Gold prices edge lower; heading for weekly losses ahead of U.S.-Russia talks

Introduction & Market Context

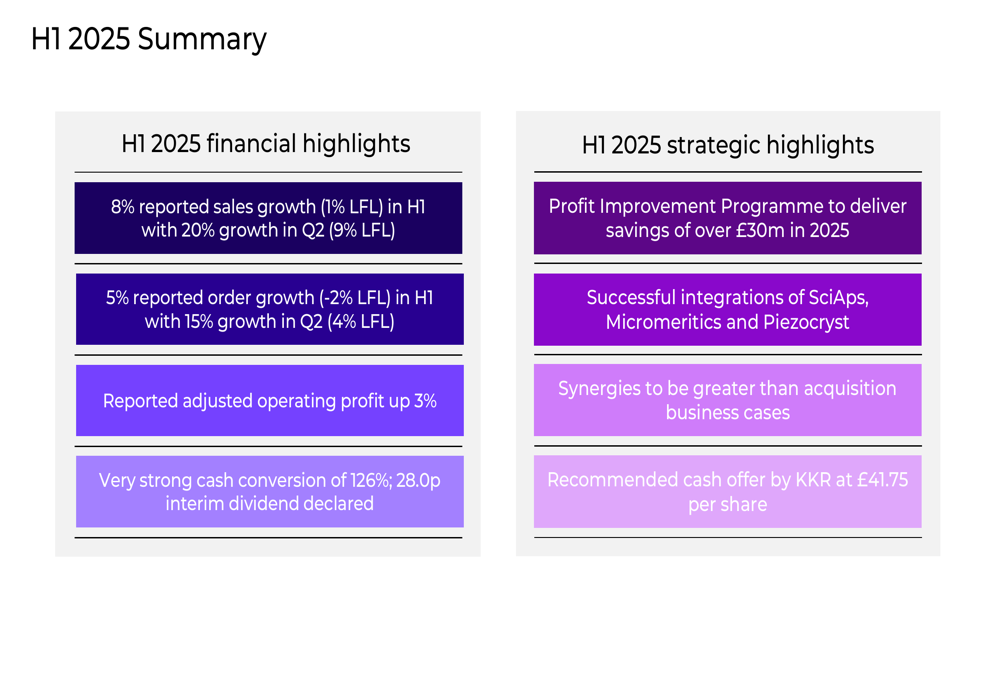

Spectris plc (LSE:LON:SXS) presented its half-year 2025 results on August 7, showing a significant recovery in the second quarter after a challenging start to the year. The precision measurement and testing equipment specialist reported 8% reported sales growth (1% like-for-like) for H1, with Q2 showing impressive 20% growth (9% LFL). The presentation comes amid a recommended cash offer from KKR at £41.75 per share, adding a layer of strategic significance to the company’s performance metrics.

The company’s stock is currently trading around 4,134p, showing a slight increase of 0.05% on the day of the presentation. This represents a recovery from earlier in the year, though still below the offer price from KKR.

As shown in the following summary of H1 2025 financial and strategic highlights:

