Infosys, Wipro decline despite upbeat Q2 earnings; margin concerns weigh

SM Energy Company (NYSE:SM) presented its second quarter 2025 financial and operating results on July 31, 2025, highlighting record production levels, strong financial performance, and continued progress on debt reduction. Despite these achievements, the stock experienced a 2.29% decline in aftermarket trading, closing at $22.61, reflecting mixed investor sentiment amid broader market volatility.

Quarterly Performance Highlights

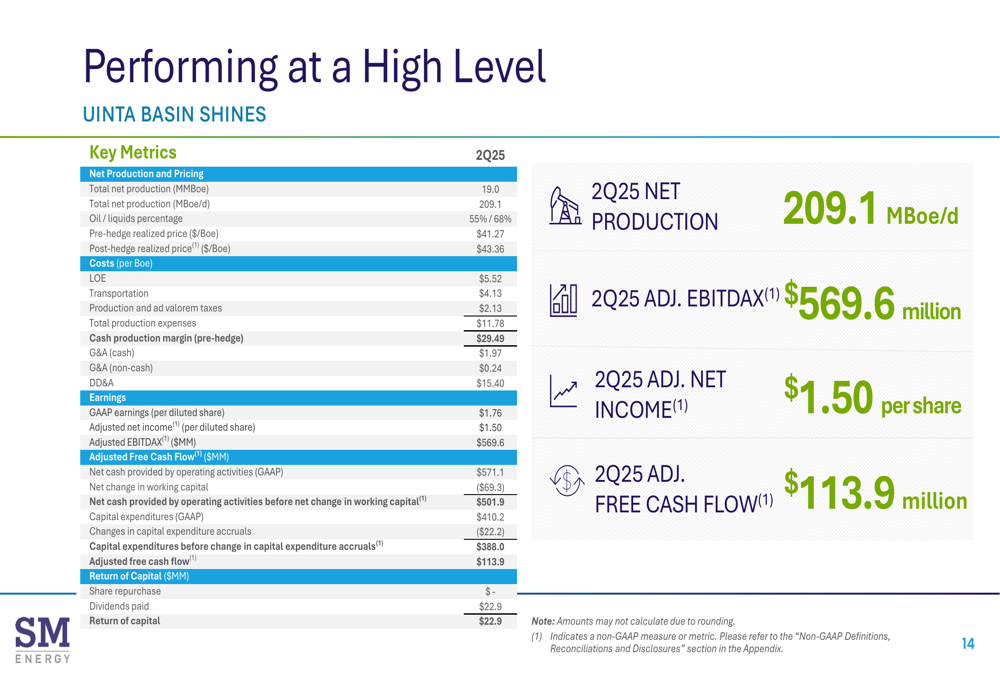

SM Energy reported record-breaking Q2 production of 209.1 MBoe/d with 55% oil content, driving strong financial results including adjusted net income of $1.50 per share and adjusted EBITDAX of $570 million. The company generated $113.9 million in adjusted free cash flow, allowing for continued debt reduction and dividend payments.

As shown in the following performance summary from the presentation:

The company’s operational excellence has translated into significant financial strength, with adjusted EBITDAX reaching nearly $570 million for the quarter. This performance builds on SM Energy’s multi-year growth trajectory, which has seen substantial increases in both production and reserves since 2020.

