Bank CEOs meet with Trump to discuss Fannie Mae and Freddie Mac - Bloomberg

SPS Commerce Inc (NASDAQ:SPSC) shared its Q1 2025 corporate presentation on April 24, showcasing the company’s continued strong performance and strategic positioning in the retail supply chain solutions market. The presentation highlighted SPS Commerce’s recent 19% revenue growth, the acquisition of Carbon6, and an expanded total addressable market of $11.1 billion.

Financial Performance Highlights

SPS Commerce reported impressive financial results, with 2024 revenue growth of 19% and an adjusted EBITDA margin of 29%. The company’s Q4 2024 earnings, released alongside the presentation, exceeded analyst expectations with EPS of $0.89 against a forecast of $0.87, and revenue of $170.9 million versus the anticipated $168.76 million.

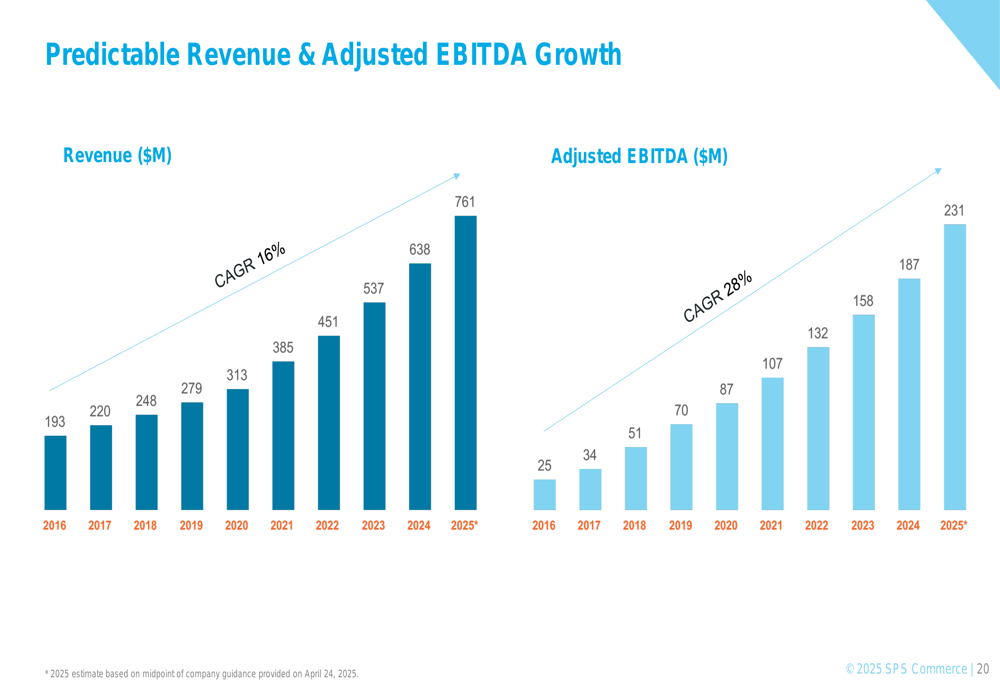

The presentation revealed a consistent growth trajectory, with revenue increasing from $193 million in 2016 to a projected $761 million in 2025, representing a 16% compound annual growth rate (CAGR).

As shown in the following chart of revenue and adjusted EBITDA growth:

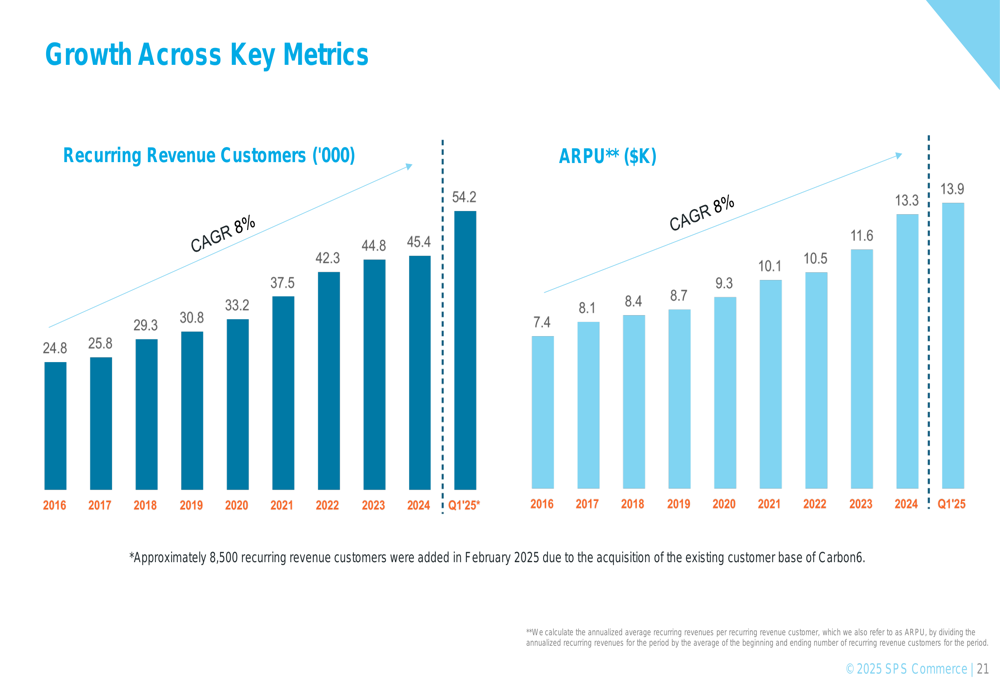

Similarly, the company has demonstrated steady growth in its customer base and average revenue per user (ARPU):

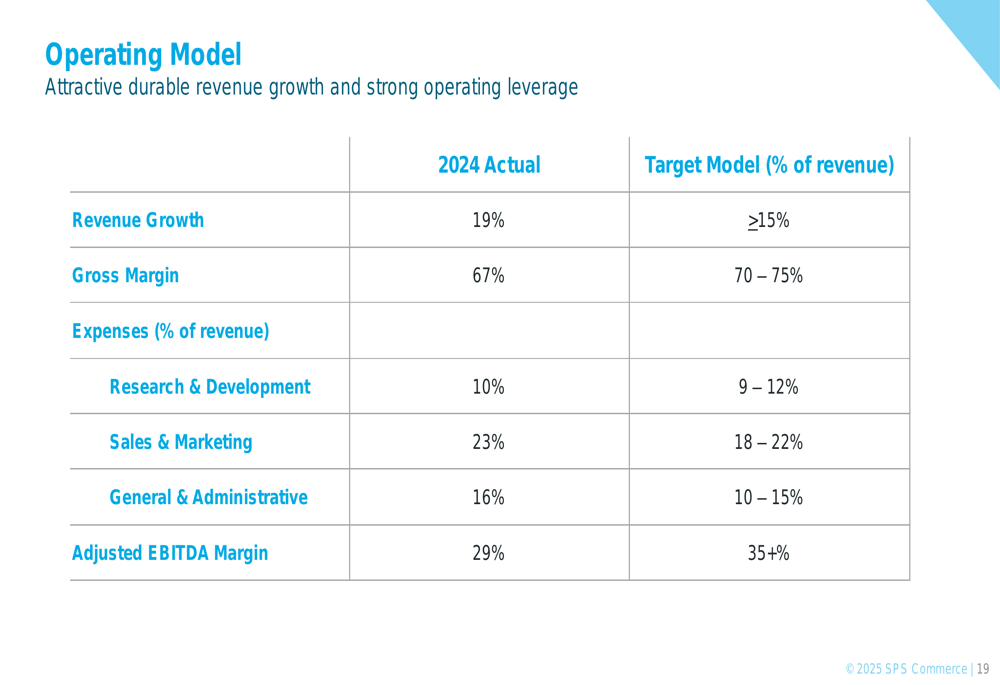

SPS Commerce’s operating model demonstrates both strong revenue growth and improving profitability metrics, with targets that suggest continued margin expansion:

Strategic Market Positioning

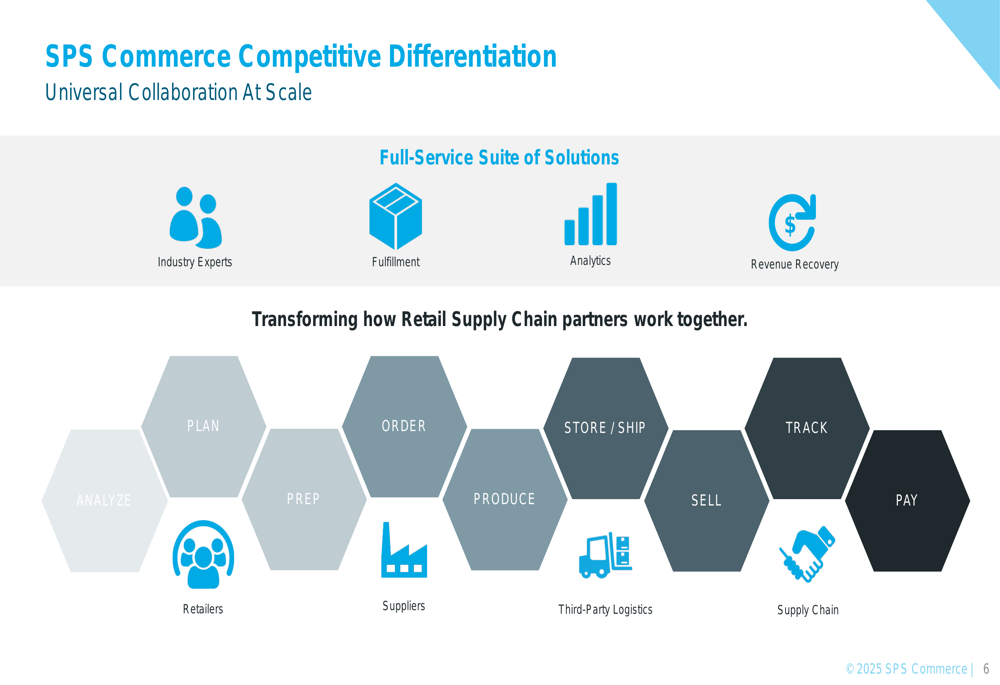

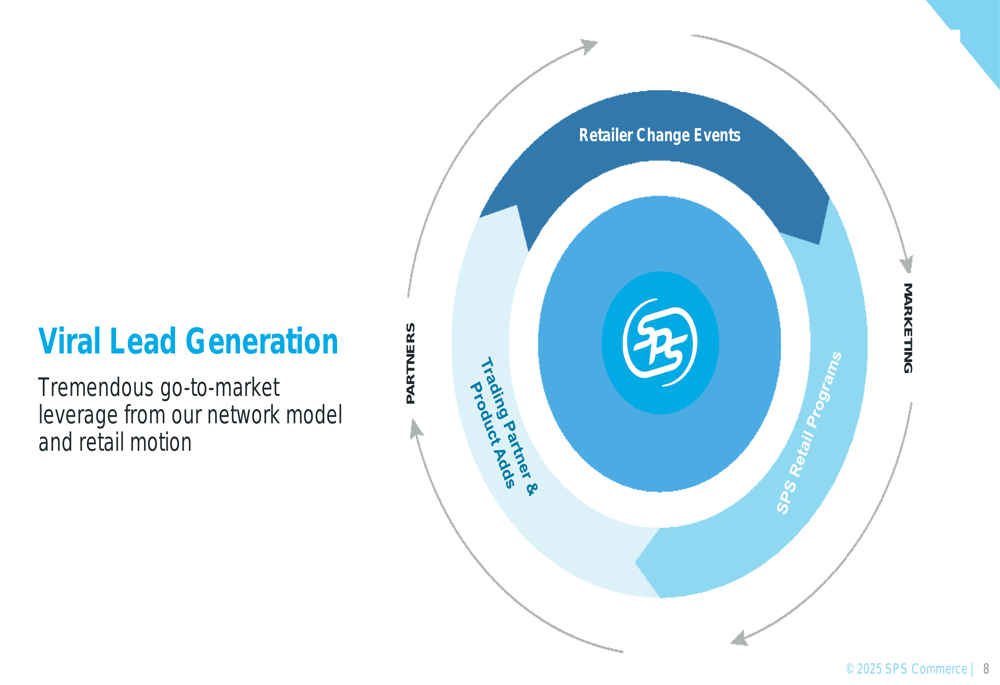

The presentation emphasized SPS Commerce’s unique competitive positioning as a provider of "Universal Collaboration At Scale" with a "Full-Service Suite of Solutions" for retail supply chain partners. The company’s network model creates a significant barrier to entry and enables viral lead generation.

