AlphaTON stock soars 200% after pioneering digital asset oncology initiative

Introduction & Market Context

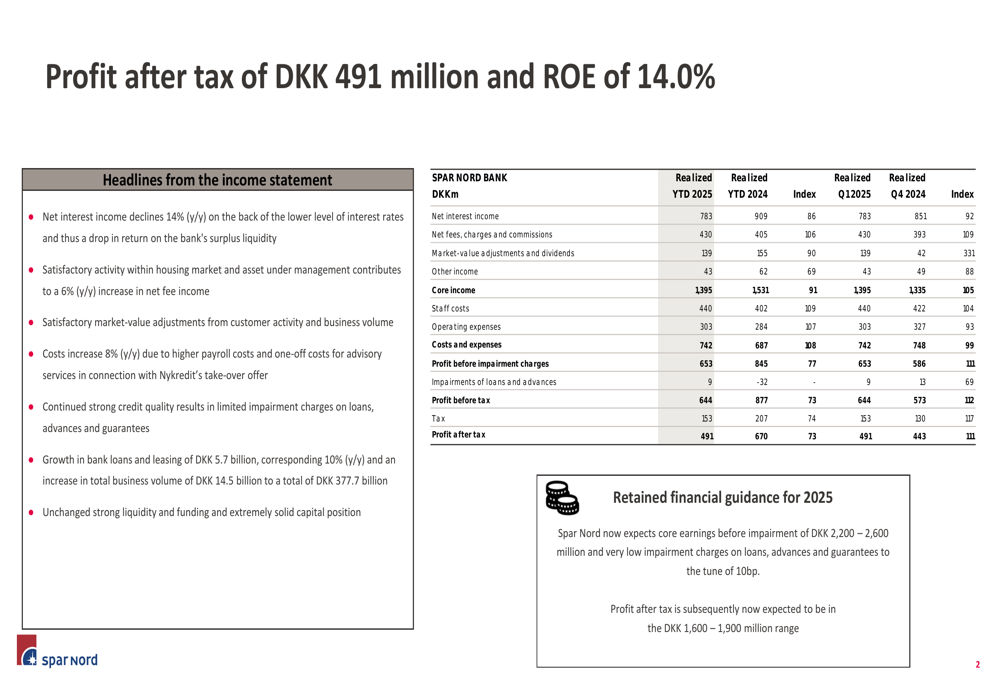

Spar Nord Bank (CPH:SPNO) presented its first quarter 2025 financial results on May 1, 2025, reporting a profit after tax of DKK 491 million and a return on equity of 14.0%. The Danish bank’s shares closed at DKK 211.40, experiencing a slight decline of 0.66% following the presentation.

The results come amid ongoing discussions regarding Nykredit’s takeover offer for Spar Nord, with the bank incurring DKK 21 million in one-off advisory costs related to the potential acquisition. Despite these expenses and a challenging interest rate environment, Spar Nord maintained solid profitability while growing its lending portfolio.

Quarterly Performance Highlights

Spar Nord’s Q1 2025 performance was characterized by strong lending growth offsetting pressure on interest margins. The bank reported core income of DKK 1,395 million, with profit before impairment charges reaching DKK 653 million. Impairment charges remained low at DKK 9 million, contributing to the solid bottom-line result.

As shown in the following financial highlights table, the bank delivered a profit after tax of DKK 491 million, with key metrics comparing favorably to previous periods despite some headwinds:

