ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

Sinclair Inc. (NASDAQ:SBGI) presented its third-quarter 2025 earnings results on November 5, 2025, revealing performance that exceeded guidance on key metrics. The company's stock responded positively to the news, rising 2.02% to close at $13.36, though it retreated slightly in after-market trading.

The broadcast media company continues to navigate industry headwinds while pursuing strategic acquisitions and portfolio optimization in a favorable regulatory environment. Sinclair's presentation highlighted both its current financial strength and its positioning for future growth opportunities.

Quarterly Performance Highlights

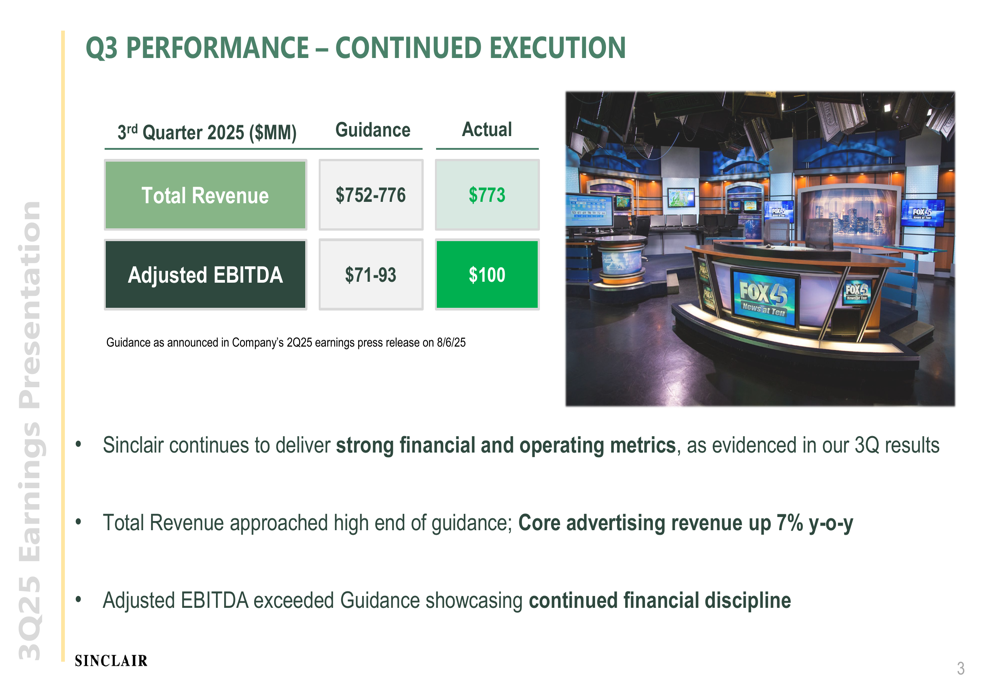

Sinclair delivered strong financial results in Q3 2025, with total revenue of $773 million approaching the high end of guidance ($752-776 million) and adjusted EBITDA of $100 million exceeding the guidance range of $71-93 million. The company reported core advertising revenue growth of 7% year-over-year, demonstrating resilience in a challenging media landscape.

As shown in the following performance summary:

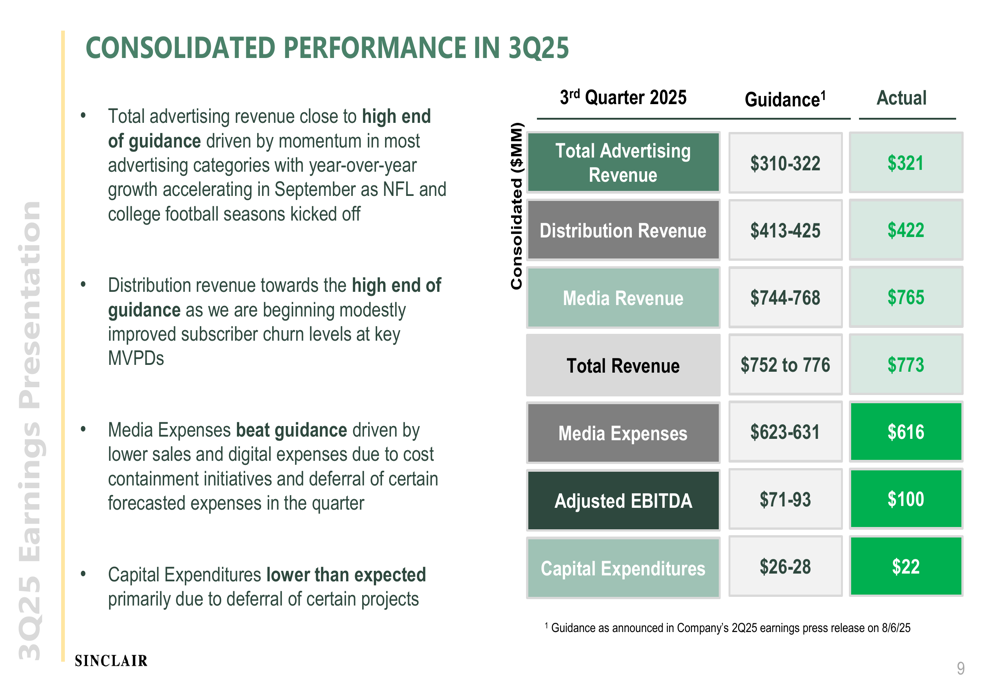

A more detailed breakdown of Sinclair's consolidated performance shows that total advertising revenue reached $321 million, near the high end of guidance due to momentum across most advertising categories. Distribution revenue also performed well at $422 million, while media expenses came in below guidance at $616 million, driven by lower sales and digital expenses.

