AlphaTON stock soars 200% after pioneering digital asset oncology initiative

Introduction & Market Context

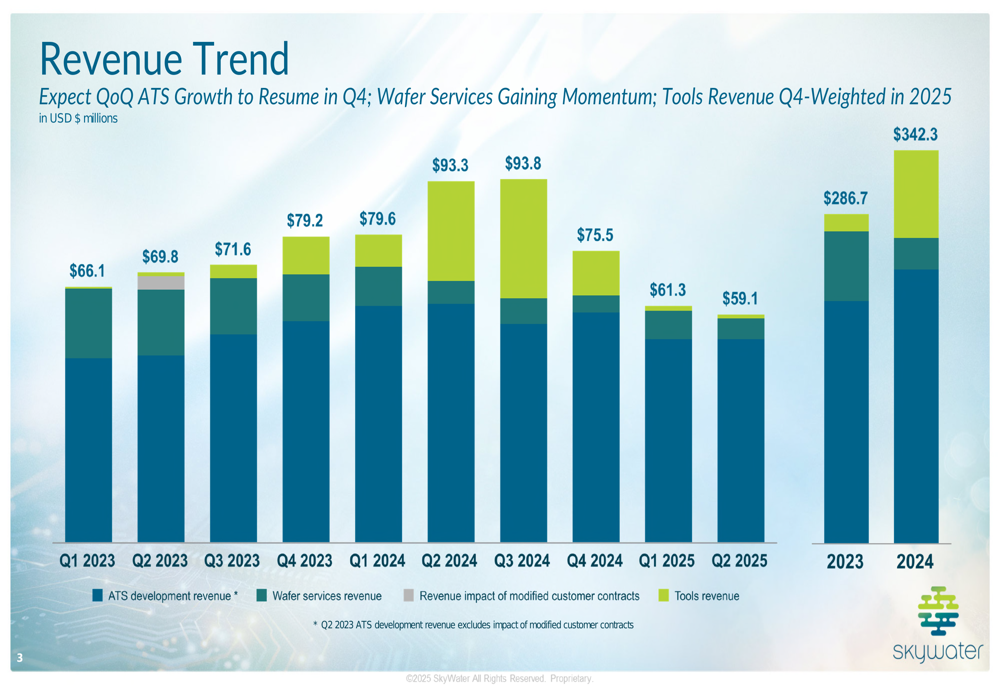

SkyWater Technology (NASDAQ:SKYT) presented its Q2 2025 earnings on August 6, highlighting a transformative acquisition that promises to significantly expand its market presence despite current quarter revenue challenges. The semiconductor foundry reported revenue of $59.1 million for the quarter, representing a decline from both the previous quarter ($61.3 million) and the same period last year ($93.3 million), but landing at the upper end of the company’s guidance range.

The focal point of the presentation was SkyWater’s completed acquisition of Infineon (OTC:IFNNY)’s Fab 25 in Austin, Texas, for approximately $93 million. This strategic move is expected to double the company’s annual revenue and adjusted EBITDA while significantly strengthening its position in the U.S. semiconductor manufacturing landscape.

Quarterly Performance Highlights

SkyWater’s Q2 2025 revenue breakdown shows $52.6 million in ATS (Advanced Technology Services) development revenue, $5.4 million in Wafer Services revenue, and $1.1 million in Tools revenue. The significant year-over-year revenue decline was primarily due to lower Tools revenue, which was $25.9 million in Q2 2024 compared to just $1.1 million in the current quarter.