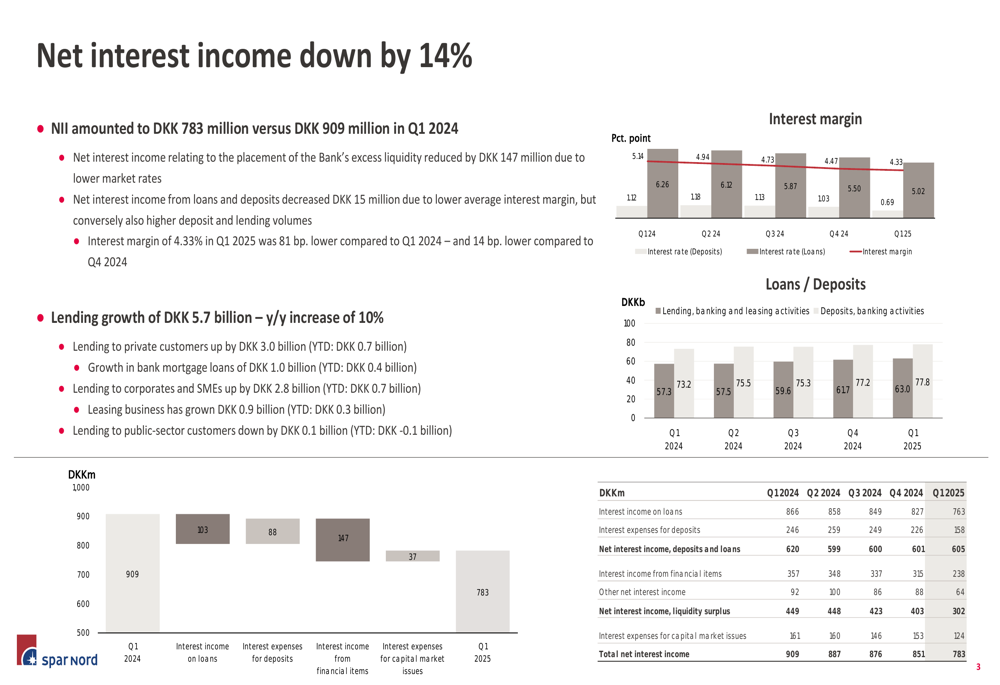

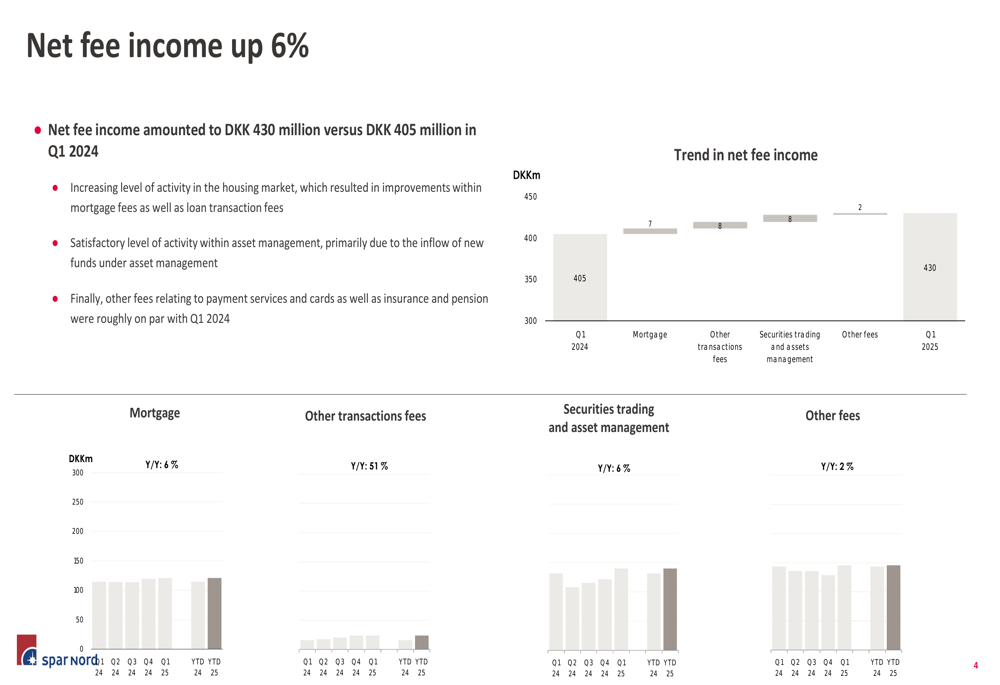

Net interest income declined 14% year-over-year to DKK 783 million, primarily due to lower market rates affecting the bank’s excess liquidity and a decrease in interest margin. However, this was partially offset by a 6% increase in net fee income to DKK 430 million, driven by strong activity in the housing market and asset management.

