Robinhood shares gain on Q2 beat, as user and crypto growth accelerate

Introduction & Market Context

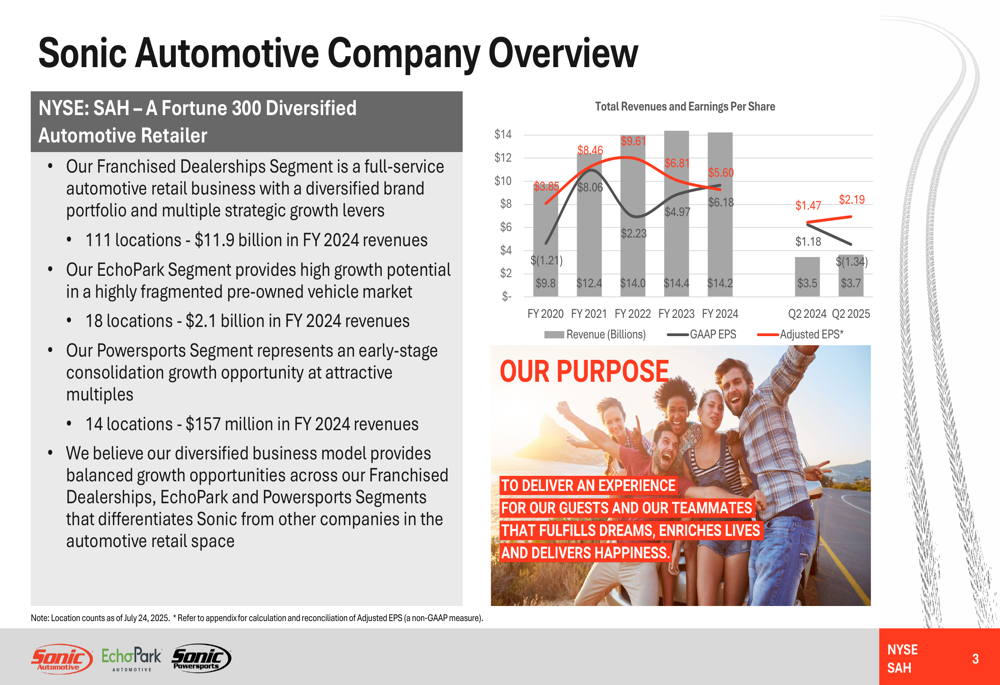

Sonic Automotive Inc . (NYSE:SAH) released its second quarter 2025 investor presentation on July 24, showing strong performance with GAAP earnings per share of $2.19, a 49% increase from $1.47 in Q2 2024. The Fortune 300 diversified automotive retailer’s shares jumped 5.07% in premarket trading to $84, building on momentum from its Q1 results when the company reported record consolidated revenue of $3.7 billion.

The presentation highlighted Sonic’s three-segment business model spanning franchised dealerships, pre-owned vehicle retail through EchoPark, and an emerging powersports division. The company’s strategic positioning in the hybrid vehicle market appears to be paying dividends as consumer preference continues to shift toward hybrid electric vehicles (HEVs) over battery electric vehicles (BEVs).

Quarterly Performance Highlights

Sonic Automotive’s Q2 2025 results demonstrate significant growth across key metrics. The company’s GAAP EPS of $2.19 represents a substantial improvement over the $1.47 reported in Q2 2024. This performance continues the positive trajectory seen in Q1 2025, when the company reported adjusted EPS of $1.48.

As shown in the following comprehensive business overview, Sonic has maintained steady revenue growth from $9.8 billion in FY 2020 to $14.2 billion in FY 2024, while dramatically improving profitability:

The company’s diversified business model provides balanced growth across segments, with the franchised dealerships generating $11.9 billion in FY 2024 revenues, EchoPark contributing $2.1 billion, and the newer powersports segment adding $157 million.