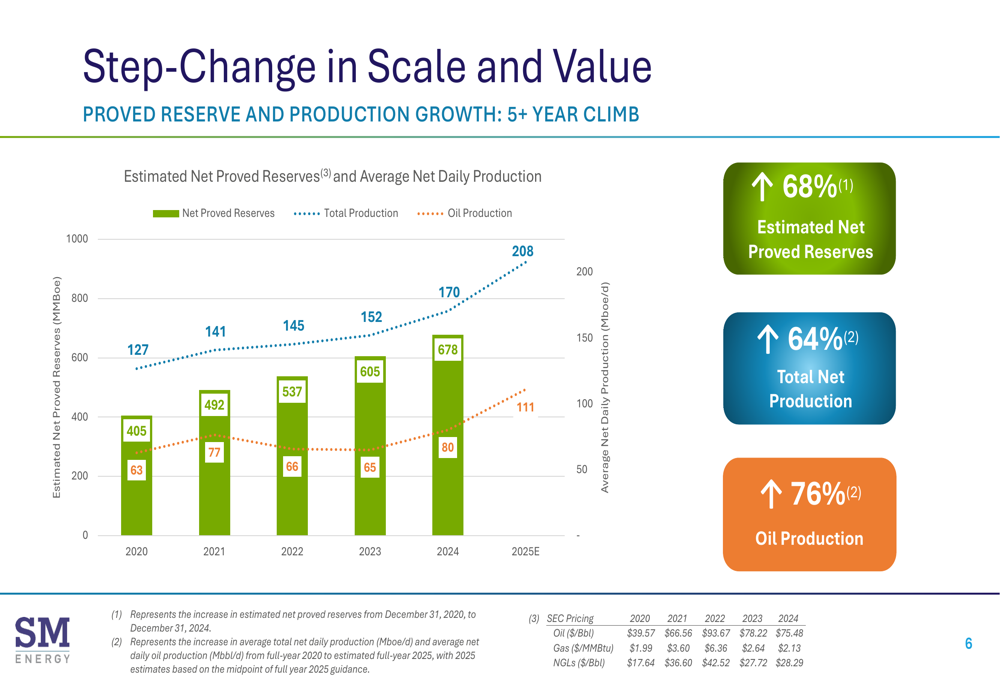

The following chart illustrates this growth trend:

Since 2020, SM Energy has achieved a 68% increase in estimated net proved reserves and a 64% increase in total net production, with oil production growing by 76%. This step-change in scale has been accomplished while maintaining capital discipline and focusing on shareholder returns.

Operational Excellence Across Basins

SM Energy’s portfolio spans three core basins – Uinta Basin, Midland Basin, and South Texas – each contributing to the company’s strong performance through technological innovation and operational efficiencies.

In the Uinta Basin, SM Energy has completed integration of recently acquired assets and is seeing strong well performance, with 22 Lower Cube wells reaching initial 30-day production rates averaging 1,386 Boe/d per well with 89% oil content. The company has implemented several efficiency initiatives, including a conveyor system at its operated sand mine that delivers $15-30 per lateral foot in savings.

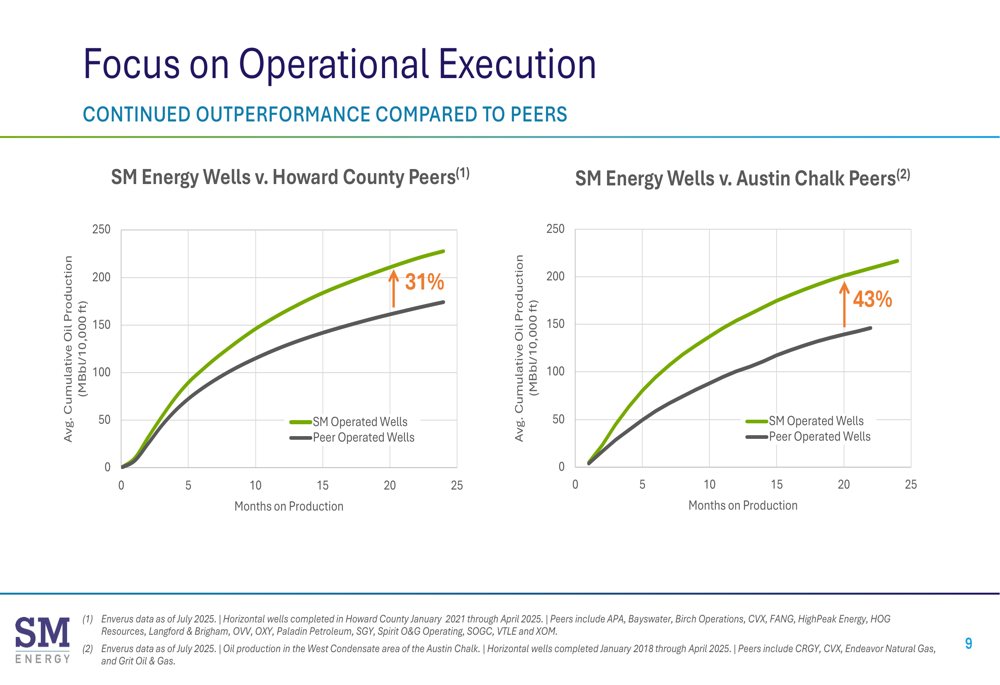

The company’s wells are outperforming peers in key operational regions, as shown in the following comparison:

SM Energy’s wells are demonstrating approximately 31% better performance than peers in Howard County and 43% better performance in the Austin Chalk region. This outperformance reflects the company’s technical expertise and focus on operational execution.

In Texas, SM Energy has achieved significant efficiency gains, including a 19% increase in average daily drilling footage, a 64% increase in average daily completed footage, and a 15% reduction in average per-foot drilling and completion costs.

