AI underweights weigh on large-cap funds performance says Goldman

Stem Inc. (NYSE:STEM) released its second quarter 2025 financial results on August 7, showing continued revenue growth and a significant debt reduction through a strategic exchange. The clean energy software provider’s stock jumped 6.87% to $12.45 following the announcement, building on momentum from its positive Q1 results.

Quarterly Performance Highlights

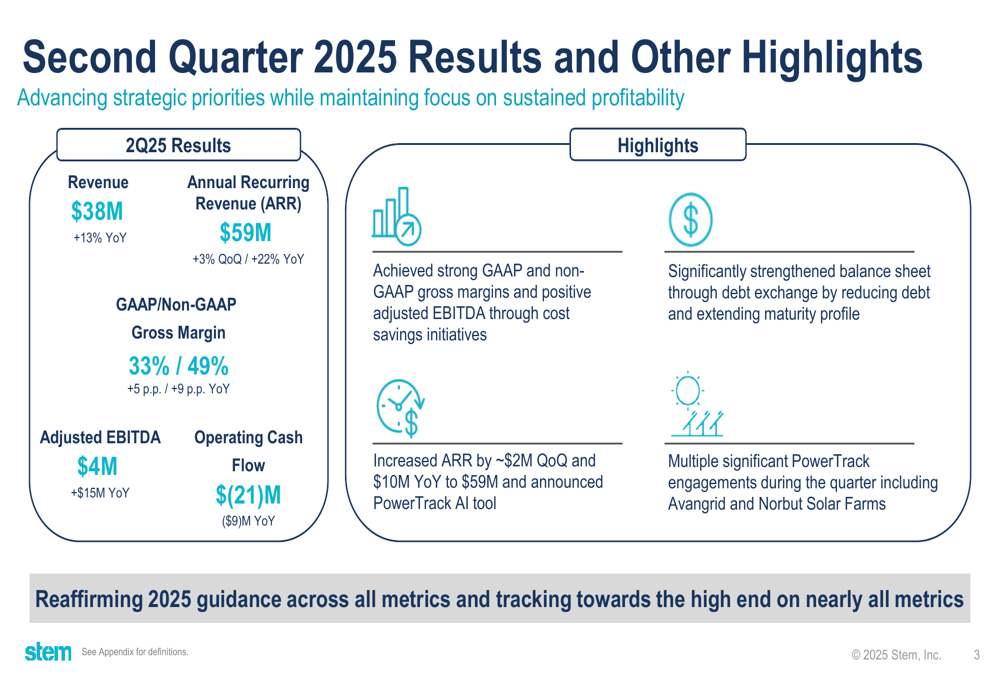

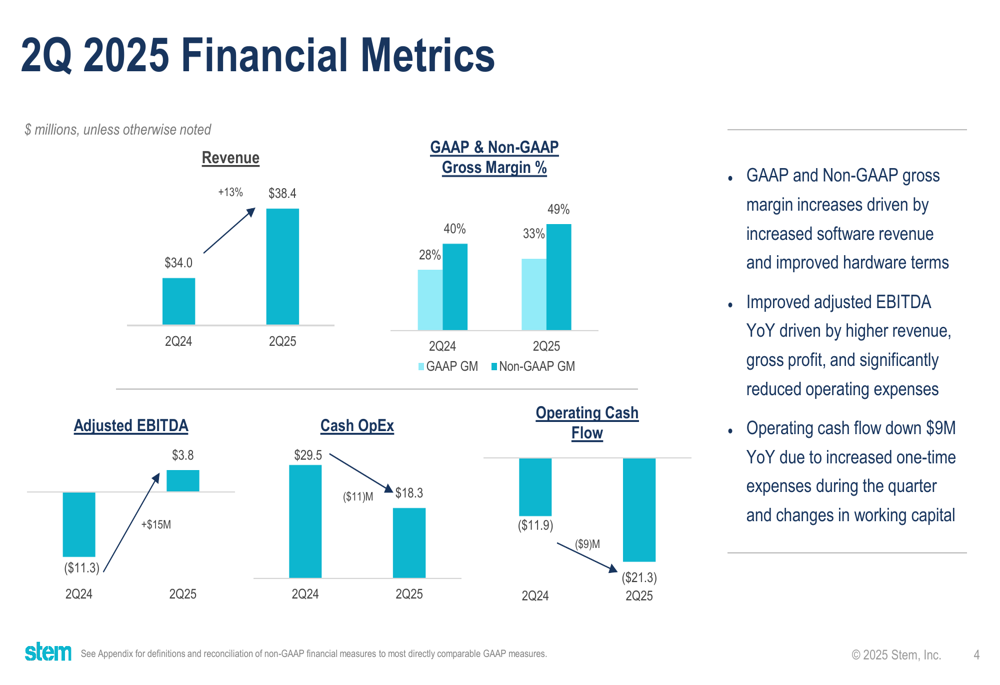

Stem reported Q2 2025 revenue of $38.4 million, representing a 13% year-over-year increase from $34 million in the same period last year. The company achieved positive adjusted EBITDA of $4 million, a $15 million improvement compared to the $(11) million reported in Q2 2024.

