CTAs keep buying Treasuries, gold longs face stop-loss risk: BofA

Introduction & Market Context

SoftwareOne Holding (SWX:SWON) reported mixed first quarter 2025 results on May 21, showing revenue decline but improved profitability as the company’s cost reduction program exceeded targets. The Swiss IT services provider saw its shares rise 5.77% to close at CHF 7.33 following the presentation, suggesting investors were encouraged by margin improvements and the upcoming Crayon acquisition despite top-line challenges.

Quarterly Performance Highlights

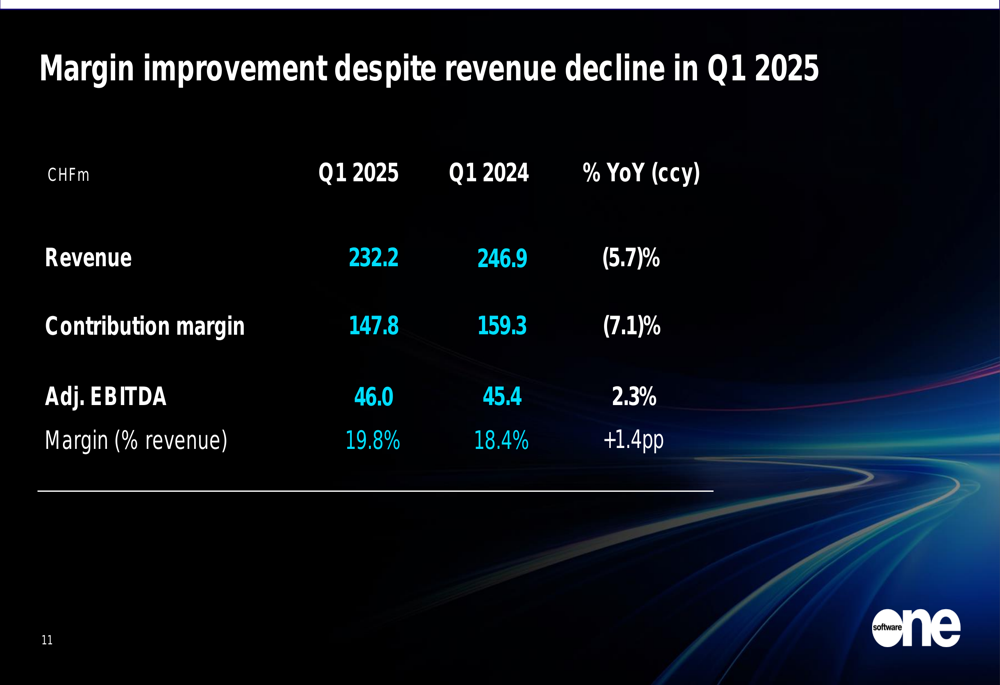

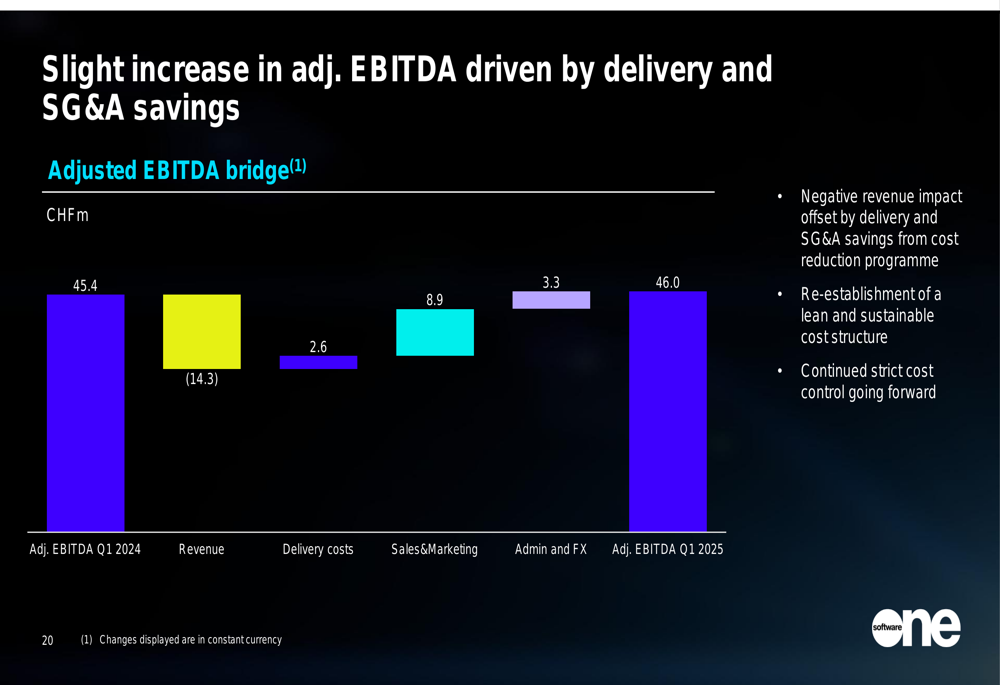

