Street Calls of the Week

Introduction & Market Context

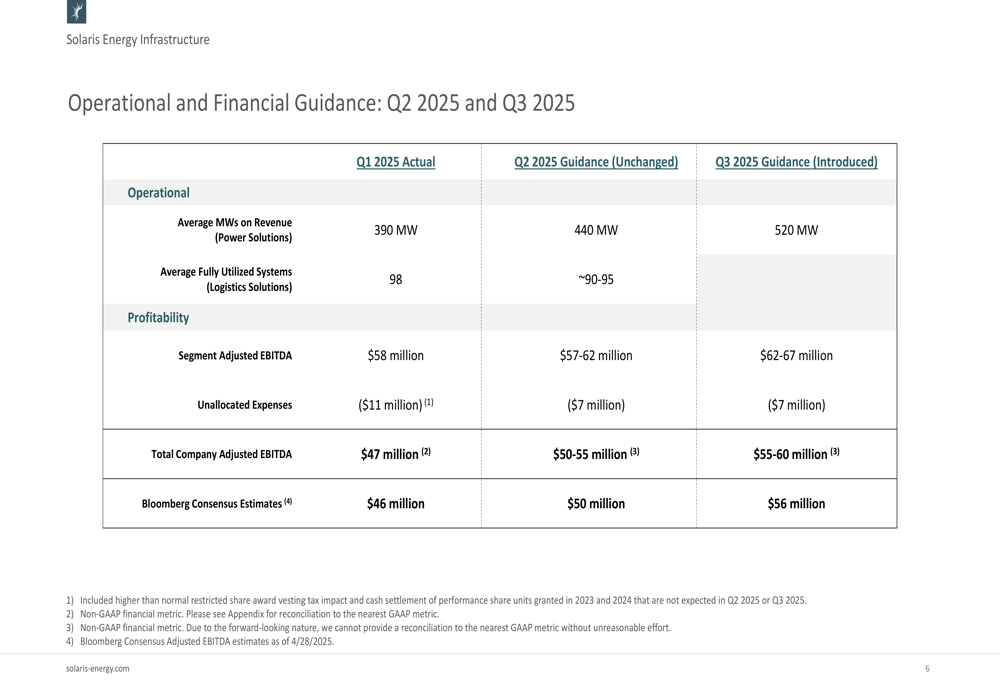

Solaris Energy Infrastructure, Inc. (NYSE:SEI) presented its Q1 2025 earnings results on April 29, 2025, revealing a strategic pivot toward data center power solutions and ambitious fleet expansion plans. The company reported Q1 2025 adjusted EBITDA of $47 million, slightly beating Bloomberg consensus estimates of $46 million, while outlining plans to grow its power generation fleet to 1,700 MW by the first half of 2027.

The company’s presentation highlighted a significant shift in business focus from traditional oilfield services to energy infrastructure, with a particular emphasis on providing power solutions for the rapidly growing data center market. This strategic repositioning comes amid surging demand for reliable power sources to support AI computing infrastructure and ongoing challenges with grid power interconnection queues.

Quarterly Performance Highlights

Solaris Energy Infrastructure delivered solid financial results for the first quarter of 2025, with total company adjusted EBITDA reaching $47 million. The company’s Power Solutions segment, which now forms the core of its business, operated an average of 390 MW during the quarter, generating $58 million in segment adjusted EBITDA.

As shown in the following financial guidance table, Solaris expects continued growth in the coming quarters, with projected total company adjusted EBITDA of $50-55 million in Q2 2025 and $55-60 million in Q3 2025:

The company’s performance reflects its successful transition to energy infrastructure services, with sequential growth in average MWs on revenue projected to increase from 390 MW in Q1 2025 to 440 MW in Q2 and 520 MW in Q3. This growth trajectory underscores the company’s ability to capitalize on increasing demand for flexible power solutions, particularly in the data center sector.