Financial Strategy and Capital Allocation

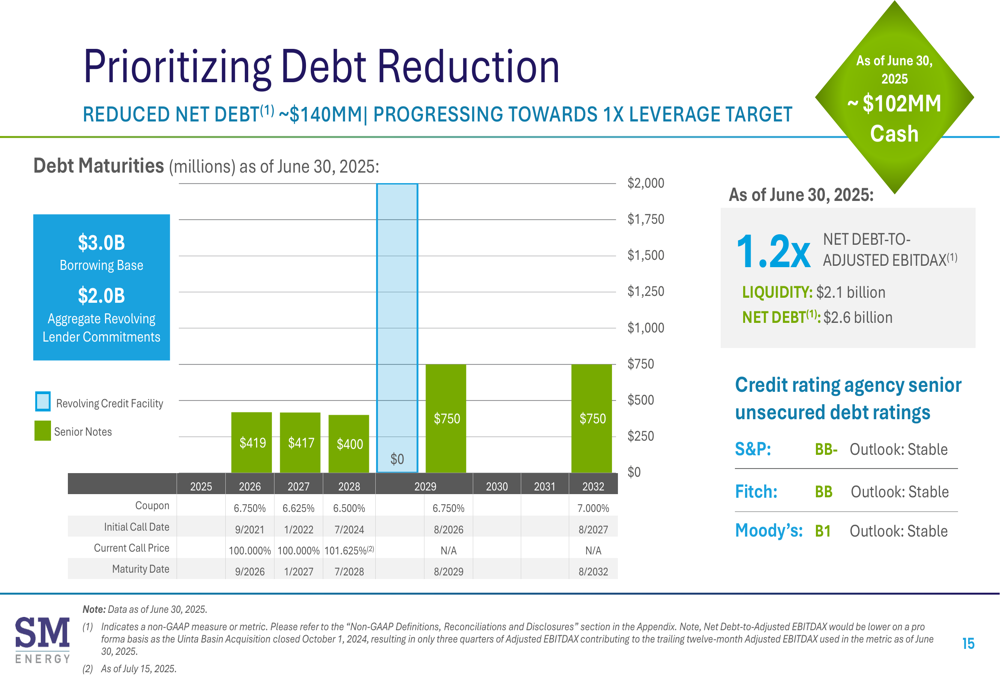

SM Energy continues to prioritize debt reduction as part of its financial strategy, reducing net debt by approximately $140 million in Q2 2025. The company is progressing toward its target of 1.0x leverage, with current net debt-to-adjusted EBITDAX at 1.2x as of June 30, 2025.

The following chart details the company’s debt reduction progress and maturity schedule:

With $102 million in cash and $2.1 billion in liquidity as of June 30, 2025, SM Energy is well-positioned to manage its $2.6 billion in net debt while continuing to return capital to shareholders.

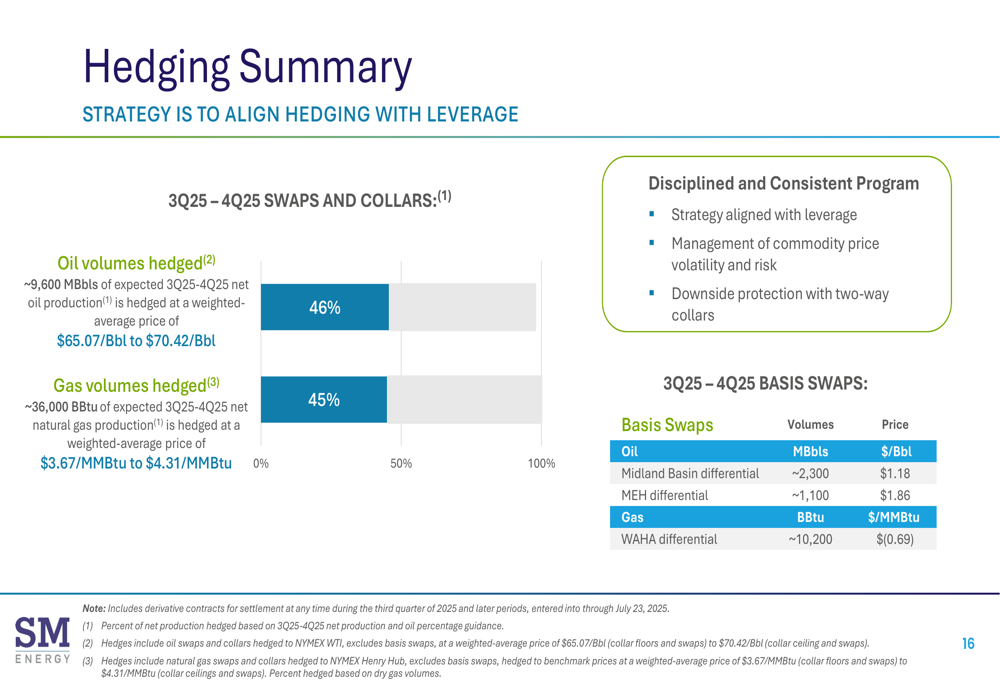

The company has implemented a disciplined hedging program to protect cash flows and support its capital allocation strategy, with approximately 46% of oil production and 45% of gas production hedged for the second half of 2025.

