AlphaTON stock soars 200% after pioneering digital asset oncology initiative

Introduction & Market Context

Spar Nord Bank (CPH:SPNO) reported a significant decline in profits for the first half of 2025, primarily due to costs related to Nykredit’s takeover of the bank. Despite the bottom-line pressure, the bank demonstrated solid operational performance with strong lending growth and maintained its full-year guidance.

The Danish bank’s shares closed at DKK 209.60 on July 23, near its 52-week high of DKK 211.50, suggesting investors remain confident in the bank’s long-term prospects despite the short-term profit decline.

Quarterly Performance Highlights

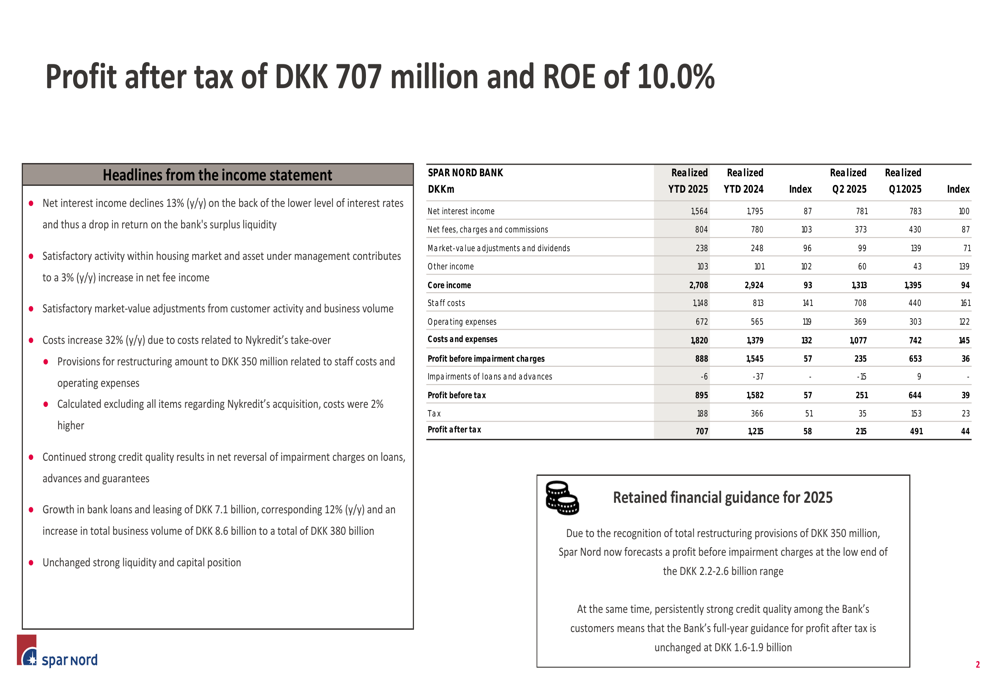

Spar Nord reported a profit after tax of DKK 707 million for H1 2025, down 42% from DKK 1,215 million in the same period last year. The decline was primarily attributed to restructuring provisions and costs related to Nykredit’s takeover, which significantly increased the bank’s operating expenses.

Core income decreased by 7% year-over-year to DKK 2,708 million, while total costs surged by 32% to DKK 1,820 million. Despite these challenges, the bank maintained its full-year guidance for profit after tax between DKK 1.6-1.9 billion.