Quarterly Performance Highlights

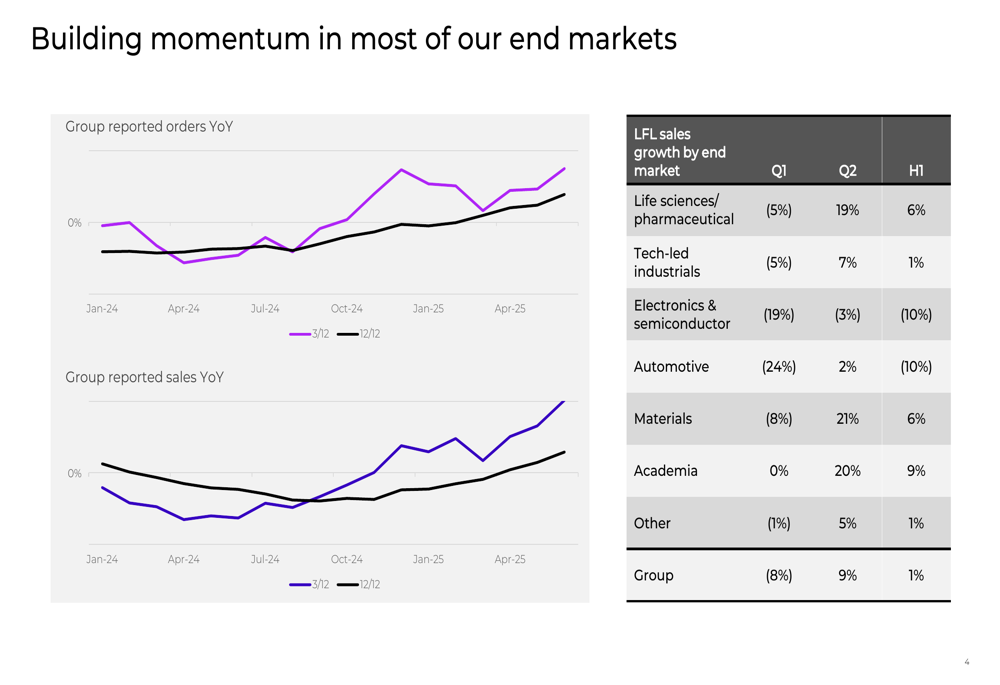

After a challenging first quarter where LFL sales declined by 8%, Spectris demonstrated strong recovery momentum in Q2 with 9% LFL sales growth. This pattern was also reflected in orders, which showed 4% LFL growth in Q2 after declining in Q1, resulting in an overall book-to-bill ratio of 1.02x for the half-year.

The company’s end markets showed mixed performance, with particularly strong recovery in materials (21% Q2 growth) and academia (20% Q2 growth). The life sciences/pharmaceutical sector also rebounded strongly with 19% growth in Q2 after a 5% decline in Q1. However, the electronics & semiconductor sector remained challenging with a 3% decline in Q2, though this represented an improvement from the 19% drop in Q1.

The following chart illustrates the performance across different end markets:

Detailed Financial Analysis

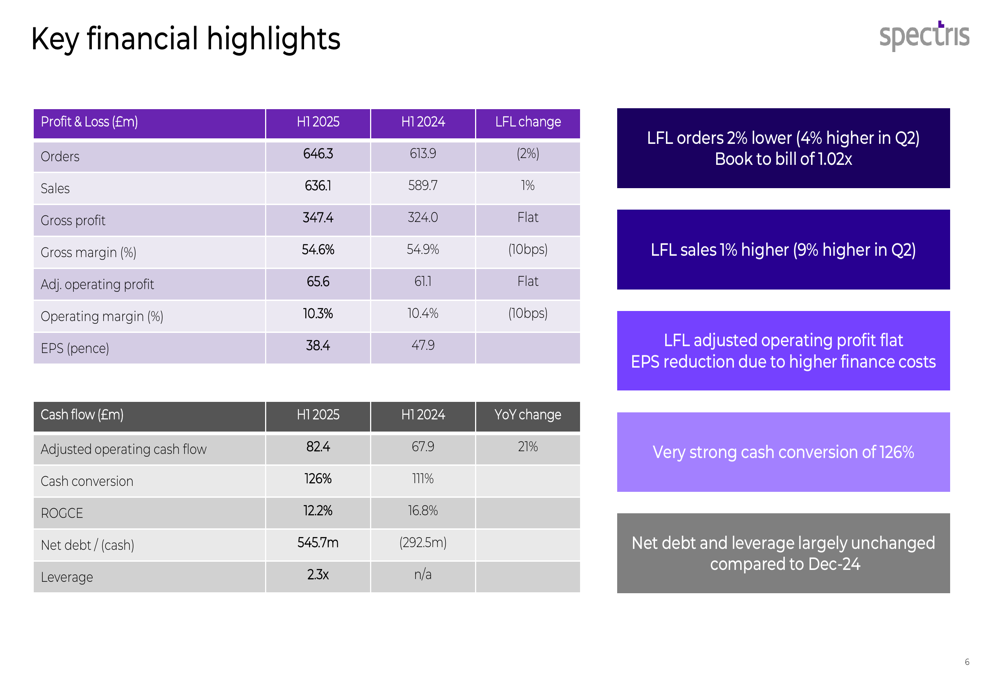

Spectris reported adjusted operating profit of £65.6 million for H1 2025, up 3% on a reported basis but flat on a like-for-like basis compared to H1 2024. The company maintained a solid adjusted operating margin of 10.3%, only slightly below the 10.4% achieved in the same period last year.

Cash performance was particularly strong, with adjusted operating cash flow of £82.4 million, representing a 21% year-on-year increase. This translated to an impressive cash conversion rate of 126%, up from 111% in H1 2024. The company’s financial position has changed significantly, moving from a net cash position of £292.5 million in H1 2024 to a net debt position of £545.7 million, with leverage at 2.3x, primarily due to acquisitions.

The comprehensive financial highlights are presented in the following table:

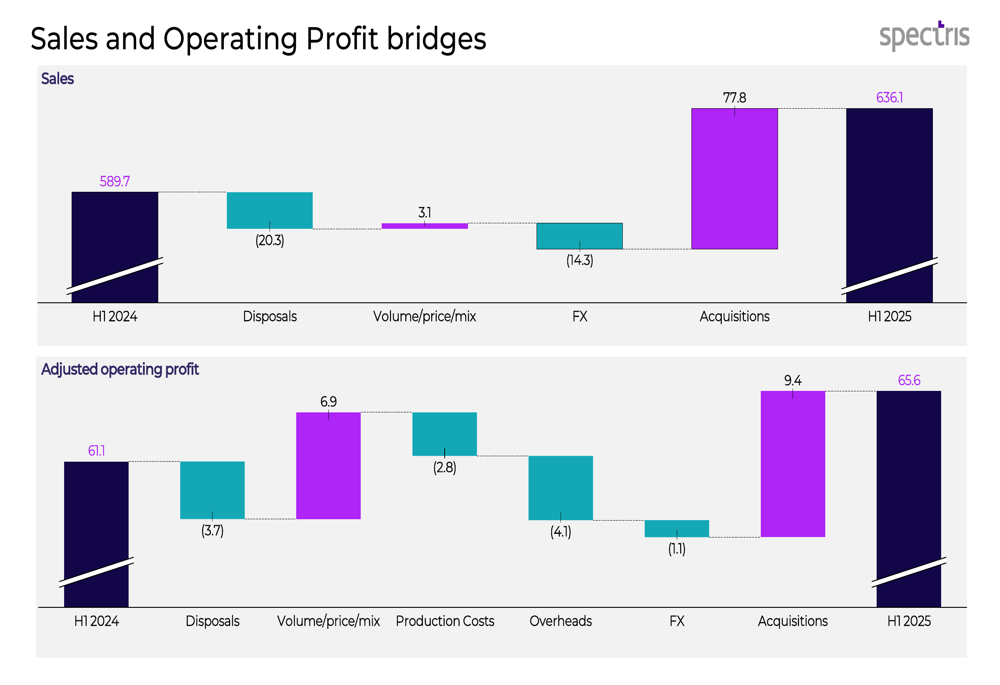

A closer look at the drivers of sales and profit changes reveals the significant impact of acquisitions, which contributed £77.8 million to sales and £9.4 million to adjusted operating profit. This helped offset the negative impact of disposals and foreign exchange movements. The company also achieved £6.9 million in volume/price/mix improvements, though this was partially offset by increased production costs and overheads.

