Gold rally takes a breather amid Gaza ceasefire, Fed minutes

Introduction & Market Context

Snowflake Inc . (NYSE:SNOW) delivered strong first-quarter fiscal year 2026 results, with product revenue growing 26% year-over-year to $996.8 million. The company’s stock responded positively to the results, rising 5.58% in after-hours trading to $189.12, following a 2.06% decline during the regular session.

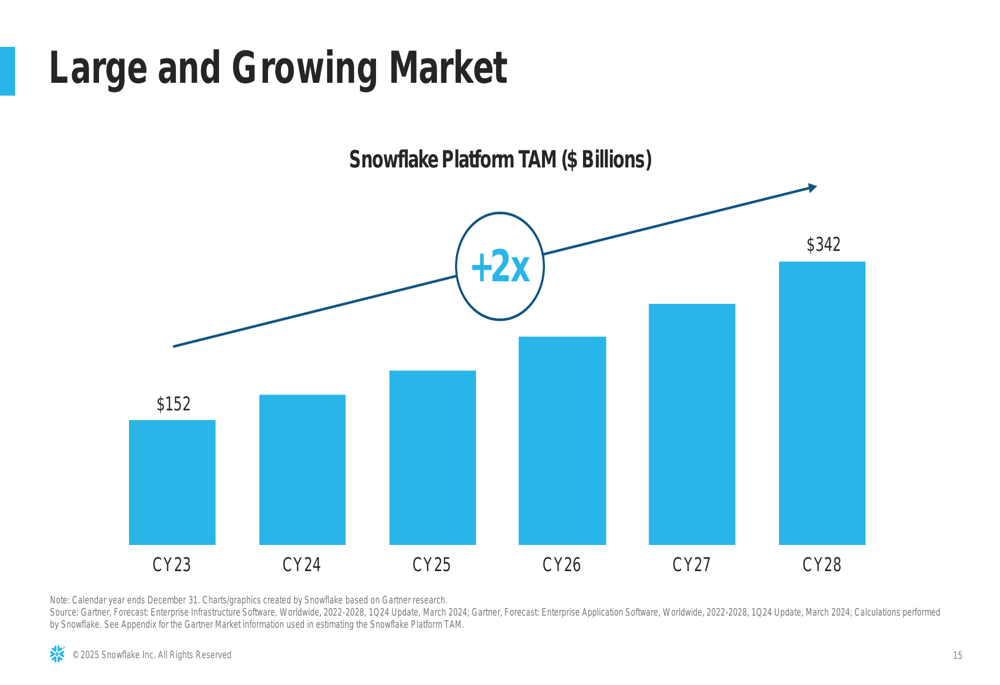

The data cloud company continues to position itself at the intersection of data management and artificial intelligence, emphasizing that "There Is No AI Strategy Without a Data Strategy" throughout its investor presentation. This focus comes as Snowflake projects its total addressable market to more than double from $152 billion in 2023 to $342 billion by 2028.

As shown in the following chart of Snowflake’s market opportunity:

Quarterly Performance Highlights

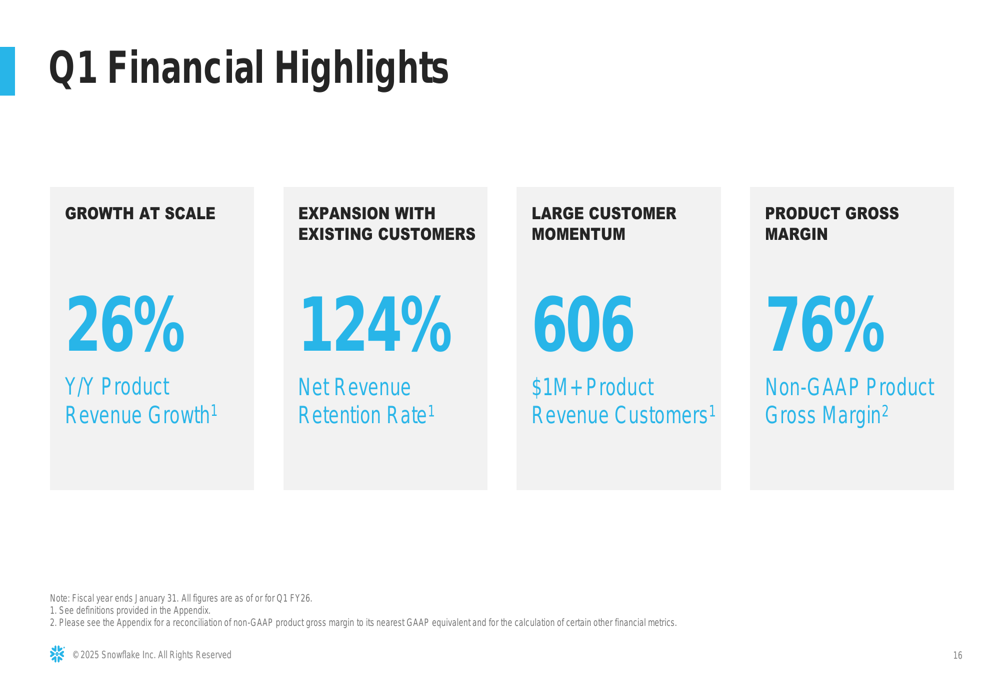

Snowflake’s Q1 FY26 results demonstrated continued momentum across key metrics. The company highlighted four main areas of strength: revenue growth, customer expansion, large customer acquisition, and strong margins.

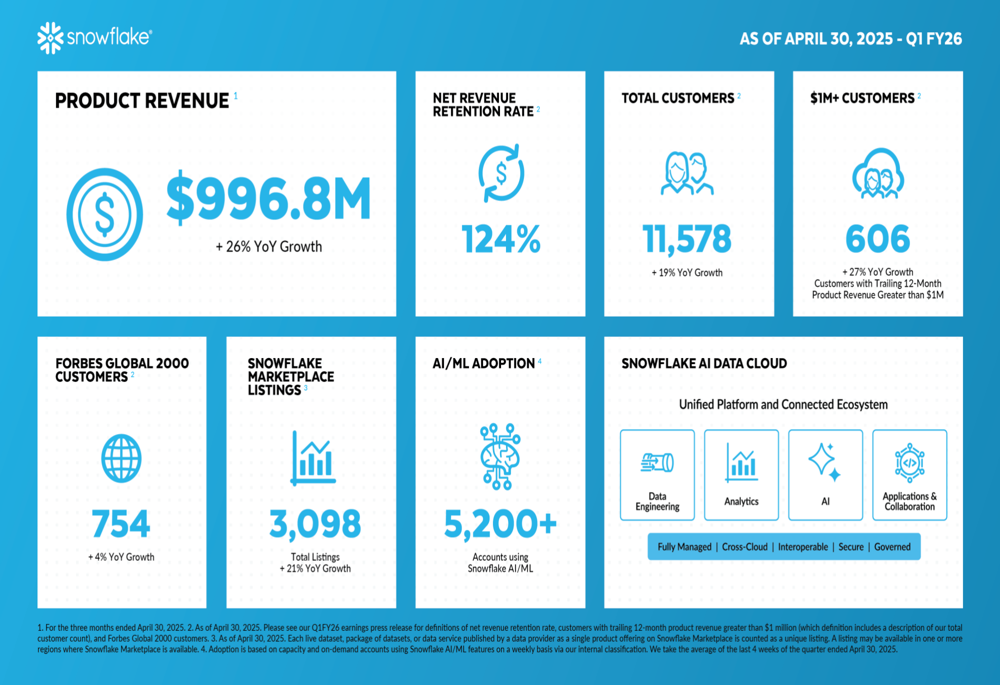

The company reported 26% year-over-year product revenue growth, a net revenue retention rate of 124%, and 606 customers with over $1 million in product revenue (up 27% year-over-year). Additionally, Snowflake maintained a healthy non-GAAP product gross margin of 76%.

