What happens to stocks if AI loses momentum?

Introduction & Market Context

Sonida Senior Living Inc (NYSE:SNDA) released its second quarter 2025 investor presentation on August 11, 2025, highlighting continued revenue growth, strategic acquisitions, and progress toward its long-term NOI targets. The company, which owns and operates senior living communities across the United States, is capitalizing on favorable demographic trends while expanding its footprint in high-growth Southeastern markets.

The presentation comes after Sonida reported better-than-expected Q1 2025 results, with an actual EPS of -$0.77 versus a forecast of -$0.83. The company’s stock has been trading near $24.38, up from its 52-week low of $19.34 but below its 52-week high of $32.90.

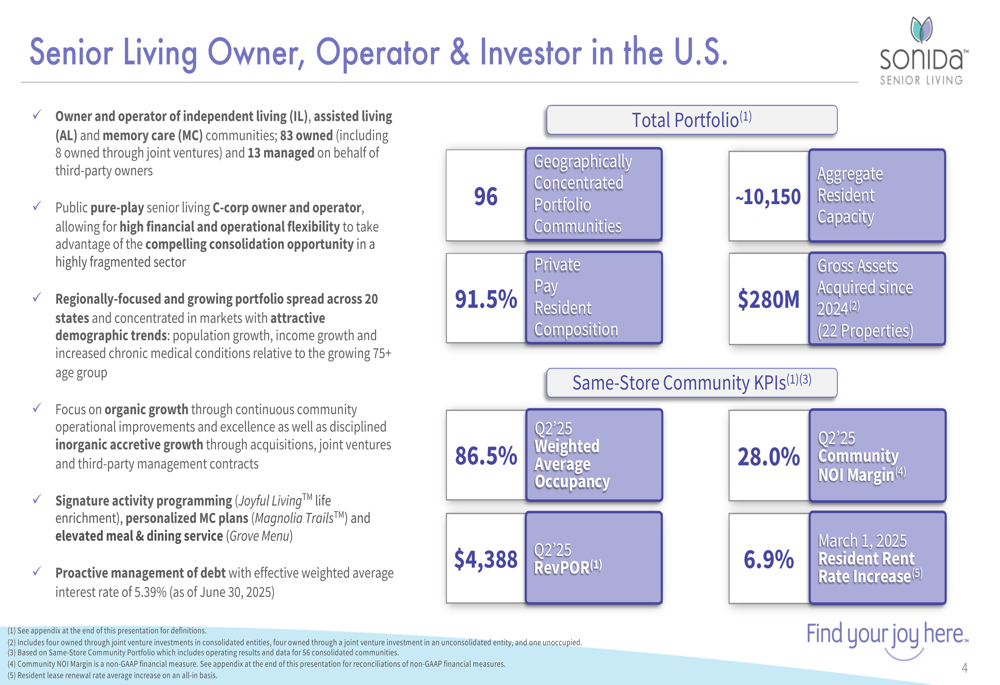

As shown in the following overview of Sonida’s business model and portfolio:

Quarterly Performance Highlights

Sonida reported strong financial performance in Q2 2025, with notable growth in revenue per occupied room (RevPOR) and net operating income (NOI). The company’s same-store portfolio, consisting of 56 communities with 5,349 owned units, maintained a weighted average occupancy of 86.5% in Q2 2025, slightly higher than the 86.1% reported in Q2 2024.