SoftwareOne reported Q1 2025 revenue of CHF 232.2 million, down 5.7% year-over-year in constant currency, while adjusted EBITDA increased by 2.3% to CHF 46.0 million. The adjusted EBITDA margin improved to 19.8%, up from 18.4% in the same period last year.

As shown in the following financial summary:

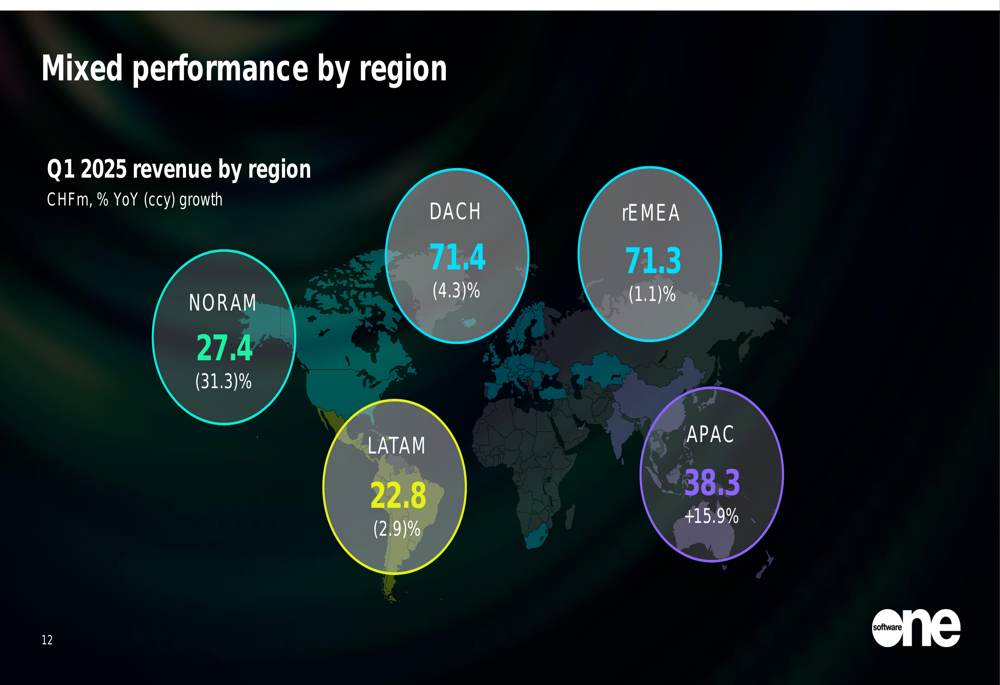

The company faced significant regional disparities in performance. NORAM (North America) showed the steepest decline at -31.3%, while APAC demonstrated strong growth at 15.9%. Other regions showed modest declines: DACH (-4.3%), rest of EMEA (-1.1%), and LATAM (-2.9%).