Strategic Initiatives

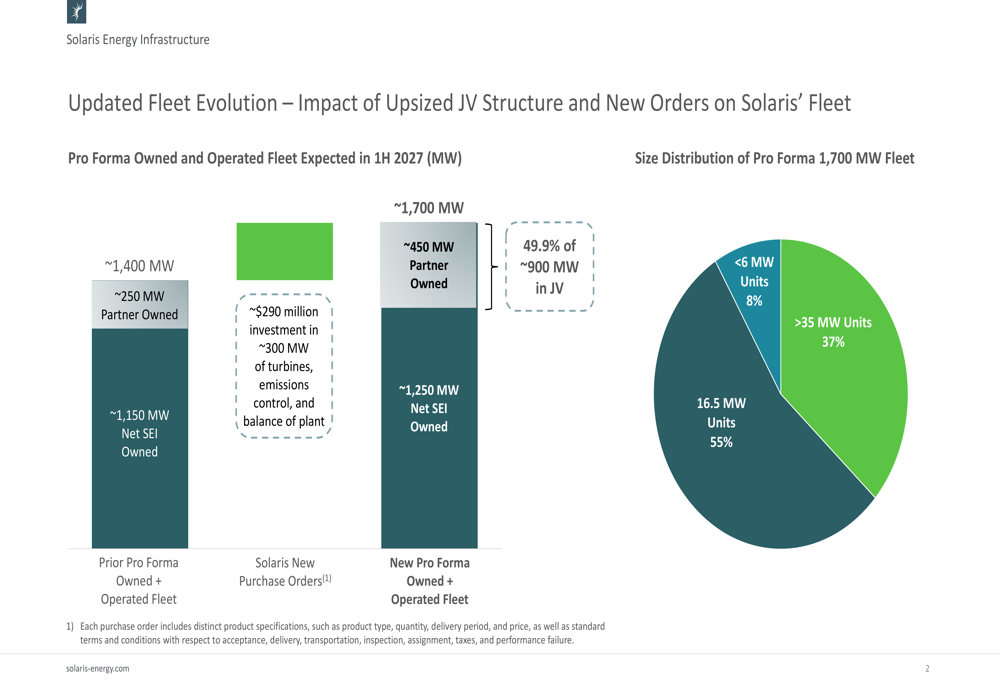

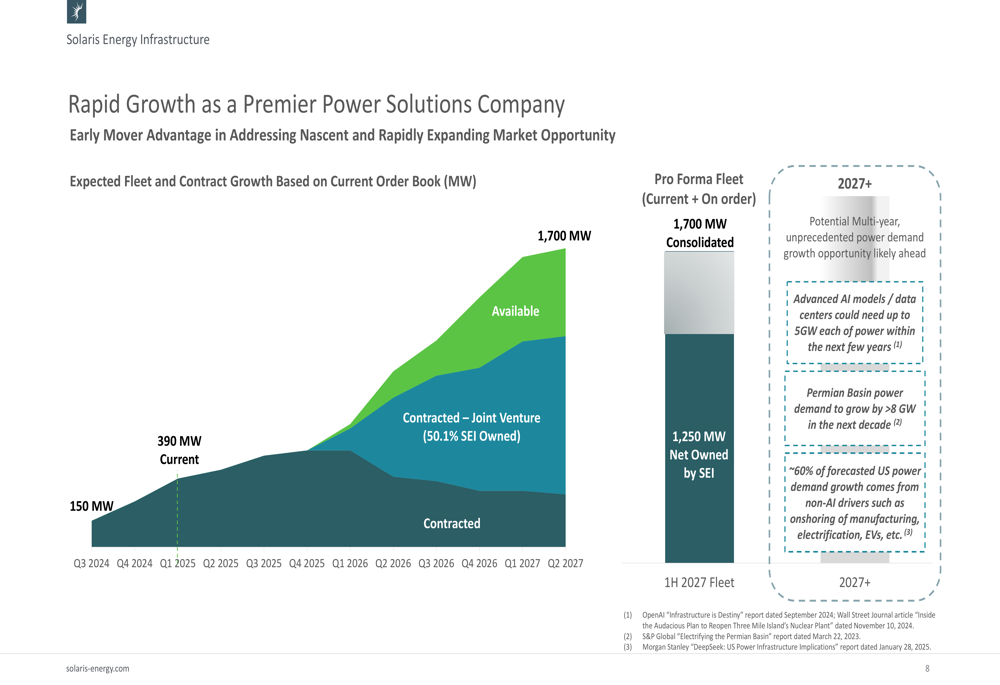

At the center of Solaris’s strategy is an ambitious fleet expansion plan that will increase its power generation capacity from approximately 1,400 MW to 1,700 MW by the first half of 2027. This expansion involves a $290 million investment in approximately 300 MW of new turbines, emissions control equipment, and balance of plant.