The following bridge charts illustrate these movements:

Segment Performance

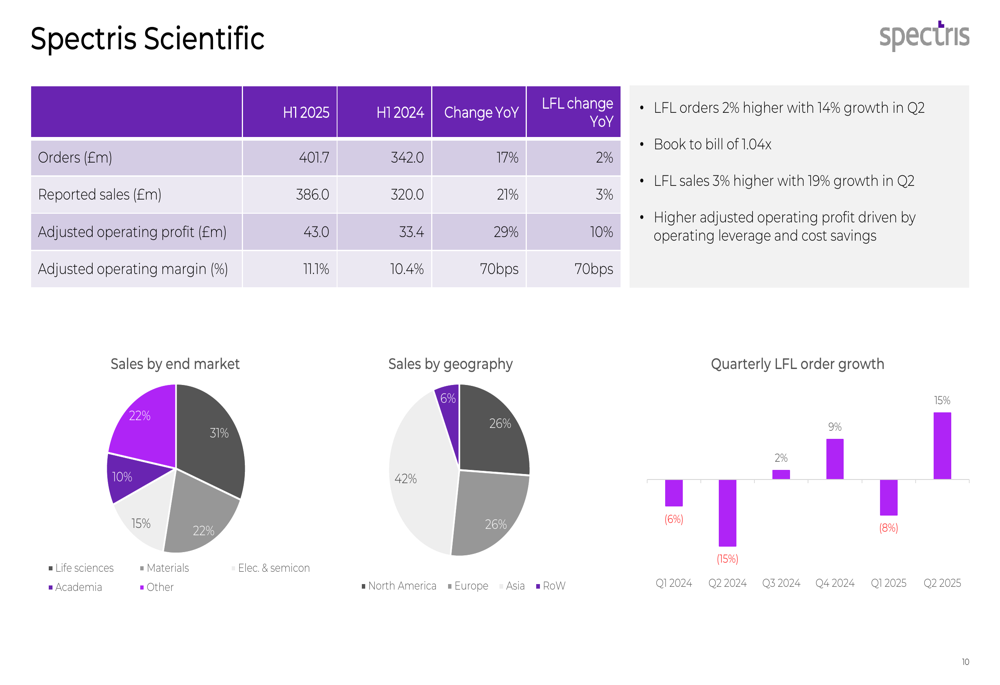

Spectris Scientific emerged as the stronger performer of the company’s two divisions, with reported sales growth of 21% (3% LFL) and adjusted operating profit growth of 29% (10% LFL). The division showed particularly strong momentum in Q2, with 19% LFL sales growth and a book-to-bill ratio of 1.04x. The adjusted operating margin improved by 70 basis points to 11.1%.

The division’s performance across different end markets and geographies is detailed in the following slide:

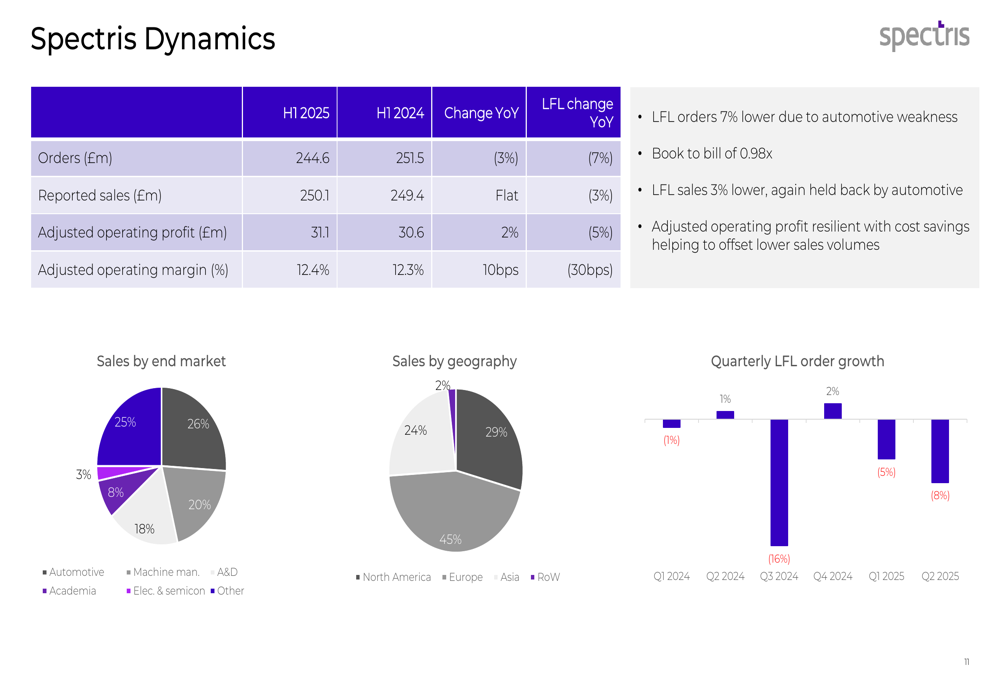

In contrast, Spectris Dynamics faced more challenging conditions, particularly in the automotive sector. The division reported flat sales growth (-3% LFL) and 2% growth in adjusted operating profit (-5% LFL). Despite these challenges, the division maintained its operating margin at 12.4%, slightly up from 12.3% in H1 2024, demonstrating effective cost management.

The division’s performance was affected by a 7% LFL decline in orders, with particular weakness in the automotive sector. However, management noted that cost savings helped offset lower sales volumes:

Strategic Initiatives

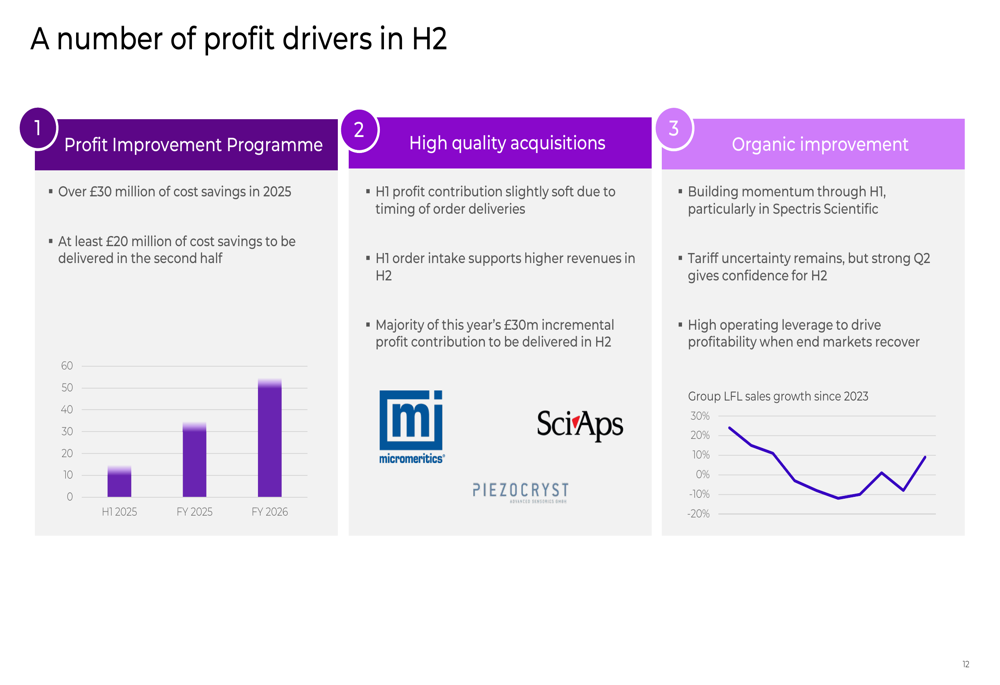

Spectris highlighted three key profit drivers for H2 2025. First, the Profit Improvement Programme is expected to deliver over £30 million in cost savings for the full year, with at least £20 million to be realized in the second half. Second, the company’s recent acquisitions (Micromeritics, SciAps, and Piezocryst) are expected to make a stronger contribution in H2, supported by strong order intake in H1. Third, the organic improvement seen through H1, particularly in Spectris Scientific, is expected to continue.