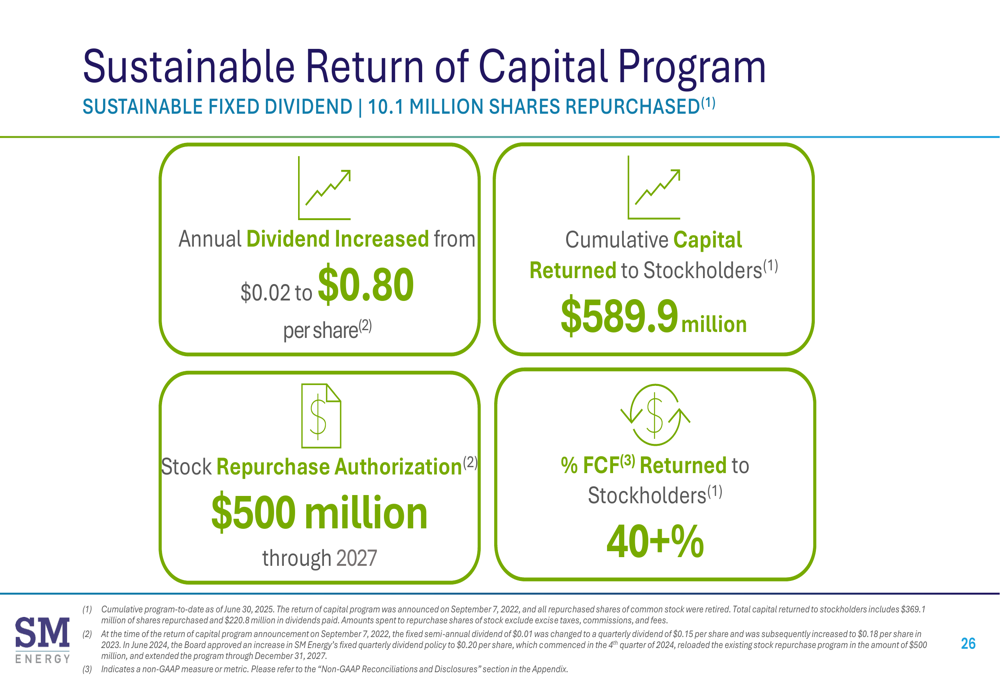

In addition to debt reduction, SM Energy has established a sustainable return of capital program for shareholders, increasing its annual dividend from $0.02 to $0.80 per share and authorizing a $500 million stock repurchase program through 2027.

To date, the company has repurchased 10.1 million shares and returned a cumulative $589.9 million to stockholders, representing over 40% of free cash flow.

