Street Calls of the Week

Introduction & Market Context

Sonoco Products Company (NYSE:SON) presented its second quarter 2025 financial results on July 24, 2025, revealing substantial revenue growth and continued progress on its strategic transformation. The packaging company reported significant gains driven by its recent acquisition of Sonoco Metal Packaging (NYSE:PKG) EMEA and strong performance across its core business segments.

The presentation comes after Sonoco’s stock has shown positive momentum, with shares up 2.16% in the previous trading session to close at $47.65, and gaining an additional 1.36% in after-hours trading to reach $48.30. This represents a recovery from earlier in the year when the company missed Q1 2025 earnings expectations.

Quarterly Performance Highlights

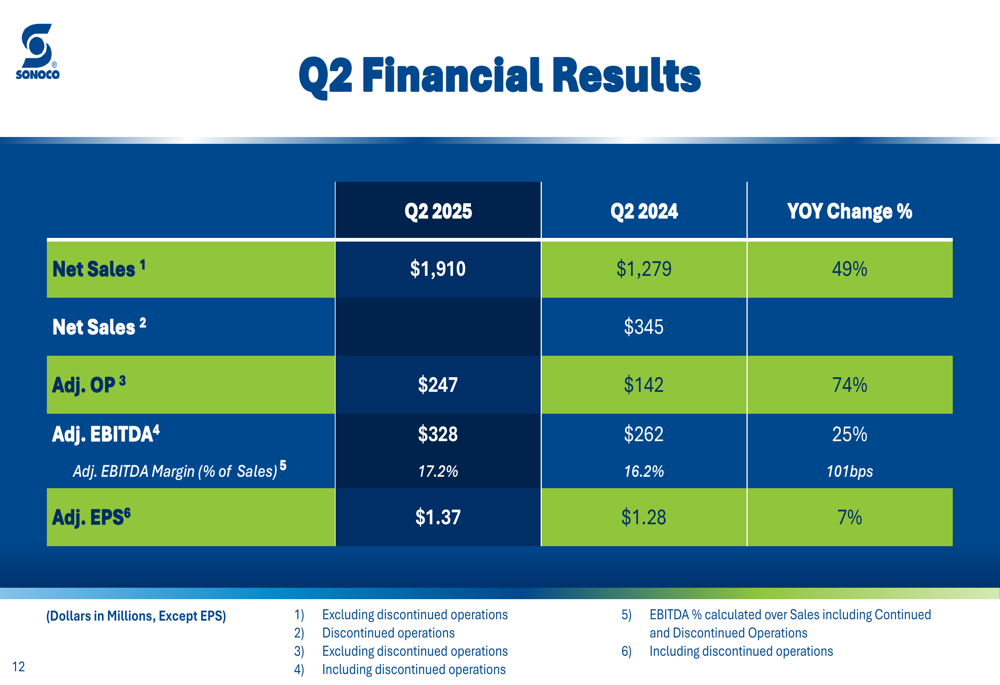

Sonoco delivered impressive financial results for Q2 2025, with revenue reaching $1.91 billion, a 49% increase compared to the same period last year. The company’s adjusted operating profit surged 74% to $247 million, while adjusted EBITDA grew 25% to $328 million with a margin improvement of 101 basis points to 17.2%.

As shown in the following comprehensive summary of Q2 results:

Adjusted earnings per share reached $1.37, representing a 7.1% year-over-year increase. This marks a slight decline from the $1.38 adjusted EPS reported in Q1 2025, which had missed analyst expectations at that time. The company noted that higher than projected interest expenses of approximately $10 million impacted the bottom line.

The detailed financial comparison between Q2 2025 and Q2 2024 further illustrates the company’s growth trajectory:

Segment Performance Analysis

The Consumer Packaging segment emerged as the standout performer, with sales more than doubling to $1.23 billion, a 110% increase year-over-year. This dramatic growth was primarily driven by the SMP EMEA acquisition and favorable pricing. Adjusted EBITDA for the segment surged 115% to $213 million.