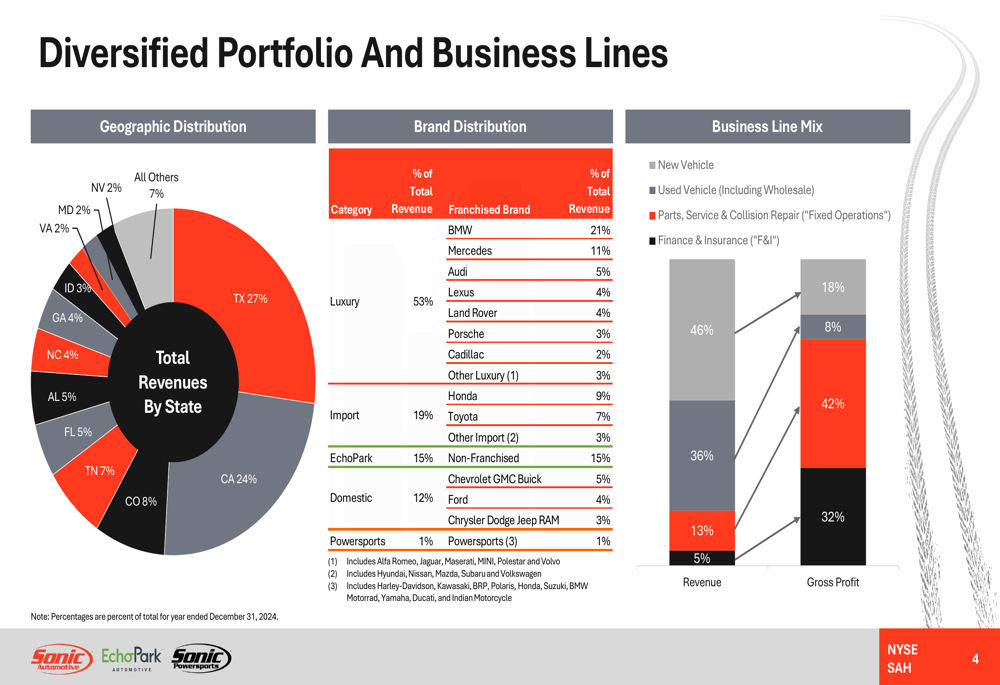

Sonic’s geographic and brand distribution reveals a strategic focus on high-margin luxury vehicles and key markets, as illustrated in this breakdown:

Texas (27%) and California (24%) represent the company’s largest markets, while luxury brands account for 53% of revenue, followed by import brands (19%), domestic brands (12%), EchoPark (15%), and powersports (1%). This diversification helps insulate the company from regional economic fluctuations and brand-specific challenges.

Strategic Initiatives

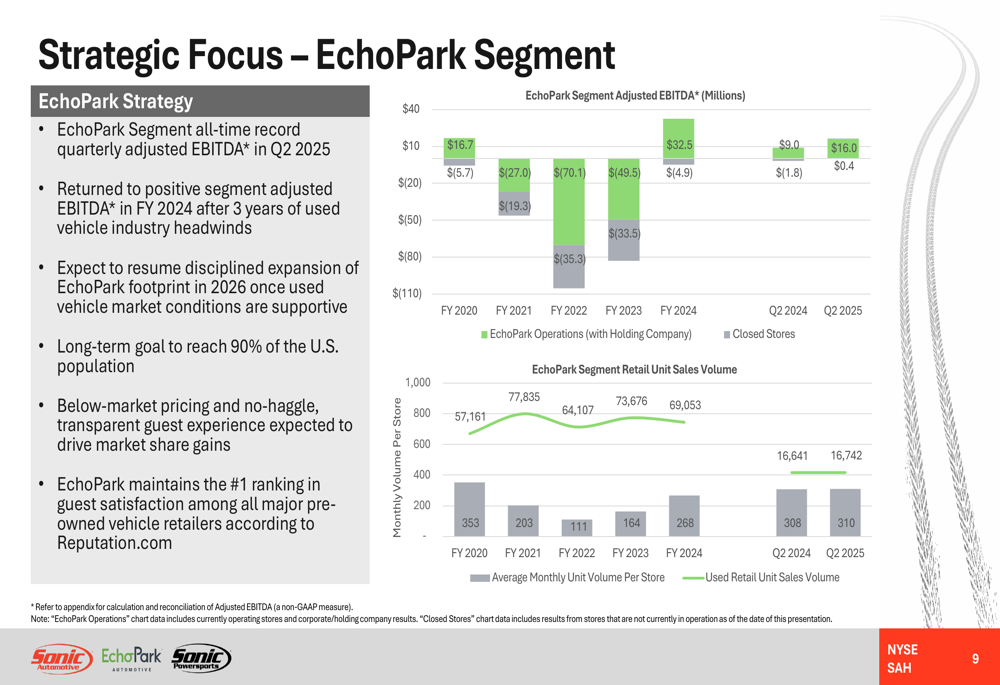

The EchoPark segment achieved an all-time record quarterly adjusted EBITDA of $16.0 million in Q2 2025, marking a significant turnaround from a negative $1.8 million in Q2 2024. This improvement validates management’s strategic focus on optimizing this pre-owned vehicle retail segment.