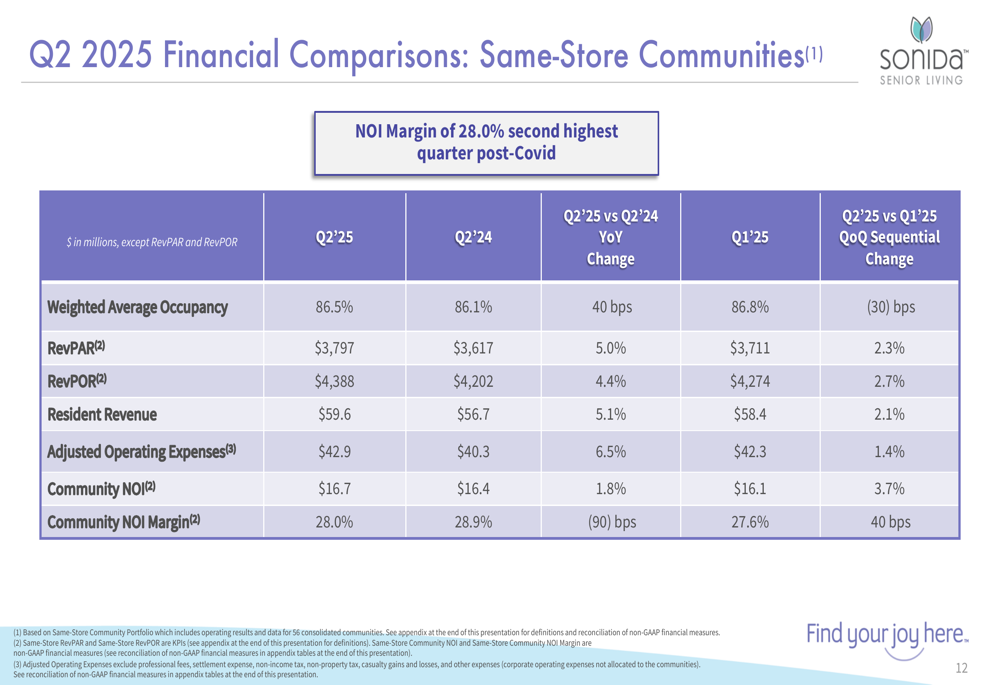

The following chart details Sonida’s same-store financial performance, showing improvements in key metrics:

RevPOR for same-store communities increased by 4.4% year-over-year to $4,388 in Q2 2025, while community NOI reached $16.7 million with a margin of 28.0%. This represents the second-highest NOI margin post-Covid, though slightly below the 28.9% reported in Q2 2024.

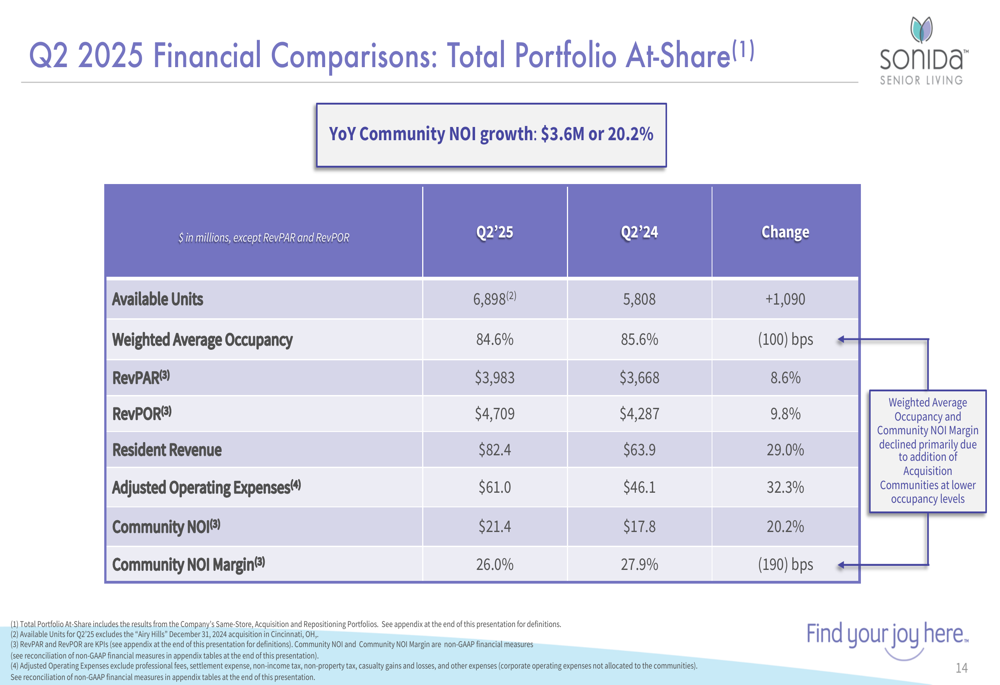

For the total portfolio, which includes both same-store and acquisition communities, Sonida reported even stronger growth metrics:

Total (EPA:TTEF) portfolio NOI increased by 20.2% year-over-year to $21.4 million, driven by recent acquisitions. However, the weighted average occupancy for the total portfolio declined to 84.6% from 85.6% in Q2 2024, primarily due to the addition of acquisition communities with lower initial occupancy levels.