The company’s strategic focus on these profit drivers is illustrated in the following slide:

Forward-Looking Statements

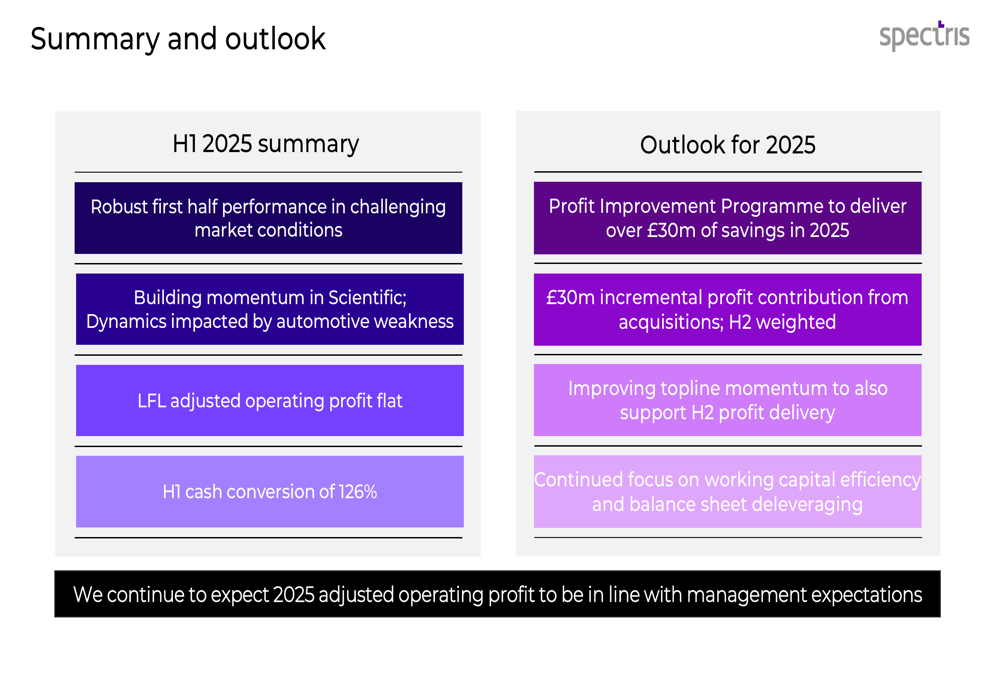

Looking ahead, Spectris remains confident in its outlook for the remainder of 2025, despite ongoing market uncertainties. The company expects adjusted operating profit to be in line with management expectations, supported by the Profit Improvement Programme, acquisition contributions, and improving topline momentum.

Management also emphasized continued focus on working capital efficiency and balance sheet deleveraging, which will be important given the shift to a net debt position following recent acquisitions.

The company’s summary and outlook are presented in the following slide:

KKR Acquisition Offer

A significant development mentioned in the presentation is the recommended cash offer from KKR at £41.75 per share. While details of the offer were not extensively discussed in the slides, this represents a premium to the current trading price and adds an important strategic dimension to the company’s near-term outlook.

The offer comes after Spectris has completed a significant portfolio transformation, having made eight disposals and invested £1.1 billion in 16 acquisitions, while also returning £1.1 billion to shareholders since 2019. This transformation has positioned the company as a more focused entity with two world-class divisions in high-growth markets.

In conclusion, Spectris’s H1 2025 results demonstrate a company in transition, with a strong recovery in Q2 offsetting a weak start to the year. The combination of strategic acquisitions, cost-saving initiatives, and organic improvements provides a solid foundation for H2 performance, while the KKR offer presents shareholders with a potential exit opportunity at a premium valuation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.