Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

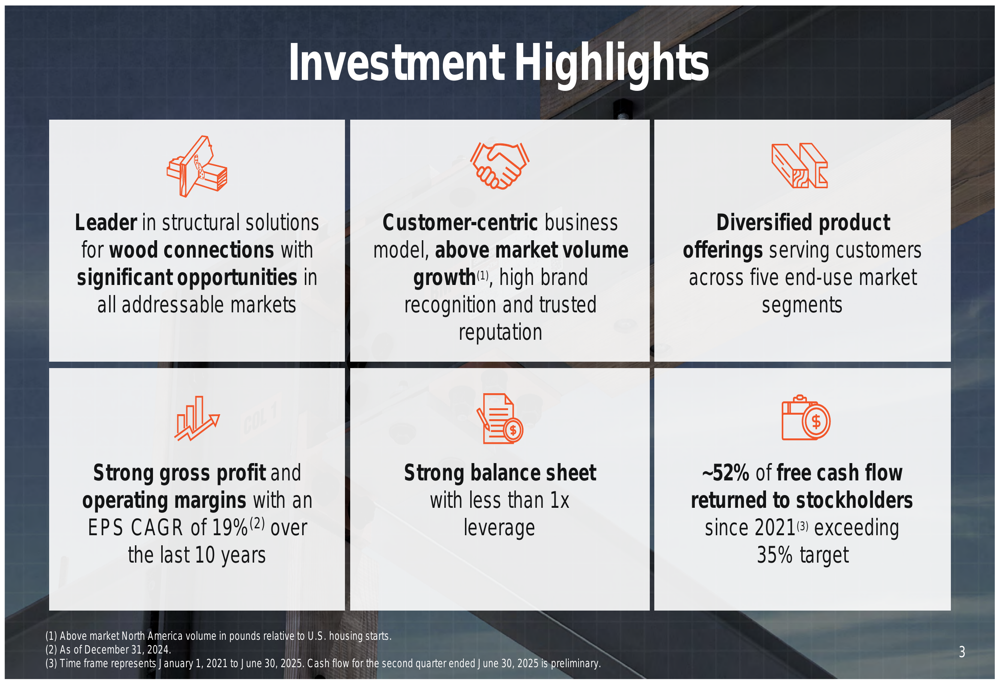

Simpson Manufacturing Co., Inc. (NYSE:SSD), a leader in structural building solutions, presented its July 2025 investor deck highlighting the company’s continued market outperformance despite a relatively flat housing market. The presentation showcases Simpson’s strategic positioning, financial strength, and growth initiatives as it celebrates 30 years as a public company.

The construction products manufacturer, valued at approximately $6.46 billion, recently reported strong Q1 2025 results with earnings per share of $1.85, exceeding forecasts of $1.65. Revenue reached $538.9 million, representing a 1.6% year-over-year increase, with North American sales rising 3.4% while European sales declined 5.1%.

As shown in the following investment highlights, Simpson emphasizes its leadership in structural solutions, customer-centric business model, and strong financial performance:

Financial Performance Highlights

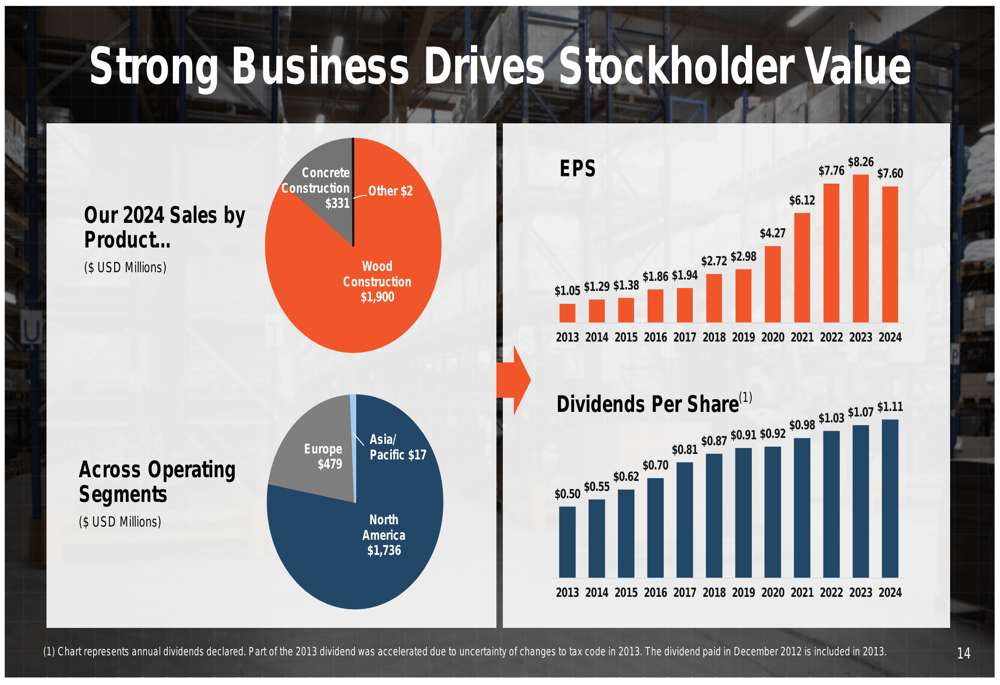

Simpson Manufacturing has delivered impressive long-term growth since its 1994 IPO, with a compound annual growth rate of approximately 15% including dividends. The company has grown revenue from $150 million in 1994 to $2.2 billion in 2024, representing a 15-fold increase. During the same period, earnings per share grew from $0.14 to $7.60, a remarkable 54-fold increase.

The company’s recent performance is particularly noteworthy given the flat housing market. Between 2020 and 2024, Simpson increased revenue from $1.25 billion to $2.23 billion and operating income from $250 million to $430 million, despite U.S. housing starts remaining essentially unchanged at approximately 1.37-1.38 million units.

The following chart illustrates the company’s sales breakdown by product and geographic segment, along with EPS and dividend growth:

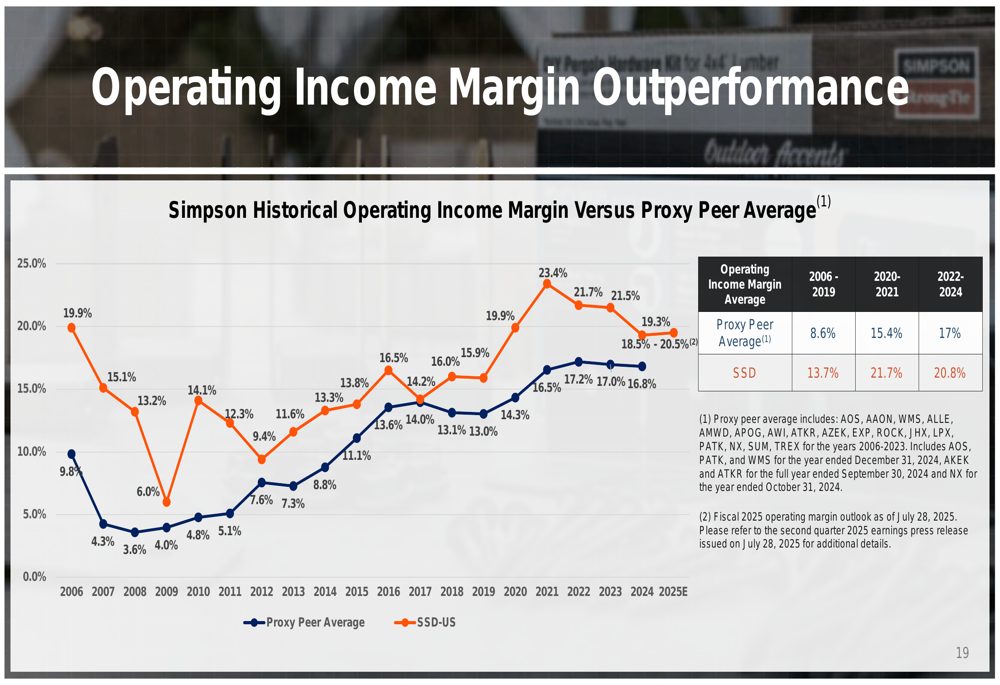

Simpson has consistently outperformed its peers in terms of operating margin. For the period 2022-2024, the company maintained an operating income margin of 20.8% compared to the proxy peer average of 17%. This margin strength was reflected in the recent Q1 2025 results, which showed a gross margin of 46.8%, up from 46.1% year-over-year.

The following chart demonstrates Simpson’s operating margin advantage over time:

Strategic Market Positioning

Simpson’s market-focused approach spans five key end-use markets in North America: Residential Construction, Commercial Construction, OEM, National Retail (NYSE:NNN), and Component Manufacturer. This diversification helps insulate the company from fluctuations in any single market segment.

