US stock futures dip as Trump’s firing of Cook sparks Fed independence fears

Introduction & Market Context

Standex International Corporation (NYSE:SXI) reported its third-quarter fiscal 2025 results on May 2, 2025, highlighting strong revenue growth driven by recent acquisitions while achieving record profit margins. The company’s stock, which has declined from its 52-week high of $212.66 to $144.85, showed signs of recovery with a 2.43% gain on the day of the earnings release.

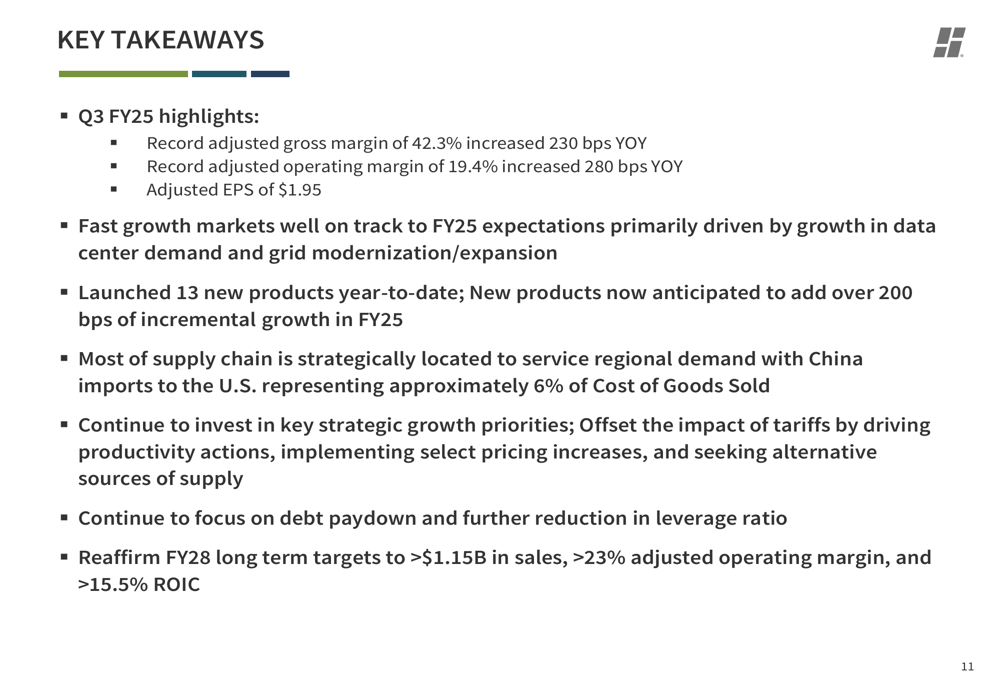

The industrial manufacturer reported that its "in region – for region" business model has limited exposure to tariff and trade disruptions, with over 85% of products manufactured and sold within the same region. Notably, imports from China represent only about 6% of the company’s cost of goods sold, positioning Standex to weather potential trade tensions.

