TSX gains after CPI shows US inflation rose 3%

Introduction & Market Context

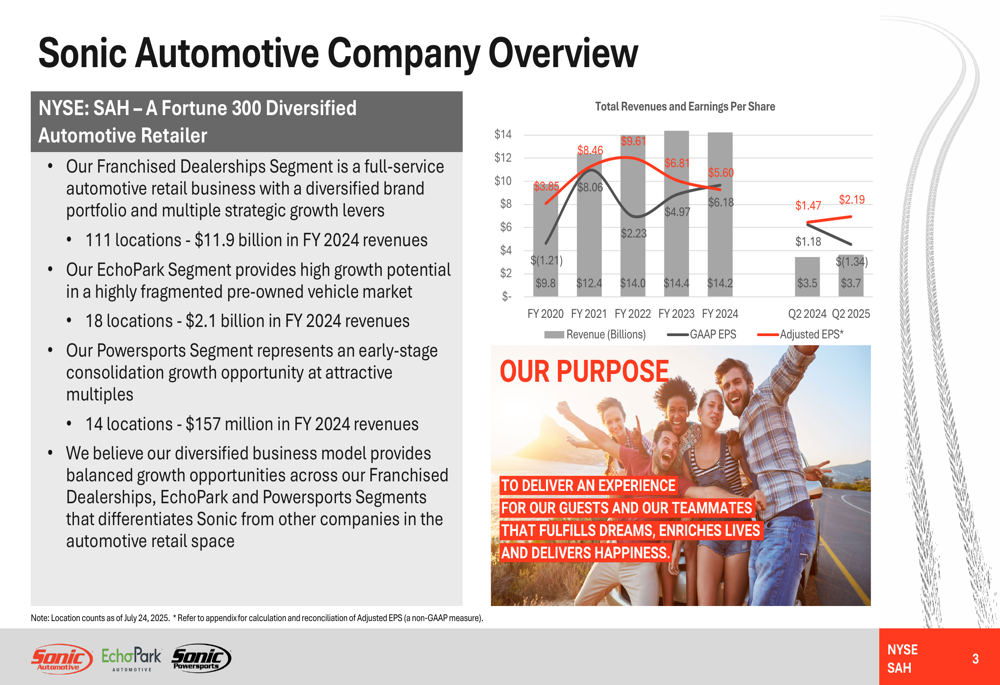

Sonic Automotive (NYSE:SAH) presented its Q2 2025 investor presentation on July 24, 2025, showcasing strong financial performance across its diversified business segments. The Fortune 300 automotive retailer reported a significant 49% year-over-year increase in adjusted earnings per share to $2.19, driving its stock price up 6.16% to $71.86. The company’s consolidated revenues reached a quarterly record of $14.7 billion, reflecting a 6% increase from the previous year.

Sonic operates through three business segments: Franchised Dealerships (111 locations, $11.9 billion in FY 2024 revenues), EchoPark used vehicle centers (18 locations, $2.1 billion), and Powersports (14 locations, $157 million). This diversified approach has helped the company navigate changing market dynamics, including tariff impacts and the ongoing transition toward hybrid and electric vehicles.

As shown in the following company overview chart, Sonic has demonstrated consistent revenue growth while managing earnings volatility in recent years:

Quarterly Performance Highlights

Sonic’s Q2 2025 performance was highlighted by significant improvements across all segments, with particular strength in the EchoPark division, which achieved an all-time record quarterly adjusted EBITDA of $16 million. The Franchised Dealerships segment saw a 6% revenue increase to $3.1 billion, while the Powersports segment showed seasonal strength with adjusted EBITDA of $2.3 million, up from a $0.7 million loss in Q2 2024.