The following chart illustrates the Consumer segment’s exceptional performance:

Meanwhile, the Industrial Paper Packaging segment demonstrated resilience and margin improvement despite a slight sales decline. While segment sales decreased by 2% to $588 million, adjusted EBITDA increased by 16% to $113 million, reflecting successful cost management and favorable pricing.

As shown in the Industrial segment results:

Rodger Fuller, Chief Operating Officer and Interim CEO of Sonoco Metal Packaging EMEA, noted that food can and end unit volumes were impacted in Q2 due to delayed packing season startup compared to last year, macroeconomic issues reducing demand across Europe, and decline in fish availability in Africa. However, pet food volumes remained strong, and the company secured a new 5-year pet food contract that could generate up to 400 million incremental units per year.

Strategic Initiatives & Portfolio Realignment

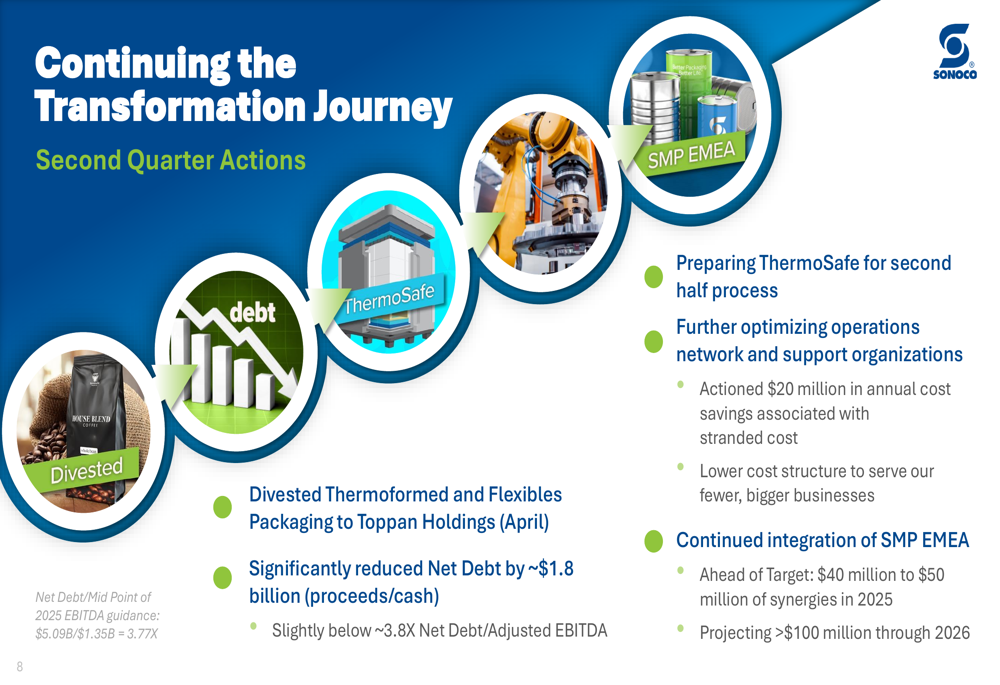

Sonoco continues to execute its strategic transformation, focusing on businesses that align with its core competencies in value-added packaging. In April, the company completed the divestiture of its Thermoformed and Flexibles Packaging business to Toppan Holdings, which contributed to a significant reduction in net debt by approximately $1.8 billion.

The company is also preparing its ThermoSafe business for a divestiture process in the second half of the year, further streamlining its portfolio. These strategic moves align with Sonoco’s focus on businesses with advanced material science, high product functionality, continuous process manufacturing, large global customers, and favorable market dynamics.