As shown in the following revenue trend chart, SkyWater’s quarterly performance has fluctuated significantly over the past two years, with the company expecting ATS growth to resume in Q4 2025:

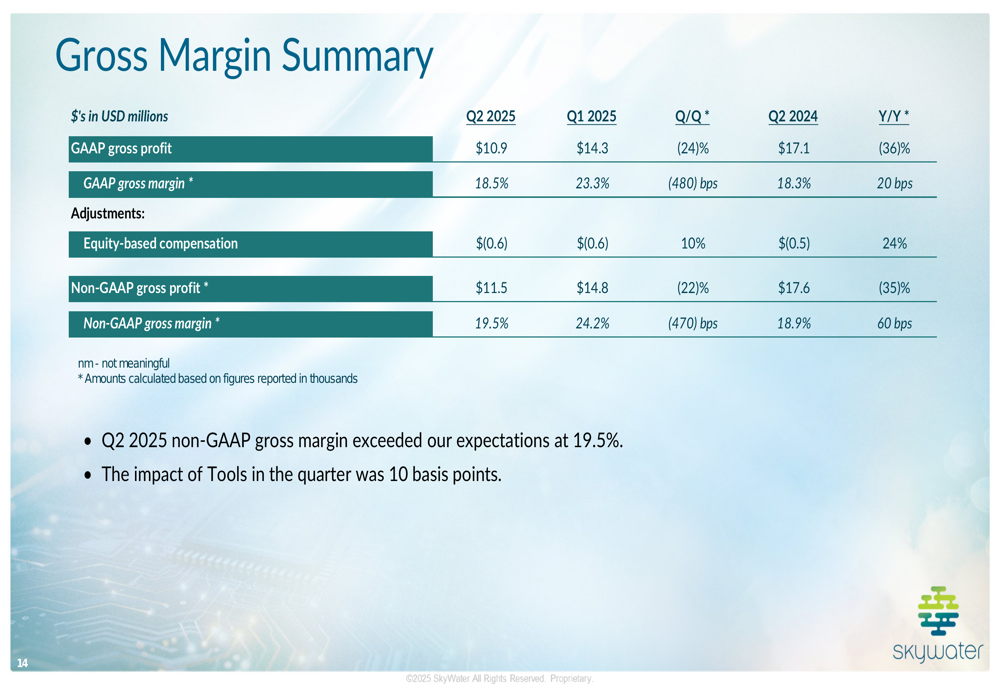

Despite the revenue challenges, SkyWater reported better-than-expected profitability metrics. Non-GAAP gross margin exceeded expectations at 19.5%, though this represents a decline from 24.2% in Q1 2025. The following chart details the gross margin performance:

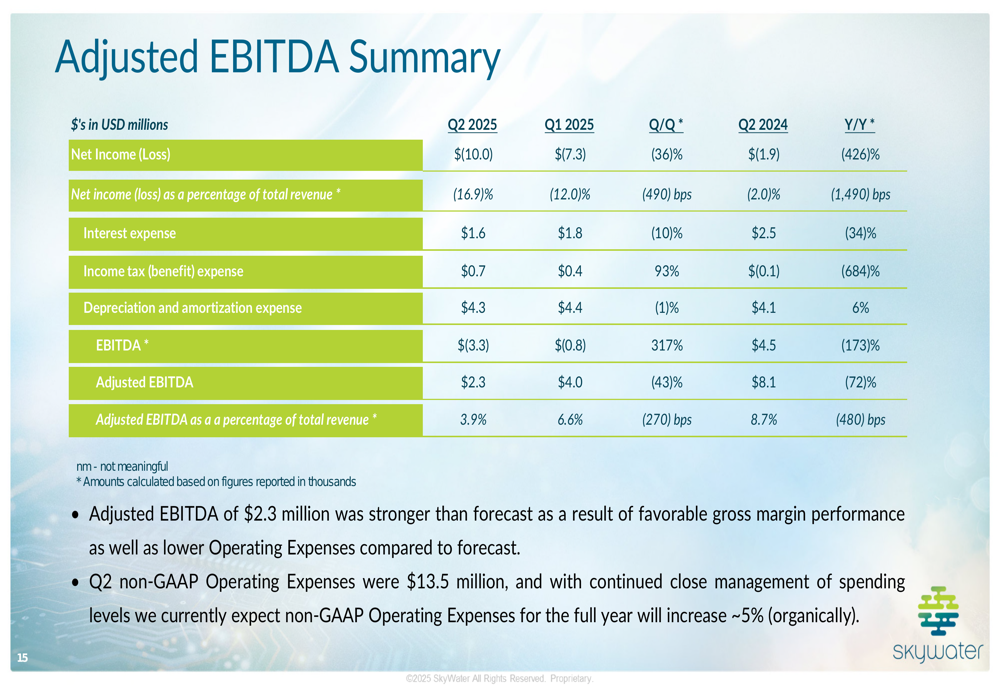

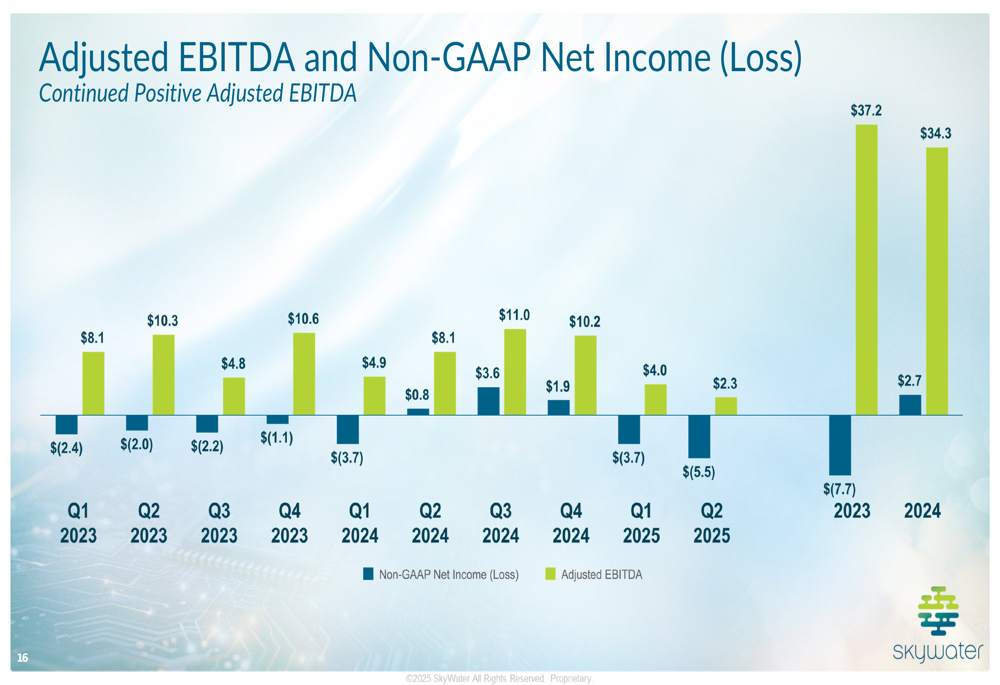

Adjusted EBITDA for Q2 2025 was $2.3 million (3.9% of revenue), stronger than forecast but down from $4.0 million (6.6% of revenue) in Q1 2025 and $8.1 million (8.7% of revenue) in Q2 2024. The company reported a non-GAAP net loss of $5.5 million, compared to a loss of $3.7 million in Q1 2025.

The quarterly trend of Adjusted EBITDA and Non-GAAP Net Income shows a challenging start to 2025 after a relatively strong performance in the latter half of 2024:

Strategic Initiatives

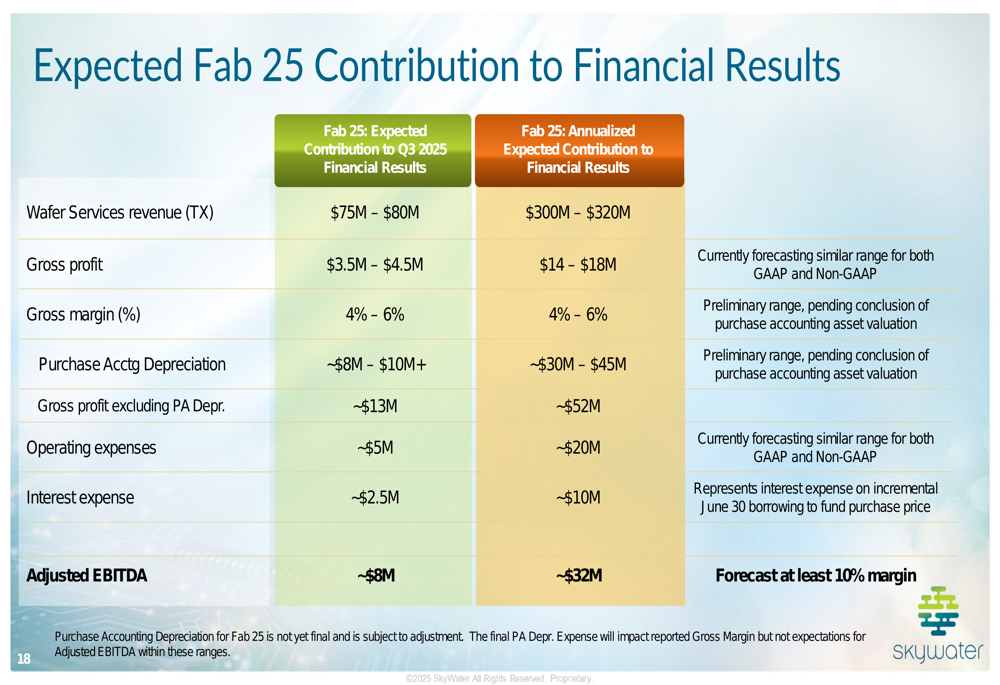

The acquisition of Infineon’s Fab 25 represents SkyWater’s most significant strategic move. Funded by a new credit facility, the $93 million purchase is expected to have an immediate and substantial impact on the company’s financial profile. The following slide illustrates how Fab 25 is positioned to address critical market needs:

SkyWater expects Fab 25 to contribute $75-80 million in Wafer Services revenue in Q3 2025 alone, with an annualized contribution of $300-320 million. While initial gross margins from the facility are projected at a modest 4-6%, the acquisition is expected to generate approximately $8 million in Adjusted EBITDA in Q3 2025 and approximately $32 million on an annualized basis.

Beyond the Fab 25 acquisition, SkyWater highlighted progress in several strategic growth areas. The company is building momentum in quantum computing, positioning itself as a U.S.-based provider of quantum chip development and production with capabilities to support a wide range of architectures.