As shown in the following income statement highlights:

Detailed Financial Analysis

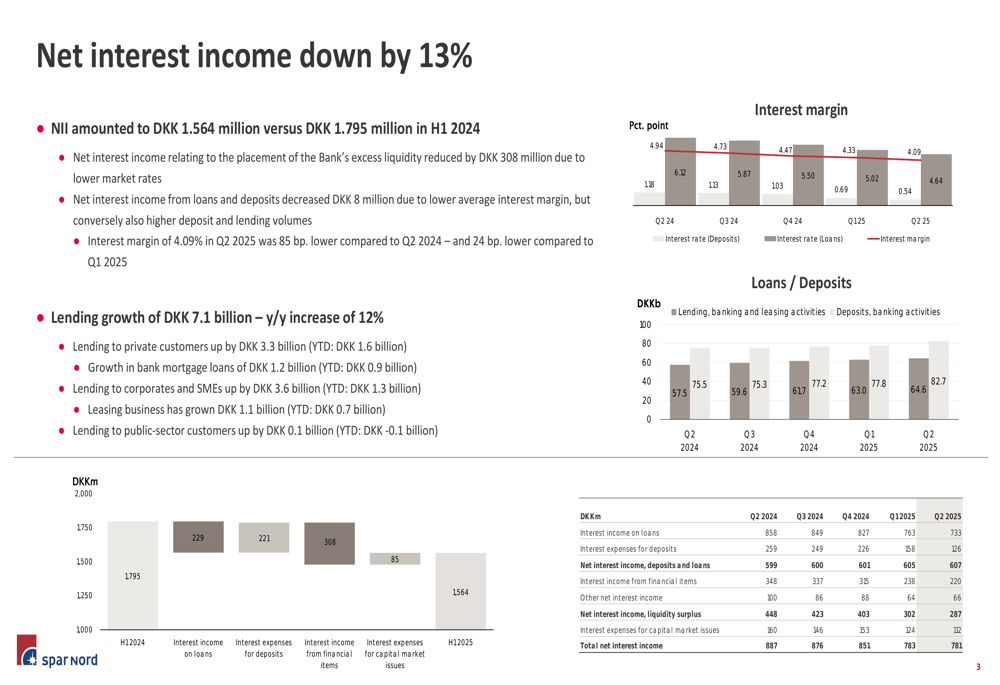

Net interest income declined by 13% year-over-year to DKK 1,564 million, primarily due to lower market rates affecting the placement of the bank’s excess liquidity. The interest margin contracted from 4.94% in Q2 2024 to 4.09% in Q2 2025.

However, this decline was partially offset by strong lending growth of 12% year-over-year, amounting to DKK 7.1 billion across private customers, bank mortgage loans, corporate and SME segments, and leasing business.

The following chart illustrates the trends in interest margin and loan growth:

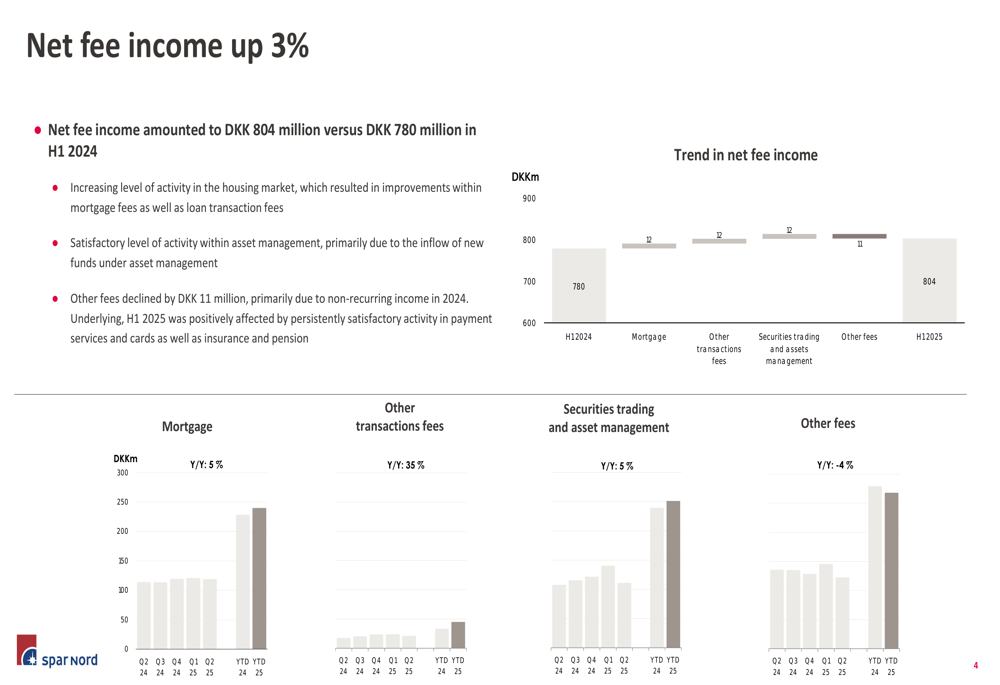

Net fee income showed positive momentum, increasing by 3% year-over-year to DKK 804 million. This growth was driven by increased activity in the housing market, which improved mortgage fees and loan transaction fees. Asset management also performed well, primarily due to the inflow of new funds under management.

The breakdown of fee income sources demonstrates these trends:

Market value adjustments and dividends remained relatively stable at DKK 238 million compared to DKK 248 million in H1 2024. Customer activity and business volume generated market value adjustments of DKK 219 million, while adjustments on equities and bonds contributed DKK 19 million, exclusively related to the bond portfolio.

Cost Structure and Efficiency

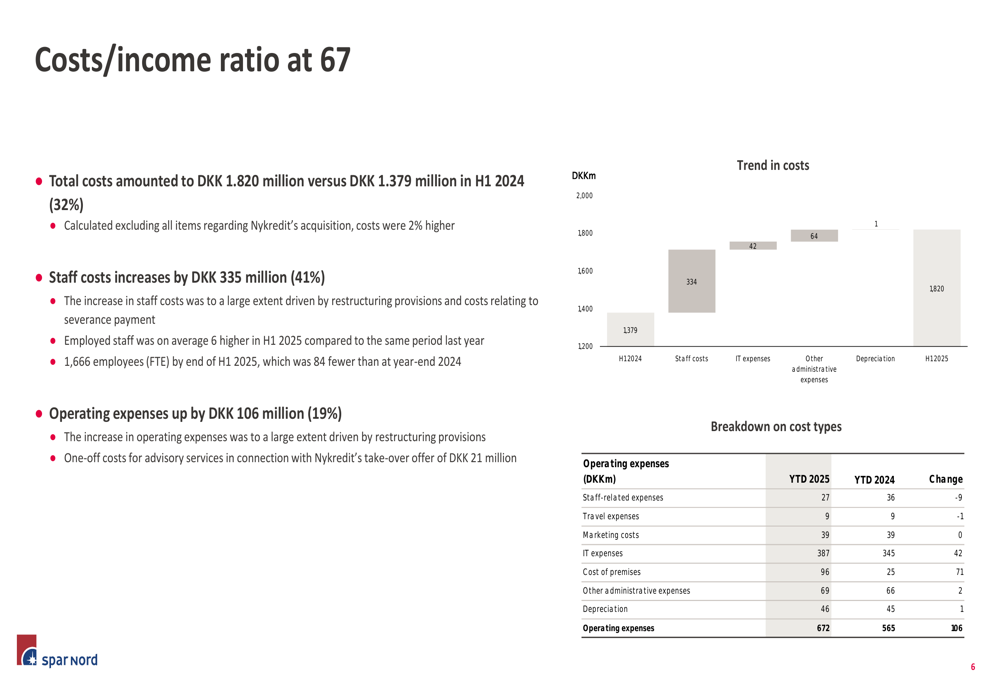

The most significant impact on Spar Nord’s H1 2025 results came from the substantial increase in costs, which rose 32% year-over-year to DKK 1,820 million. Staff costs increased by 41% to DKK 1,148 million, while operating expenses grew by 19% to DKK 672 million.