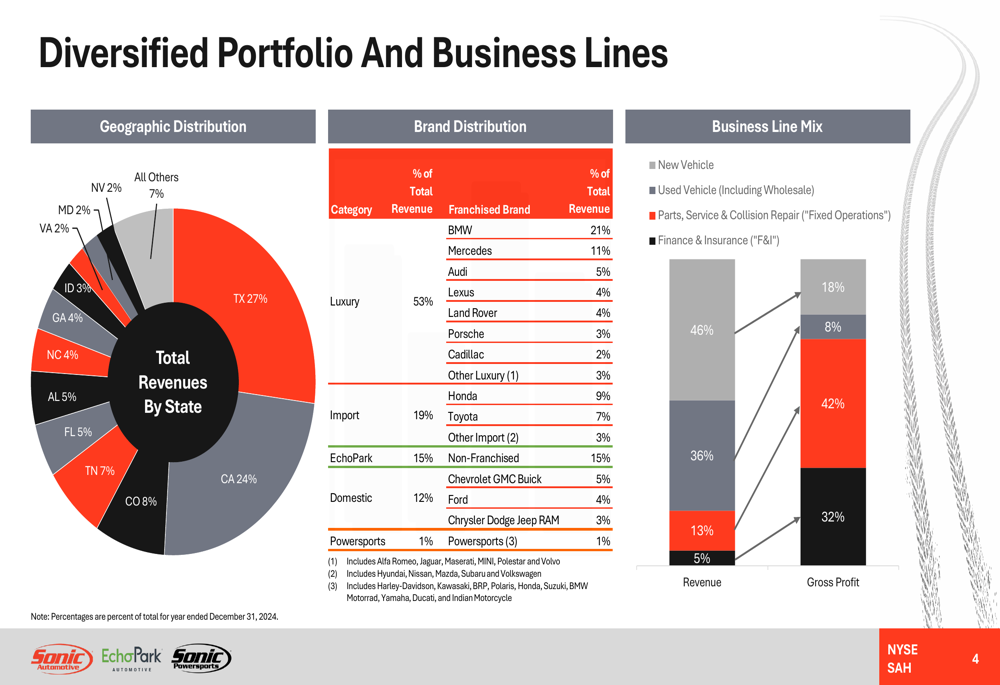

The company’s geographic and brand diversification has been a key strength, with operations spread across 13 states and a strong focus on luxury brands, which comprise 53% of the business. Texas (27%) and California (24%) represent the largest markets by revenue.

The following chart illustrates Sonic’s diversified portfolio across geographic regions, brand categories, and business lines:

Segment Analysis: Franchised Dealerships

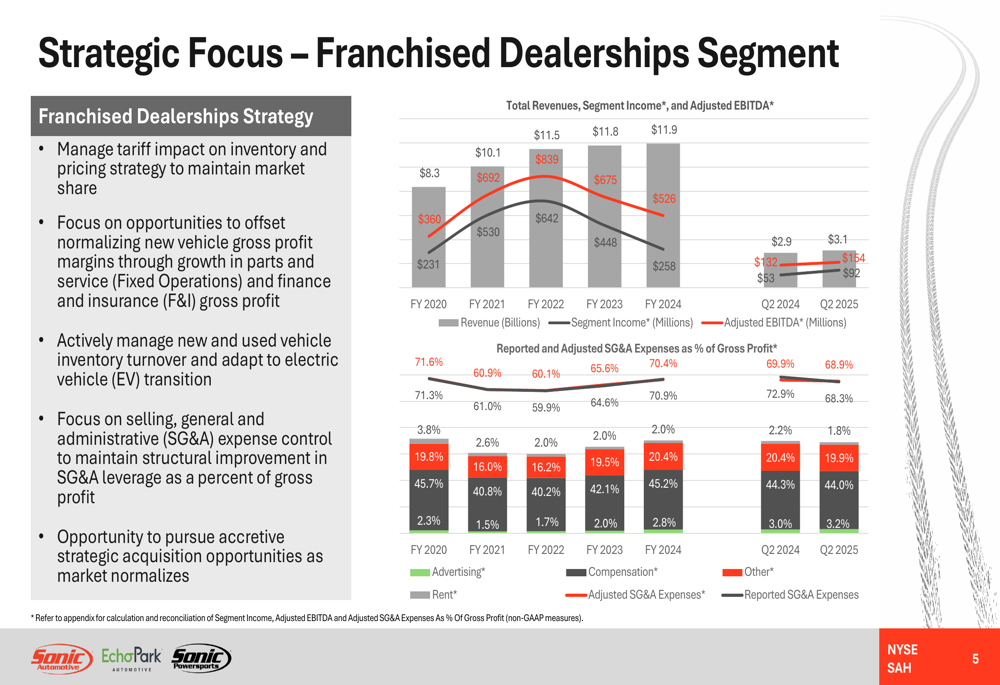

The Franchised Dealerships segment continues to be Sonic’s largest revenue driver, with strategic focus on managing tariff impacts and offsetting normalizing new vehicle margins through growth in fixed operations and F&I. The company has made significant improvements in SG&A expense control, with reported SG&A as a percentage of gross profit improving from 72.9% in Q2 2024 to 68.3% in Q2 2025.