Business Segment Performance

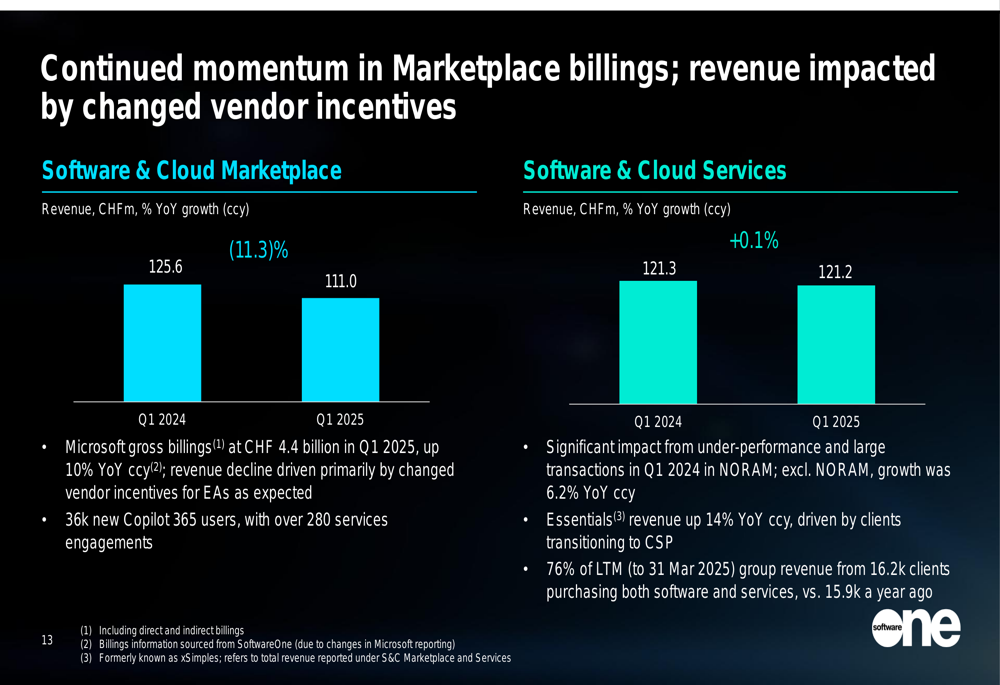

SoftwareOne’s two main business segments showed divergent performance. Software (ETR:SOWGn) & Cloud Marketplace revenue fell 11.3% to CHF 111.0 million, impacted by changes in vendor incentives. However, Microsoft (NASDAQ:MSFT) gross billings grew 10% to CHF 4.4 billion, and the company added 36,000 new Copilot 365 users.

Meanwhile, Software & Cloud Services revenue remained essentially flat at CHF 121.2 million (+0.1%), with Essentials revenue growing 14%. The company noted that 76% of last twelve months group revenue came from 16,200 clients purchasing both software and services.

The following chart illustrates this segment performance:

Cost Reduction Program Success

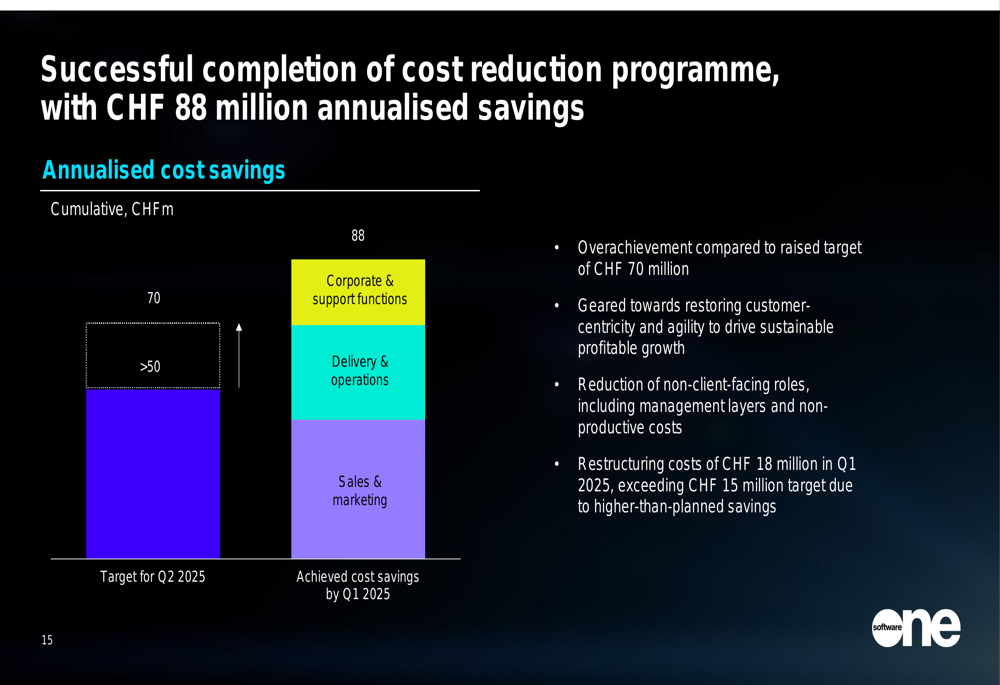

A key highlight of the presentation was the successful completion of SoftwareOne’s cost reduction program, which delivered CHF 88 million in annualized savings, significantly exceeding the raised target of CHF 70 million. The program focused on reducing non-client-facing roles and non-productive costs.

The cost savings breakdown is illustrated here:

These cost reductions helped drive the improvement in adjusted EBITDA despite the revenue decline. The adjusted EBITDA bridge shows how delivery and SG&A savings offset the impact of lower revenue:

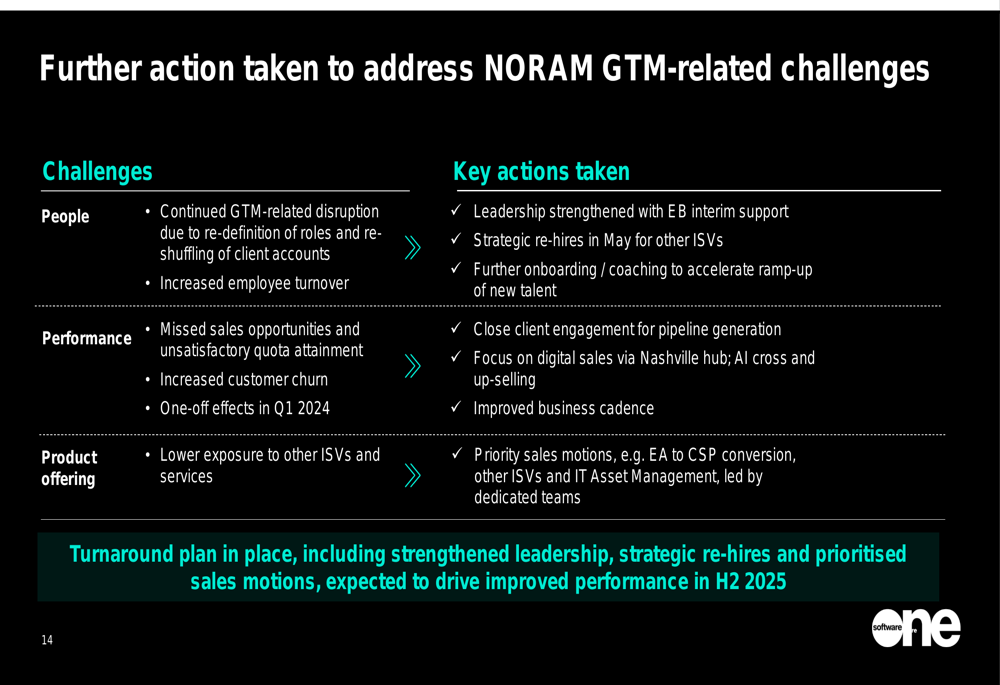

North America Challenges

SoftwareOne continues to face significant challenges in its North American operations, which saw a 31.3% revenue decline. The company cited ongoing GTM (Go-To-Market) disruptions, increased employee turnover, missed sales opportunities, and customer churn.

Management outlined several actions to address these issues, including strengthened leadership, strategic re-hires, improved business cadence, and priority sales motions. The company expects these measures to drive improved performance in the second half of 2025.

