China’s Xi speaks with Trump by phone, discusses Taiwan and bilateral ties

Introduction & Market Context

Simulations Plus (NASDAQ:SLP) released its third-quarter fiscal 2025 results on July 14, 2025, showing 10% revenue growth despite facing headwinds in the biopharma sector. The company's stock reacted positively to the earnings report, rising 1.1% to $16.32, as investors focused on improved adjusted metrics rather than a significant GAAP loss due to a non-cash impairment charge.

The pharmaceutical simulation software provider continues to navigate a challenging market environment characterized by client consolidations, site closures, and budget constraints across the biopharma industry. Despite these challenges, Simulations Plus has maintained revenue growth through its diversified portfolio of software and services.

Quarterly Performance Highlights

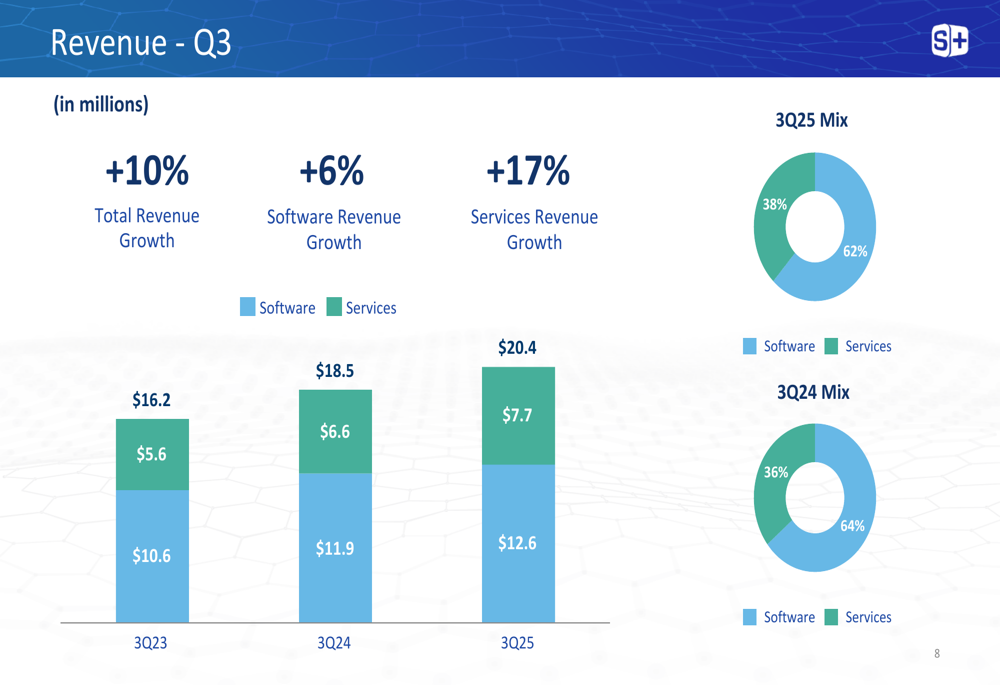

Simulations Plus reported Q3 FY25 revenue of $20.4 million, a 10% increase from $18.5 million in Q3 FY24. While GAAP diluted EPS showed a significant loss of $(3.35) compared to earnings of $0.15 in the prior year, adjusted diluted EPS improved to $0.45 from $0.27, representing a 67% year-over-year increase. The company's adjusted EBITDA margin expanded to 37% from 30% in the same period last year.

As shown in the following quarterly highlights chart, the company maintained revenue growth while significantly improving its adjusted metrics:

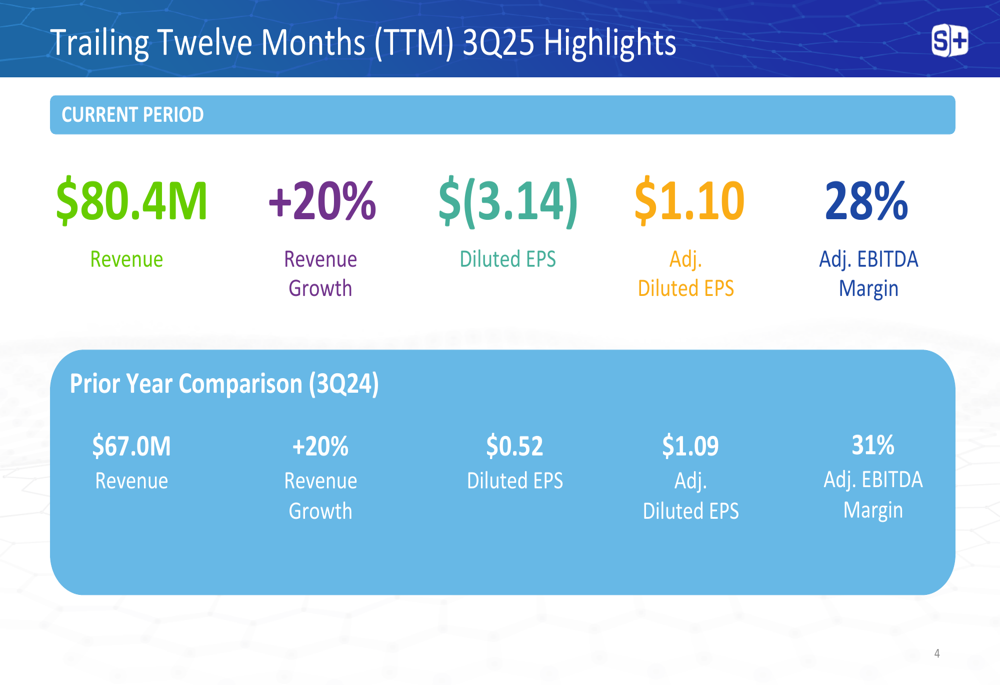

The trailing twelve months (TTM) results demonstrate even stronger performance, with revenue growing 20% to $80.4 million. However, the GAAP diluted EPS for the TTM period showed a loss of $(3.14) compared to earnings of $0.52 in the prior TTM period, primarily due to the impairment charge in Q3.

Detailed Financial Analysis

Simulations Plus's revenue growth was driven by both software and services segments, though at different rates. Software revenue increased 6% to $12.6 million, while services revenue grew 17% to $7.7 million. The revenue mix continues to shift slightly toward services, which now represent 38% of total revenue compared to 36% in the prior year.

The following chart illustrates the revenue breakdown and growth trends over the past three years:

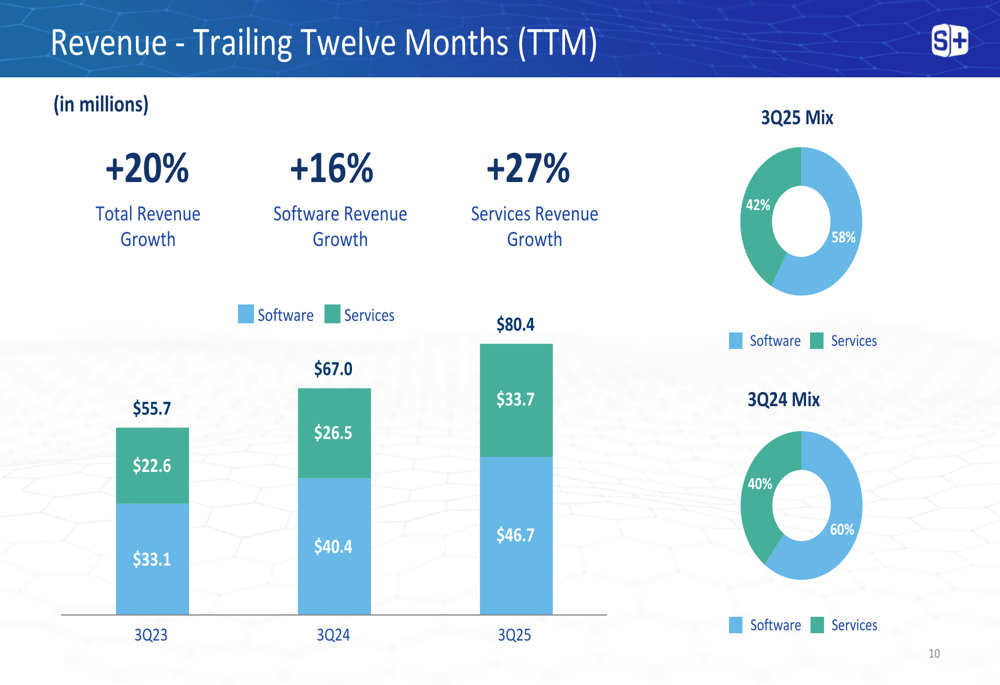

On a trailing twelve months basis, the trend is even more pronounced, with services growing to 42% of total revenue compared to 40% in the prior TTM period:

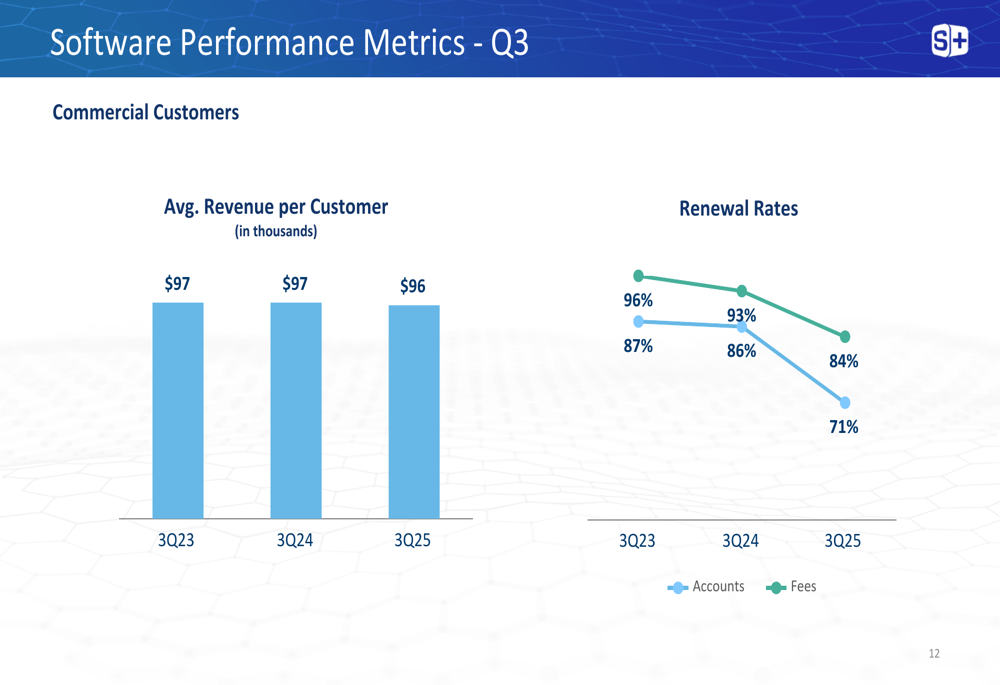

Despite overall revenue growth, the company faces challenges in software renewal rates. Account renewal rates declined to 84% in Q3 FY25 from 93% in Q3 FY24, while fee renewal rates dropped more significantly to 71% from 86%. The company attributed these declines to client consolidations and site closures in the biopharma industry.

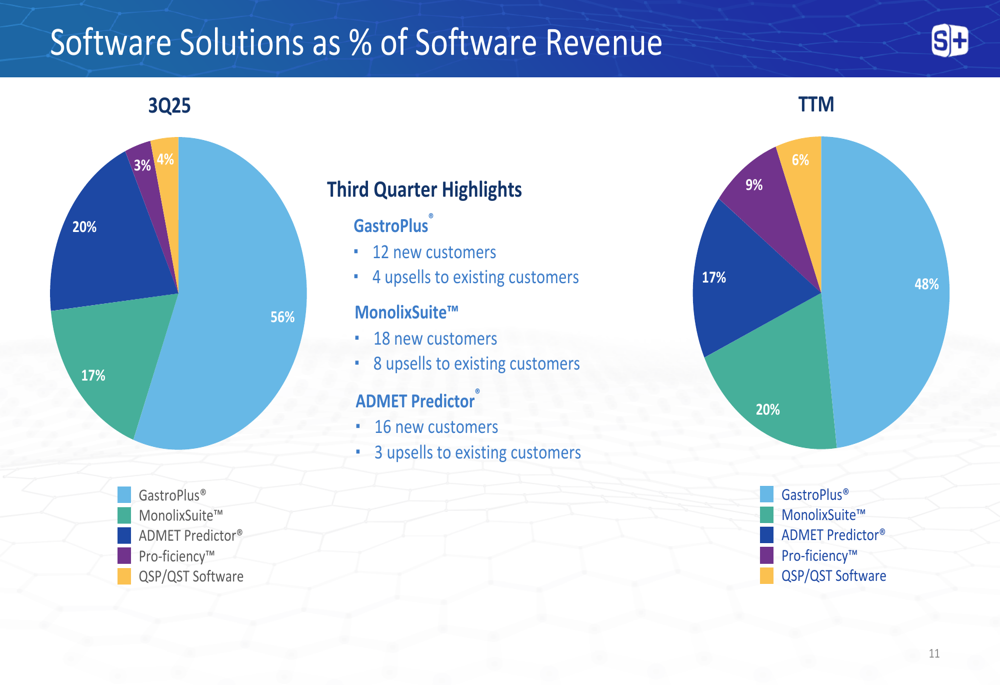

Within the software segment, GastroPlus remains the dominant product, accounting for 56% of software revenue in Q3 FY25. ADMET Predictor and MonolixSuite contributed 20% and 17% respectively, while the recently acquired Pro-ficiency platform accounted for 4%.