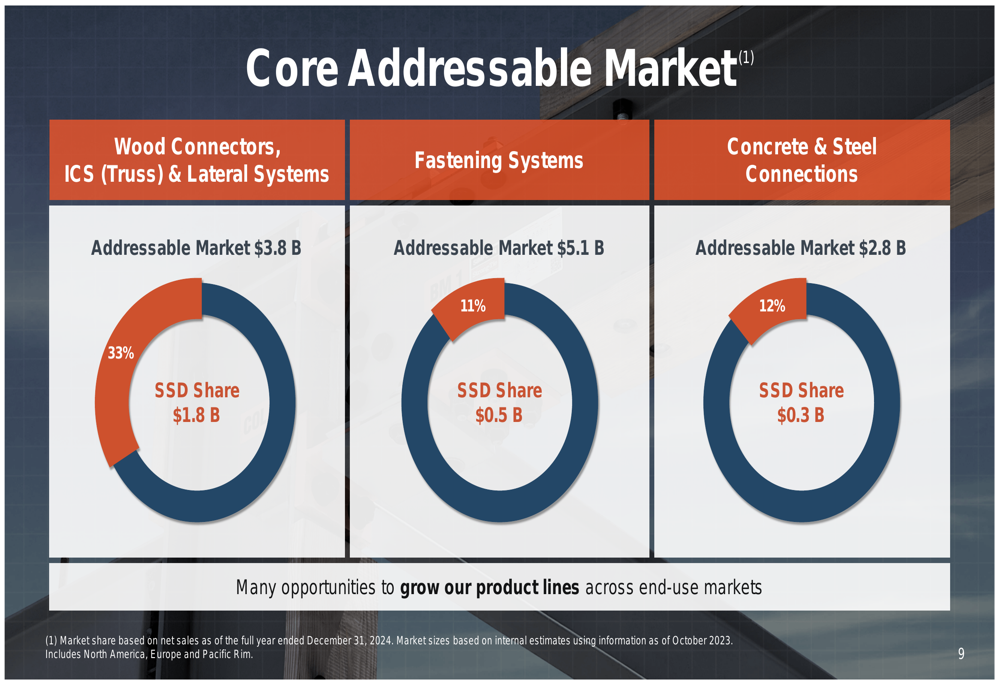

The company has identified significant growth opportunities within its core addressable markets, where it currently holds varying market shares: 33% in Wood Connectors ($3.8 billion market), 11% in Fastening Systems ($5.1 billion market), and 12% in Concrete & Steel Connections ($2.8 billion market).

The following chart details Simpson’s position in these core markets:

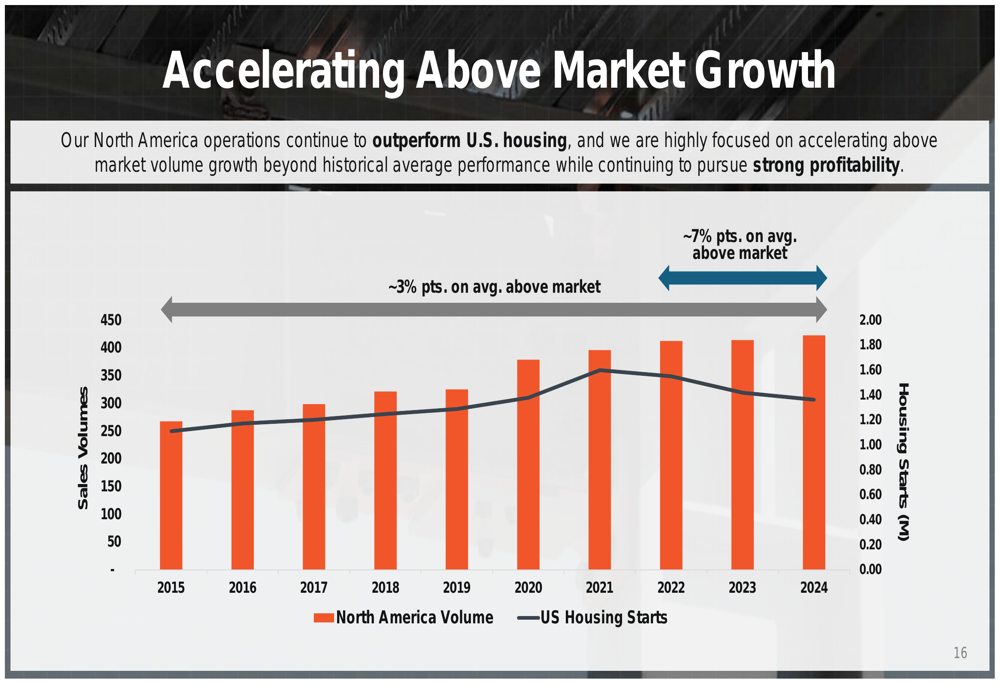

A key driver of Simpson’s success has been its ability to consistently outperform the broader housing market. The company’s North American sales volumes have grown approximately 7 percentage points on average above U.S. housing starts, demonstrating its ability to gain market share even in challenging conditions.

This outperformance is clearly illustrated in the following chart comparing Simpson’s volume growth to U.S. housing starts:

Growth Initiatives and Expansion Plans

Simpson is investing in capacity expansion to meet growing demand. Key initiatives include the expansion of its Columbus (WA:CLC), Ohio facility, which opened in the first half of 2025, and a new greenfield facility in Gallatin, Tennessee, expected to be operational in the second half of 2025. The Tennessee facility will support fastener sales growth, an area where Simpson sees significant market share opportunity.