Annual Recurring Revenue (ARR) reached $58.5 million, growing 3% quarter-over-quarter and 22% year-over-year, driven by new site activations. Both GAAP and non-GAAP gross margins showed substantial improvement, reaching 33% and 49% respectively, representing year-over-year increases of 5 and 9 percentage points.

As shown in the following quarterly results summary:

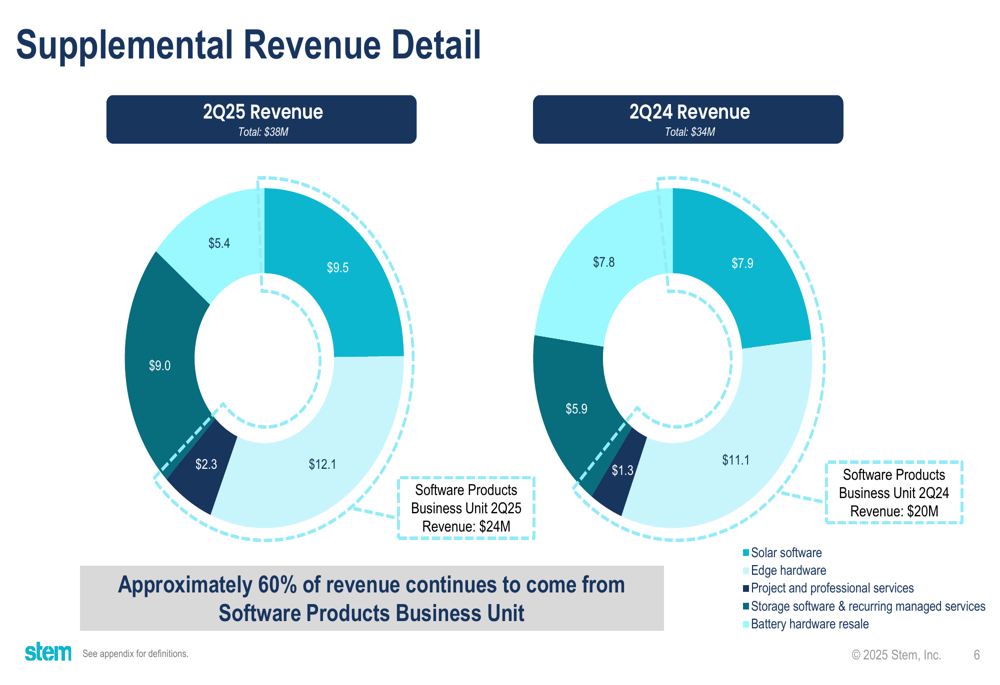

The company’s software-focused strategy appears to be bearing fruit, with approximately 60% of revenue now coming from the Software (ETR:SOWGn) Products Business Unit. This segment generated $24 million in Q2 2025, up from $20 million in Q2 2024, with notable growth in solar software revenue and storage software & recurring managed services.

