Gevo shares jump as Q3 results top estimates, posts positive EBITDA

Introduction & Market Context

SSR Mining Inc. (NASDAQ:SSRM) reported substantial financial improvements in its second quarter 2025 results, with revenue more than doubling year-over-year despite ongoing challenges at its suspended Çöpler operation in Türkiye. The diversified precious metals producer, now positioned as the third-largest gold producer in the United States following its CC&V acquisition, delivered strong cash flow generation while advancing several growth initiatives.

The company’s performance comes amid relatively stable gold prices, with production increases primarily driven by the addition of the CC&V mine and operational improvements at existing assets. However, SSR Mining continues to face headwinds from the Çöpler incident, with remediation costs now exceeding previous estimates.

Quarterly Performance Highlights

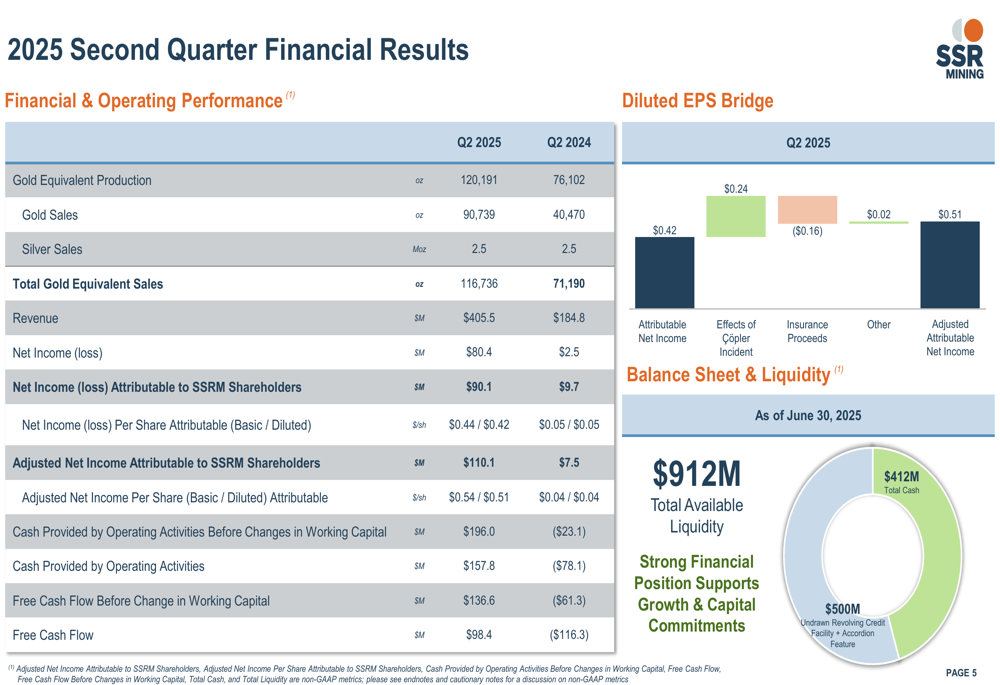

SSR Mining reported gold equivalent production of 120,191 ounces for Q2 2025, representing a significant 58% increase from 76,102 ounces in Q2 2024. This production growth, coupled with favorable metal prices, drove revenue to $405.5 million, a 119% increase from $184.8 million in the prior-year period.

The company’s profitability metrics showed dramatic improvement, with net income attributable to shareholders reaching $90.1 million ($0.44 per basic share, $0.42 per diluted share), compared to just $9.7 million ($0.05 per share) in Q2 2024. Adjusted net income, which excludes certain one-time items, was $110.1 million ($0.54 per basic share, $0.51 per diluted share).

As shown in the company’s financial results summary:

Cash flow performance was particularly strong, with operating cash flow of $157.8 million compared to negative $78.1 million in Q2 2024. Free cash flow reached $98.4 million, a substantial improvement from negative $116.3 million in the prior-year quarter. This cash generation strengthened the company’s balance sheet, with cash and cash equivalents increasing to $412.1 million as of June 30, 2025, providing total liquidity of $912.1 million including an undrawn revolving credit facility.

