Fubotv earnings beat by $0.10, revenue topped estimates

Introduction & Market Context

Sprout Social (NASDAQ:SPT) released its Q2 FY2025 investor presentation on August 6, 2025, highlighting continued revenue growth and profitability improvements, alongside a significant acquisition to expand its service offerings. The social media management platform provider continues to capitalize on the growing importance of social channels for businesses, noting that over 5.24 billion consumers now use social media globally.

Despite solid operational performance, Sprout Social’s stock has faced pressure in recent months, trading at $16.23 at market close on August 6, with a slight 1.97% gain in after-hours trading. The stock remains well below its 52-week high of $36.30, reflecting broader market concerns about growth deceleration in the tech sector.

Quarterly Performance Highlights

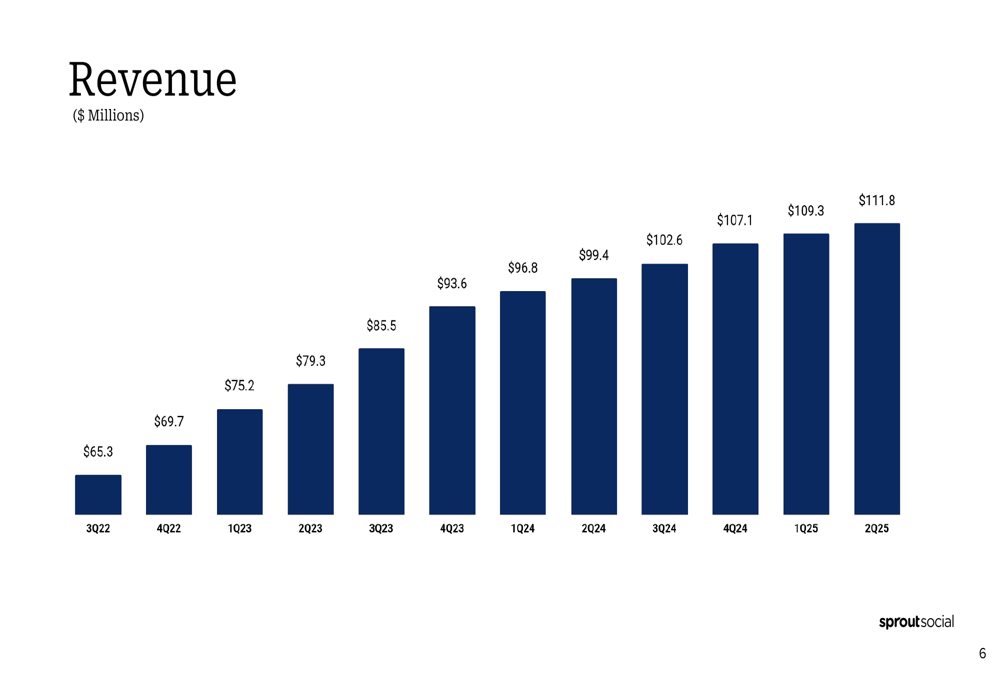

Sprout Social reported Q2 FY2025 revenue of $111.8 million, representing 12% year-over-year growth compared to $99.4 million in Q2 FY2024. The company maintains a subscription-heavy business model with 99% of revenue coming from subscriptions and a healthy gross profit margin of 78%.

As shown in the following chart of quarterly revenue growth, Sprout has maintained consistent revenue increases over the past three years, though the growth rate has moderated from previous years:

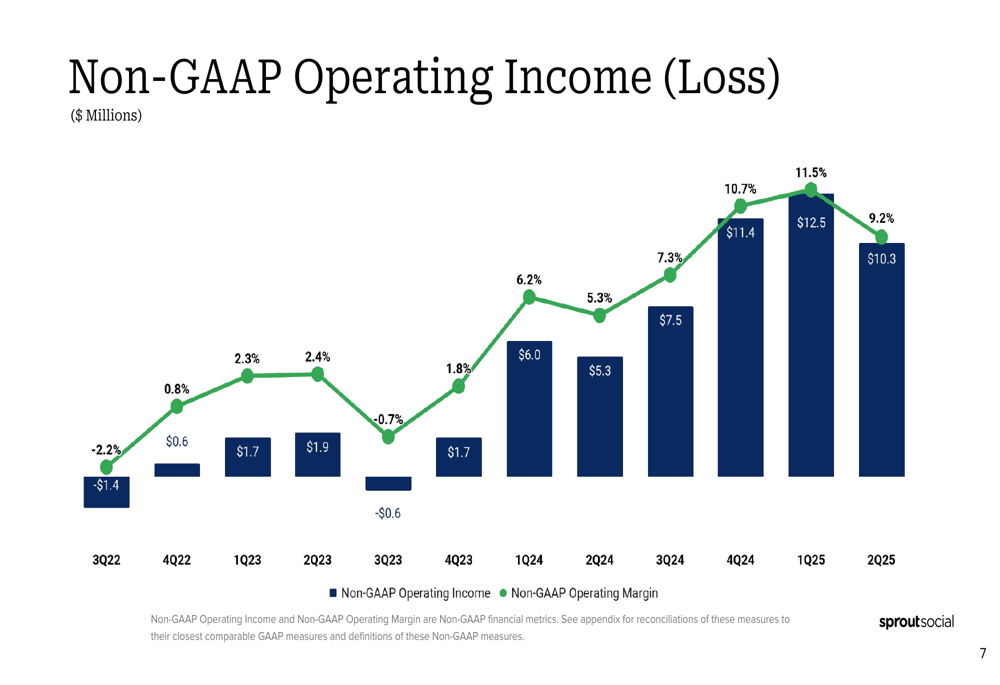

The company’s profitability metrics showed notable improvement, with Non-GAAP Operating Margin reaching 9% in Q2 FY2025, up from 5% in the same period last year. This represents a continuation of the positive trend in operating income, though it marks a slight decrease from the record 11.5% operating margin achieved in Q1 FY2025.

The following chart illustrates Sprout’s improving profitability trajectory:

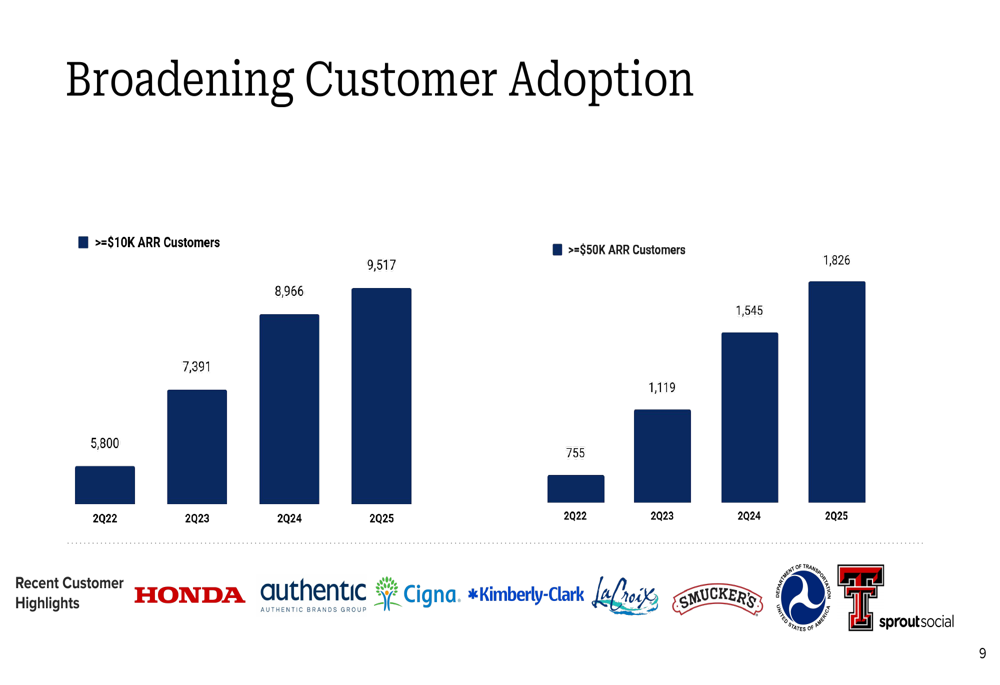

Sprout Social’s customer metrics demonstrated continued success in moving upmarket. The company now serves approximately 30,000 customers across more than 100 countries. More importantly, the number of customers contributing $50,000 or more in annual recurring revenue (ARR) grew to 1,826, up from 1,545 a year earlier, representing an 18% increase.