As illustrated in this summary of Q1 financial highlights:

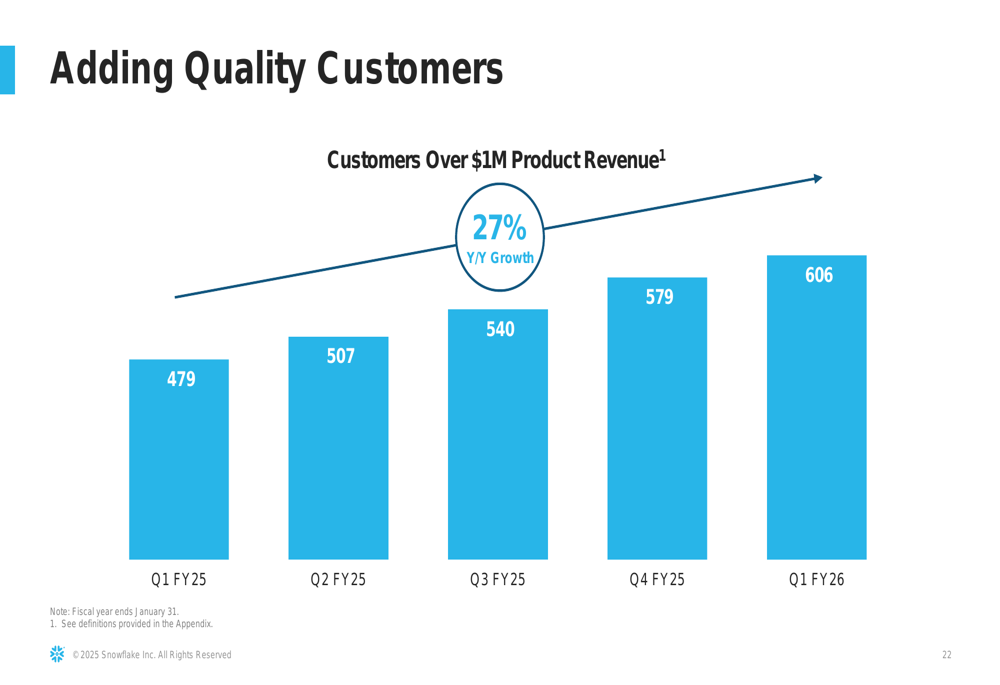

The company’s customer base continues to expand, with total customers reaching 11,578 (up 19% year-over-year) and Forbes Global 2000 customers increasing to 754 (up 4% year-over-year). Particularly noteworthy is the growth in high-value customers, with those generating over $1 million in product revenue increasing 27% year-over-year to 606.

The following chart shows the steady growth in Snowflake’s $1M+ customer base:

Strategic Initiatives

Snowflake’s strategic focus centers on positioning its platform as the foundation for AI and data strategies. The company emphasized its ability to unify data across various architectures, including data warehouses, data lakes, and data lakehouses, while supporting structured, semi-structured, and unstructured data formats.

The company highlighted its extensive partner ecosystem, which includes major technology providers and consulting firms. This network of partnerships enhances Snowflake’s market reach and integration capabilities.

As shown in this comprehensive view of Snowflake’s partner ecosystem:

Snowflake’s customer base spans numerous industries and includes many prominent global organizations, demonstrating the platform’s broad appeal and versatility.

The following image showcases the diversity of Snowflake’s customer base:

The company also reported significant adoption of its AI and machine learning capabilities, with over 5,200 accounts using Snowflake AI/ML features and 3,098 marketplace listings (up 21% year-over-year). Additionally, 39% of customers are engaged in data sharing activities, highlighting the platform’s collaborative capabilities.