Çöpler Incident Update

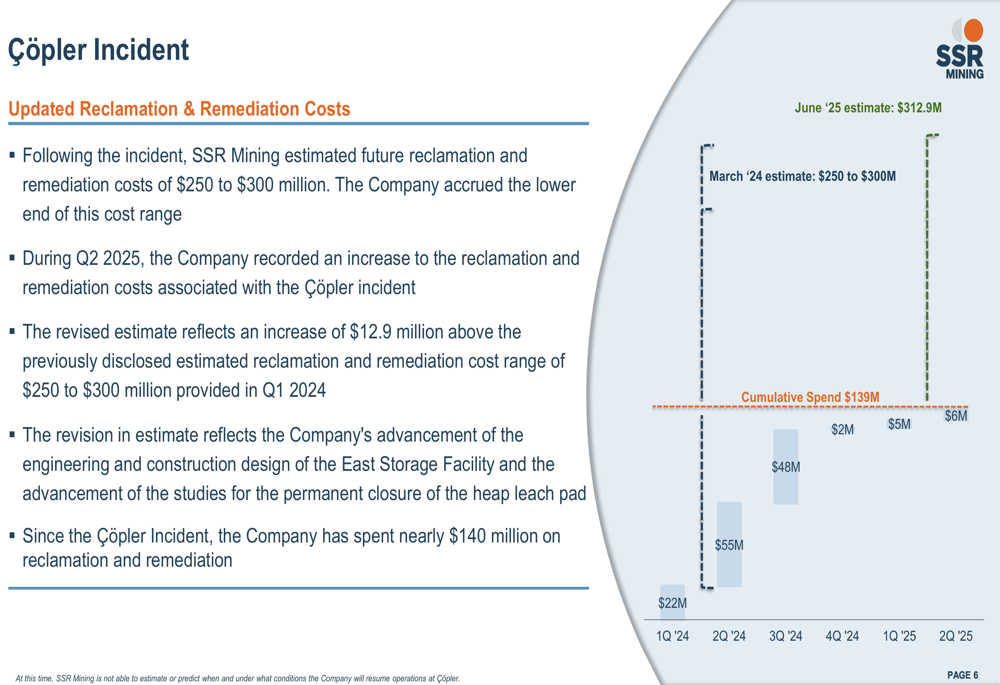

SSR Mining provided an updated assessment of reclamation and remediation costs related to the Çöpler incident. The company now estimates total costs at $312.9 million, an increase of $12.9 million above the previously disclosed range of $250-300 million announced in March 2024. Through Q2 2025, the company has spent approximately $139 million on remediation efforts.

The quarterly breakdown of remediation spending shows significant expenditures in Q2-Q3 2024, with reduced spending in subsequent quarters:

Notably, SSR Mining stated it "is not able to estimate or predict when and under what conditions the Company will resume operations at Çöpler," indicating continued uncertainty around this significant asset. During Q2 2025, the company incurred $36.7 million in care and maintenance costs at Çöpler, in addition to $6.1 million in remediation spending.

