Verizon to cut 15,000 jobs amid growing competition pressures - WSJ

Introduction & Market Context

SmartRent Inc. (NYSE:SMRT) presented its third quarter fiscal year 2025 earnings on November 5, revealing a company in transition. The smart home technology provider’s stock responded positively to the results, rising 8.89% to $1.47 in pre-market trading despite a revenue miss. The company’s strategic pivot from hardware-led growth to a SaaS-focused business model is showing early signs of success, with improved profitability metrics and strong customer retention.

Quarterly Performance Highlights

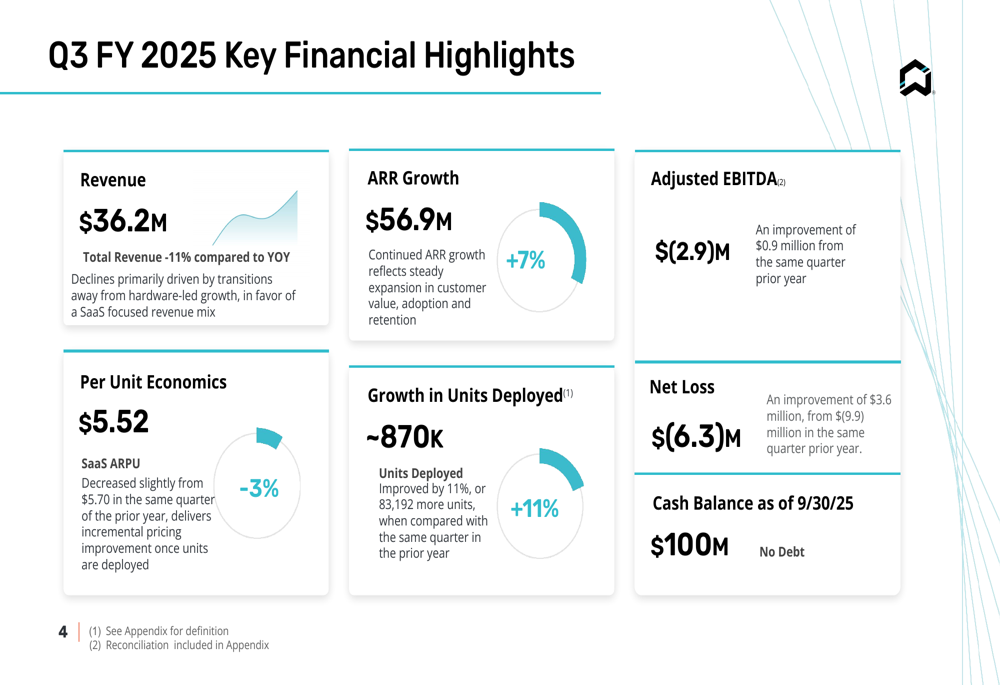

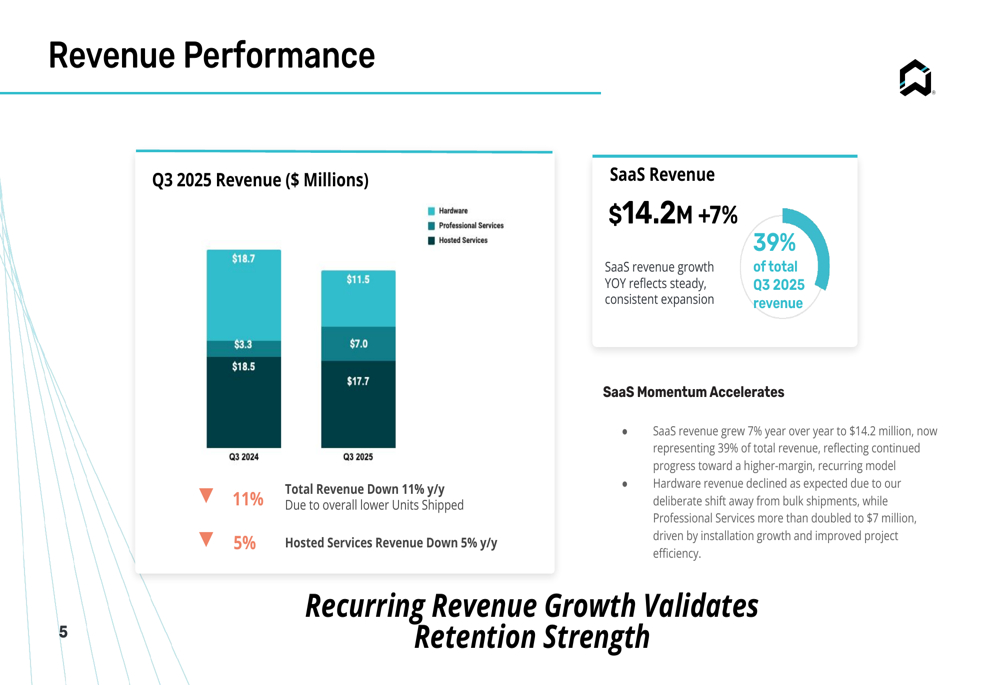

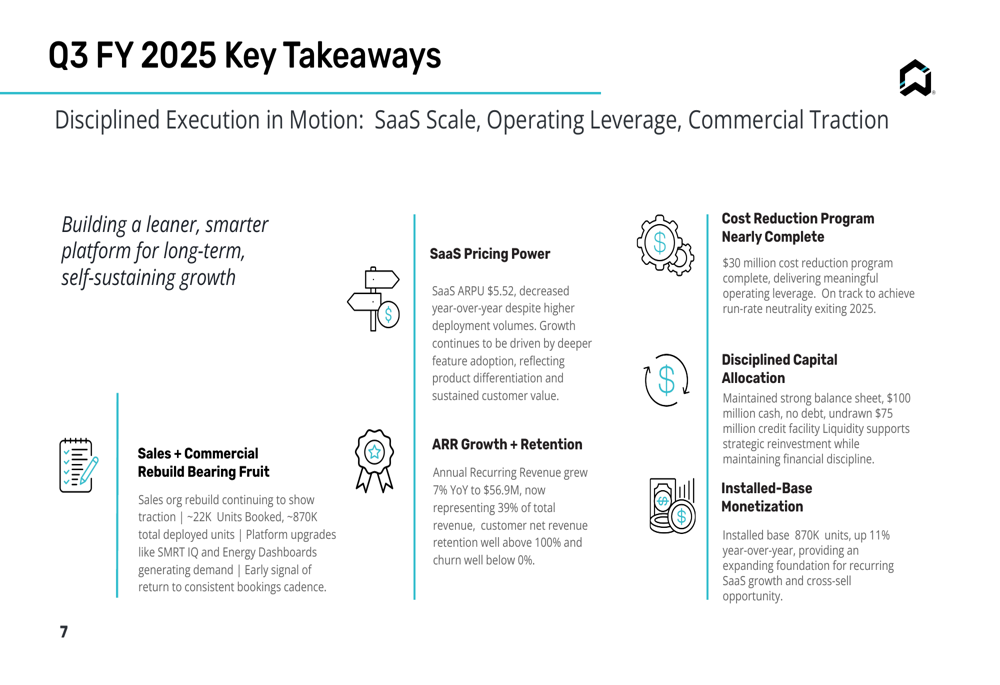

SmartRent reported total revenue of $36.2 million for Q3 2025, representing an 11% decrease year-over-year, primarily due to the company’s deliberate transition away from hardware sales. However, SaaS revenue grew by 7% to $14.2 million, now comprising 39% of total revenue, highlighting the company’s successful shift toward recurring revenue streams.

As shown in the following financial highlights:

The company’s net loss improved significantly to $6.3 million, a $3.6 million improvement from the $9.9 million loss reported in Q3 2024. Similarly, Adjusted EBITDA loss narrowed to $2.9 million, an improvement of $0.9 million compared to the same period last year. These improvements reflect SmartRent’s successful implementation of its $30 million cost reduction plan, which is now nearly complete.

The revenue breakdown shows the company’s transition in progress, with hardware revenue declining while SaaS revenue continues to grow:

Strategic Initiatives

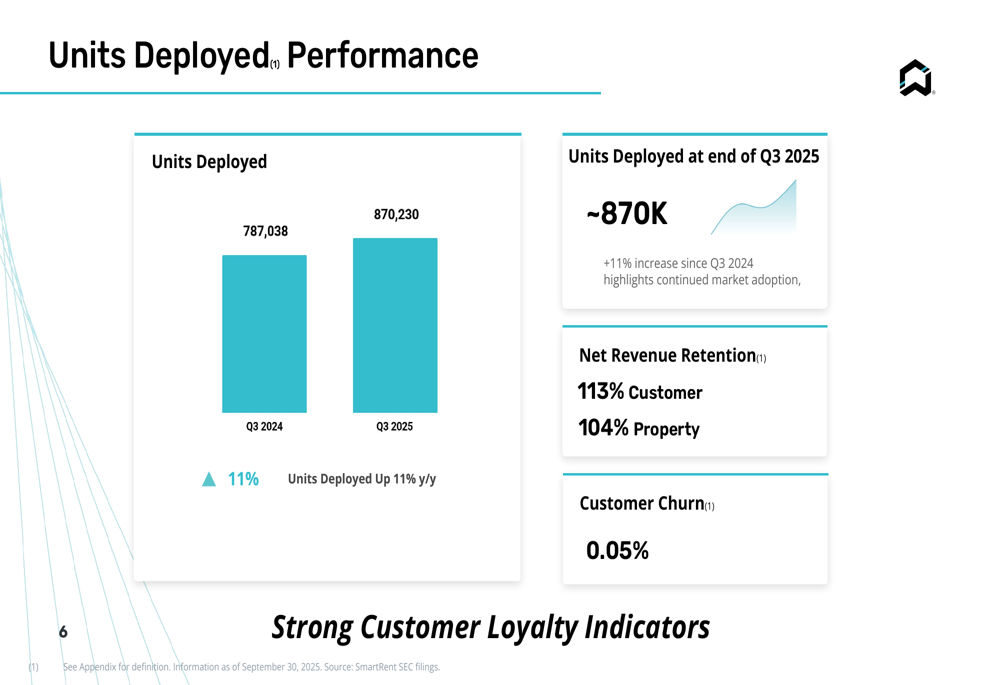

SmartRent’s strategic focus on building its installed base continues to yield results, with approximately 870,000 units deployed as of Q3 2025, representing an 11% increase year-over-year. This growth in deployed units provides a foundation for future SaaS revenue expansion.

The company’s deployment performance is illustrated in the following chart:

Customer retention metrics remain exceptionally strong, with churn at just 0.05% and net revenue retention rates of 113% for customers and 104% for properties. These figures indicate high satisfaction levels among existing clients and successful upselling efforts.

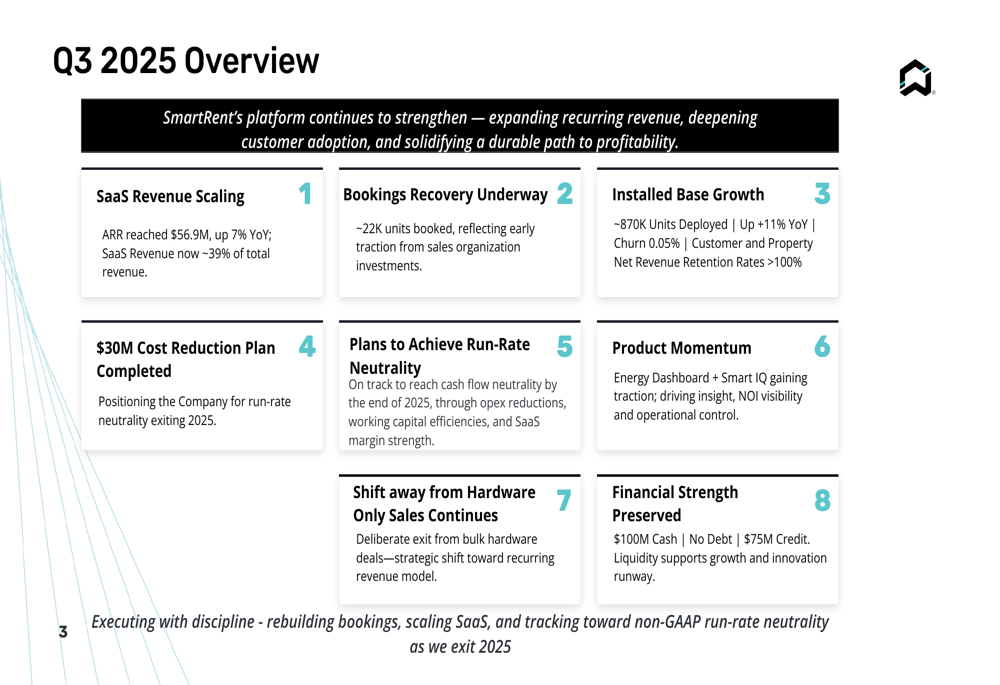

SmartRent’s comprehensive overview of Q3 2025 highlights both financial performance and strategic progress:

The company’s bookings recovery is underway, with approximately 22,000 units booked during the quarter, reflecting early traction from investments in the sales organization. Additionally, SmartRent is seeing momentum with its Energy Dashboard and Smart IQ products, which are driving insights, NOI visibility, and operational control for property managers.

Detailed Financial Analysis

SmartRent maintains a strong financial position with $100 million in cash and no debt, providing ample liquidity to support growth initiatives. The company also has access to a $75 million credit facility, further strengthening its financial flexibility.

Annual Recurring Revenue (ARR) reached $56.9 million, up 7% year-over-year, demonstrating the company’s ability to grow its subscription business. SaaS ARPU (Average Revenue Per Unit) was $5.52, slightly down from $5.70 in the same quarter of the prior year, but still representing a healthy revenue stream per deployed unit.

The company’s key takeaways from Q3 2025 emphasize disciplined execution across multiple fronts:

Forward-Looking Statements

SmartRent is on track to achieve run-rate neutrality by the end of 2025, through a combination of operating expense reductions, working capital efficiencies, and SaaS margin strength. The company’s deliberate exit from bulk hardware deals represents a strategic shift toward a recurring revenue model that should provide more predictable and profitable growth in the long term.

The improving financial metrics, combined with the growing installed base and strong customer retention, position SmartRent well for future growth as it completes its transition to a SaaS-focused business model. With its cost reduction program nearly complete and bookings recovery underway, the company appears to be successfully navigating its strategic transformation despite the short-term revenue headwinds.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.