The following visualization shows the company’s success in expanding its base of high-value customers:

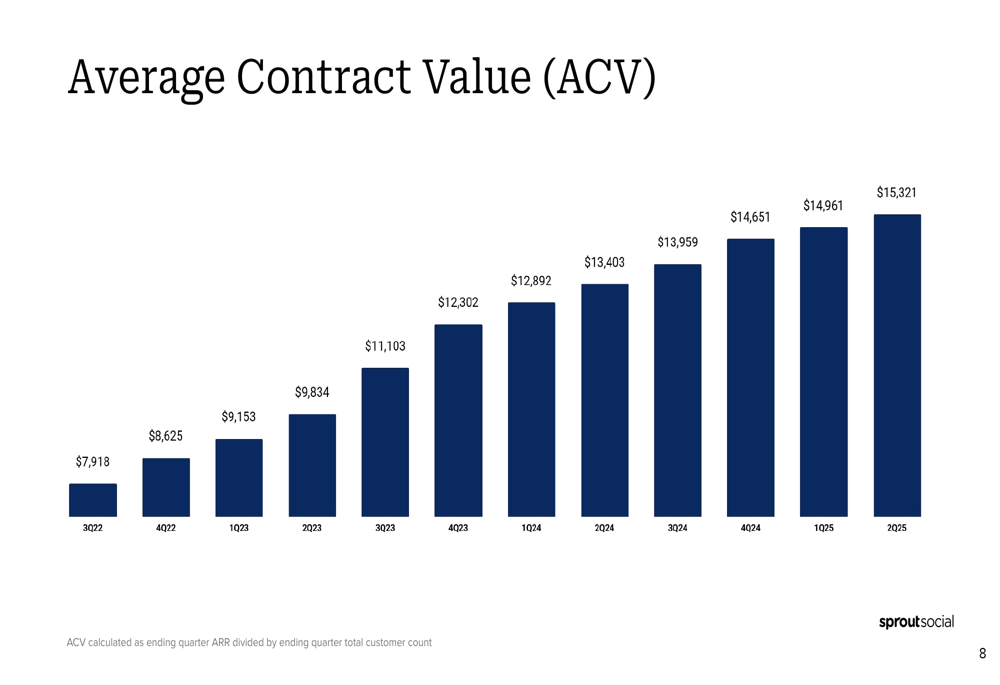

Average Contract Value (ACV) continued its upward trajectory, reaching $15,321 in Q2 FY2025, a 14% increase from $13,403 in Q2 FY2024. This metric highlights Sprout’s ability to extract more value from its customer relationships through upselling and cross-selling additional products.

As shown in the following chart, ACV has grown consistently over the past three years:

Strategic Initiatives: NewsWhip Acquisition

The most significant strategic announcement in the presentation was Sprout Social’s acquisition of NewsWhip, a media intelligence platform. The acquisition, which closed on July 30, 2025, was valued at $55 million in cash with up to $10 million in additional performance-based earnouts. The company funded the purchase through its revolving credit facility.

The following slide details the acquisition terms and strategic rationale:

This acquisition represents a strategic expansion into the PR and crisis monitoring space, complementing Sprout’s existing social media management capabilities. NewsWhip’s AI-powered predictive media intelligence will allow Sprout to offer enhanced services to its enterprise customers.