The following chart illustrates the company’s updated fleet evolution plan:

The expanded fleet will feature a diverse mix of generation units, with 55% comprised of 16.5 MW units, 37% larger units exceeding 35 MW, and 8% smaller units under 6 MW. Approximately 900 MW of the total fleet will be operated through a joint venture structure, with Solaris maintaining 50.1% ownership.

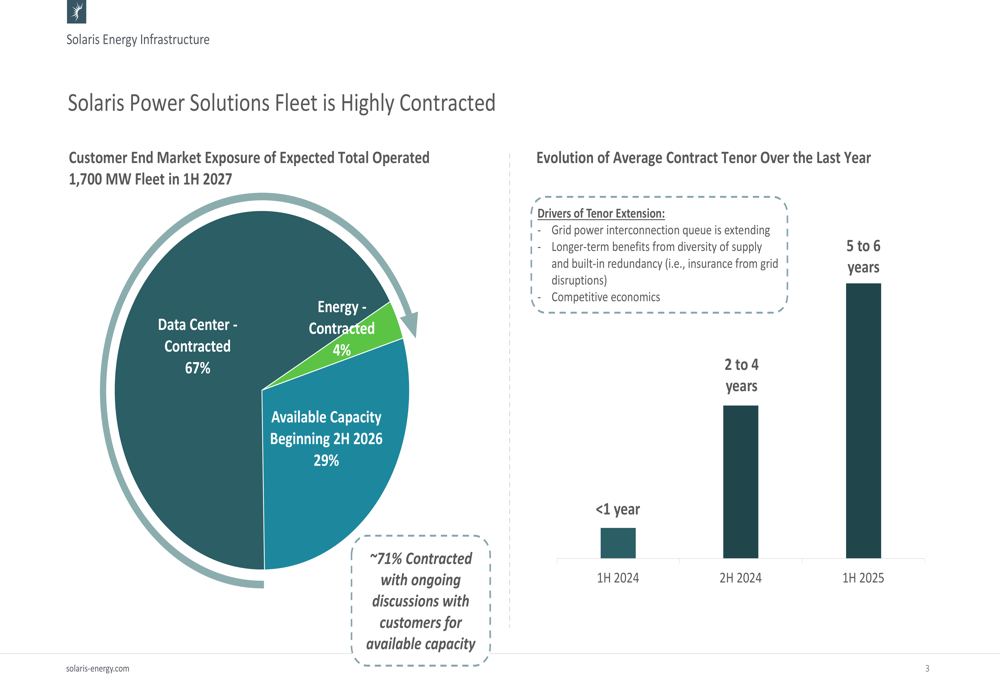

Solaris has successfully secured contracts for 71% of its expected 1,700 MW fleet, with the data center sector representing the largest customer segment at 67% of contracted capacity. The company is actively in discussions with potential customers for the remaining 29% of capacity, which will become available beginning in the second half of 2026.

As illustrated in the following chart of customer end market exposure and contract tenor evolution:

The company has significantly extended its average contract tenor from less than one year in the first half of 2024 to 5-6 years in the first half of 2025. This extension is driven by several factors, including lengthening grid power interconnection queues, the benefits of supply diversity, and competitive economics of Solaris’s solutions.