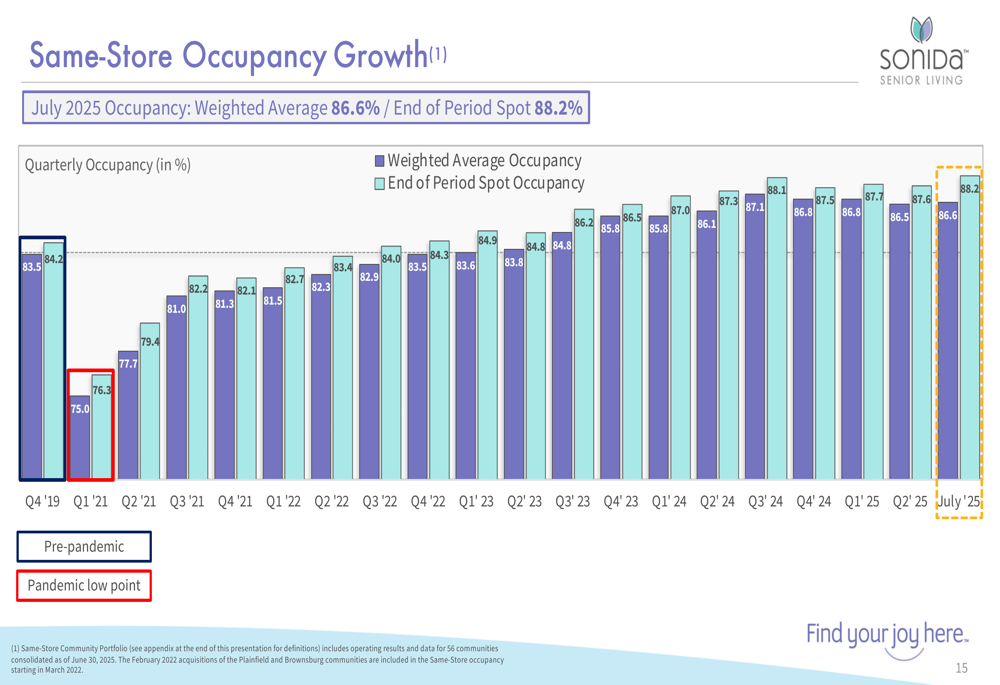

Occupancy trends continue to show improvement, with July 2025 spot occupancy reaching 88.2%, as illustrated in the following chart:

Strategic Initiatives

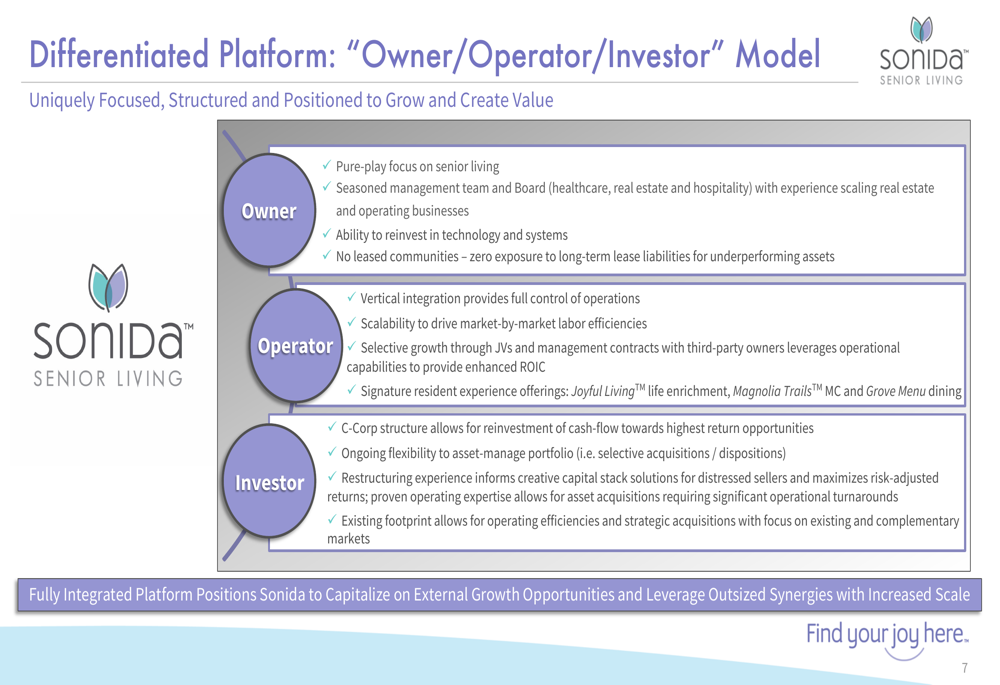

Sonida’s presentation highlighted its differentiated "Owner/Operator/Investor" model, which the company believes provides competitive advantages in the senior living market:

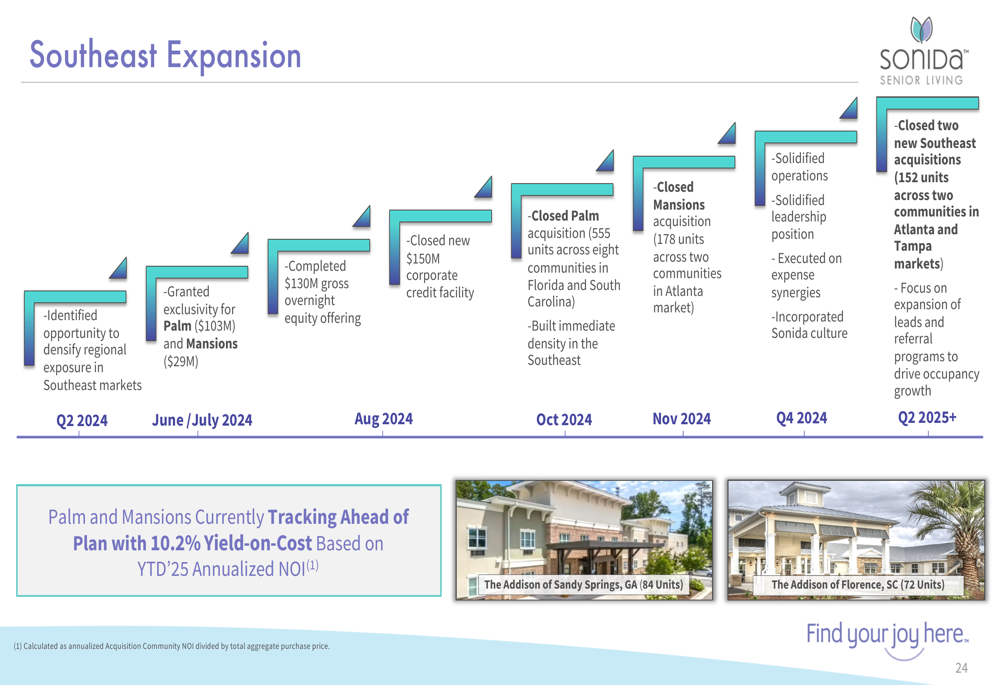

A key strategic focus for Sonida is its expansion in the Southeast region. The company has acquired multiple communities in Florida and Georgia since 2024, with recent additions including "East Lake" in Tampa (64 units, $11M purchase price) and "Alpharetta" in Atlanta (88 units, $11M purchase price).

The following timeline illustrates Sonida’s Southeast expansion strategy:

These acquisitions are part of Sonida’s broader inorganic growth strategy, which aims to capitalize on market dislocations and distressed capital structures in the senior housing sector. The company reported that its Palm and Mansions acquisitions from 2024 are currently tracking ahead of plan with a 10.2% yield-on-cost based on YTD 2025 annualized NOI.

Another strategic initiative involves repositioning certain communities to reduce Medicaid dependence and increase private-pay revenue. The company has identified opportunities in four of its five Indiana communities to generate significant ROI through conversions of care levels and physical plant upgrades.