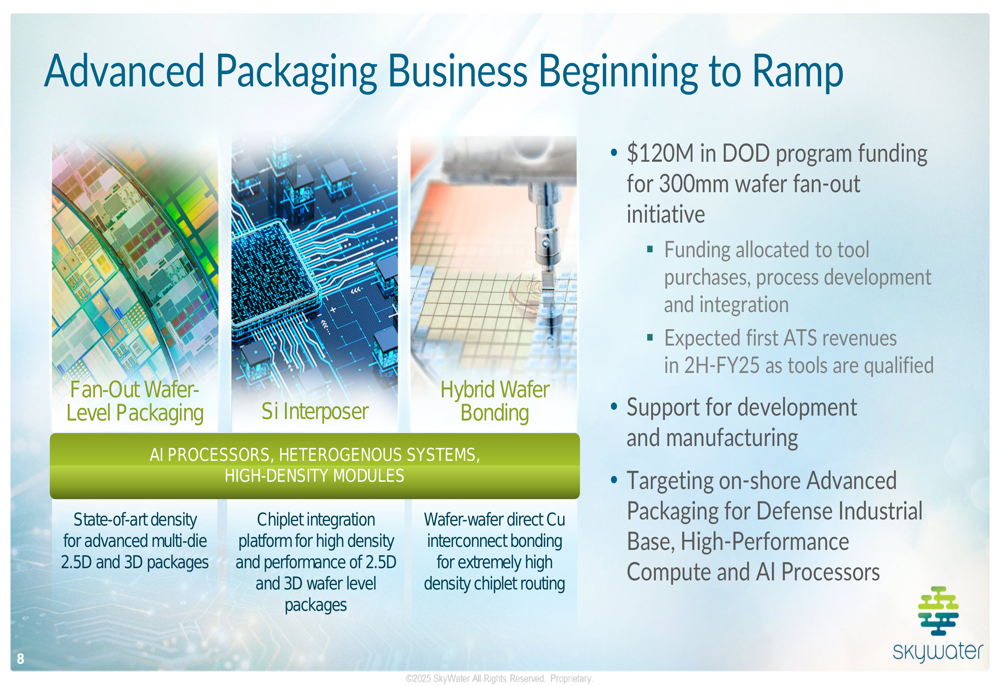

SkyWater is also advancing its Advanced Packaging (NYSE:PKG) business, with new tooling installations in Florida expected to drive revenue growth in the second half of 2025. The company has secured $120 million in Department of Defense funding for its 300mm wafer fan-out initiative, with first ATS revenues expected in the second half of 2025.

Competitive Industry Position

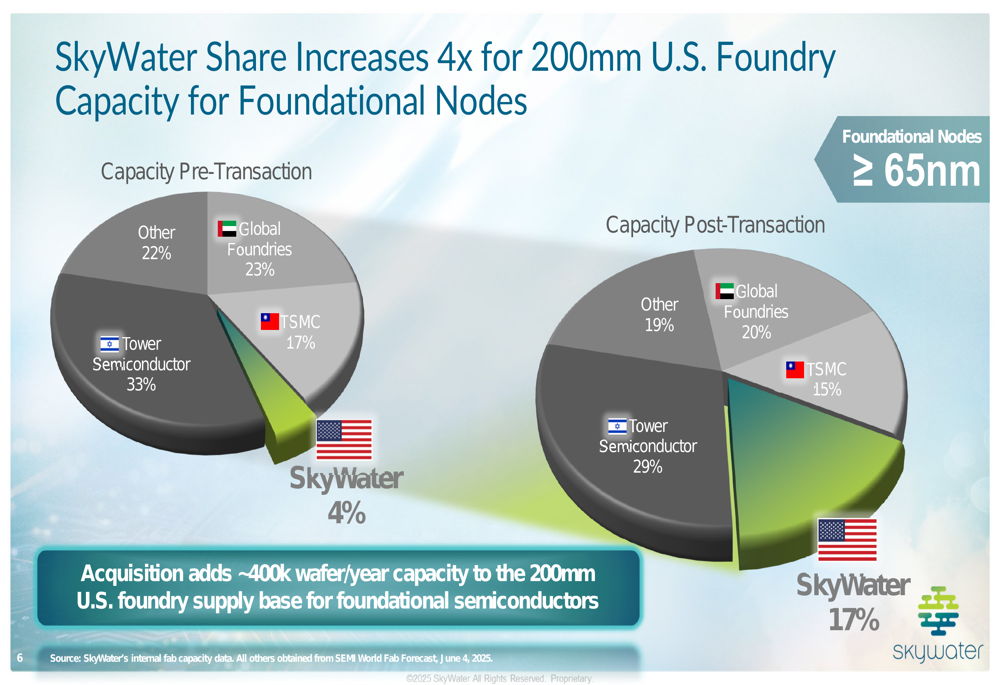

The Fab 25 acquisition dramatically improves SkyWater’s competitive position in the U.S. semiconductor manufacturing landscape. As illustrated in the following chart, SkyWater’s share of 200mm U.S. foundry capacity for foundational nodes has increased from 4% to 17% following the transaction:

This expanded capacity strengthens SkyWater’s ability to address growing demand in several key markets, including medical devices, defense and aerospace, industrial automation, and automotive applications. The company emphasized its role in providing a U.S.-based secure supply chain for critical technologies.