Financial Analysis

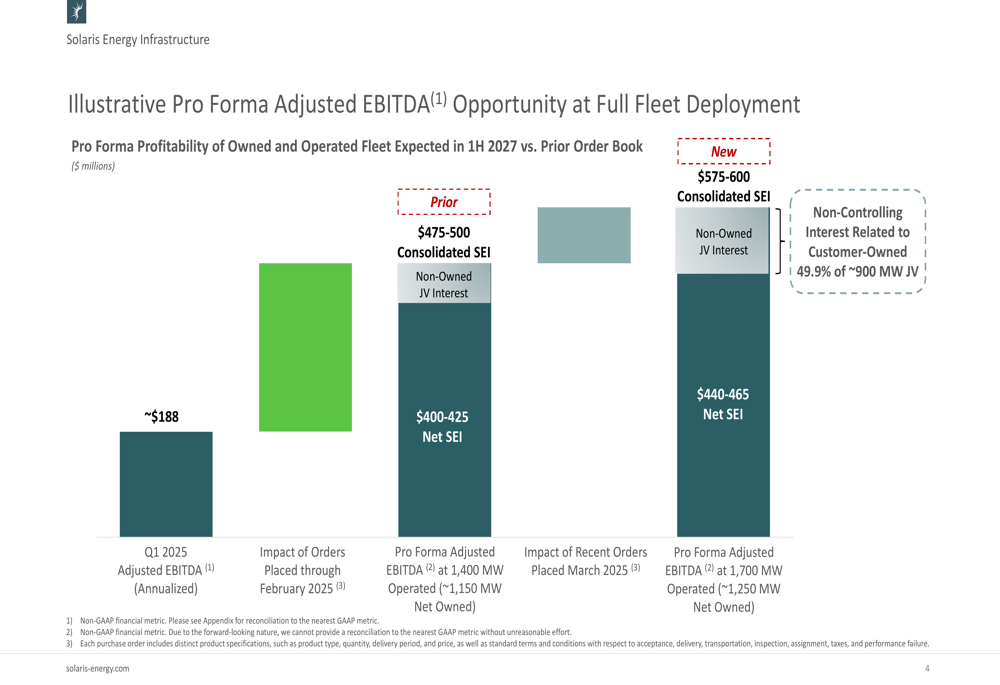

Solaris Energy Infrastructure projects substantial growth in adjusted EBITDA as it deploys its expanded fleet. The company’s Q1 2025 annualized adjusted EBITDA of approximately $188 million is expected to grow significantly with the full deployment of its 1,700 MW operated fleet.

The following chart demonstrates the projected EBITDA growth opportunity:

Upon full deployment of the 1,700 MW operated fleet (with approximately 1,250 MW net owned by SEI), the company expects to generate pro forma adjusted EBITDA of $440-465 million attributable to Solaris, with consolidated SEI adjusted EBITDA reaching $475-500 million.

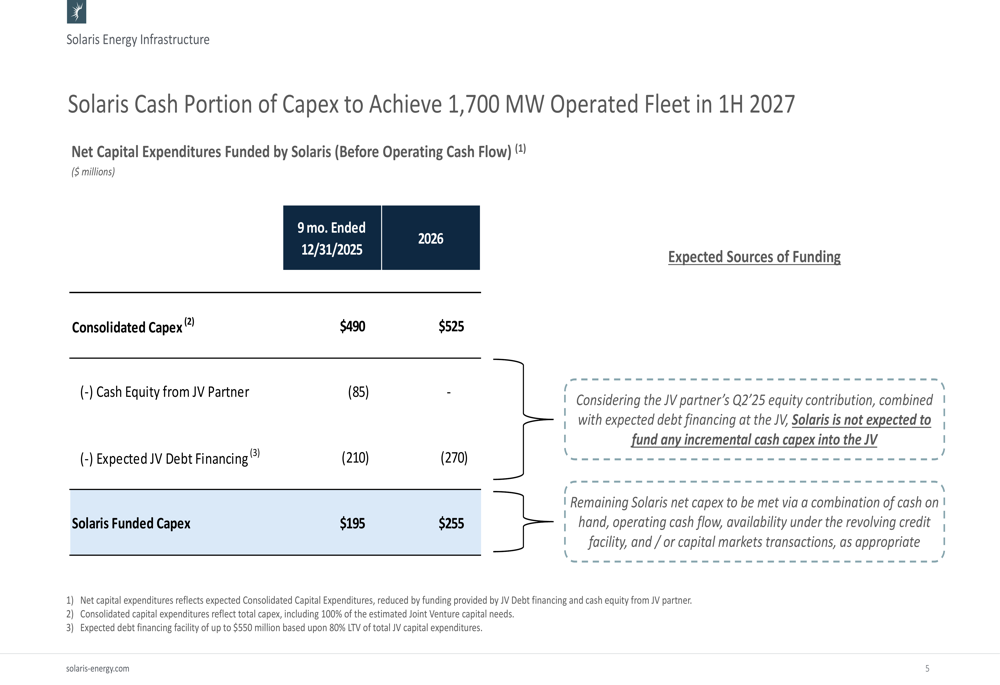

To finance this expansion, Solaris has outlined a detailed capital expenditure plan for the coming periods. The company expects consolidated capex of $490 million for the nine months ending December 31, 2025, and $525 million for 2026, as shown in the following capex breakdown:

The funding strategy leverages joint venture partnerships, with expected cash equity contributions of $85 million from JV partners and anticipated JV debt financing of $210 million in 2025 and $270 million in 2026. This approach reduces Solaris’s direct capital requirements to $195 million for the remainder of 2025 and $255 million for 2026.