Quarterly Performance Highlights

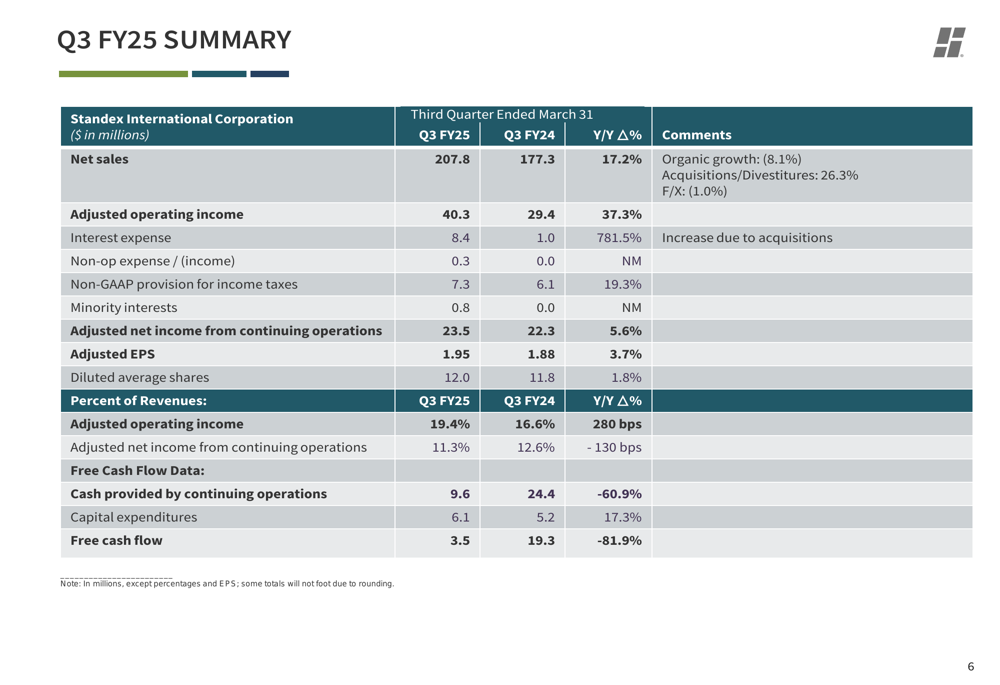

Standex reported Q3 FY25 net sales of $207.8 million, a 17.2% increase year-over-year, primarily driven by contributions from recent acquisitions. Despite this top-line growth, the company faced organic revenue declines in several segments.

As shown in the following comprehensive financial summary:

The company achieved record adjusted operating income of $40.3 million, up 37.3% year-over-year, with adjusted operating margin expanding to 19.4%, an improvement of 280 basis points. Adjusted earnings per share reached $1.95, representing a modest 3.7% increase compared to the prior year, as higher interest expenses of $8.4 million (up 781.5% year-over-year) weighed on bottom-line growth.

Free cash flow declined significantly to $3.5 million, down 81.9% from the previous year, reflecting higher capital expenditures and lower cash from operations.

Segment Performance Analysis

The Electronics segment emerged as the standout performer, with revenue increasing 38.4% to $111.3 million and adjusted operating income surging 85.4% to $33.2 million. This segment benefited substantially from the Amran/Narayan Group acquisition, which contributed over $33 million in sales with a book-to-bill ratio of 1.04.

The Engineering Technologies segment also showed strong growth with revenue up 36.2% to $27.4 million, primarily driven by the recent McStarlite acquisition. Adjusted operating income for this segment increased 44.3% year-over-year.

However, other segments faced challenges. The Engraving segment saw revenue decline 15.7% to $30.6 million, with adjusted operating income falling 48.8% due to continued softness in North America and Europe. The Specialty Solutions segment experienced a 13.9% revenue decline to $20.2 million, reflecting general market softness.

The Scientific segment reported 8.1% revenue growth to $18.3 million, benefiting from an acquisition, though adjusted operating income decreased 19.7% year-over-year.