Asset Performance

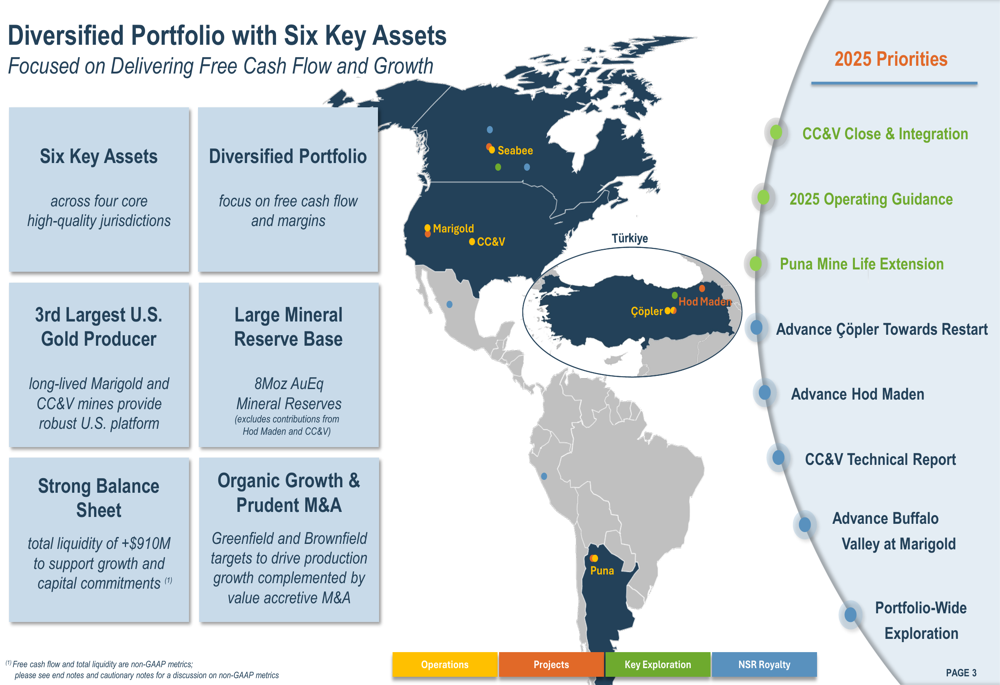

SSR Mining’s portfolio now consists of six key assets across four jurisdictions, with current production from Marigold, CC&V, Seabee, and Puna, while Çöpler remains suspended and Hod Maden is under development.

The company’s diversified operational footprint is illustrated in this overview:

Marigold, the company’s large-scale open-pit operation in Nevada, produced 35,906 ounces of gold in Q2 at a cost of sales of $1,584 per ounce and all-in sustaining costs (AISC) of $1,977 per ounce. Management noted that H2 2025 production is expected to be approximately 55-60% weighted to Q4.

CC&V, acquired in early 2025, contributed 44,062 ounces of gold at a cost of sales of $1,116 per ounce and AISC of $1,339 per ounce. Since acquisition, CC&V has generated nearly $85 million in mine site free cash flow, validating the company’s acquisition strategy.

Seabee operations in Saskatchewan were impacted by temporary power interruptions caused by forest fires, resulting in reduced production of 10,998 ounces at elevated costs. The company now expects Seabee’s full-year production to be at the low end of its previously issued guidance range of 70,000-80,000 ounces.

Puna, the company’s silver-focused operation in Argentina, produced 2.8 million ounces of silver at a cost of sales of $15.03 per ounce and AISC of $12.57 per ounce. The company is advancing mine life extension opportunities at Puna, with initial plans for nearly three additional years of production.

Strategic Initiatives

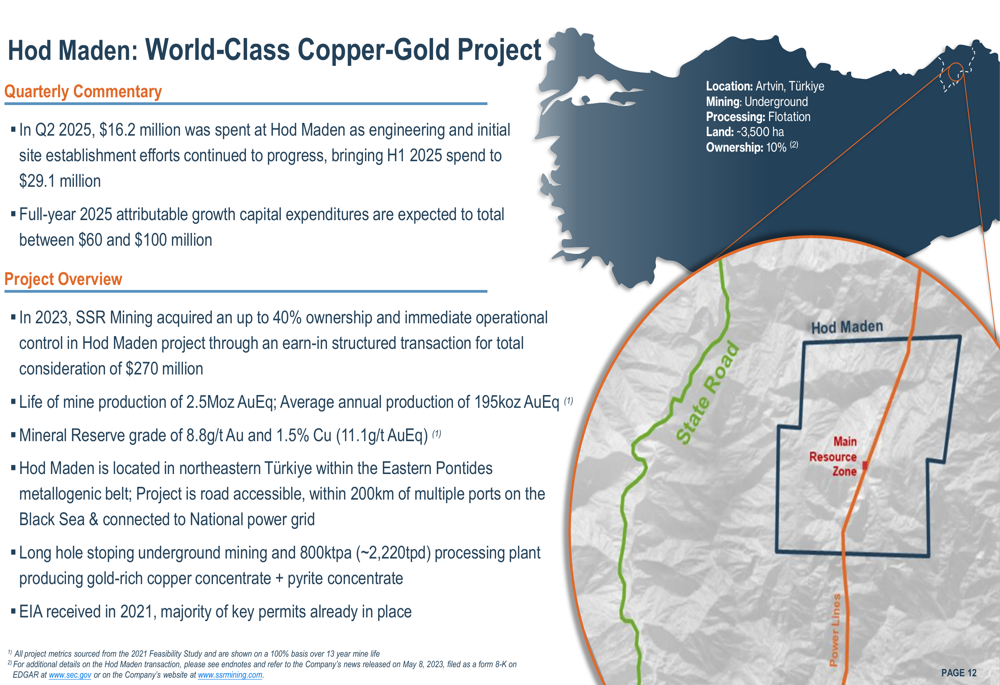

SSR Mining continues to advance several key strategic initiatives aimed at driving future growth. The Hod Maden project in Türkiye, described as a "world-class copper-gold project," saw capital expenditures of $16.2 million in Q2 2025 as engineering and initial site establishment efforts progressed. This brought first-half 2025 spending to $29.1 million, with full-year attributable growth capital expenditures expected to total between $60-100 million.