Detailed Financial Analysis

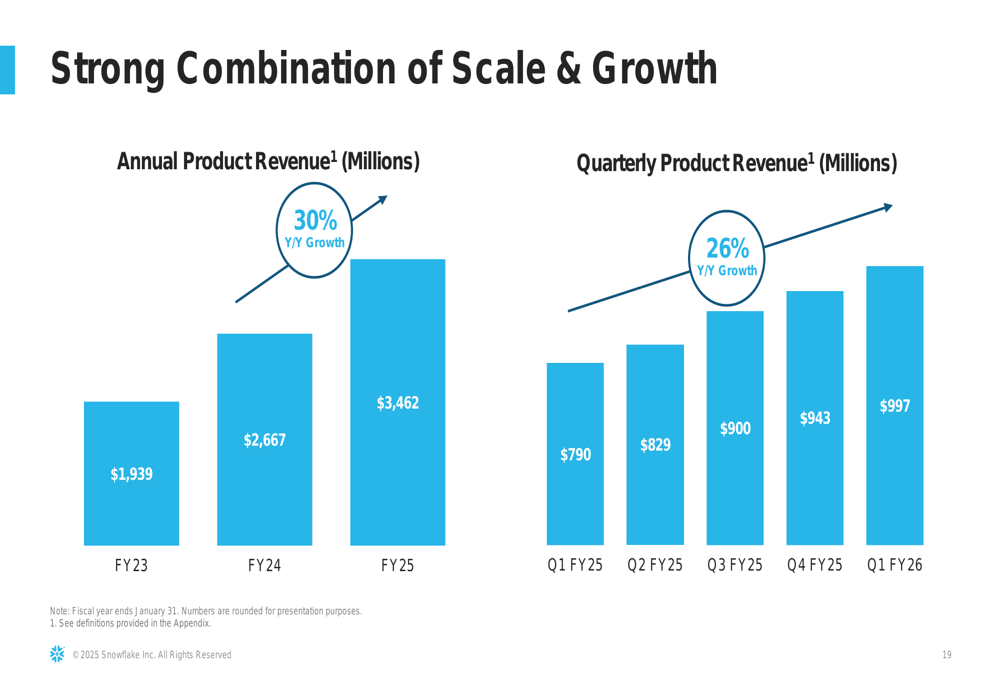

Snowflake’s revenue growth remains strong, though the pace has moderated compared to previous years. Annual product revenue has grown from $1.94 billion in FY23 to $2.67 billion in FY24 and $3.46 billion in FY25, representing a 30% year-over-year increase in FY25.

Quarterly product revenue shows consistent growth, reaching $997 million in Q1 FY26, up from $790 million in Q1 FY25:

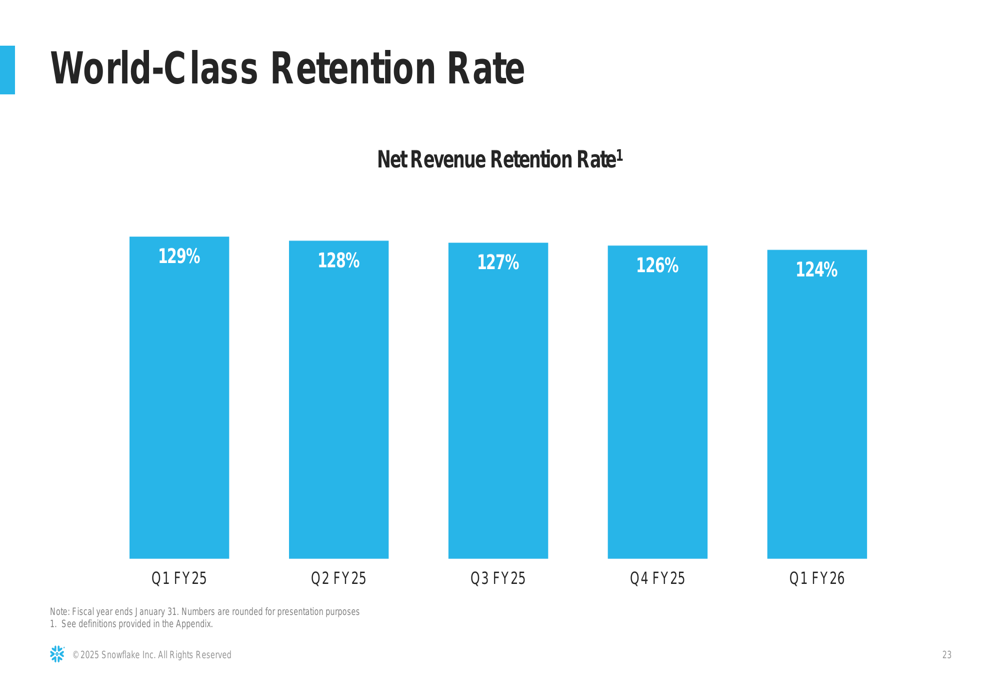

The company’s net revenue retention rate, while still impressive at 124%, has shown a gradual decline from 129% in Q1 FY25. This metric reflects the company’s ability to expand revenue from existing customers.