Acquisition Strategy

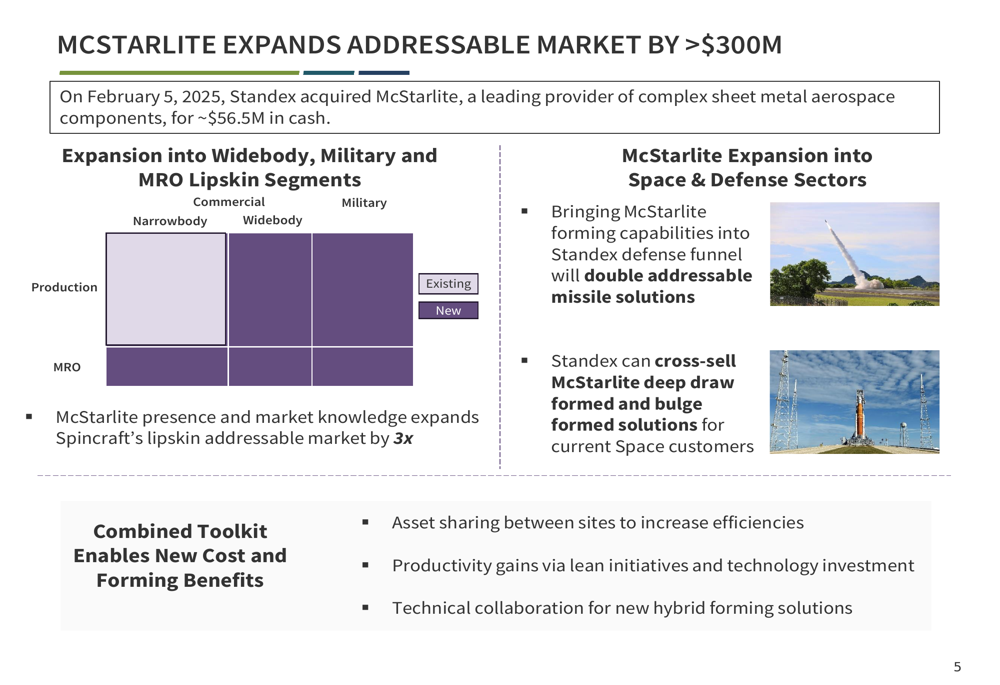

A central element of Standex’s growth strategy has been its recent acquisitions. The company highlighted the benefits of its February 2025 acquisition of McStarlite for approximately $56.5 million in cash:

The McStarlite acquisition expands Standex’s addressable market by over $300 million, particularly in the widebody, military, and MRO lipskin segments. The company expects to achieve productivity gains through lean initiatives, technology investments, and technical collaboration between sites.

Similarly, the Amran/Narayan Group acquisition has significantly strengthened the Electronics segment, contributing to the record margins achieved in Q3 FY25.

