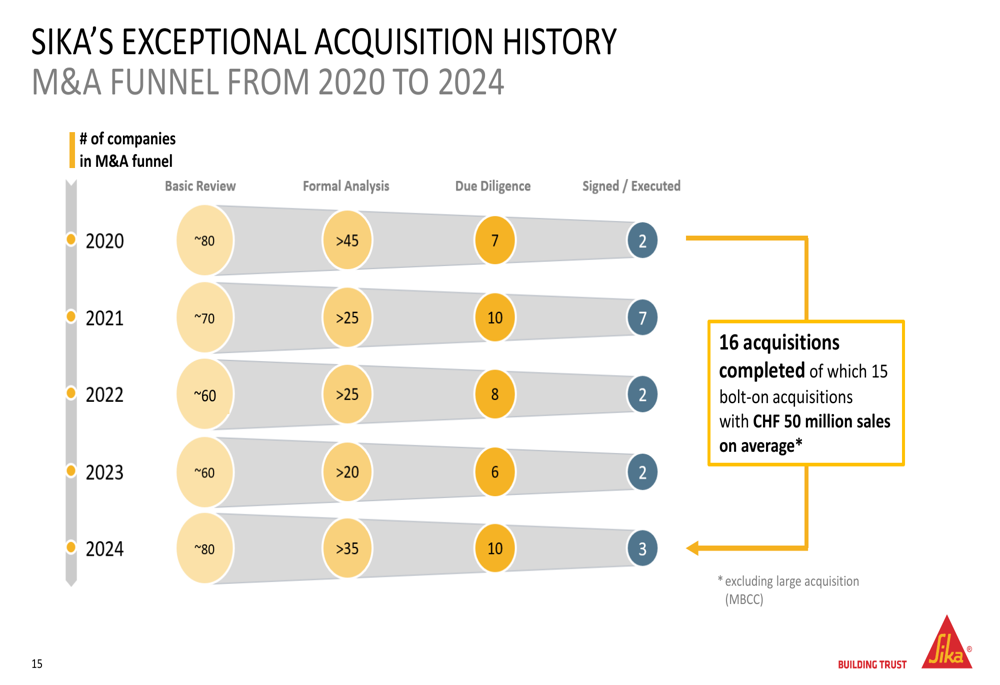

Sika continues to execute its growth strategy through targeted acquisitions and geographical expansion. In the first half of 2025, the company completed four bolt-on acquisitions: Elmich in Singapore (green roof solutions), Cromar in the UK (roofing products), HPS in the USA (building finishing materials), and Gulf Additive in Qatar (concrete admixtures).

Additionally, Sika formed a joint venture with Sulzer in Switzerland to advance plastic recycling and invested in Giatec Scientific in Canada for digital concrete technology platforms.

The company has maintained a consistent acquisition pipeline, as demonstrated in this historical M&A funnel:

Sika also commissioned seven new production facilities across the globe in Singapore, China (Xi’an and Suzhou), Morocco, Kazakhstan, Ecuador, and Brazil, strengthening its manufacturing footprint in key growth markets.