As shown in the following chart, EchoPark has successfully transitioned from consistent losses to profitability:

Management indicated plans to resume expansion of EchoPark in 2026, with a long-term goal of reaching 90% of the U.S. population. The segment maintains the #1 ranking in guest satisfaction among pre-owned vehicle retailers, providing a solid foundation for future growth.

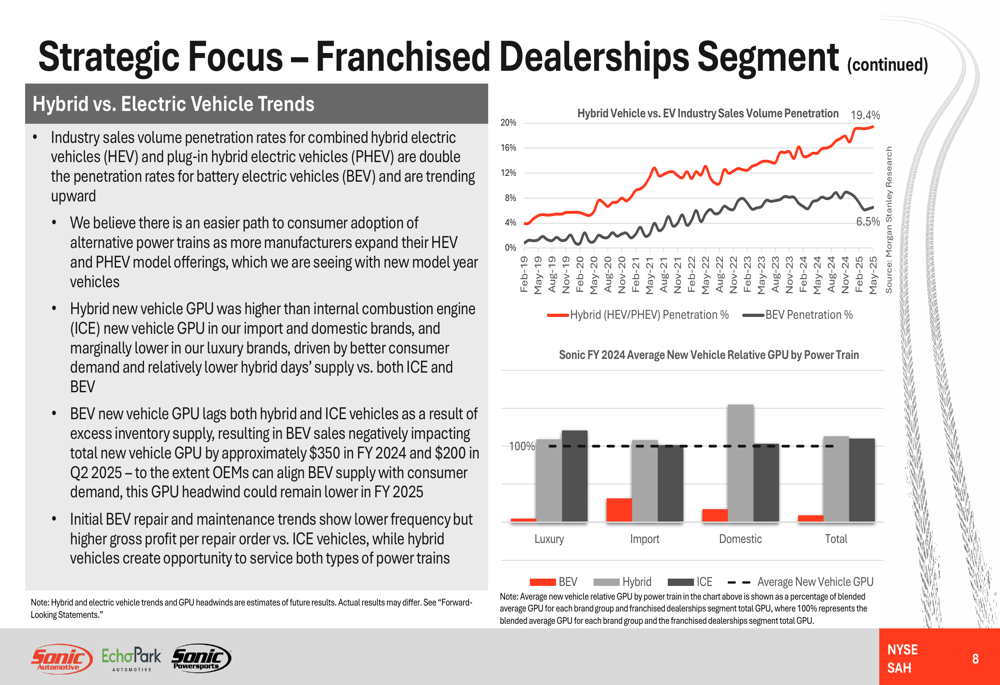

Another key strategic initiative is Sonic’s positioning in the hybrid vehicle market. Industry sales volume penetration rates for hybrid electric vehicles (HEV) and plug-in hybrid electric vehicles (PHEV) are now double those of battery electric vehicles (BEV), at 19.4% versus 6.5% as of May 2025. The company’s data shows that hybrid vehicles generally deliver better gross profit per unit than BEVs across all brand categories:

This strategic focus on hybrids appears well-timed as consumers show preference for this transitional technology over full electric vehicles, particularly in the luxury and import segments where Sonic has strong representation.