Forward Guidance and Strategic Outlook

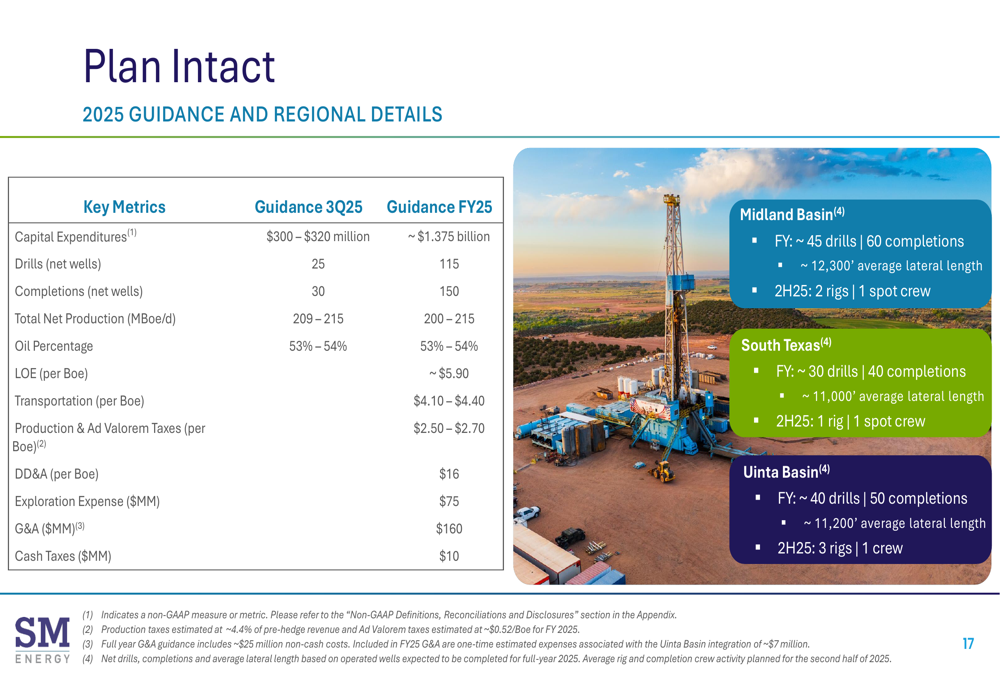

SM Energy reaffirmed its 2025 guidance, maintaining its capital expenditure target of approximately $1.375 billion to drill 115 net wells and complete 150 net wells across its three core basins. The company expects total net production of 200-215 MBoe/d with oil comprising 53-54% of the mix.

The detailed guidance breakdown by region is shown below:

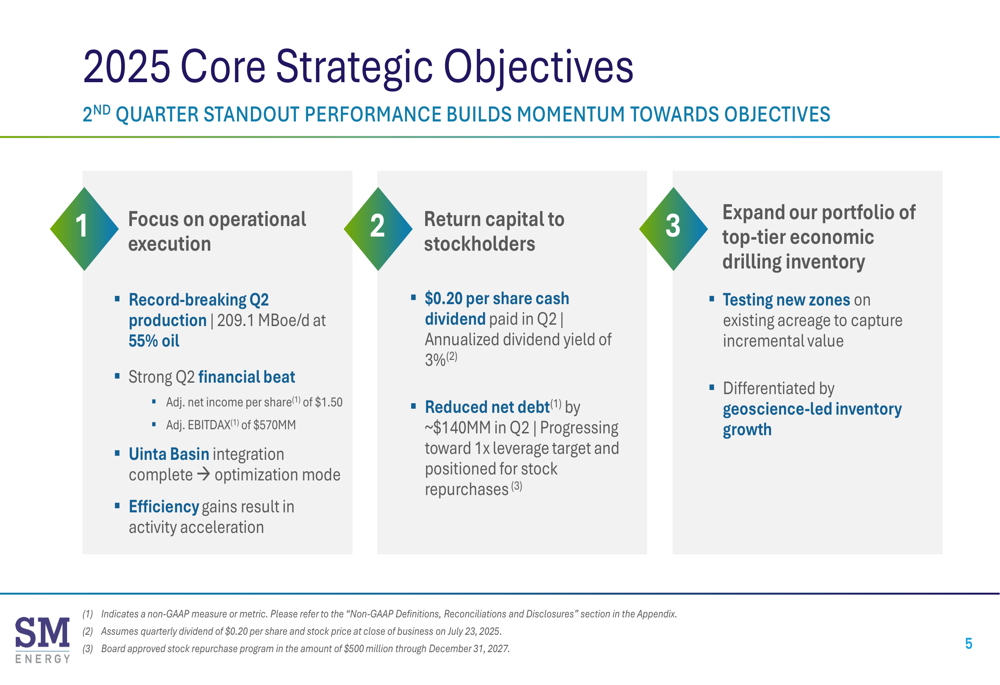

Looking ahead, SM Energy’s strategic objectives remain focused on operational execution, returning capital to stockholders, and expanding its portfolio of top-tier economic drilling inventory. The company is testing new zones on existing acreage to capture incremental value and is leveraging its geoscience capabilities to drive inventory growth.

While the presentation highlights continued growth and operational excellence, the earnings call transcript indicates a more cautious outlook for 2026, with anticipated flat BOE production and slightly reduced capital expenditures. This reflects the company’s adaptability to changing market conditions, particularly in the natural gas sector where rapid supply responses could impact pricing.

Despite strong operational performance, SM Energy’s stock has experienced significant volatility, with a 47% decline over the past year according to earnings reports. This disconnect between operational results and market performance underscores the challenges facing energy companies in the current environment, where investor sentiment can be influenced by broader market factors beyond company-specific fundamentals.

As SM Energy continues to execute its strategic plan, investors will be watching closely to see if the company’s operational excellence and financial discipline can ultimately translate into sustained share price appreciation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.