On the profitability front, Snowflake has improved its non-GAAP operating margin to 9% in Q1 FY26 from 4% in Q1 FY25, demonstrating increased operational efficiency. However, the non-GAAP adjusted free cash flow margin decreased to 20% from 44% in the same period last year.

Remaining performance obligations (RPO), which represent contracted future revenue, stood at $6.69 billion as of Q1 FY26, with 50% expected to be recognized as revenue within the next twelve months. This provides visibility into Snowflake’s future revenue streams.

Forward-Looking Statements

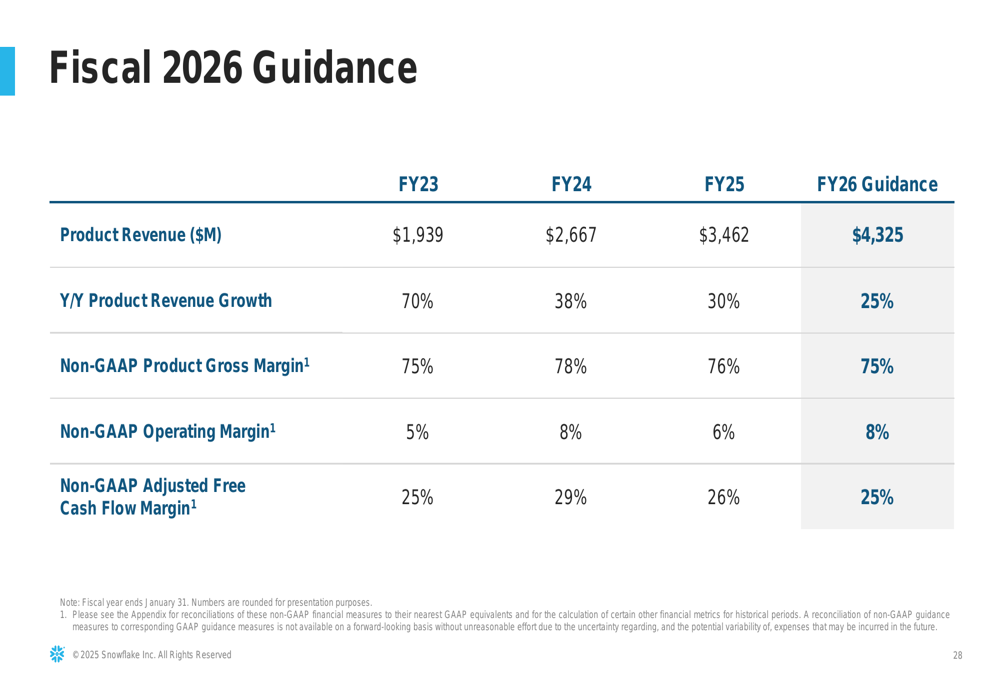

Looking ahead, Snowflake provided guidance for fiscal year 2026, projecting product revenue of $4.325 billion, representing 25% year-over-year growth. The company expects to maintain a non-GAAP product gross margin of 75% and improve its non-GAAP operating margin to 8% for the full year.

The following table outlines Snowflake’s fiscal 2026 guidance alongside historical performance:

Snowflake’s comprehensive financial summary as of Q1 FY26 showcases the company’s key metrics and strategic positioning:

Snowflake continues to invest in growth while balancing profitability. The company increased its total headcount to 8,240 in Q1 FY26 from 7,296 in Q1 FY25, with sales and marketing representing the largest functional area at 3,683 employees.

From a geographic perspective, Snowflake’s revenue remains heavily concentrated in the Americas (78%), with EMEA (16%) and Asia-Pacific/Japan (6%) making up the remainder. This distribution has remained relatively stable over recent quarters, suggesting potential opportunities for international expansion.

As Snowflake continues to execute on its AI-focused data strategy, the company appears well-positioned to capitalize on the growing demand for integrated data and AI solutions, though it faces intense competition in the rapidly evolving cloud data platform market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.