Detailed Financial Analysis

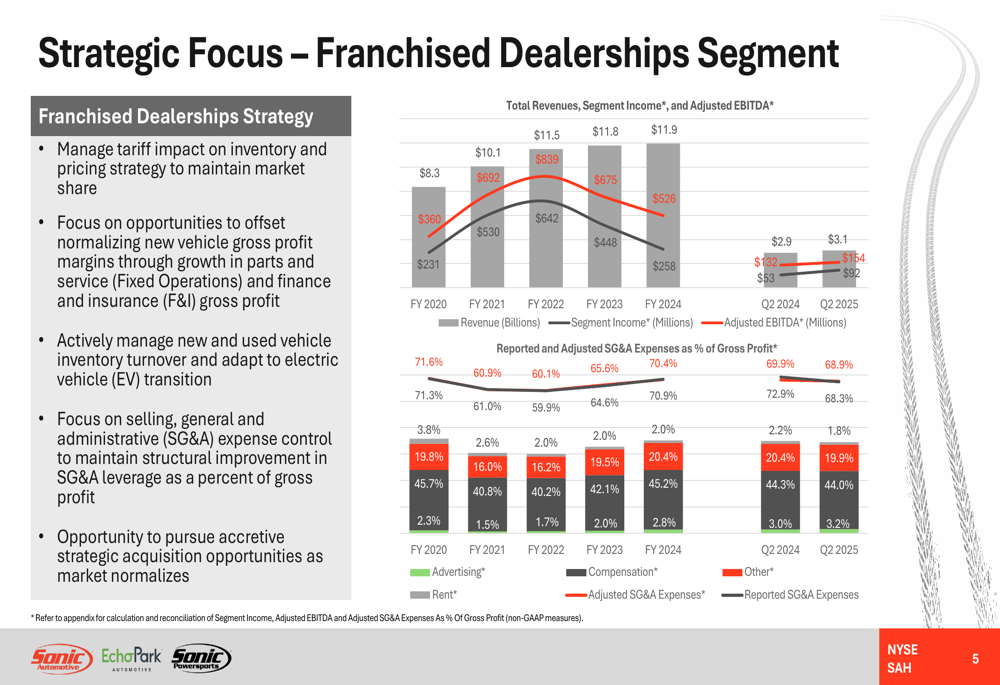

The franchised dealerships segment, which represents the core of Sonic’s business, showed mixed results in Q2 2025. Segment income was $29 million, down significantly from $258 million in Q2 2024, while adjusted EBITDA was $53 million compared to $132 million in the prior year period.

The following chart illustrates the segment’s performance trends and strategic focus areas:

Despite the year-over-year decline, the segment’s SG&A expenses as a percentage of gross profit improved to 65.6% (reported) and 68.3% (adjusted) in Q2 2025, compared to 68.9% (reported) and 72.9% (adjusted) in Q2 2024, indicating improved operational efficiency.

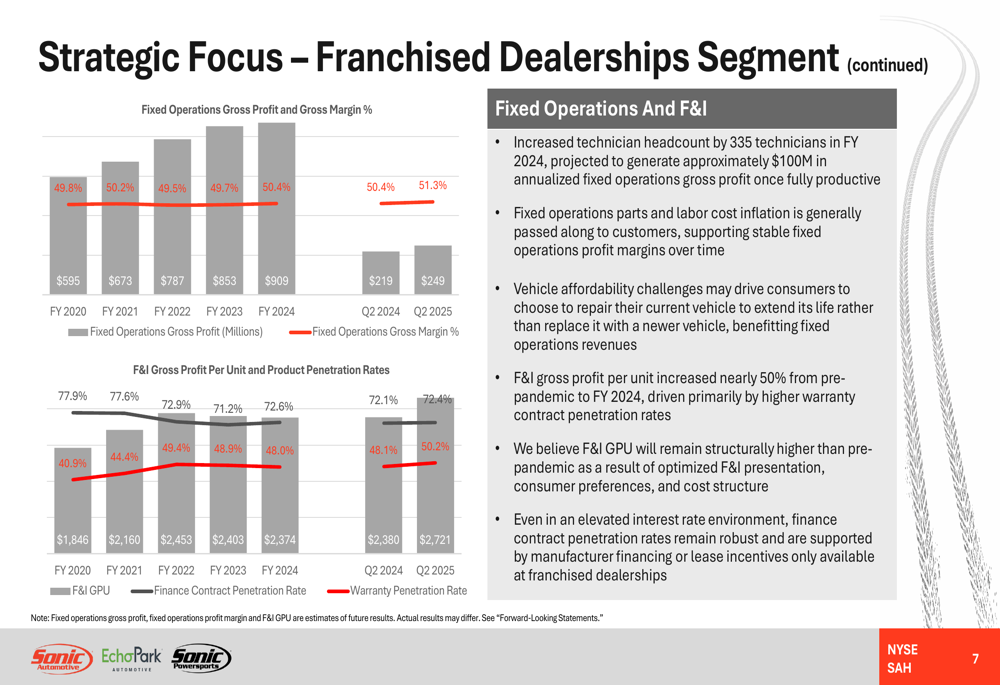

Fixed operations continue to be a bright spot, with gross profit reaching $249 million in Q2 2025, up from $219 million in Q2 2024, and gross margin improving to 51.3% from 50.4%:

F&I gross profit per unit also showed strong performance, increasing to $2,721 in Q2 2025 from $2,380 in Q2 2024, with finance contract penetration rates remaining robust at 48.1% despite elevated interest rates.