Forward-Looking Statements

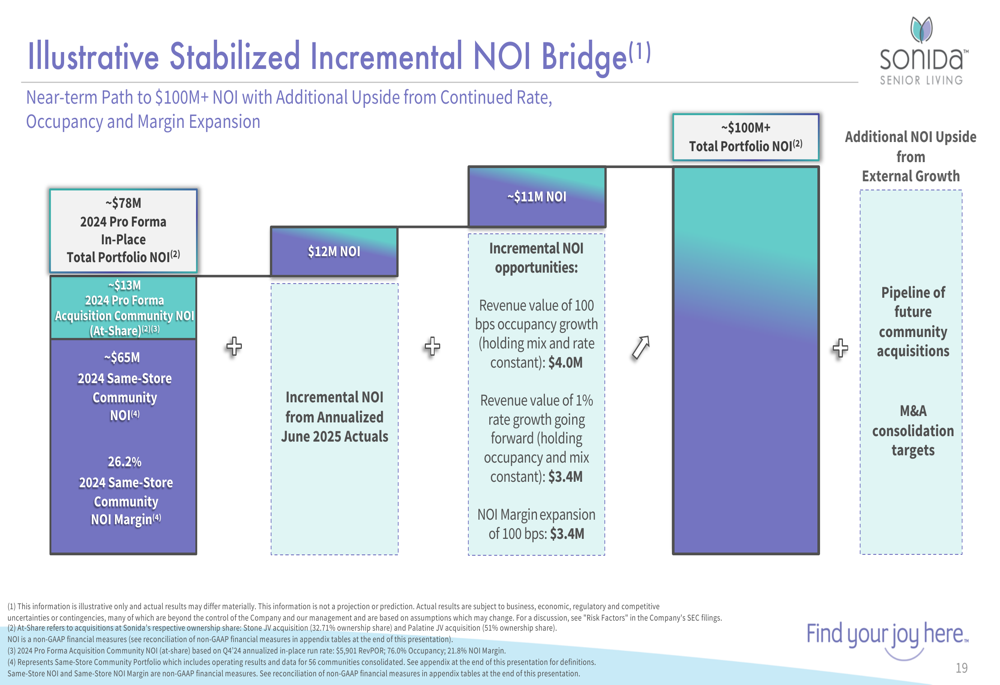

Sonida presented an illustrative path toward achieving $100M+ in NOI, building from its 2024 same-store NOI of $65M and acquisition community NOI of $13M:

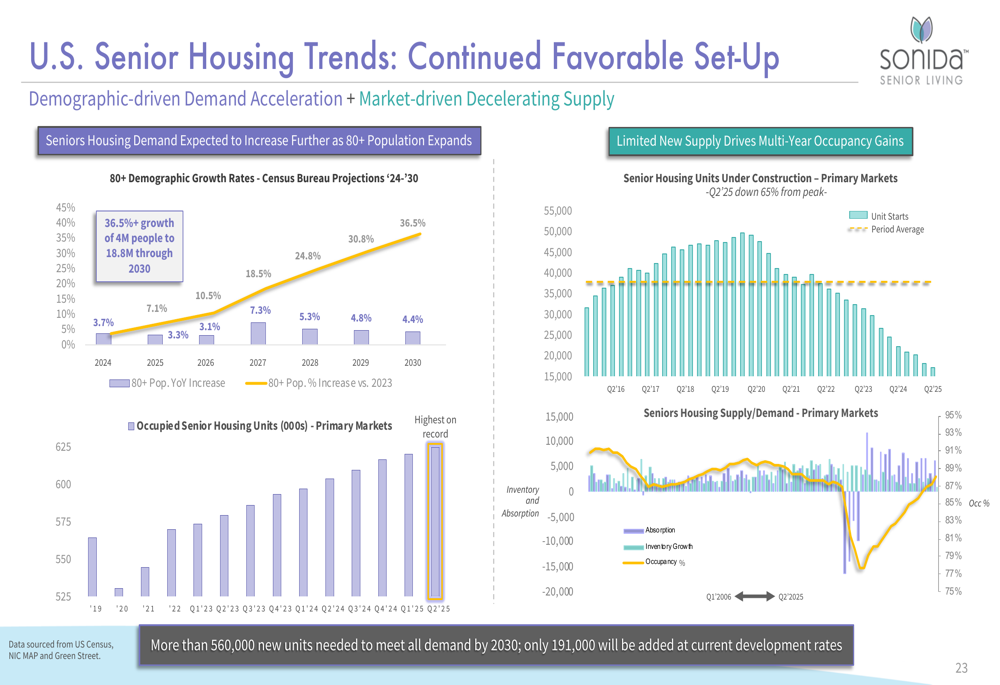

The company’s growth strategy is supported by favorable demographic trends in the U.S. senior housing market:

With the 80+ population expected to grow significantly through 2030 and limited new supply in the market (construction down 65% from peak), Sonida anticipates continued improvements in occupancy and pricing power. The company estimates that more than 560,000 new units will be needed to meet all demand by 2030.

Financial Position

In August 2025, Sonida completed a refinancing with Ally Bank, securing $122 million in initial funding with $15 million in future available draws. The debt carries an interest rate of SOFR + 2.65%, with a performance-based step down to SOFR + 2.45%, and matures in August 2030.

As of June 30, 2025, Sonida’s total debt outstanding was $680.9 million with a weighted average interest rate of 5.39%. The company’s enterprise value stood at approximately $1.2 billion, with a market capitalization of $470.6 million based on a closing stock price of $24.95.

The company also reported receiving $8.8 million in Employee Retention Credits (ERC) year-to-date, with an additional $0.2 million received in July 2025.

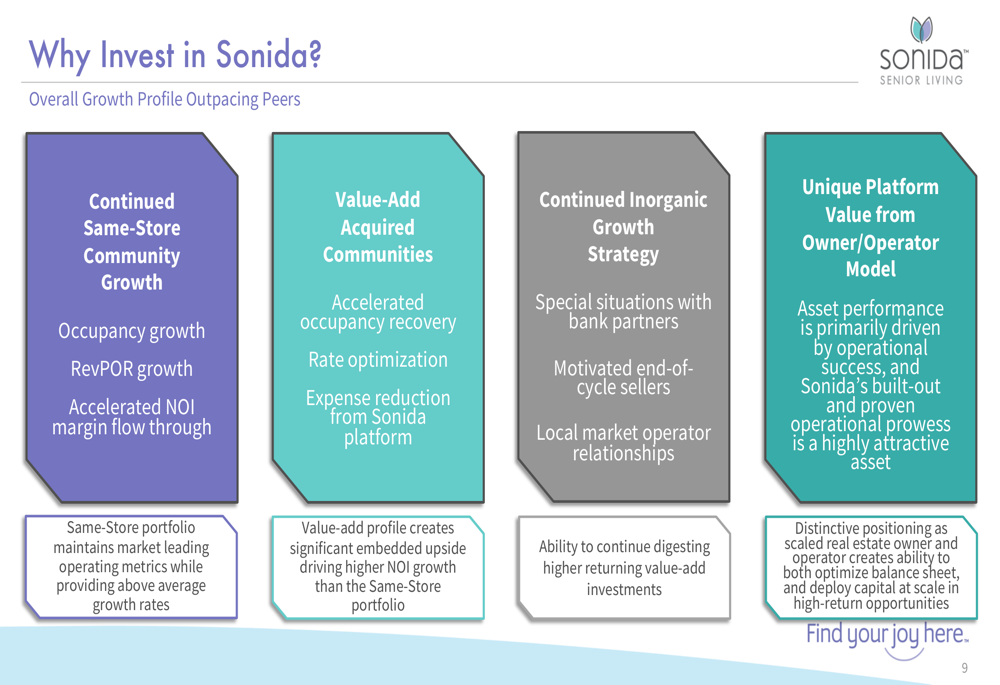

Investment Thesis

Sonida presented several compelling reasons for investors to consider the company, highlighting both organic and inorganic growth opportunities:

The company’s investment thesis centers on continued same-store community growth, value-add opportunities in acquired communities, an ongoing inorganic growth strategy, and the unique platform value derived from its owner/operator model.

With its strategic focus on high-growth markets, portfolio optimization, and favorable demographic tailwinds, Sonida aims to deliver continued revenue and NOI growth while expanding its footprint in the senior living sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.