Bank CEOs meet with Trump to discuss Fannie Mae and Freddie Mac - Bloomberg

Introduction & Market Context

SPS Commerce (NASDAQ:SPSC) presented its latest investor deck on July 30, 2025, highlighting the company’s strong growth trajectory and expanding market opportunity in supply chain management solutions. The presentation comes after SPS reported its Q1 2025 earnings with revenue of $181.5 million, representing a 21% year-over-year increase and marking the company’s 97th consecutive quarter of revenue growth.

The company’s stock has experienced volatility in recent months, trading at $140.10 as of the presentation date, significantly below its 52-week high of $218.61 but above its 52-week low of $120.09. Despite this volatility, SPS Commerce continues to demonstrate consistent revenue growth and margin expansion.

Growth Strategy & Market Opportunity (SO:FTCE11B)

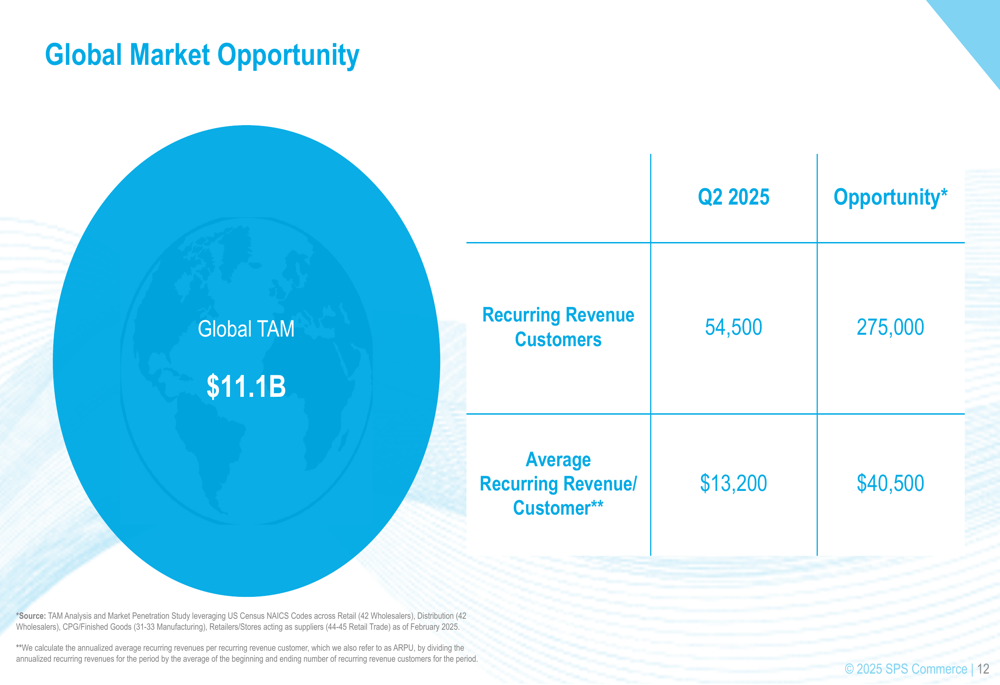

SPS Commerce identified a substantial addressable market opportunity, estimating its global total addressable market (TAM) at $11.1 billion, with the U.S. portion representing $6.5 billion. The company currently serves 54,500 recurring revenue customers as of Q2 2025, with significant room for expansion toward an estimated opportunity of 275,000 customers.

As shown in the following chart of the company’s market opportunity:

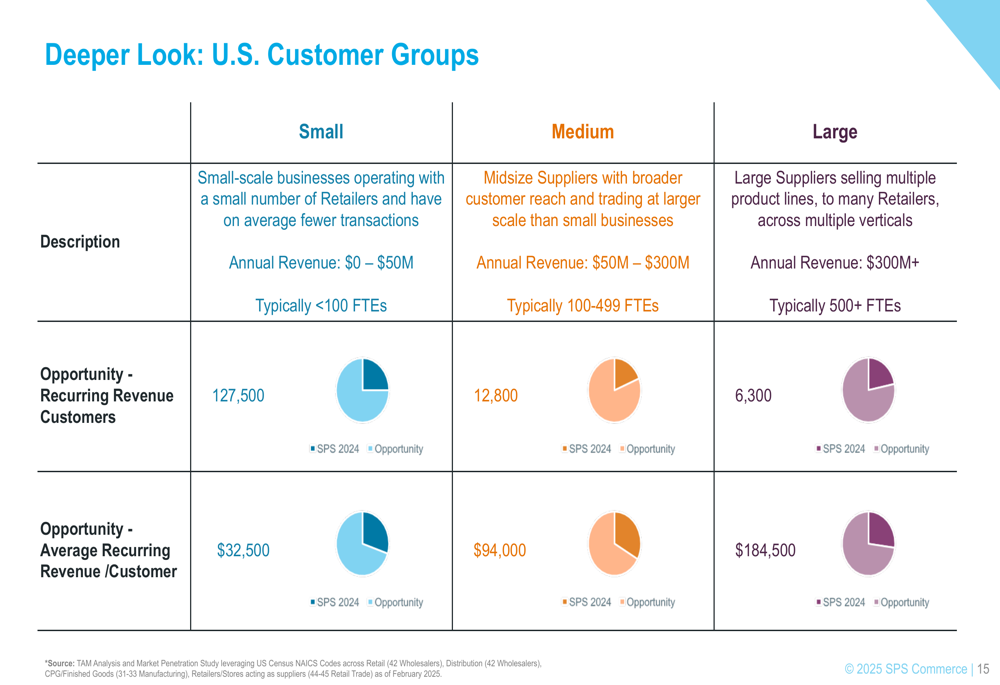

The company segments its U.S. customer base into three groups based on annual revenue: Small (<$50M), Medium ($50M-$300M), and Large (>$300M). Each segment presents different growth opportunities, with the small segment representing the largest volume of potential customers while the large segment offers the highest average revenue per customer.

The detailed breakdown of these customer segments illustrates varying needs and revenue potential:

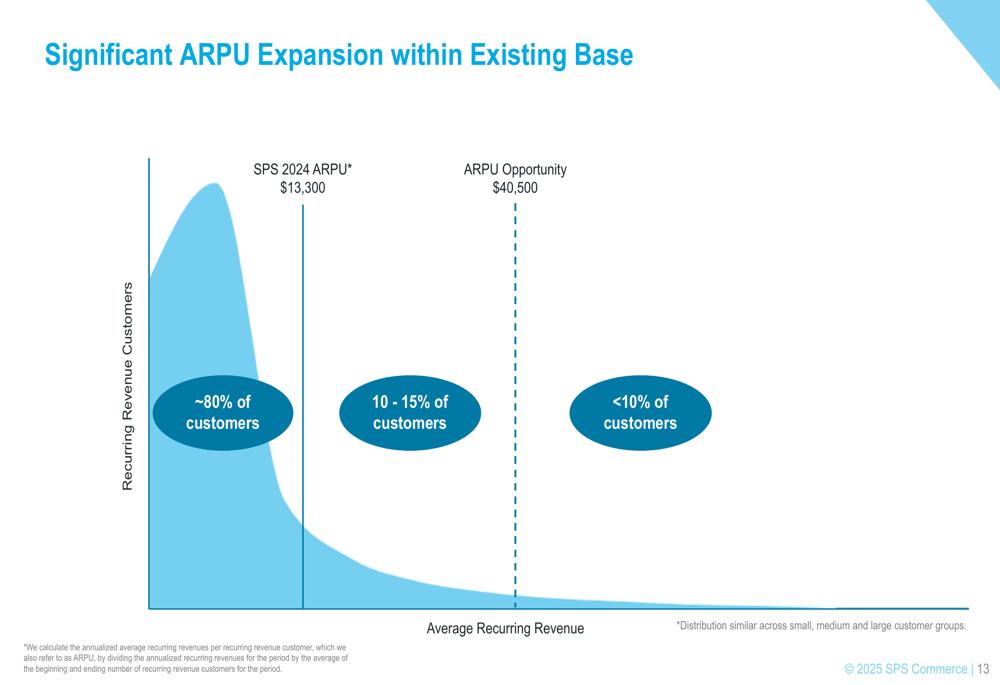

A key growth metric for SPS Commerce is its Average Revenue Per User (ARPU), which stood at $13,200 in Q2 2025 but has significant expansion potential to reach $40,500. The company’s presentation highlighted that approximately 80% of customers represent the largest opportunity for ARPU growth.