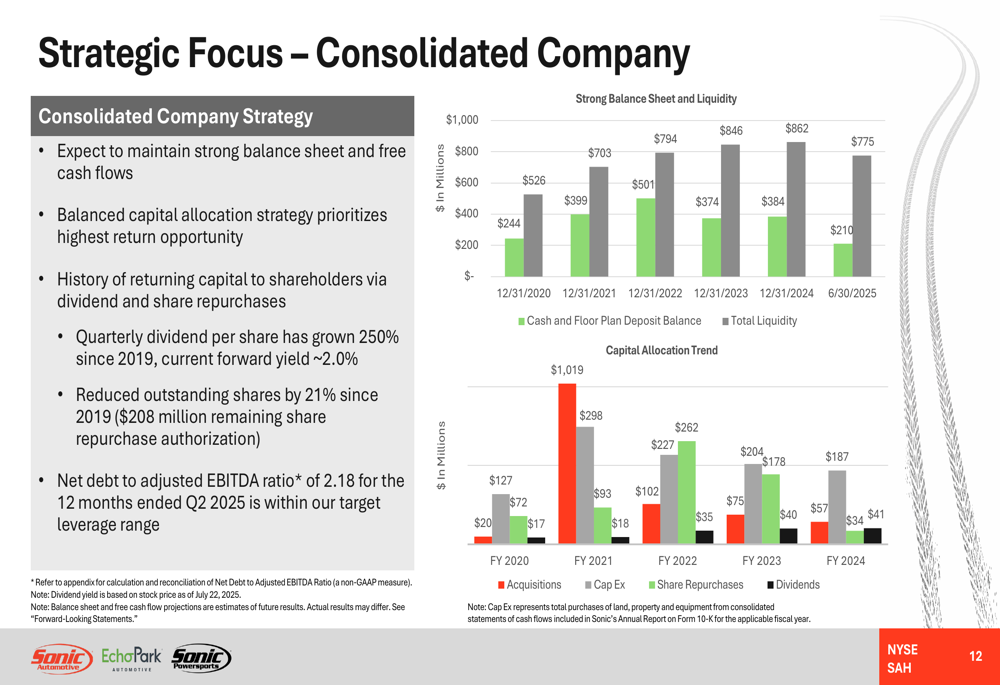

The company maintains a strong balance sheet and liquidity position, with a balanced capital allocation strategy:

Sonic’s quarterly dividend per share has grown 250% since 2019, with a current forward yield of approximately 2.0%. The company has reduced outstanding shares by 21% since 2019 and maintains a net debt to adjusted EBITDA ratio of 2.18 for the 12 months ended Q2 2025, within its target leverage range.

Forward-Looking Statements

Looking ahead, Sonic Automotive provided a detailed outlook for FY 2025 across all segments. For the franchised dealerships segment, the company anticipates new vehicle gross profit per unit in the $2,800 to $3,200 range and used vehicle GPU in the $1,300 to $1,500 range, with potential volatility due to tariff impacts.

The EchoPark segment is expected to deliver adjusted EBITDA between $50-$55 million in FY 2025, driven by operational improvements at seven stores and mid-single-digit percentage growth in used retail unit sales volume. The powersports segment is projected to contribute adjusted EBITDA between $6-$8 million.

Management noted that tariffs may create volatility in new and used vehicle pricing, volume, and gross profit per unit in the second half of 2025. Additionally, used vehicle supply is projected to reach its lowest point in late 2025, potentially impacting inventory availability and pricing.

Despite these challenges, Sonic’s diversified business model, strategic focus on hybrid vehicles, and successful turnaround of the EchoPark segment position the company well for continued growth in the evolving automotive retail landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.