Crayon Acquisition Update

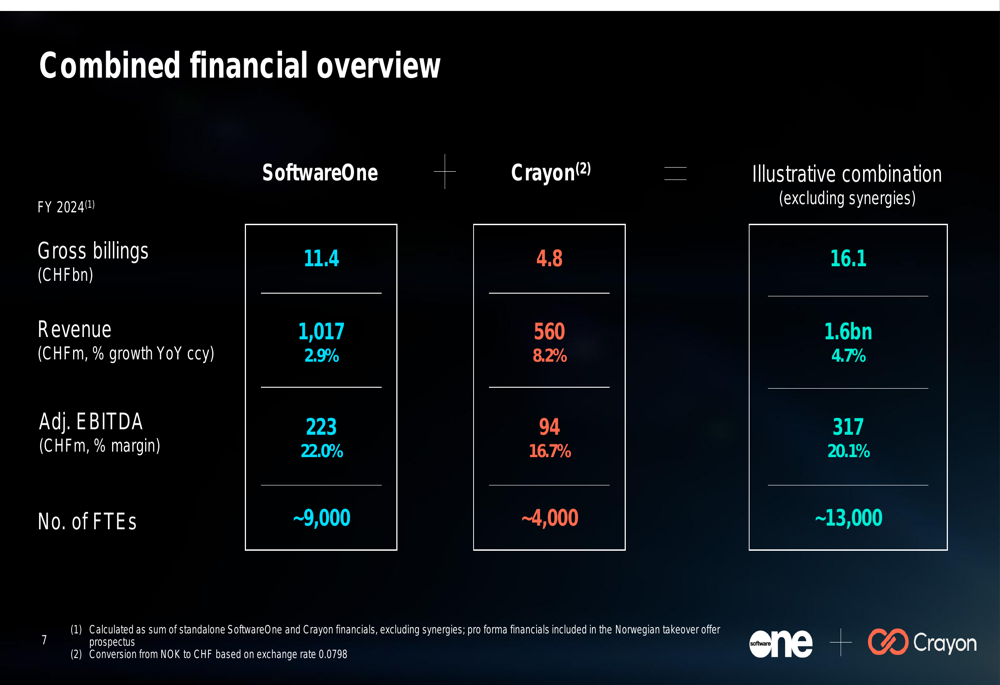

SoftwareOne provided an update on its acquisition of Crayon, which is expected to close in June 2025, subject to remaining regulatory approvals. The company has successfully completed the tender offer, reaching over 90% ownership of Crayon, and received shareholder approval at SoftwareOne’s EGM.

The combined entity would create a significantly larger organization with CHF 16.1 billion in gross billings, CHF 1.6 billion in revenue, and approximately 13,000 employees. The financial overview of the combined entity is shown here:

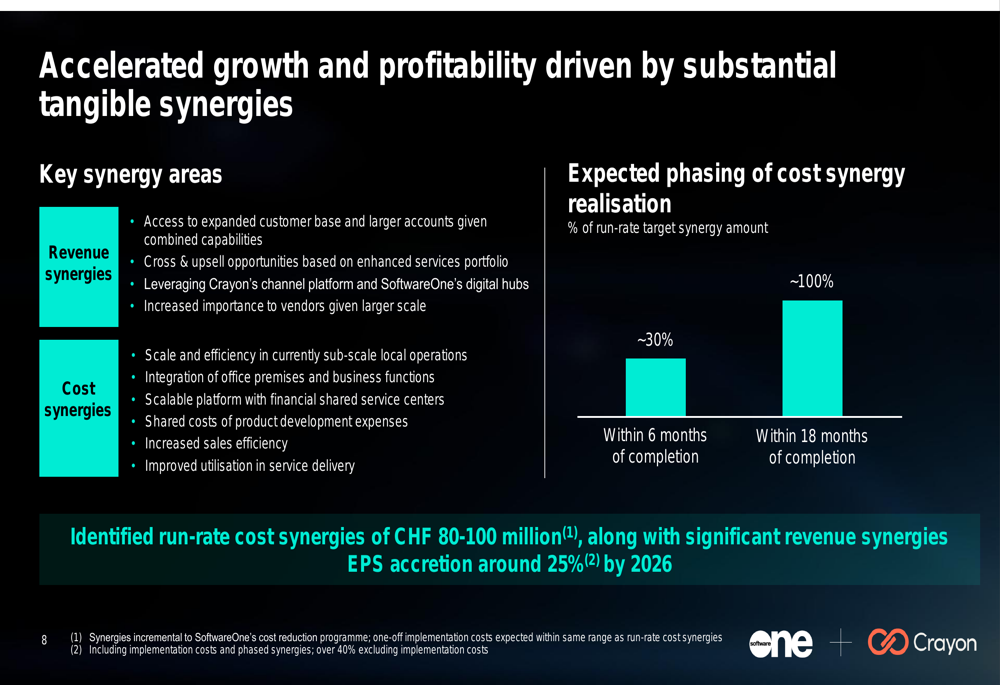

The company expects substantial synergies from the transaction, including run-rate cost synergies of CHF 80-100 million, with approximately 30% to be realized within six months of completion and 100% within 18 months. The acquisition is expected to be EPS accretive by around 25% by 2026.