As illustrated in this ARPU expansion chart:

Financial Performance & Outlook

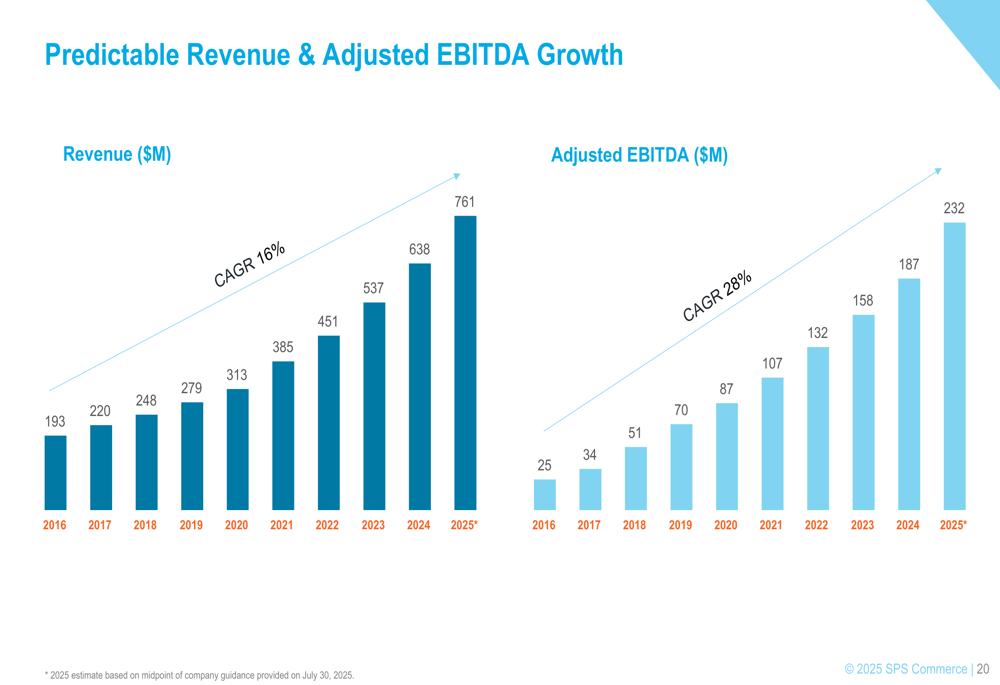

SPS Commerce has demonstrated consistent financial growth, with revenue increasing from $193 million in 2016 to a projected $761 million in 2025, representing a 16% compound annual growth rate (CAGR). Similarly, Adjusted EBITDA has grown from $25 million in 2016 to a projected $232 million in 2025, reflecting a 28% CAGR.

The following chart illustrates this predictable growth trajectory:

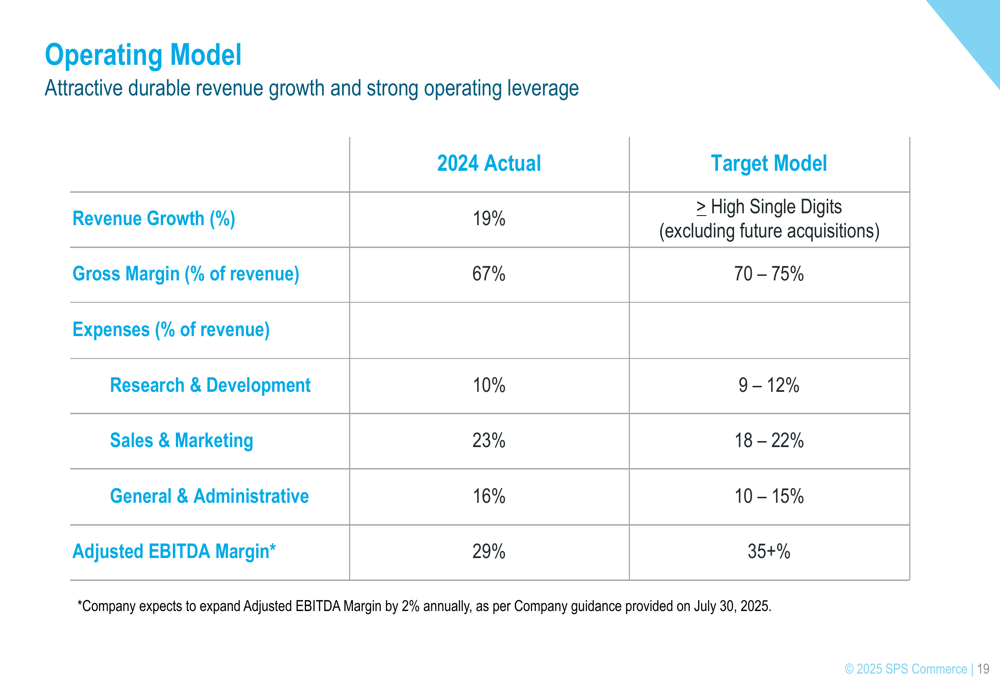

The company’s operating model shows strong leverage, with 2024 actual revenue growth of 19% and an Adjusted EBITDA margin of 29%. SPS Commerce has set target models that include high single-digit revenue growth and an Adjusted EBITDA margin of 35%+, with expectations to expand this margin by approximately 2% annually.

The company’s operating model is detailed in the following slide:

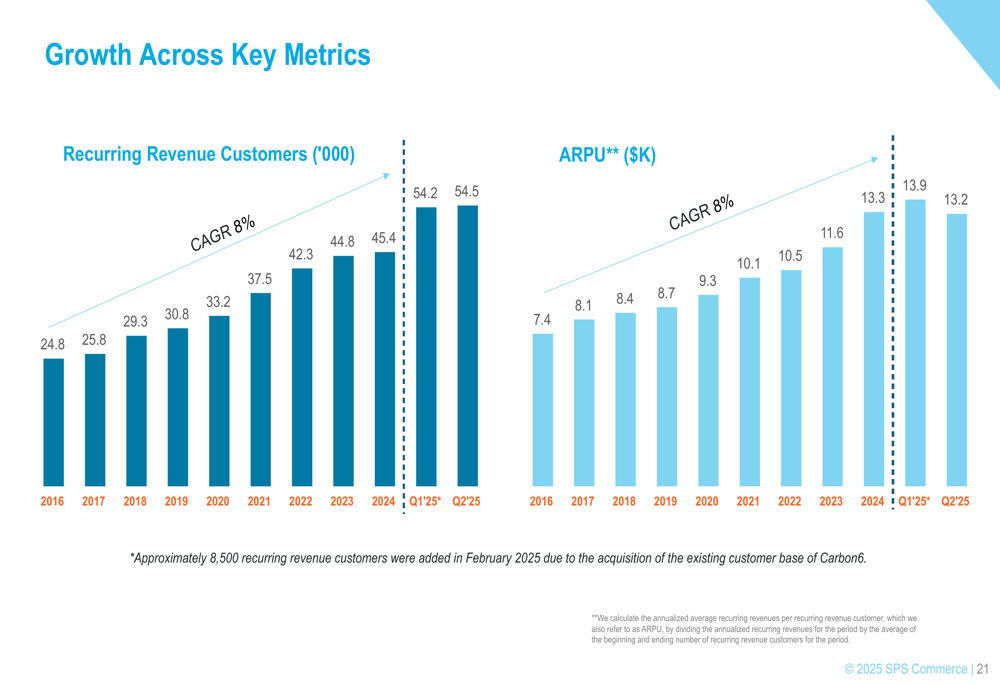

SPS Commerce has also shown consistent growth in its customer base and ARPU metrics. The number of recurring revenue customers increased from 24,800 in 2016 to 54,500 in Q2 2025, representing an 8% CAGR. This growth was bolstered by the acquisition of Carbon6, which added approximately 8,500 customers. Similarly, ARPU has grown from $7,400 in 2016 to $13,200 in Q2 2025, also representing an 8% CAGR.