The Hod Maden project represents a significant growth opportunity for SSR Mining:

At Puna, the company outlined initial mine life extension expectations, with projected 2026 silver production of 7-8 million ounces. Exploration and engineering work continues to build on this extended mine life, complemented by ongoing evaluation of Cortaderas as a longer-term growth pathway.

The company is also advancing exploration and engineering studies at Buffalo Valley (Marigold) and has commenced engineering studies at New Millennium. Additionally, a technical report for CC&V based on existing mineral reserves remains on track for publication in 2025.

Forward-Looking Statements

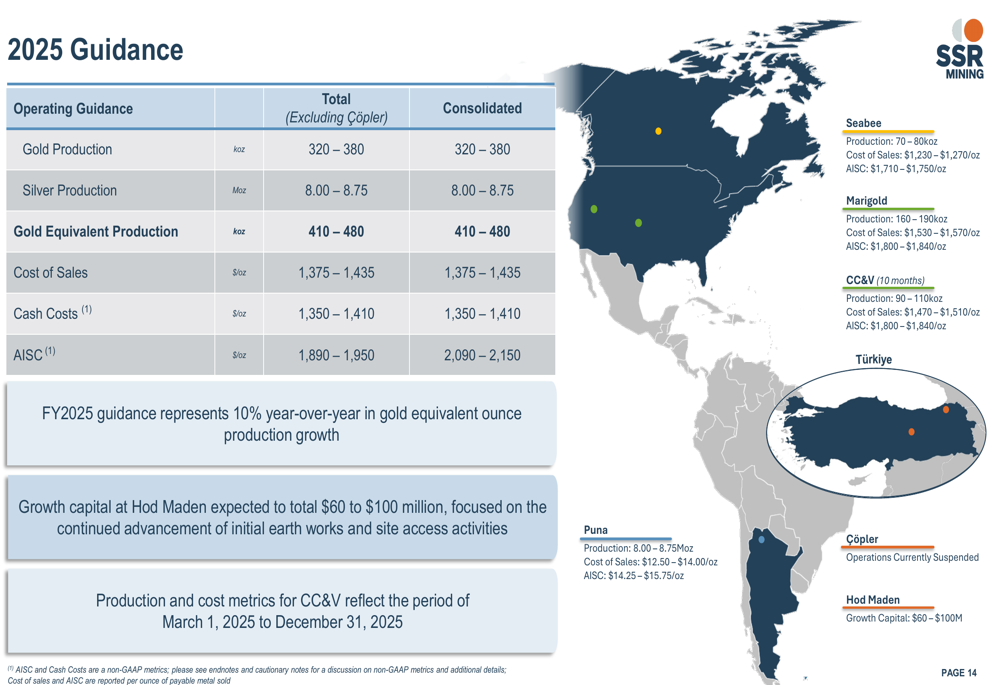

SSR Mining maintained its 2025 production guidance of 410,000-480,000 gold equivalent ounces, representing a 10% year-over-year increase in production. The guidance breakdown by asset shows the company’s diversified production base:

For 2025, the company expects consolidated cost of sales between $1,375-1,435 per ounce and AISC between $1,890-1,950 per ounce. Growth capital at Hod Maden is projected at $60-100 million for the year, focused on continued advancement of initial earthworks and site access activities.

The company’s 2025 priorities include CC&V integration, Puna mine life extension, advancing Çöpler towards restart, progressing Hod Maden development, publishing a CC&V technical report, advancing Buffalo Valley at Marigold, and portfolio-wide exploration.

Conclusion

SSR Mining delivered strong financial results in Q2 2025, with significant improvements in revenue, earnings, and cash flow compared to the prior-year period. The addition of CC&V has strengthened the company’s U.S. production base, while ongoing remediation at Çöpler remains a challenge with increased cost estimates and uncertain restart timing.

The company’s robust liquidity position of $912.1 million provides financial flexibility to advance growth initiatives, particularly the high-grade Hod Maden project. With production guidance maintained for 2025 and several mine life extension and optimization opportunities in the pipeline, SSR Mining appears well-positioned to continue its operational recovery despite the ongoing challenges at Çöpler.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.