SkyWater also highlighted its ThermaView platform, which is gaining momentum in 2025, primarily driven by two leading U.S. defense prime customers. The company is targeting a $9 billion thermal imaging market opportunity projected by 2027, with applications spanning defense, industrial, and medical sectors.

Forward-Looking Statements

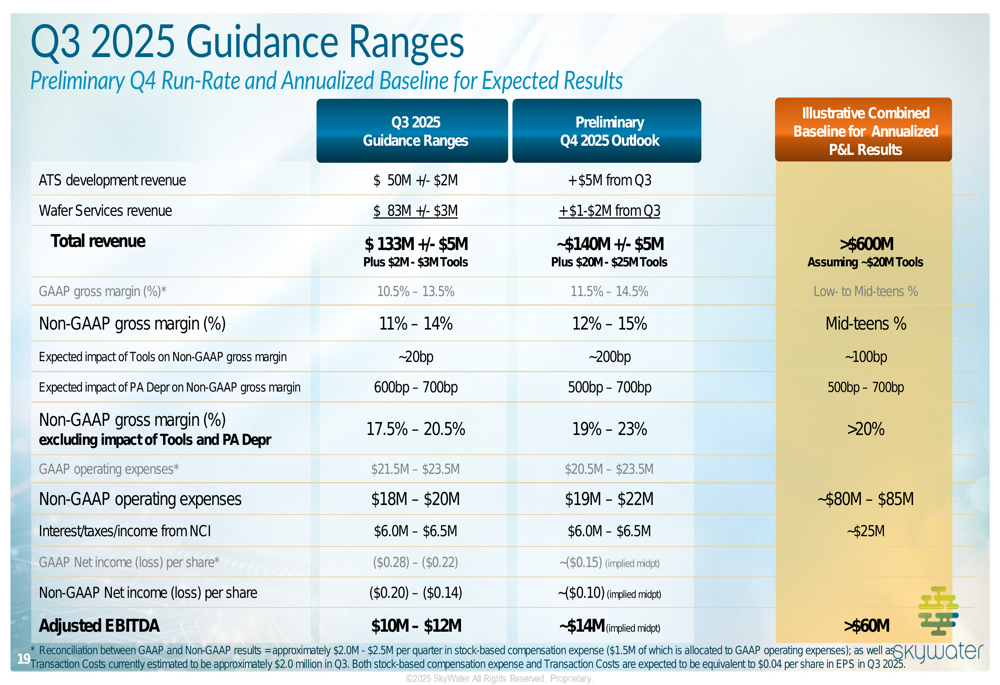

For Q3 2025, SkyWater provided guidance of approximately $50 million in ATS revenue (plus or minus $2 million) and $83 million in Wafer Services revenue (plus or minus $3 million), for a total of $133 million (plus or minus $5 million), plus an additional $2-3 million in Tools revenue.

The company’s preliminary outlook for Q4 2025 includes at least $5 million of incremental ATS revenue from Florida and $1-2 million of sequential growth in Wafer Services, bringing the quarterly revenue run-rate to approximately $140 million before Tools revenue of $20-25 million.

Looking ahead to fiscal 2026, SkyWater projects a strong foundation for more than $600 million in revenues and over $60 million in Adjusted EBITDA. The company expects to achieve Adjusted EBITDA exceeding 10% of revenues (exclusive of tools) at its projected quarterly run-rate entering 2026.

SkyWater also highlighted the benefits of its customer-funded CapEx model, which has incorporated $76 million in tool funding through contract awards in 2024. The company expects additional customer-funded CapEx of more than $90 million through year-end 2026, bringing the total expected funding from 2020 to 2026 to approximately $320 million.

The company’s optimistic outlook contrasts with its current performance challenges, suggesting that the transformative impact of the Fab 25 acquisition and the ramp-up of strategic initiatives will drive significant growth in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.