The following image illustrates Sonoco’s ongoing transformation journey:

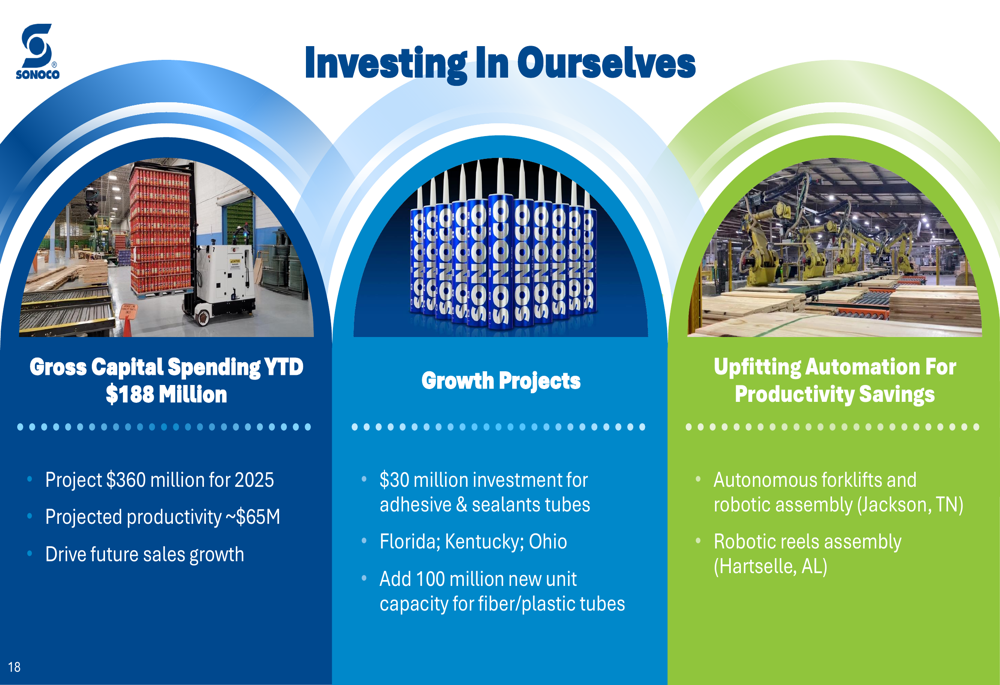

Sonoco is investing significantly in its core operations, with year-to-date capital spending of $188 million and projected full-year spending of $360 million. These investments are expected to drive approximately $65 million in productivity improvements and support future sales growth.

As shown in the company’s capital investment strategy:

Full-Year Outlook & Guidance

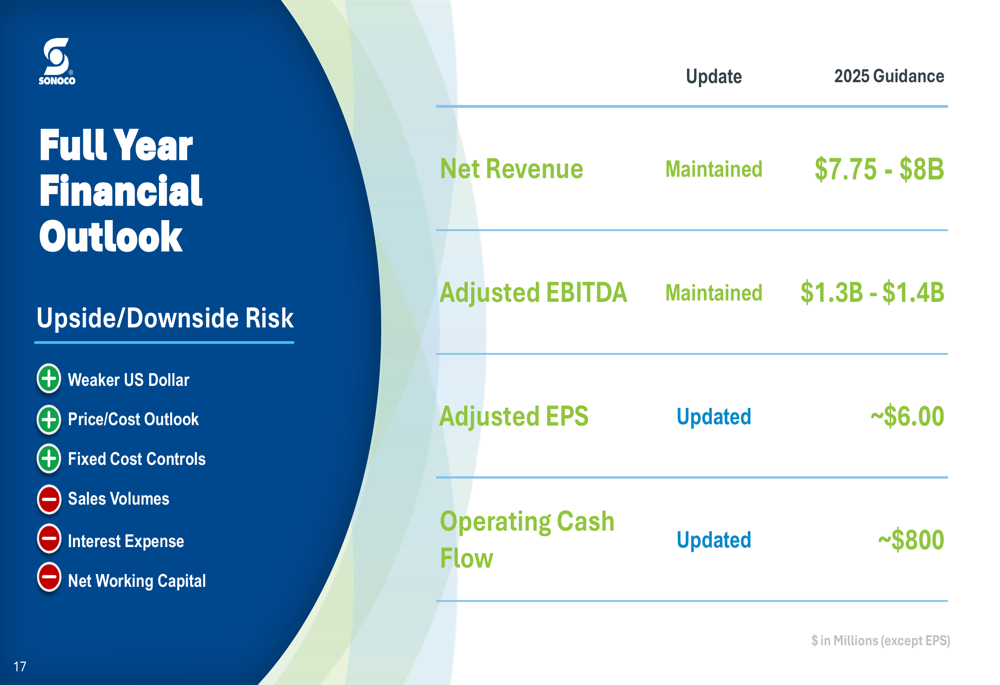

Sonoco maintained its full-year revenue guidance at $7.75-8.0 billion and adjusted EBITDA at $1.3-1.4 billion. However, the company updated its adjusted EPS target to approximately $6.00, which appears to be a slight downward revision from the previous guidance of $6.00-6.20 mentioned in the Q1 earnings report. Operating cash flow guidance was also adjusted to approximately $800 million, down from the previous range of $800-900 million.