The company’s competitive differentiation is illustrated in this comprehensive diagram:

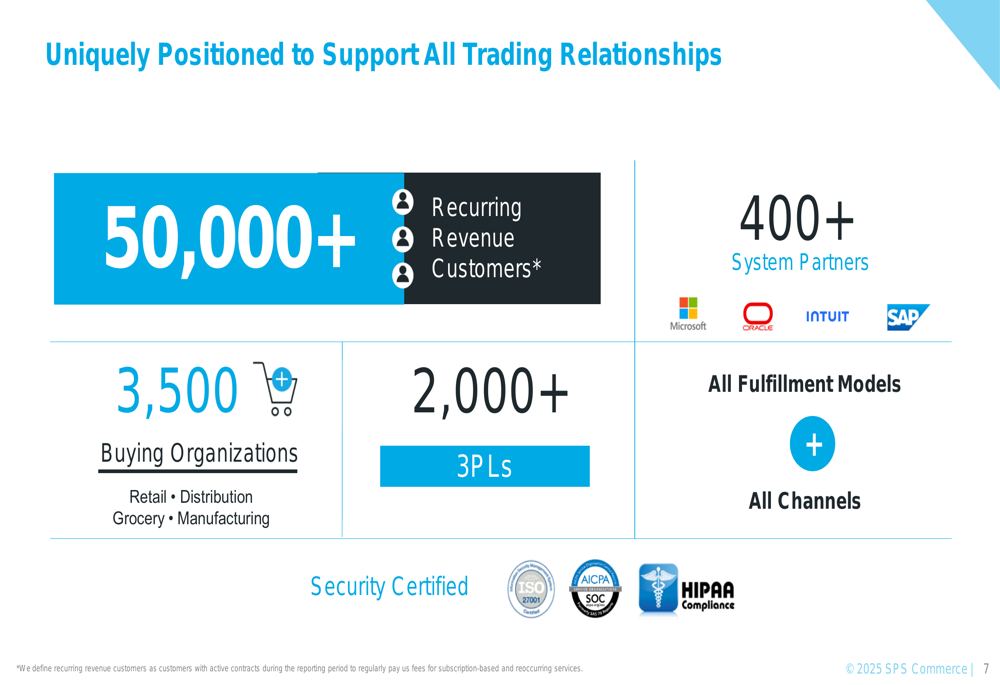

SPS Commerce highlighted its extensive reach across the retail ecosystem, serving over 50,000 recurring revenue customers, 3,500+ buying organizations, and 2,000+ third-party logistics providers:

A key competitive advantage is the company’s "viral lead generation" model, which creates a self-reinforcing growth cycle:

Expanding Market Opportunity (SO:FTCE11B)