As illustrated in the following chart, the Franchised Dealerships segment has maintained strong financial performance despite market normalization from pandemic-era peaks:

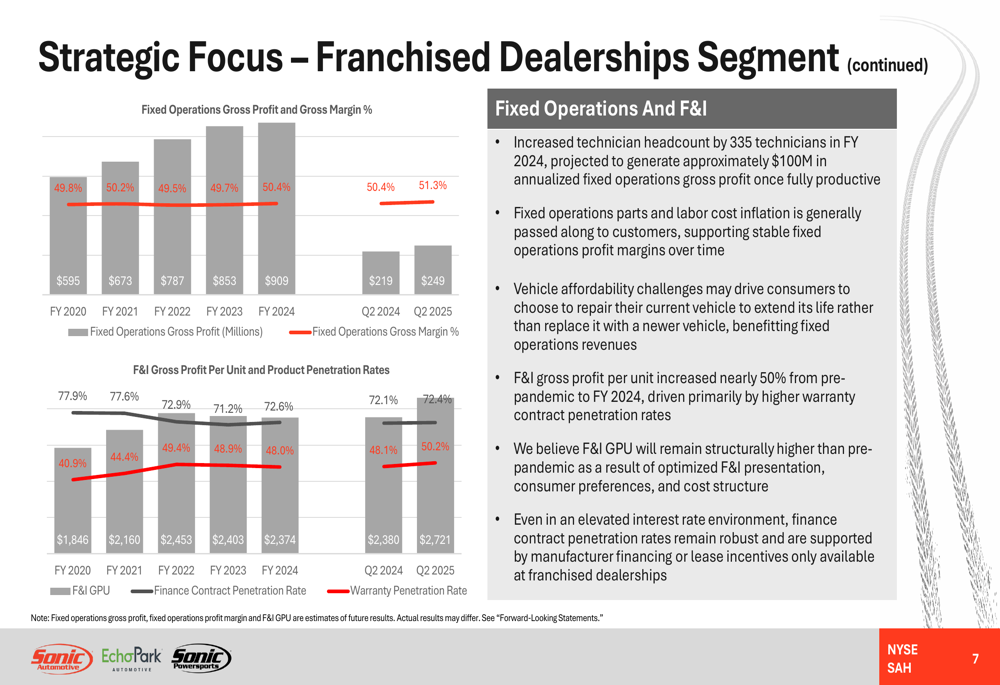

A key strength in the Franchised Dealerships segment has been the growth in fixed operations (parts, service, and collision repair) and finance & insurance (F&I). The company increased its technician headcount by 335 in FY 2024, projected to generate approximately $100 million in annualized fixed operations gross profit once fully productive. Fixed operations gross margin reached 51.3% in Q2 2025, up from 50.4% in Q2 2024.

F&I gross profit per unit has shown remarkable growth, increasing nearly 50% from pre-pandemic levels to reach $2,721 in Q2 2025, driven primarily by higher warranty contract penetration rates. Finance contract penetration rates have also improved to 50.2% in Q2 2025, up from 49.4% in the same period last year.

The following chart shows the consistent growth in F&I performance:

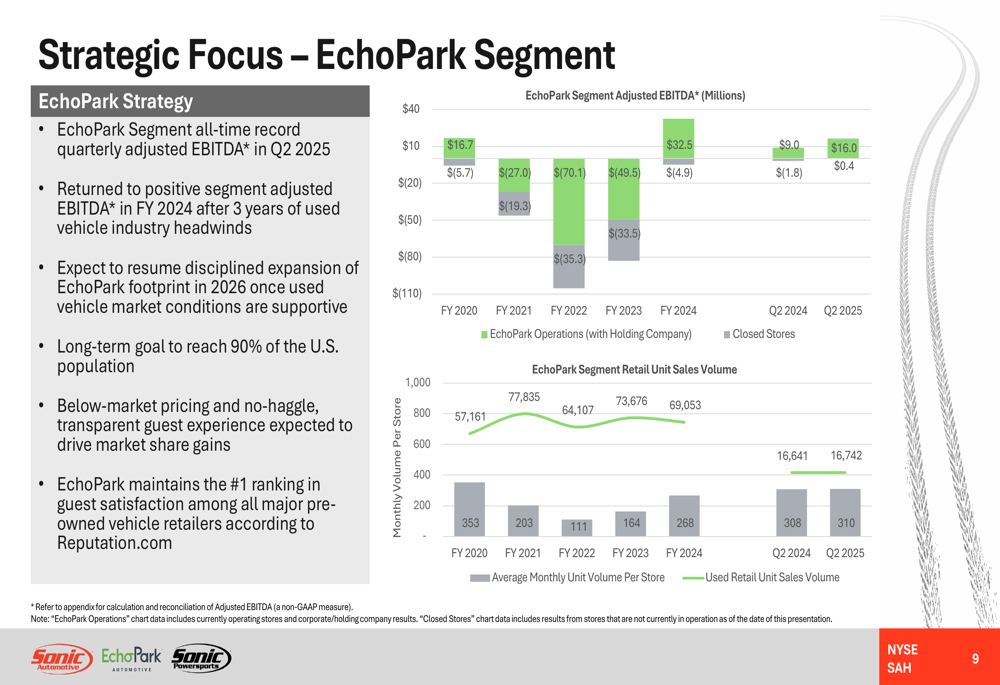

Segment Analysis: EchoPark

The EchoPark segment has been a significant success story, achieving all-time record quarterly adjusted EBITDA of $16 million in Q2 2025, a dramatic improvement from a $4.9 million loss in Q2 2024. The segment has returned to profitability after three years of used vehicle industry headwinds, with FY 2024 adjusted EBITDA of $32.5 million compared to a $49.5 million loss in FY 2023.

The following chart illustrates EchoPark’s impressive turnaround and growth trajectory:

EchoPark’s success has been driven by strategic inventory management, optimized F&I product offerings, and a focus on maintaining positive retail used vehicle gross profit per unit. The company expects total GPU in the $3,400 to $3,800 range throughout FY 2025. Sonic has raised its EchoPark EBITDA guidance to $50-$55 million for the full year, reflecting confidence in continued growth.

The company plans to resume disciplined expansion of the EchoPark footprint in 2026 once used vehicle market conditions are more supportive, with a long-term goal to reach 90% of the U.S. population. EchoPark maintains the #1 ranking in guest satisfaction among all major pre-owned vehicle retailers according to Reputation.com.

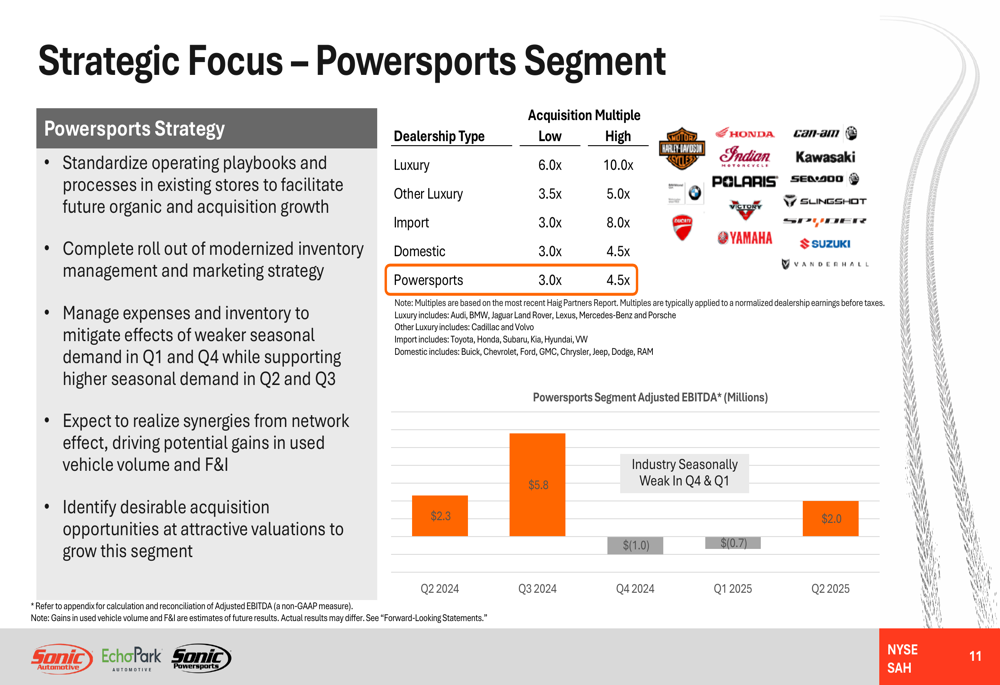

Segment Analysis: Powersports

The Powersports segment, Sonic’s newest business line, has shown significant improvement in Q2 2025, with adjusted EBITDA of $2.3 million compared to a $0.7 million loss in Q2 2024. This segment demonstrates strong seasonality, with better performance in Q2 and Q3 compared to Q1 and Q4.

The company’s strategy for Powersports includes standardizing operating playbooks and processes in existing stores, completing the rollout of modernized inventory management and marketing strategies, and identifying attractive acquisition opportunities. Sonic notes that acquisition multiples for Powersports dealerships (3.0x-4.5x) are generally lower than those for luxury automotive dealerships (6.0x-10.0x), presenting potential value opportunities.