These key growth metrics are visualized in the following chart:

Competitive Positioning

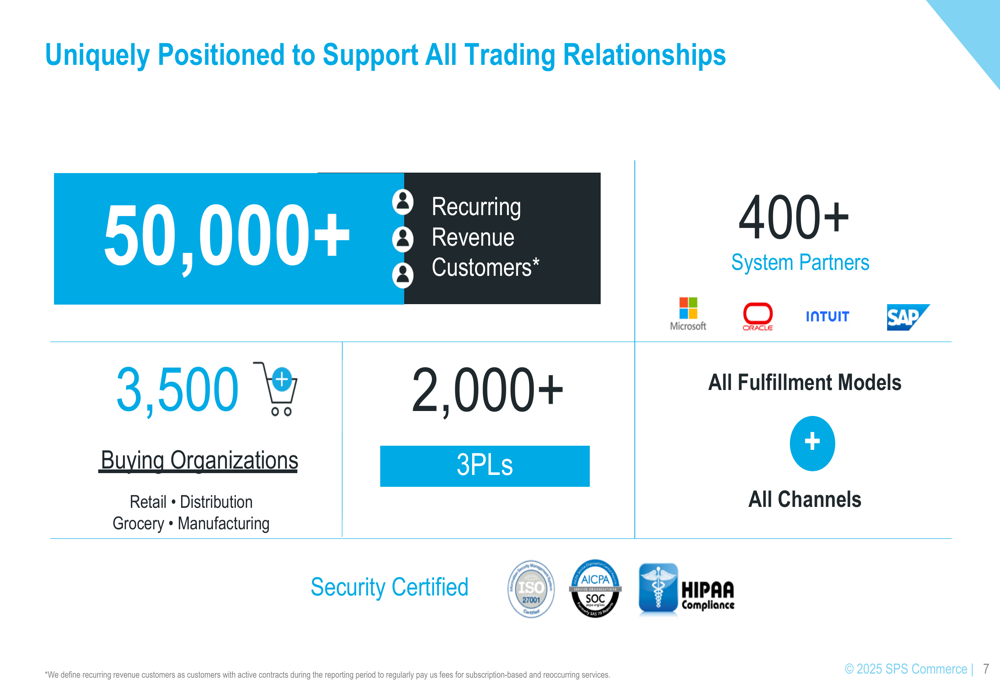

SPS Commerce emphasized its unique competitive positioning through what it describes as "Universal Collaboration At Scale." The company’s network includes over 50,000 recurring revenue customers, 3,500+ buying organizations, and 2,000+ third-party logistics providers (3PLs). This extensive network creates what the company calls a "viral lead generation" model, where retailer change events drive new customer acquisition.

The company’s extensive network is illustrated in this slide:

The presentation highlighted three primary growth levers: acquiring new customers and expanding the network, increasing ARPU through upsell and cross-sell opportunities, and pursuing consolidation opportunities across customers, products, technology, and geography.

SPS Commerce’s competitive advantage is rooted in its network model, which creates a "growth multiplier" effect as more participants join the ecosystem. This network effect is particularly evident in case studies presented for small, medium, and large customers, which demonstrated revenue growth of 6x, 110x, and 15x respectively over the course of their relationships with SPS Commerce.

Forward-Looking Statements

Looking ahead, SPS Commerce provided guidance for Q2 2025 with expected revenue between $184.5 million and $186.2 million, representing 20-21% year-over-year growth. For the full year 2025, the company projects revenue of $758.5 million to $763 million, with Adjusted EBITDA expected to range from $229.4 million to $232.9 million.

The company’s long-term strategy focuses on expanding its global footprint, which currently includes operations in North America, Europe, and Asia-Pacific. SPS Commerce also emphasized its commitment to corporate responsibility, highlighting initiatives in environmental stewardship, employee belonging, community investment, and governance.

Despite macroeconomic uncertainties affecting retail and trade dynamics, SPS Commerce remains confident in its growth trajectory, supported by its established network, recurring revenue model, and opportunities for both customer acquisition and ARPU expansion. The company’s consistent performance over 97 consecutive quarters of revenue growth demonstrates resilience and positions it well to capitalize on the substantial market opportunity in supply chain management solutions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.