The NewsWhip platform provides rich context on emerging issues and unique metrics to predict the scale and impact of media stories, as illustrated below:

The acquisition addresses specific use cases for sophisticated brands, including monitoring live issues, gaining insights on the media landscape, and distributing updates internally:

Forward-Looking Statements

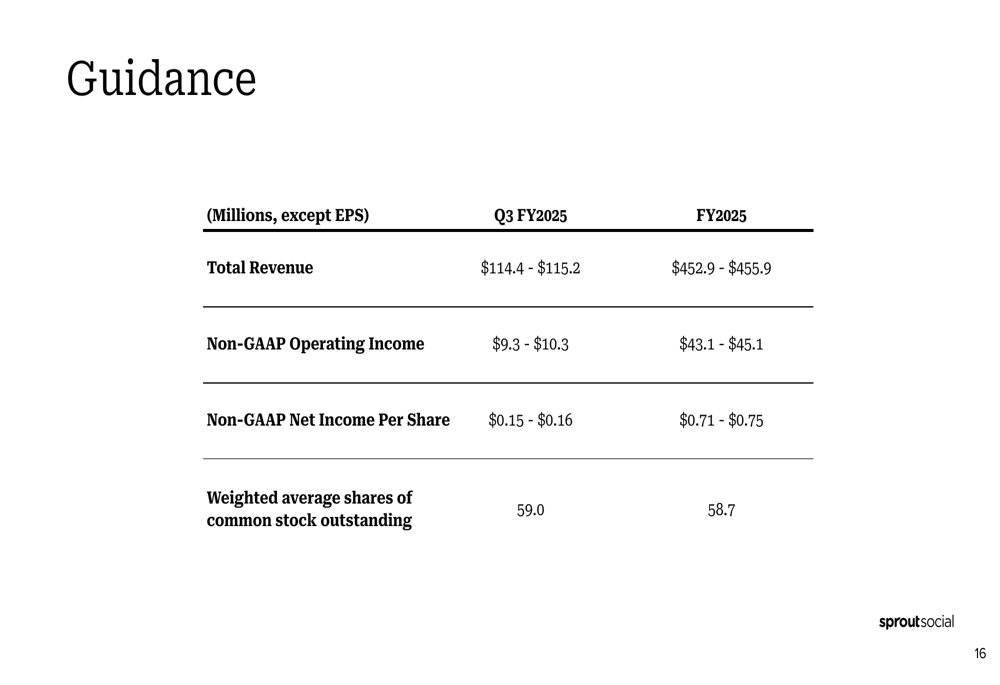

Sprout Social provided financial guidance for Q3 FY2025 and the full fiscal year. For Q3, the company expects revenue between $114.4 million and $115.2 million, with Non-GAAP Operating Income between $9.3 million and $10.3 million.

For the full year FY2025, Sprout projects revenue of $452.9 million to $455.9 million and Non-GAAP Operating Income of $43.1 million to $45.1 million. This guidance incorporates the expected impact of the NewsWhip acquisition.

The following table details the company’s financial guidance:

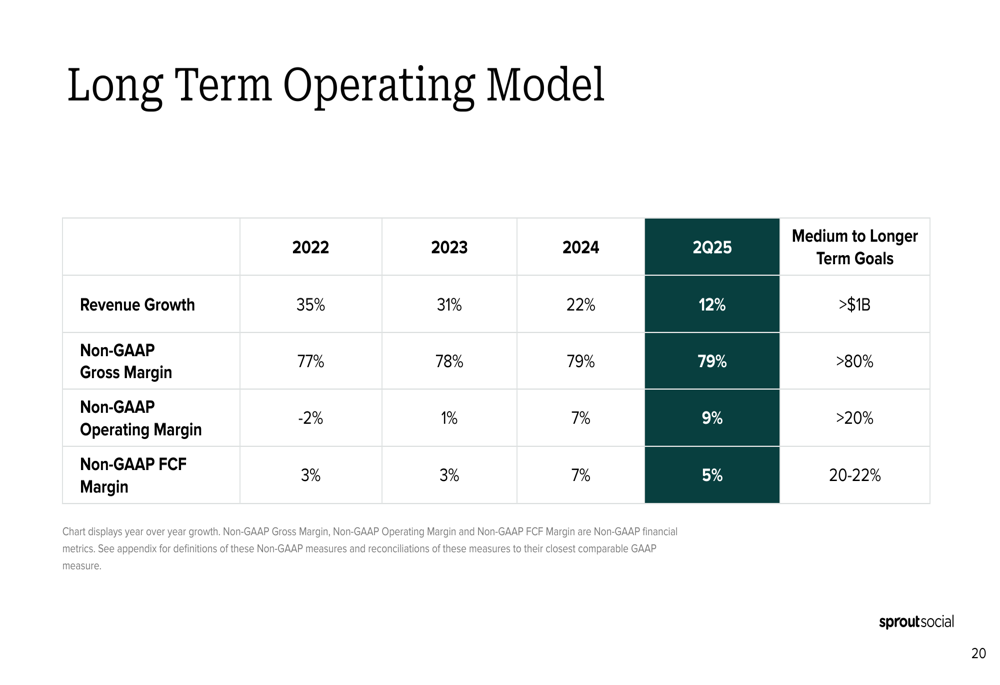

Looking further ahead, Sprout Social outlined its medium to long-term financial goals, targeting revenue exceeding $1 billion, Non-GAAP Gross Margin above 80%, Non-GAAP Operating Margin exceeding 20%, and Non-GAAP Free Cash Flow Margin of 20-22%.

The company’s long-term operating model shows steady improvement in profitability metrics over time, though revenue growth has decelerated from 35% in 2022 to 12% in 2025:

Growth Strategy and Investment Thesis

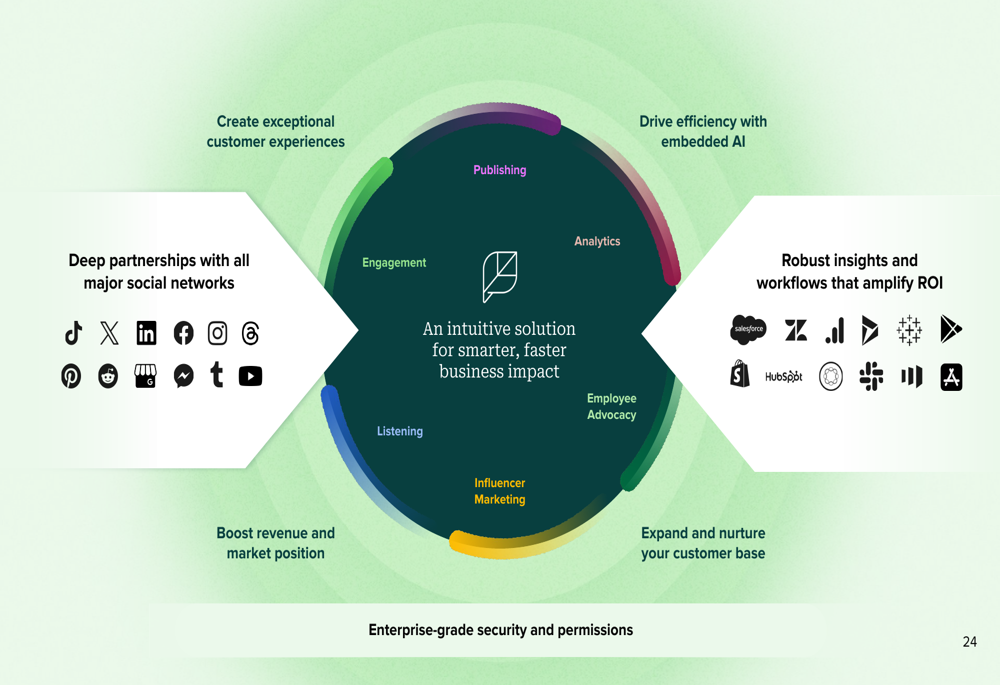

Sprout Social’s growth strategy centers around four key pillars: winning enterprise customers, improving customer health and adoption, expanding partnerships and ecosystem, and increasing account penetration. The company emphasized its focus on consolidating social media management into a single, integrated platform that serves multiple functions across organizations.

The Sprout Social platform aims to create exceptional customer experiences while driving efficiency through embedded AI and providing robust insights to amplify ROI, as illustrated in this overview:

For investors, Sprout highlighted its recurring SaaS model with 99% subscription revenue, product-led growth approach, and large addressable market as key investment considerations. The company’s leadership team, which includes executives with experience at major technology companies, remains focused on scaling the business toward its long-term goals while maintaining profitability.

Despite the recent stock price pressure, Sprout Social’s Q2 FY2025 presentation demonstrates the company’s continued execution on its strategic priorities, with solid financial results and a significant acquisition that expands its capabilities in the growing social media management market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.