The following chart shows the Powersports segment’s quarterly performance and seasonality:

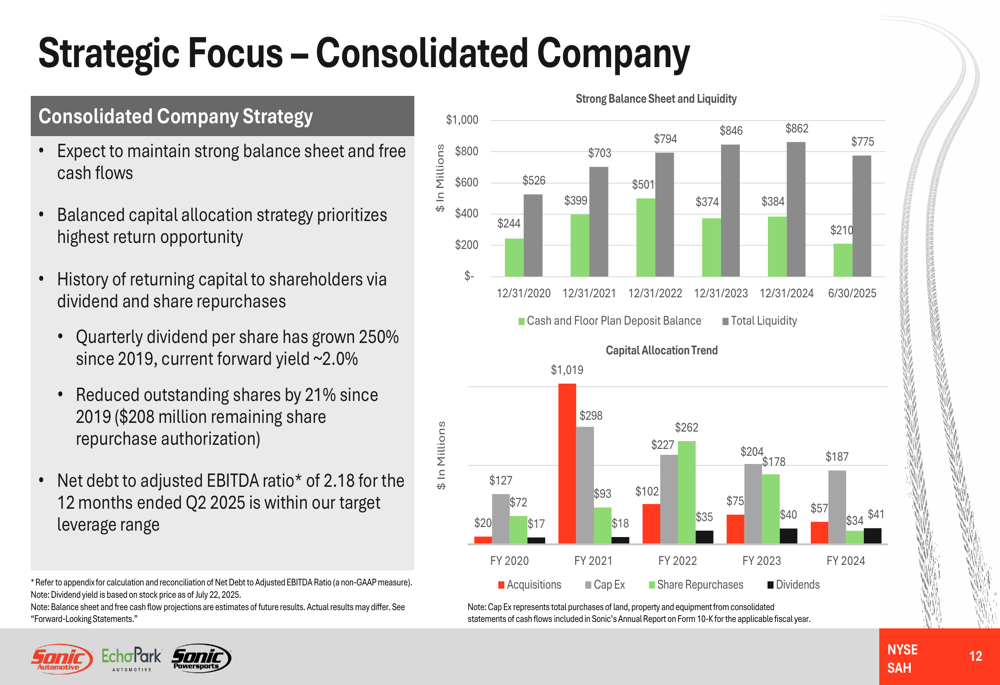

Strategic Initiatives

Sonic is strategically positioning itself to navigate the transition toward hybrid and electric vehicles. The company notes that industry sales volume penetration rates for hybrid electric vehicles (HEV) and plug-in hybrid electric vehicles (PHEV) are double the penetration rates for battery electric vehicles (BEV) and trending upward. Hybrid new vehicle gross profit per unit was higher than internal combustion engine (ICE) new vehicle GPU in import and domestic brands, while BEV new vehicle GPU lags both hybrid and ICE vehicles.

The company maintains a strong balance sheet with a net debt to adjusted EBITDA ratio of 2.18 for the 12 months ended Q2 2025, within its target leverage range. Sonic has a balanced capital allocation strategy, with a quarterly dividend that has grown 250% since 2019 (current forward yield ~2.0%) and share repurchases that have reduced outstanding shares by 21% since 2019.

As shown in the following capital allocation chart, Sonic has maintained strong liquidity while returning value to shareholders:

Forward-Looking Statements

Looking ahead, Sonic anticipates potential volatility in new and used vehicle pricing and volume due to tariff impacts in the second half of 2025. However, the company believes new vehicle gross profit per unit will stabilize in the $2,500-$3,000 range, remaining higher than pre-pandemic levels. Used vehicle supply is projected to reach its lowest point in late 2025, with gradual expansion and further normalization expected beyond 2025.

For the EchoPark segment, Sonic has raised its full-year EBITDA guidance to $50-$55 million and plans to resume expansion in 2026. The company also increased its quarterly cash dividend by 9% to $0.38 per share, demonstrating confidence in its financial position and commitment to shareholder returns.

CEO David Smith emphasized the importance of strong relationships with teammates, guests, and partners as a foundation for future success, while President Jeff Dyke highlighted the exceptional performance of EchoPark, noting its ability to manage volume and profit effectively.

With its diversified business model, strategic focus on high-margin segments, and disciplined capital allocation, Sonic Automotive appears well-positioned to navigate market challenges while delivering continued growth across its automotive retail portfolio.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.