These increases were largely driven by restructuring provisions and costs relating to severance payments associated with Nykredit’s takeover. As a result, the cost-to-income ratio deteriorated to 67.

The following chart details the cost structure and its year-over-year changes:

Asset Quality and Credit Performance

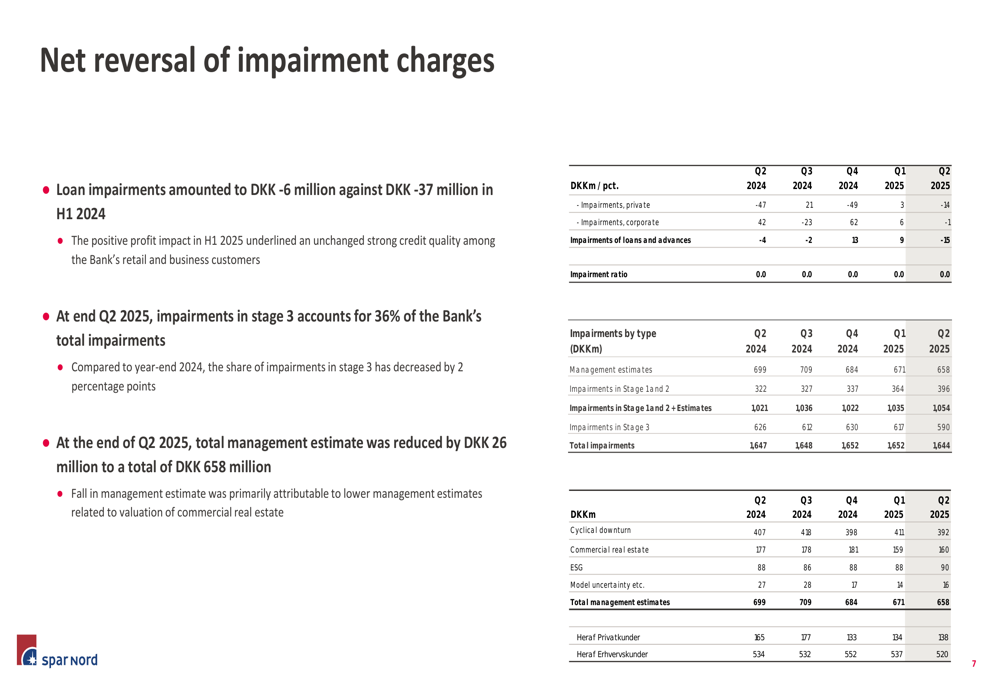

Despite the challenging profit picture, Spar Nord’s credit quality remained strong. The bank reported a net reversal of impairment charges of DKK 6 million in H1 2025, compared to a reversal of DKK 37 million in H1 2024.

At the end of Q2 2025, impairments in stage 3 (credit-impaired exposures) accounted for 36% of the bank’s total impairments. The management estimate for impairments was reduced by DKK 26 million to a total of DKK 658 million, reflecting confidence in the overall credit quality of the loan portfolio.

The detailed impairment analysis shows the breakdown by stages and categories:

Capital and Liquidity Position

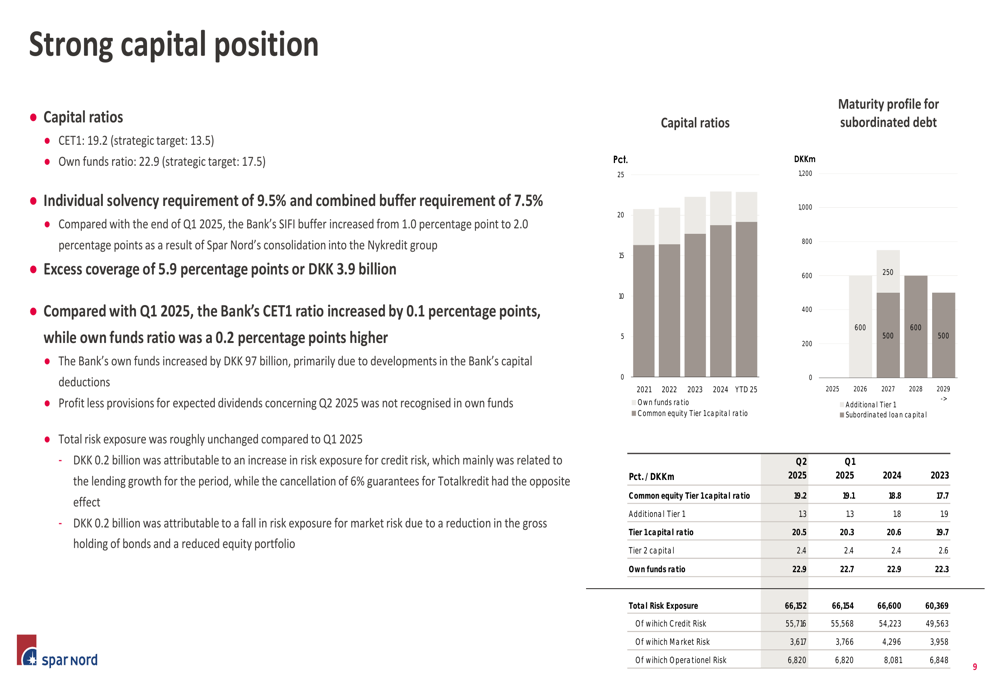

Spar Nord maintained a strong capital position, with a Common Equity Tier 1 (CET1) ratio of 19.2%, well above its strategic target of 13.5%. The own funds ratio stood at 22.9%, also comfortably exceeding the strategic target of 17.5%.

The bank’s individual solvency requirement was 9.5%, with a combined buffer requirement of 7.5%, providing substantial headroom above regulatory minimums.

The following chart illustrates the bank’s robust capital position:

Liquidity metrics remained exceptionally strong, with a Liquidity Coverage Ratio (LCR) of 459% and a Net Stable Funding Ratio (NSFR) of 120% at the end of H1 2025. Deposits excluding pooled schemes amounted to DKK 82.8 billion, representing 75% of the bank’s total funding.