Segment performance revealed strength across both Local Media and Tennis Channel operations. The Local Media segment exceeded quarterly guidance on multiple metrics, while Tennis Channel's revenue grew 12% compared to Q3 2024.

Strategic Initiatives

Sinclair continues to optimize its station portfolio through strategic acquisitions and divestitures. As of November 5, 2025, the company has closed 11 partner station acquisitions, with two more awaiting final closing after FCC approval and 10 pending FCC approval. These transactions, once completed, are expected to contribute at least $30 million in incremental annualized adjusted EBITDA.

The company is operating in what it describes as a more constructive M&A environment for the local broadcast industry, citing recent FCC and court decisions. Sinclair anticipates the FCC may raise or eliminate the nationwide ownership cap of 39% in the first half of 2026, which could create additional growth opportunities.

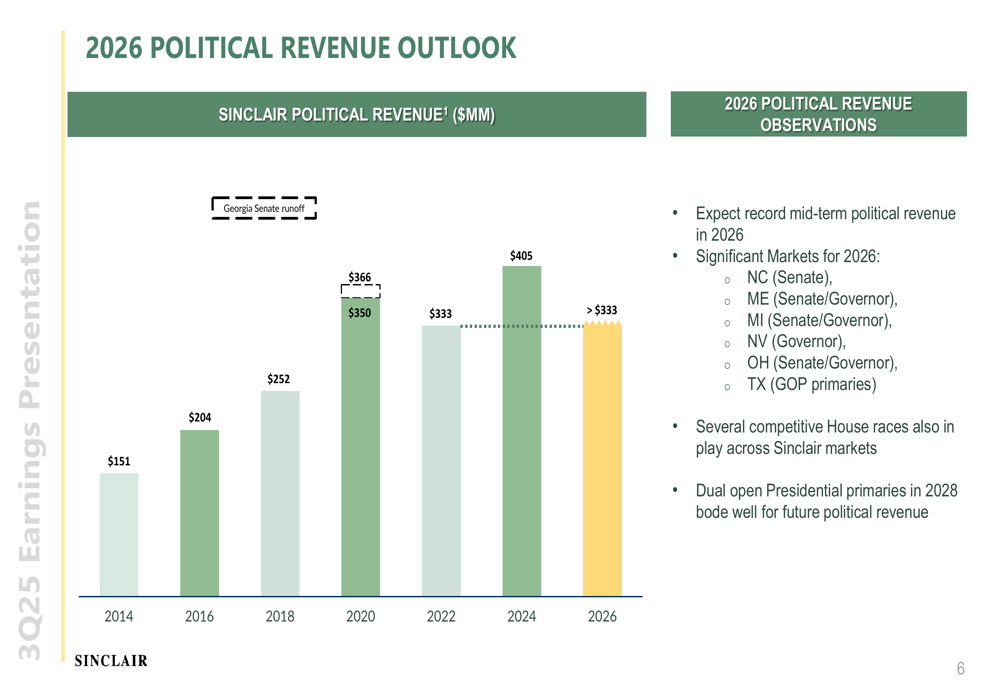

Looking ahead to 2026, Sinclair expects record mid-term political revenue, with significant markets including North Carolina, Maine, Michigan, Nevada, Ohio, and Texas driving political advertising spend. The company's historical political revenue shows a consistent upward trend, with projections for 2026 exceeding $333 million.

Capital Structure and Debt Management

As of September 30, 2025, Sinclair Television Group's total debt stood at $4.1 billion. The company reported consolidated cash of $526 million ($122 million at SBG and $404 million at Ventures) and total liquidity of $1.2 billion, including undrawn revolver capacity.

In a move to strengthen its balance sheet, Sinclair redeemed $89 million of Senior Unsecured Notes due 2027 on October 6, 2025. The company's debt maturity schedule shows a relatively manageable profile through 2033.

The Ventures portfolio, which had $404 million in cash at quarter-end, received $2 million in cash distributions during Q3 2025 while making incremental investments of approximately $6 million. Management indicated they are continuing to explore consolidated investments for Ventures as well as shareholder-friendly actions.

Forward-Looking Statements

For the fourth quarter of 2025, Sinclair provided guidance projecting total revenue between $815 million and $851 million, with adjusted EBITDA expected to range from $132 million to $154 million.

Looking further ahead, Sinclair's preliminary 2026 outlook anticipates record non-Presidential political advertising revenue, at least matching the 2022 midterm year. Core advertising is expected to see flat to low single-digit growth, while distribution revenue is projected to remain approximately flat with 2025 levels. Capital expenditures are expected to be consistent with 2025 levels.

In a strategic shift, Sinclair announced it will move to an annual guidance framework beginning with its 2026 guidance in February. The company also revealed it has launched a comprehensive strategic review of its broadcast business and has begun work to separate its Ventures division, signaling potential structural changes ahead.

The company's management expressed confidence in its positioning, citing the ongoing deregulatory environment progress and expectations for solid revenues with improving trends in Q4 2025 and into 2026.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.