The services segment showed mixed performance across different solution areas. While Med Comm services (acquired through Pro-ficiency) contributed $2.0 million in Q3 revenue, the company noted that this was below expectations. Traditional biosimulation services faced challenges, with PBPK services declining 10%, PKPD services declining 9%, and QSP/QST services declining 22% compared to the prior year.

Despite these challenges, the services backlog remained strong at $20.7 million, with over 91% expected to be converted to revenue within the next 12 months.

Financial Results

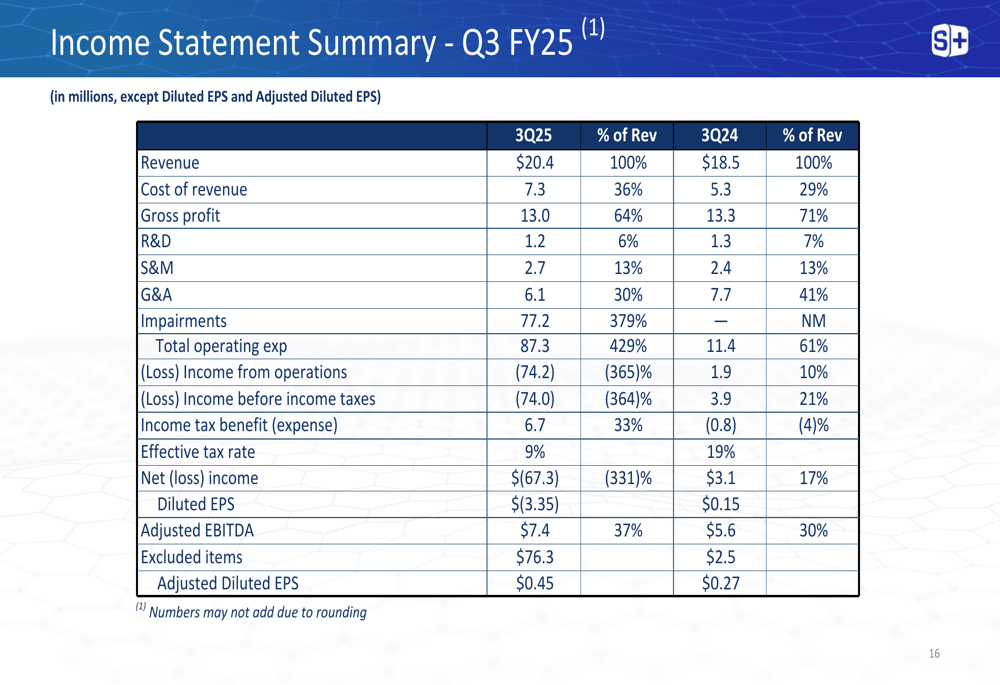

The most significant aspect of Simulations Plus's Q3 financial results was the substantial GAAP net loss of $(67.3) million, compared to net income of $3.1 million in Q3 FY24. This loss was primarily due to a non-cash impairment charge of approximately $77.2 million, as mentioned in the earnings call.

The following income statement summary highlights the impact of this impairment charge while also showing improvements in adjusted metrics:

Despite the GAAP loss, the company's balance sheet remains relatively strong with $28.5 million in cash and short-term investments as of May 31, 2025, an increase from $20.3 million at the end of fiscal 2024. Total assets declined to $134.4 million from $196.6 million, primarily reflecting the impairment charge.

Forward-Looking Statements

Looking ahead, Simulations Plus provided fiscal 2025 guidance projecting total revenue between $76 million and $80 million, representing growth of 9% to 14%. The company expects software to contribute 55% to 60% of total revenue, with adjusted EBITDA margin between 23% and 27%. Adjusted diluted EPS is projected to be between $0.93 and $1.06.

During the earnings call, CEO Shawn O'Connor emphasized the company's focus on AI initiatives to drive innovation and business growth. The company is also undergoing a strategic reorganization to streamline operations and enhance efficiency in response to market challenges.

Conclusion

Simulations Plus's Q3 FY25 results present a mixed picture. While the company continues to grow revenue and improve adjusted metrics, declining software renewal rates and the significant impairment charge highlight challenges in the current biopharma market environment. The company's diversification across software and services provides some resilience, but investor focus will likely remain on whether Simulations Plus can stabilize renewal rates and successfully integrate its recent acquisitions.

The positive stock reaction suggests investors are looking beyond the impairment charge to focus on the underlying business performance and growth potential. With the stock trading at $16.32, well below its 52-week high of $37.67, there may be room for recovery if the company can execute on its strategic initiatives and navigate the ongoing industry headwinds.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.