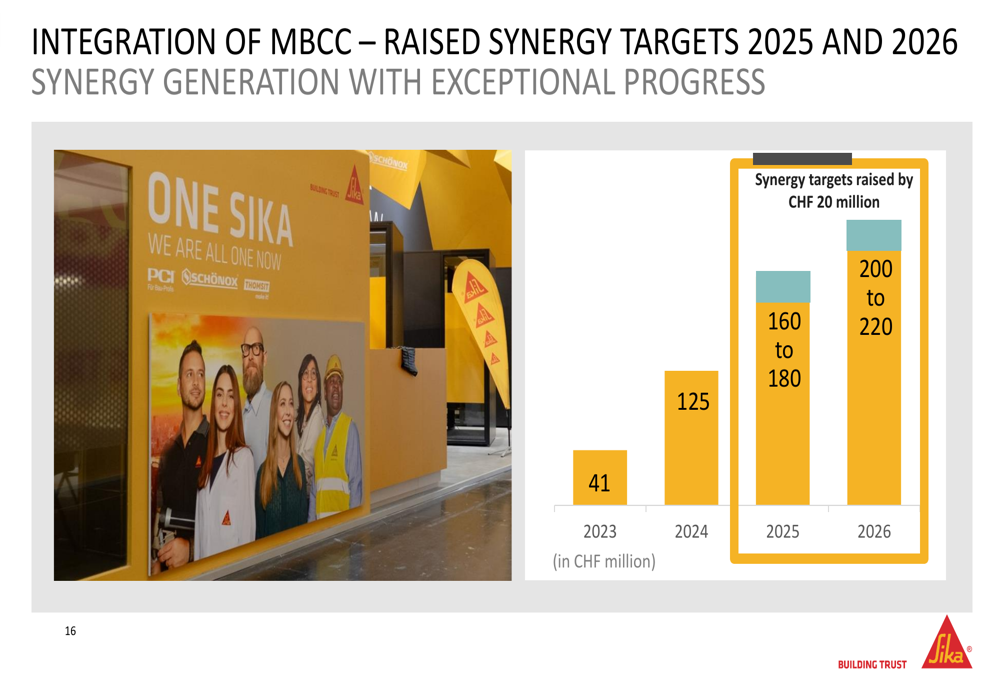

A significant achievement has been the successful integration of MBCC, with synergy targets for 2025 and 2026 raised by CHF 20 million. The revised targets now stand at CHF 160-180 million for 2025 and CHF 200-220 million for 2026, as illustrated below:

Innovation Focus

Sika continues to emphasize innovation as a key differentiator, highlighting several new solutions in its presentation. These include fiber-reinforced concrete for improved durability, concrete recycling technologies, self-healing membranes for flat roofs, conductive flooring systems, and cement-free tile adhesives with 50% lower carbon footprint.

The company’s innovation strategy aligns with its sustainability goals, which include a 20% reduction in Scope 1 and 2 greenhouse gas emissions by 2028 (compared to a 2022 baseline) and a 15% reduction in waste and water discharge per ton sold.

Market Position & Competitive Landscape

Sika maintains a 12% market share in a fragmented industry where the top 30 competitors (including Sika) account for 50% of the market. The company has consistently outperformed its peers in terms of organic growth, maintaining an average difference of 2.2% per year both pre-COVID (2015-2019) and in recent years (2021-2024).

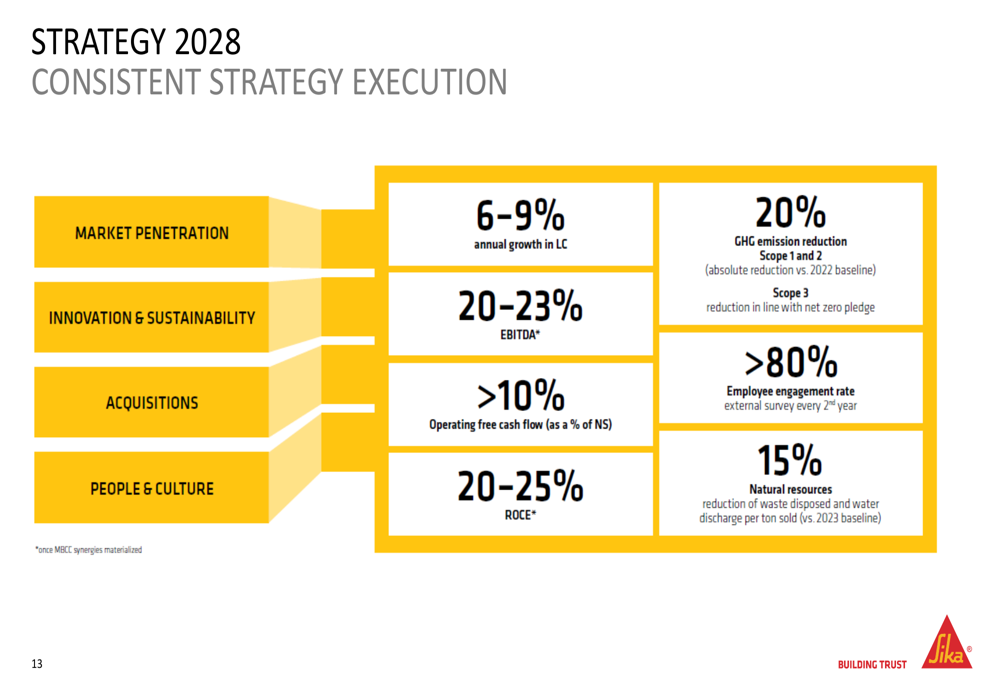

The company’s Strategy 2028 outlines ambitious targets for sustainable, profitable growth:

Outlook & Forward Guidance

Looking ahead, Sika expects modest sales increases in local currencies for the full year 2025, with an over-proportional EBITDA increase. The company has set an EBITDA margin target between 19.5% and 19.8% for the year.

Despite uncertain market developments, Sika has confirmed its strategic medium-term targets for 2028, maintaining its focus on growing above market rates and improving margins. The company aims to achieve 6-9% annual growth in local currencies, an EBITDA margin of 20-23% (once MBCC synergies are fully realized), operating free cash flow above 10% of net sales, and return on capital employed (ROCE) of 20-25%.

These targets represent a continuation of Sika’s long-term strategy, though the current growth rate of 1.6% falls below the medium-term target range, suggesting challenges in the current market environment that the company will need to overcome to achieve its 2028 objectives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.