Forward-Looking Statements

Looking ahead, Solaris Energy Infrastructure has maintained its Q2 2025 guidance and introduced Q3 2025 projections that indicate continued growth. The company expects its Power Solutions segment to expand from 390 MW in Q1 to 440 MW in Q2 and 520 MW in Q3, driving sequential increases in adjusted EBITDA.

The company’s long-term growth trajectory is illustrated in the following fleet and contract growth chart:

By 2027, Solaris aims to have a fully contracted 1,700 MW consolidated fleet, with 1,250 MW net owned by SEI. The company has identified several potential growth drivers, including increasing power demands from advanced AI models/data centers and energy needs in the Permian Basin.

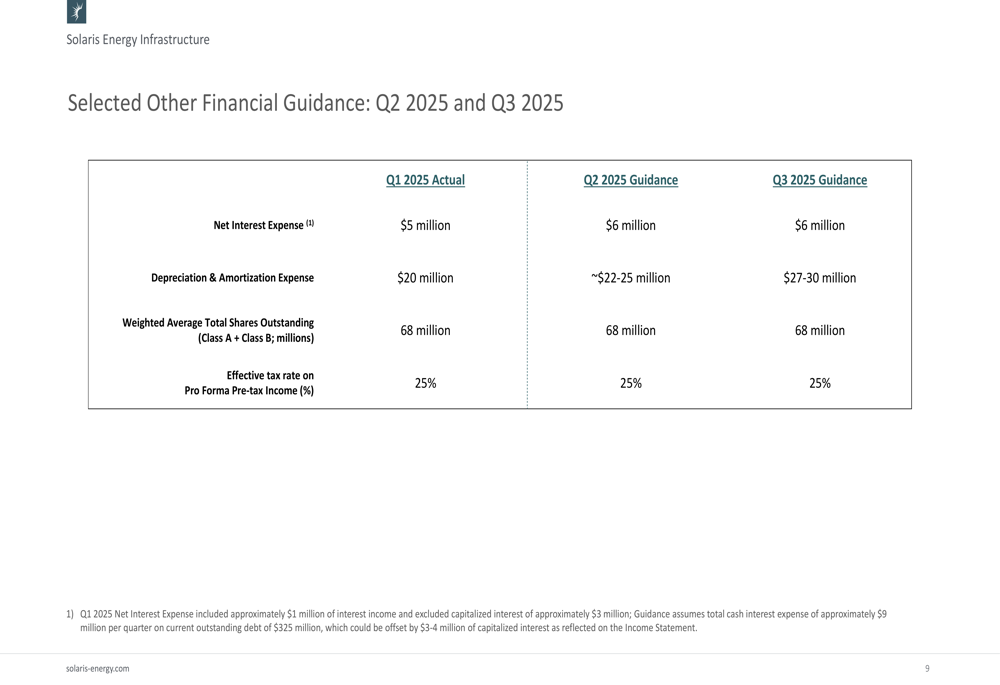

Additional financial guidance provided by the company includes:

With stable interest expenses, increasing depreciation and amortization reflecting fleet growth, and a consistent effective tax rate of 25%, Solaris is positioning itself for sustainable long-term financial performance.

Conclusion

Solaris Energy Infrastructure’s Q1 2025 earnings presentation reveals a company in the midst of a strategic transformation, pivoting from traditional oilfield services to energy infrastructure with a strong focus on data center power solutions. The planned expansion to a 1,700 MW fleet by 2027, backed by $290 million in new investments, positions the company to capitalize on growing demand for reliable power generation, particularly in the rapidly expanding data center market.

With 71% of its projected capacity already under contract, increasing contract tenors, and a clear funding strategy for its capital expenditures, Solaris appears well-positioned to execute its growth plans. Investors will be watching closely to see if the company can maintain its momentum and deliver on its ambitious adjusted EBITDA targets as it completes its strategic transformation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.