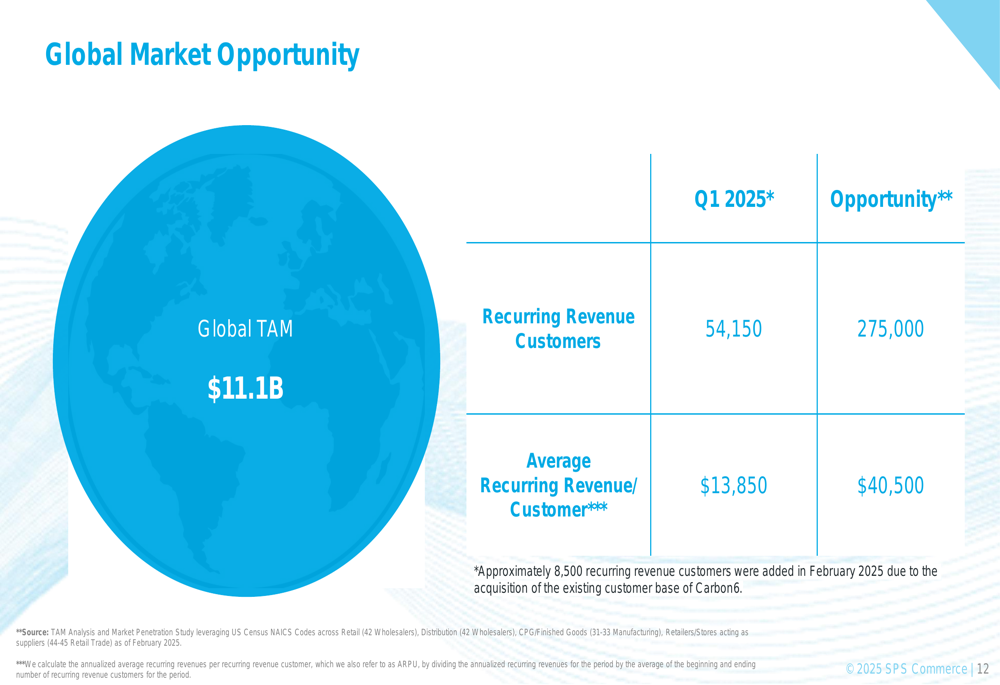

SPS Commerce quantified its global total addressable market (TAM) at $11.1 billion, with the U.S. representing $6.5 billion of that opportunity. As of Q1 2025, the company reported 54,150 recurring revenue customers, with an average recurring revenue per customer of $13,850.

The global market opportunity is visualized in this slide:

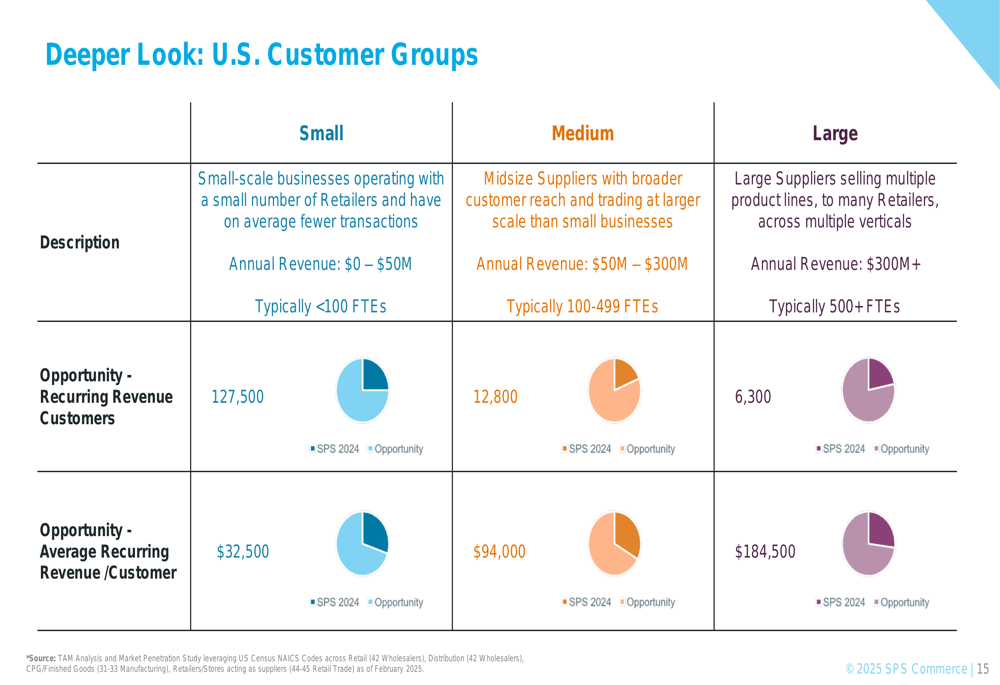

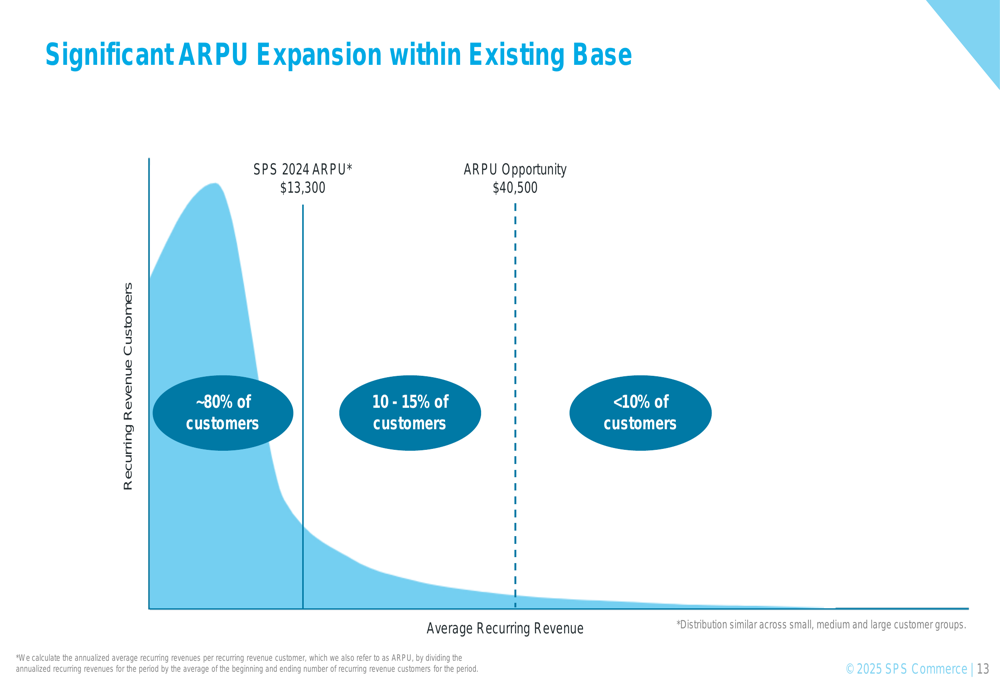

The company segments its customers into three groups based on annual revenue: Small (<$50M), Medium ($50M-$300M), and Large (>$300M). Each segment represents different growth opportunities and ARPU potential:

SPS Commerce sees significant ARPU expansion potential within its existing customer base, with approximately 80% of customers currently having an ARPU below the 2024 average of $13,300:

Growth Strategy and Case Studies

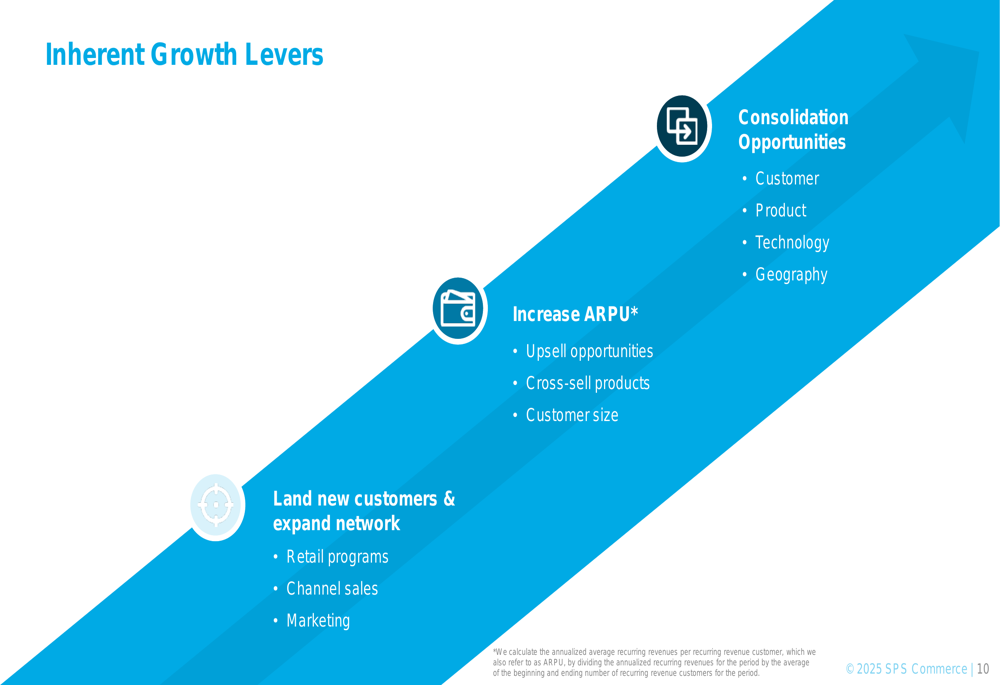

The presentation outlined several inherent growth levers, including new customer acquisition, ARPU expansion through upselling and cross-selling, and strategic consolidation opportunities:

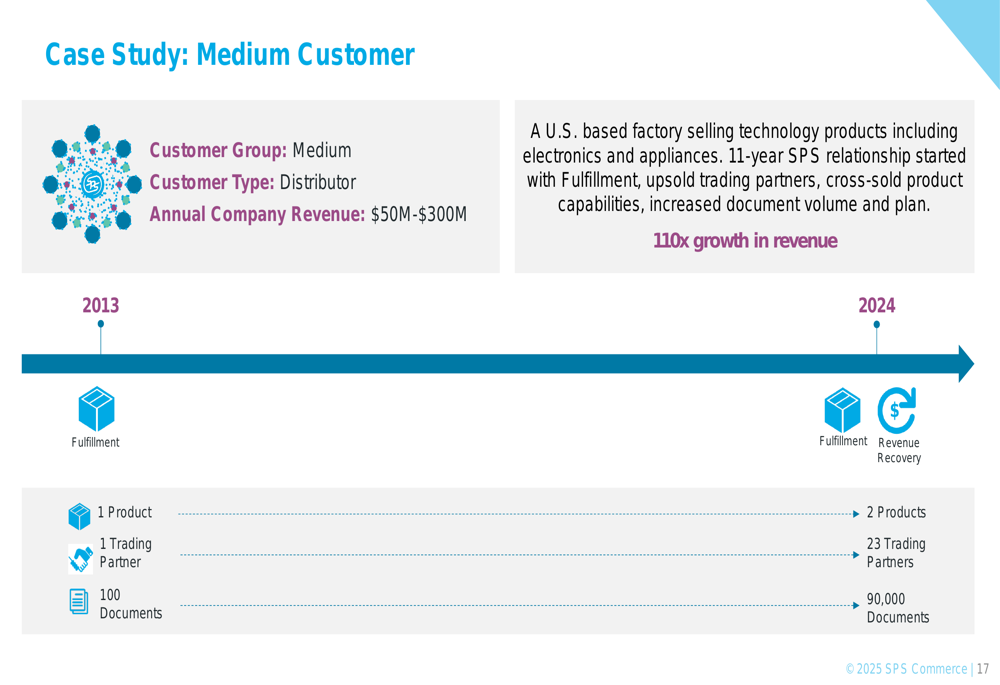

To illustrate its growth strategy, SPS Commerce shared case studies across different customer segments. These examples demonstrated the company’s ability to significantly expand relationships over time through additional products, trading partners, and document volumes.