Detailed Financial Analysis

The decline in net interest income represents one of the main challenges for Spar Nord in Q1 2025. The interest margin contracted to 4.33% from 5.14% in Q1 2024, reflecting the impact of lower market rates on the bank’s profitability. Despite this pressure, lending growth of DKK 5.7 billion (10% year-over-year) helped mitigate some of the margin compression effects.

The following chart illustrates the evolution of net interest income and its components over the past five quarters:

On a more positive note, net fee income showed healthy growth, increasing to DKK 430 million from DKK 405 million in Q1 2024. This 6% improvement was primarily driven by higher activity in the housing market, resulting in increased mortgage fees and loan transaction fees, as well as continued inflows into asset management.

The following chart breaks down the sources of fee income growth:

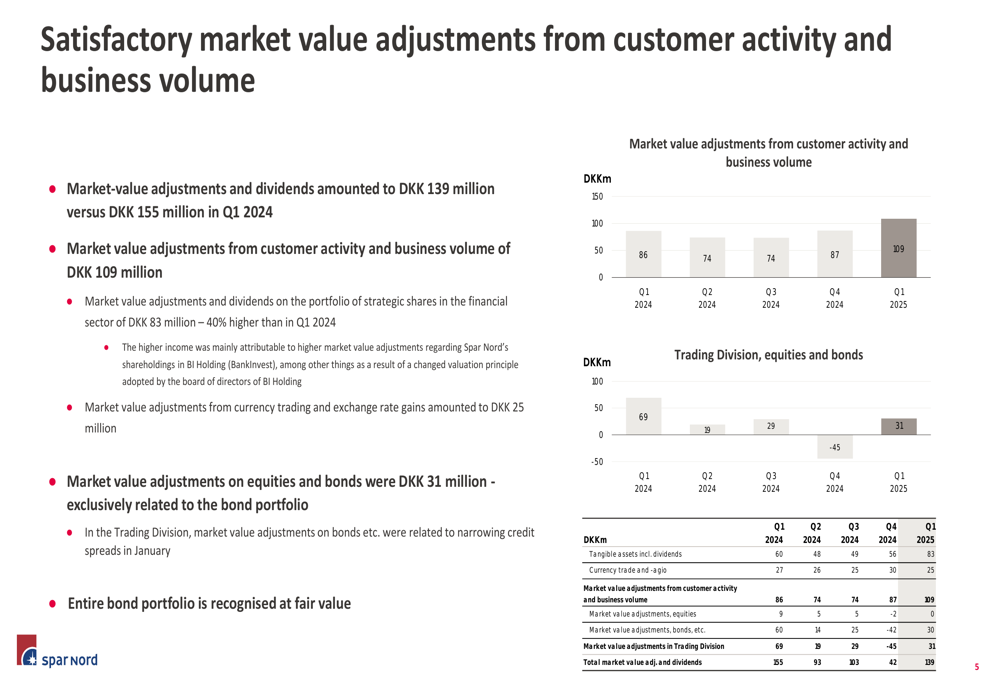

Market value adjustments and dividends contributed DKK 139 million to the quarter’s results, slightly down from DKK 155 million in Q1 2024. Customer activity and business volume generated DKK 109 million of these adjustments, while equities and bonds accounted for DKK 31 million.

Cost management remains an area of focus, with total costs increasing 8% year-over-year to DKK 742 million. Payroll costs rose by DKK 37 million (9%), while operating expenses increased by DKK 19 million (7%). However, excluding the DKK 21 million in one-off costs related to Nykredit’s takeover offer, underlying operating expenses actually decreased by DKK 2 million (-1%), demonstrating the bank’s commitment to operational efficiency.