Financial Position and Outlook

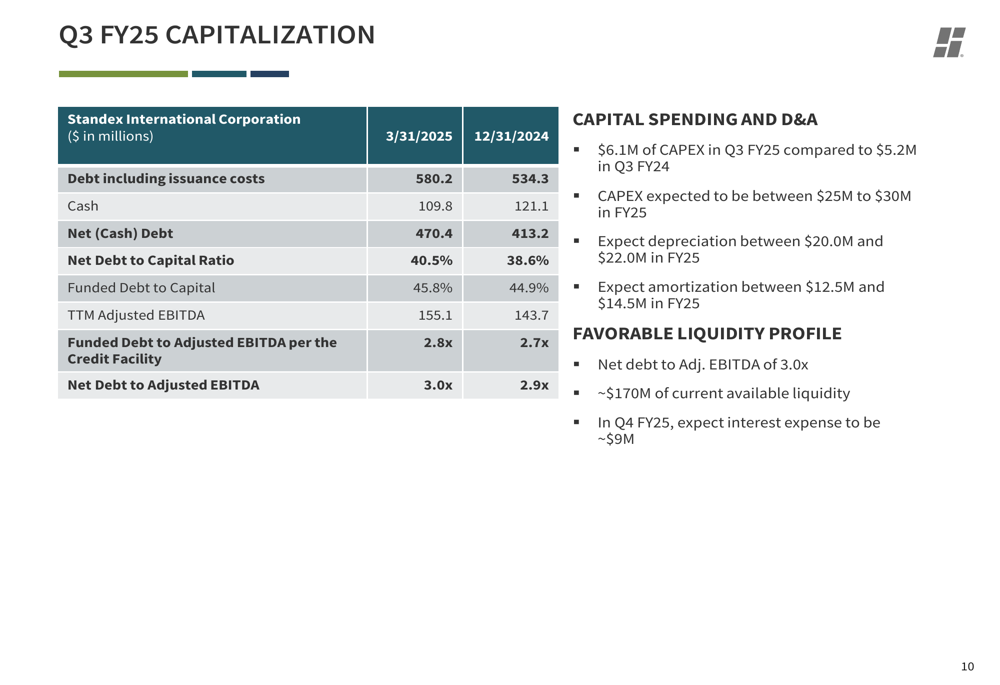

Standex’s balance sheet reflects its acquisition-focused strategy, with total debt increasing to $580.2 million as of March 31, 2025, compared to $534.3 million at the end of December 2024. The company’s net debt to adjusted EBITDA ratio rose to 3.0x from 2.9x in the previous quarter:

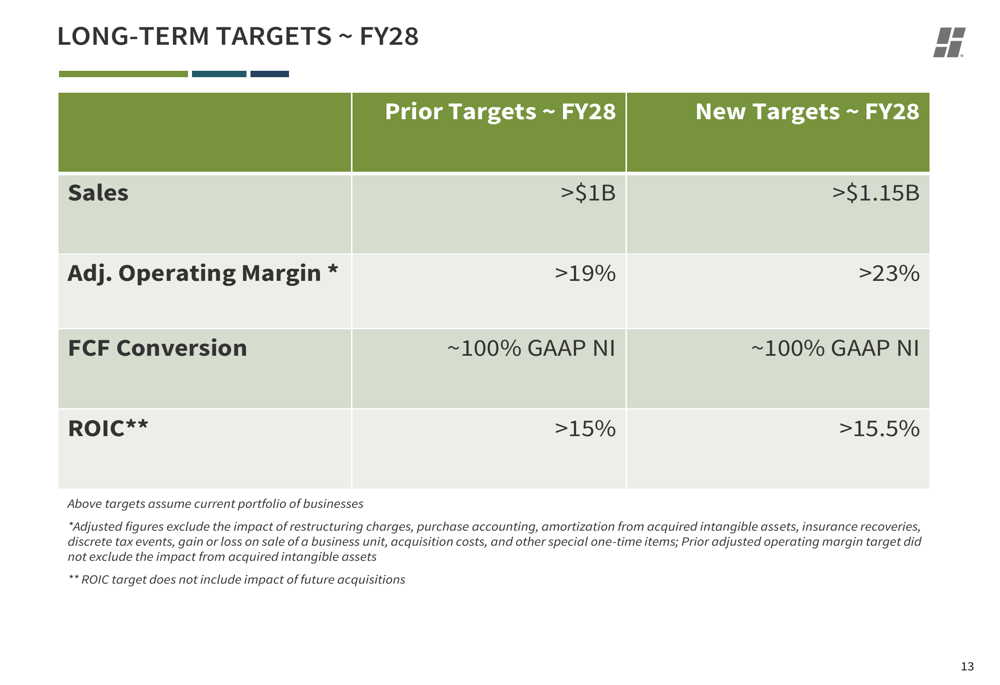

Looking ahead, Standex expects Q4 FY25 to deliver slightly to moderately higher revenue and adjusted operating margin, driven by recent acquisitions, higher sales into fast-growth markets, and pricing initiatives. The company reaffirmed its long-term FY28 targets:

New product development remains a key focus, with sales from new products expected to contribute over 200 basis points of incremental growth in FY25. The company reported that fast-growth markets now represent 29% of total sales, up from previous quarters.

Management indicated that debt reduction would be a priority going forward, aiming to lower the leverage ratio in coming quarters. The company’s strategy continues to focus on high-margin, high-growth opportunities while navigating market challenges in segments like Engraving and Specialty Solutions.

Despite mixed organic performance across segments, Standex’s acquisition strategy appears to be yielding positive results in terms of margin expansion and revenue growth, though investors will likely monitor the company’s ability to manage its increased debt load while delivering on its ambitious long-term targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.