The following slide details the company’s full-year financial outlook:

Management identified several factors that could impact full-year results, including currency fluctuations, price/cost outlook, fixed cost controls, sales volumes, interest expense, and net working capital management.

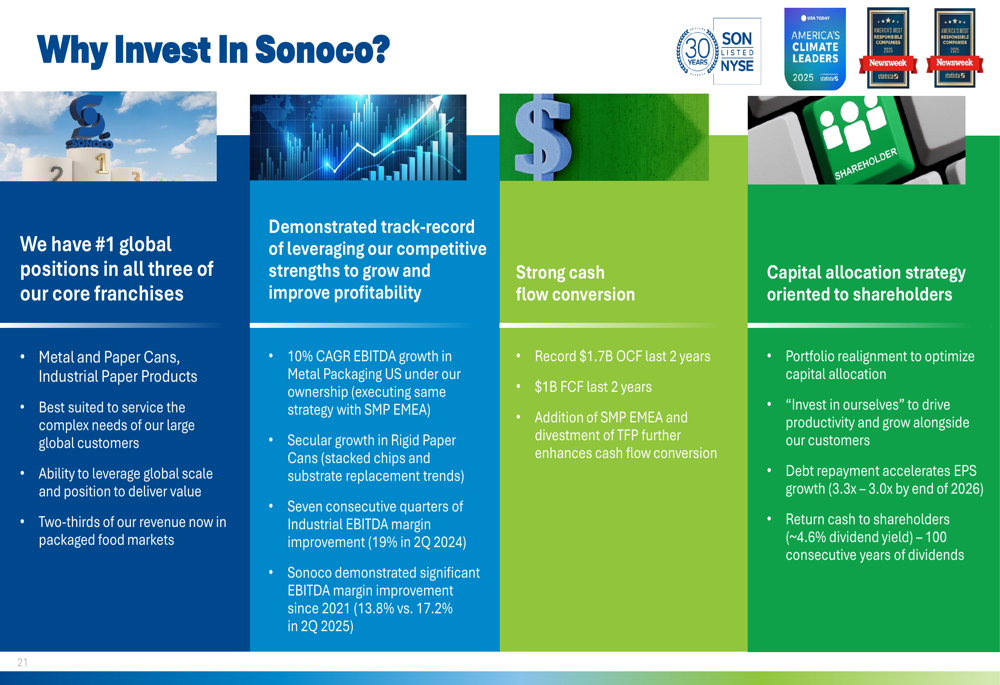

Investment Thesis & Conclusion

Sonoco presented a compelling investment case based on its leading global positions in core franchises, track record of growth and profitability improvement, strong cash flow conversion, and shareholder-oriented capital allocation strategy.

The company highlighted its 10% CAGR EBITDA growth in Metal Packaging US under its ownership and record operating cash flow of $1.7 billion over the past two years. Sonoco also noted its recent recognition as "Sustainable Packaging Company of the Year," underscoring its commitment to environmentally responsible packaging solutions.

As illustrated in the company’s investment thesis:

Following its strategic transformation, Sonoco projects a more focused business with approximately $7.75-8.0 billion in sales, 23,400 employees, 285 plants across 40 countries, and a balanced geographical footprint with 52% of sales in the Americas.

The "New Sonoco" is positioned as a global leader in sustainable packaging with strong market positions in its core businesses and improved financial metrics following its portfolio realignment. While the slight adjustments to full-year EPS and cash flow guidance suggest some caution, the overall trajectory remains positive with substantial year-over-year growth and continued strategic progress.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.