Business Volume and Capital Position

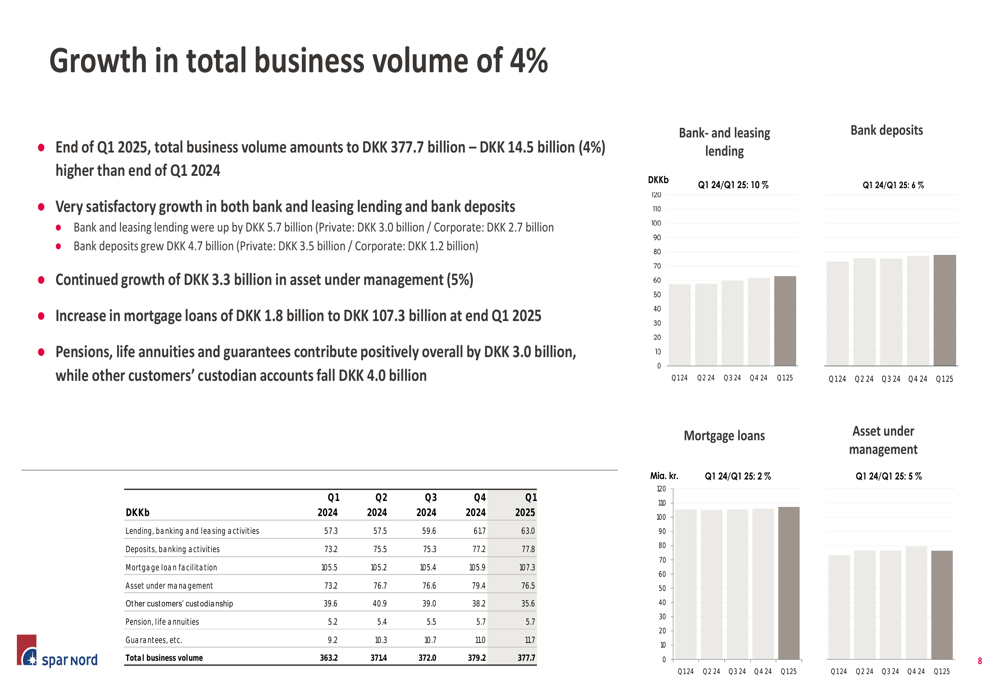

Spar Nord’s total business volume grew by DKK 14.5 billion (4%) year-over-year to reach DKK 377.7 billion by the end of Q1 2025. This growth was driven by increases across multiple segments, including a DKK 5.7 billion rise in bank and leasing lending, DKK 4.7 billion growth in bank deposits, DKK 3.3 billion increase in assets under management, and DKK 1.8 billion expansion in mortgage loans.

The following chart illustrates the growth across these key business segments:

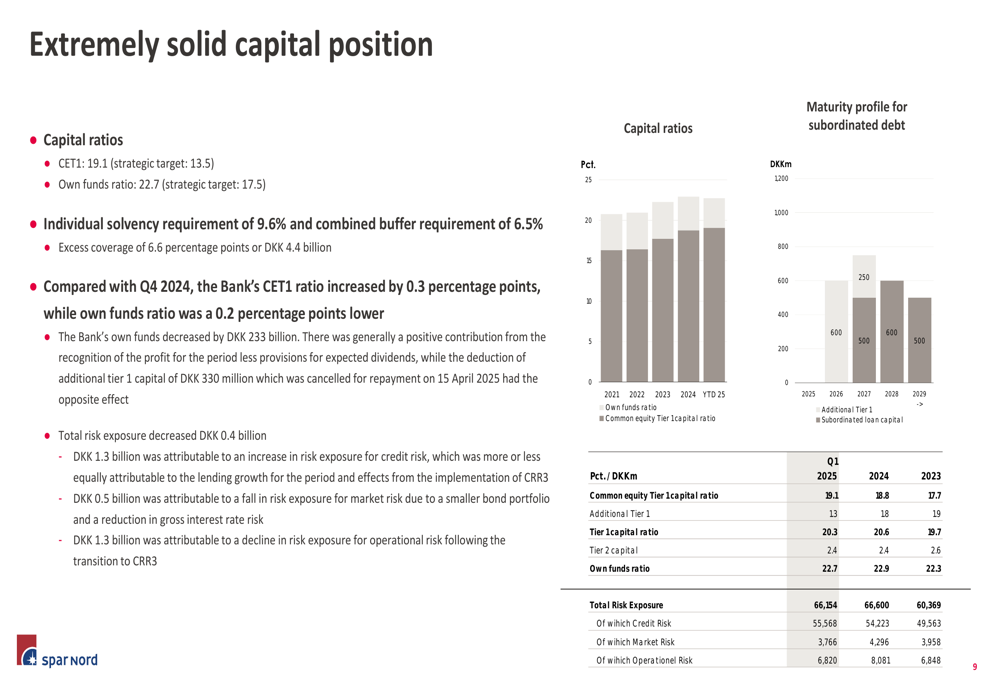

The bank maintained a strong capital position, with a Common Equity Tier 1 (CET1) ratio of 19.1% and an own funds ratio of 22.7%. This represents excess coverage of 6.6 percentage points or DKK 4.4 billion above regulatory requirements. Compared to Q4 2024, the CET1 ratio increased by 0.3 percentage points, while the own funds ratio decreased slightly by 0.2 percentage points.

Liquidity metrics also remained robust, with the Liquidity Coverage Ratio (LCR) at 296% and the Net Stable Funding Ratio (NSFR) at 131%, both well above regulatory requirements. Deposits excluding pooled schemes amounted to DKK 77.9 billion, representing 70% of the bank’s total funding.

Forward-Looking Statements

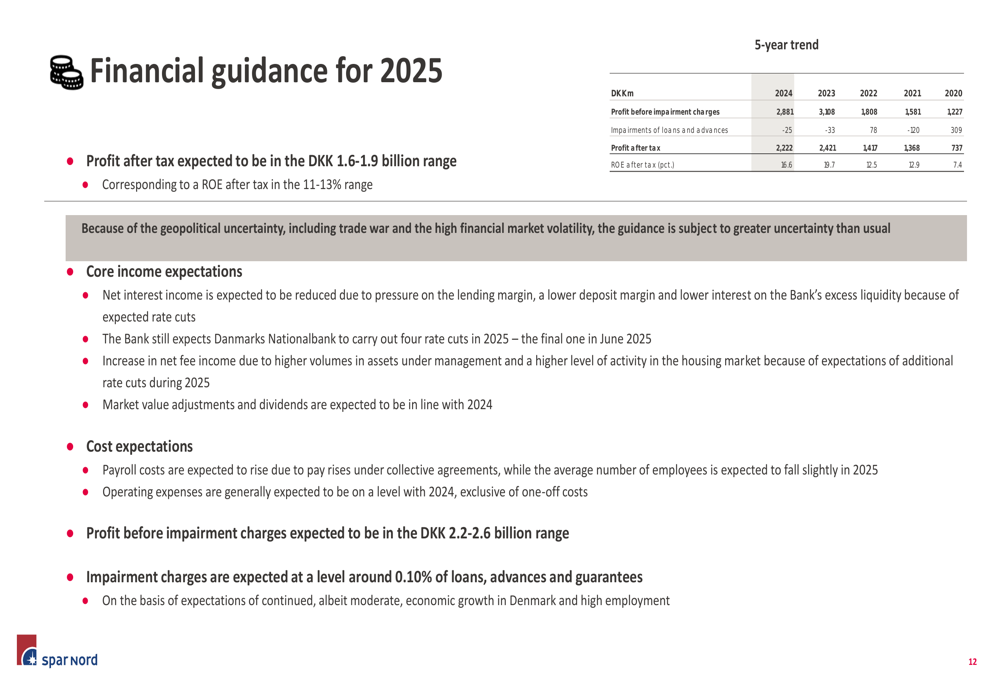

Spar Nord maintained its financial guidance for 2025, expecting core earnings before impairment of DKK 2,200-2,600 million and profit after tax in the range of DKK 1,600-1,900 million. This corresponds to a return on equity after tax of 11-13%. The bank anticipates very low impairment charges on loans, advances, and guarantees, around 10 basis points.

The following table presents Spar Nord’s five-year financial trend and outlook:

CEO Lasse Nyby expressed confidence in the bank’s ability to navigate the current interest rate environment while continuing to grow its business volumes. The ongoing discussions regarding Nykredit’s takeover offer remain a key focus area, with further developments expected in the coming quarters.

Despite the challenges posed by declining interest margins, Spar Nord’s strong lending growth, fee income performance, and solid capital position provide a foundation for continued profitability as the bank moves through 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.