The following case study of a medium-sized customer shows how SPS Commerce grew the relationship from a single product and trading partner to multiple products and 23 trading partners, resulting in 110x revenue growth over 11 years:

Carbon6 Acquisition and Future Outlook

A significant development highlighted in the presentation was the February 2025 acquisition of Carbon6, which added approximately 8,500 recurring revenue customers to SPS Commerce’s base. This acquisition aligns with the company’s strategy of expanding its product offerings and customer reach.

For 2025, SPS Commerce has provided revenue guidance of $758-$763 million, representing 19-20% growth, along with adjusted EBITDA projections of $227.5-$231 million. The company’s long-term target model aims for annual revenue growth of 15% or higher and adjusted EBITDA growth of 15-25%.

Despite the positive presentation and earnings beat, SPS Commerce’s stock showed mixed performance. According to the earnings report, the stock initially declined 2.35% in after-hours trading to $173 following the Q4 2024 results announcement. However, more recent data indicates the stock has recovered, with after-hours trading showing a 2.5% gain to $142.50.

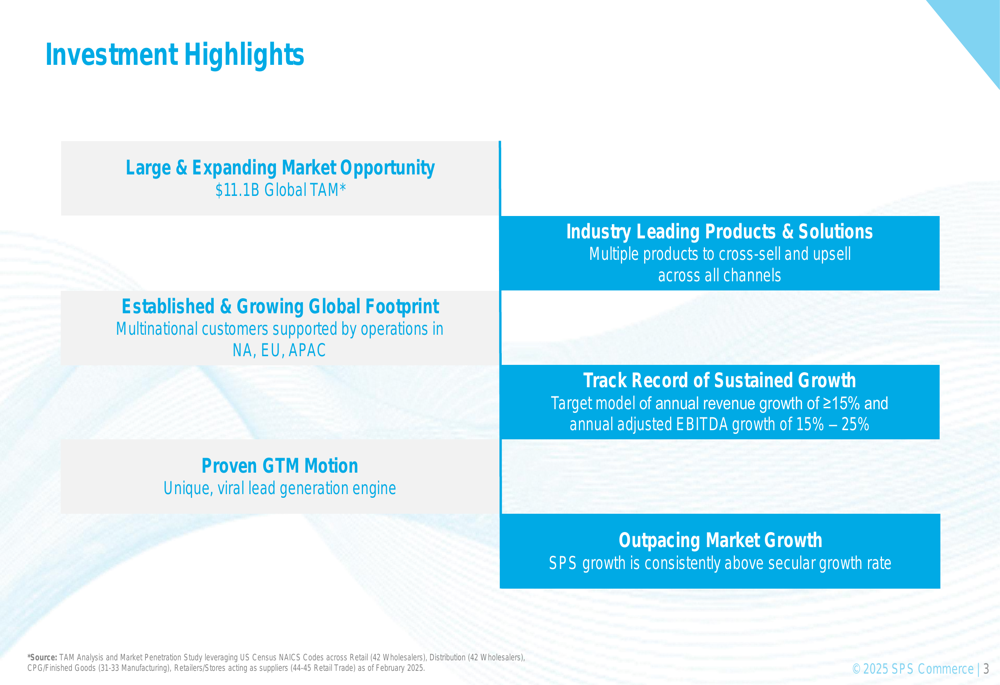

SPS Commerce’s investment highlights, which summarize the company’s value proposition, include its large and expanding market opportunity, industry-leading products and solutions, growing global footprint, and track record of sustained growth:

With its strong financial performance, expanding market opportunity, and strategic acquisition of Carbon6, SPS Commerce appears well-positioned to continue its growth trajectory in the retail supply chain solutions market throughout 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.