The company is also focusing on digital transformation to enhance customer experience and operational efficiency. Simpson’s digital strategy aims to make it easier for customers to specify and order products, streamline partnerships, and provide comprehensive software solutions across its customer base.

In Europe, despite recent challenges reflected in the Q1 2025 results (sales down 5.1%), Simpson maintains a strategic focus on building strong brands, growing its core solutions, and targeting high-potential markets. The company is strengthening its position in wood connectors, doubling down on structural fasteners, and expanding in facade and pavement reinforcement products.

Capital Allocation and Shareholder Returns

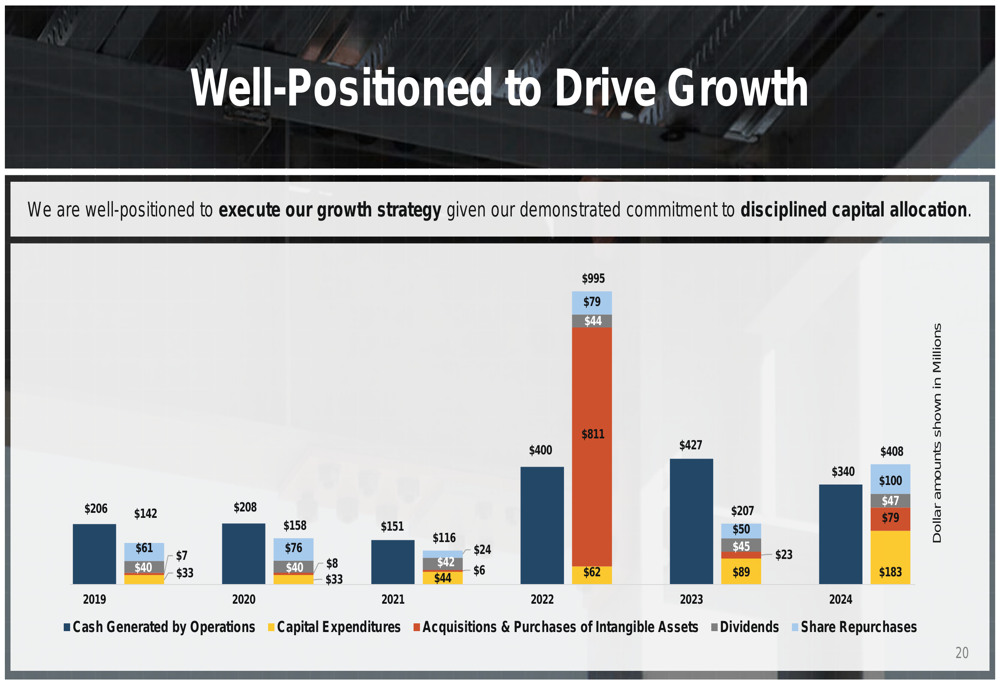

Simpson has demonstrated a strong commitment to shareholder returns, with approximately 52% of free cash flow returned to stockholders since 2021, exceeding its 35% target. Between 2021 and 2025, the company generated cumulative free cash flow of $983.2 million, allocating 31.8% to stock repurchases and 20.4% to quarterly cash dividends.

The company’s capital allocation priorities include:

1. Organic growth through facility expansions and growth initiatives

2. Share repurchases (with a $100 million authorization through December 2025)

3. Maintaining quarterly cash dividends

4. Strategic acquisitions

5. Debt repayment, particularly related to the ETANCO acquisition

The following chart illustrates Simpson’s strong cash generation and capital allocation:

Forward Outlook

Looking ahead, Simpson has outlined several key ambitions, including strengthening its values-based culture, becoming the business partner of choice, maintaining leadership in innovation, continuing above-market volume growth, maintaining operating income margins above 20%, and delivering EPS growth ahead of net revenue growth.

The company sees favorable long-term housing market dynamics, citing an estimated shortage of approximately 2 million homes in the U.S. and projecting total U.S. housing demand of 18.6 million over the 2024-2034 period (1.86 million per year).

In the near term, as noted in the recent earnings call, Simpson expects to navigate ongoing macroeconomic uncertainty while maintaining its strategic focus. The company forecasts EPS of $2.36 for Q2 2025 and $2.57 for Q3 2025, with analyst price targets ranging from $182 to $190, suggesting potential upside from the current price of $165.66.

Simpson’s management remains committed to maintaining gross margins through strategic pricing and cost management, with capital expenditures projected between $150 million and $170 million for the year. With its strong market position, diversified product portfolio, and consistent financial performance, Simpson Manufacturing appears well-positioned to continue its trajectory of market outperformance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.