Strategic Wins and Case Studies

Despite the challenging quarter, SoftwareOne highlighted several strategic wins, including a DKK 1.5 billion (approximately CHF 200 million) four-year framework agreement with the Danish government for cloud services across Microsoft, AWS, and Google (NASDAQ:GOOGL).

The company also showcased a case study with Oxygen Finance, where it implemented an AI-powered solution that reduced data processing times by over 60% and increased procurement data summarization by over 40%.

Forward-Looking Statements

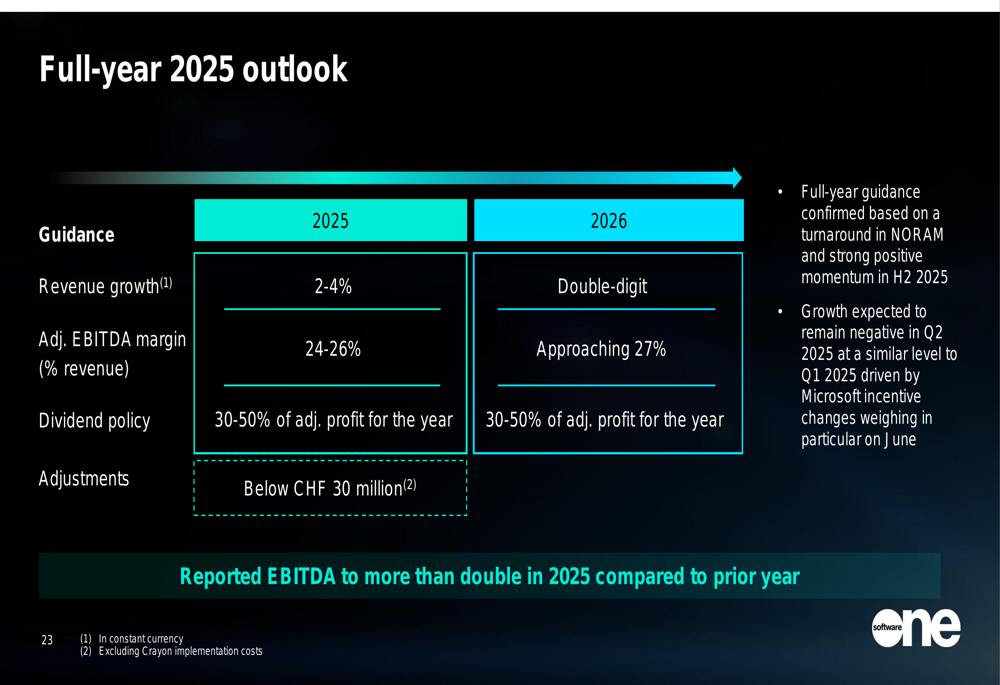

SoftwareOne maintained its full-year 2025 outlook, projecting 2-4% revenue growth and an adjusted EBITDA margin of 24-26%. For 2026, the company expects double-digit revenue growth and an adjusted EBITDA margin approaching 27%.

However, management noted that growth is expected to remain negative in Q2 2025 at a similar level to Q1, particularly impacted by Microsoft incentive changes in June. The company anticipates a turnaround in NORAM and strong positive momentum in the second half of 2025.

Conclusion

SoftwareOne’s Q1 2025 results reflect a company in transition, balancing short-term revenue challenges with improved profitability through cost optimization. The successful cost reduction program has created a more efficient organization, while the pending Crayon acquisition promises to significantly expand the company’s scale and market presence.

The stark regional disparities in performance, particularly the continued struggles in North America versus strong growth in Asia-Pacific, highlight areas requiring management attention. Investors will be watching closely to see if the company can deliver on its promised second-half turnaround and achieve its full-year guidance despite the challenging start to 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.