Forward-Looking Statements

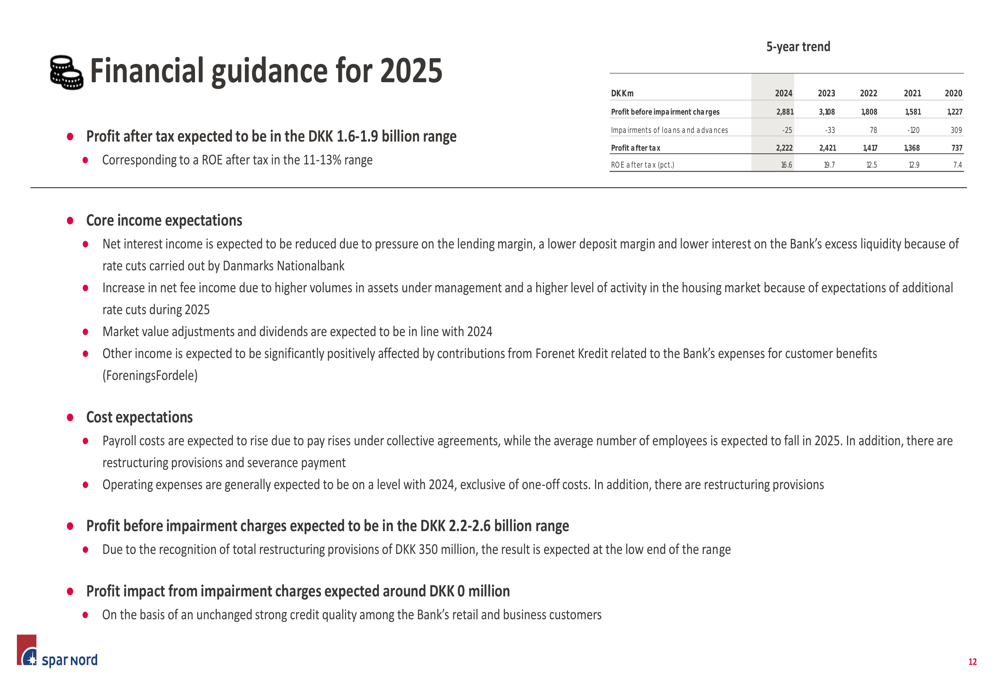

Despite the impact of restructuring costs, Spar Nord maintained its full-year guidance for 2025, expecting profit after tax to be in the range of DKK 1.6-1.9 billion. This corresponds to a return on equity (ROE) after tax in the 11-13% range.

However, due to the recognition of total restructuring provisions of DKK 350 million, the bank now forecasts profit before impairment charges to be at the lower end of the previously guided DKK 2.2-2.6 billion range.

The following chart shows the bank’s financial guidance for 2025 in the context of historical performance:

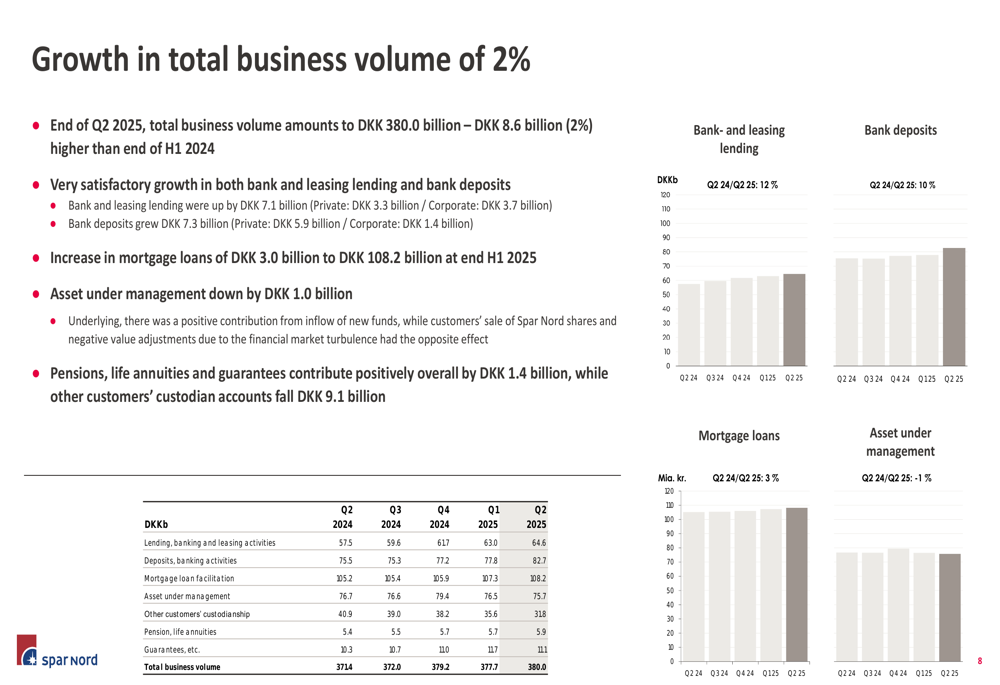

Spar Nord’s business volume growth remains strong, with total business volume amounting to DKK 380.0 billion at the end of Q2 2025, representing a 2% increase (DKK 8.6 billion) compared to the end of H1 2024. This growth was driven by increases in bank and leasing lending, bank deposits, and mortgage loans, partially offset by a slight decline in assets under management.

The bank’s maintained guidance suggests management expects stronger performance in the second half of 2025 as the impact of one-time restructuring costs diminishes and the benefits of strong lending growth and improved operational efficiency begin to materialize.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.