Detailed Financial Analysis

Stem’s financial metrics showed several positive trends compared to the previous year. Revenue growth was accompanied by significant improvements in gross margins and a substantial reduction in operating expenses. Cash OpEx decreased from $29.5 million in Q2 2024 to $18.3 million in Q2 2025, contributing to the positive adjusted EBITDA.

The detailed financial comparison reveals the extent of these improvements:

However, operating cash flow declined from $(11.9) million to $(21.3) million year-over-year, which the company attributed to increased one-time expenses during the quarter and changes in working capital. This represents a reversal from Q1 2025, when Stem reported its first positive operating cash flow of $9 million.

The revenue breakdown shows diversification across multiple segments, with growth in both solar and storage software offerings:

Strategic Initiatives

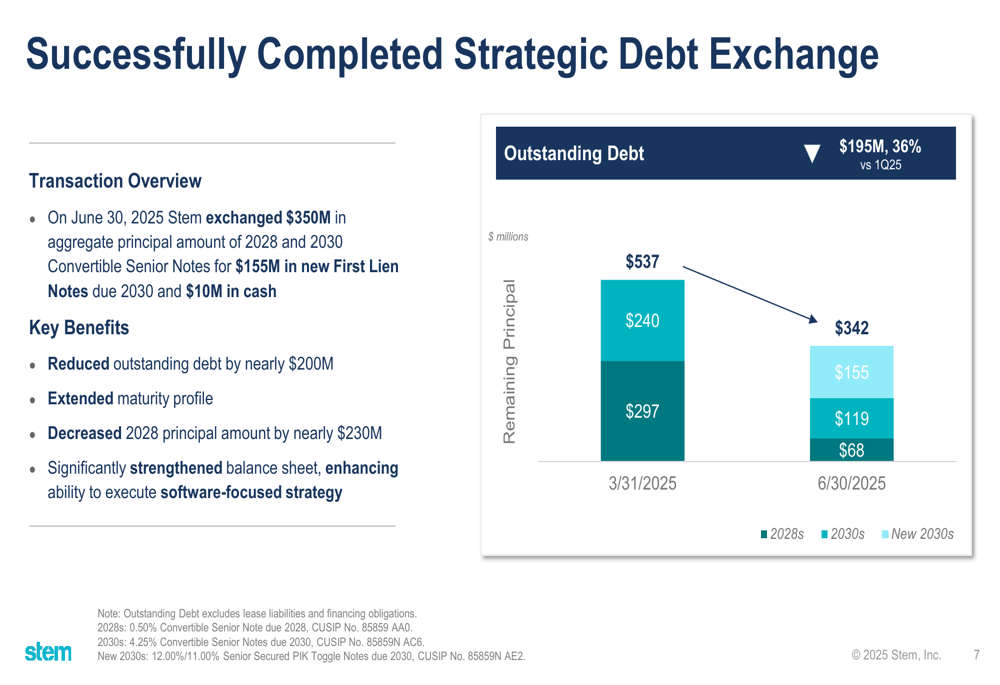

The most significant strategic move during the quarter was Stem’s debt exchange completed on June 30, 2025. The company exchanged $350 million in aggregate principal amount of 2028 and 2030 Convertible Senior Notes for $155 million in new First Lien Notes due 2030 and $10 million in cash.

This transaction reduced Stem’s outstanding debt by nearly $200 million (36%), extended its maturity profile, and decreased the 2028 principal amount by nearly $230 million, as illustrated in the following chart:

"The debt exchange significantly strengthened our balance sheet, enhancing our ability to execute our software-focused strategy," noted the company in its presentation.

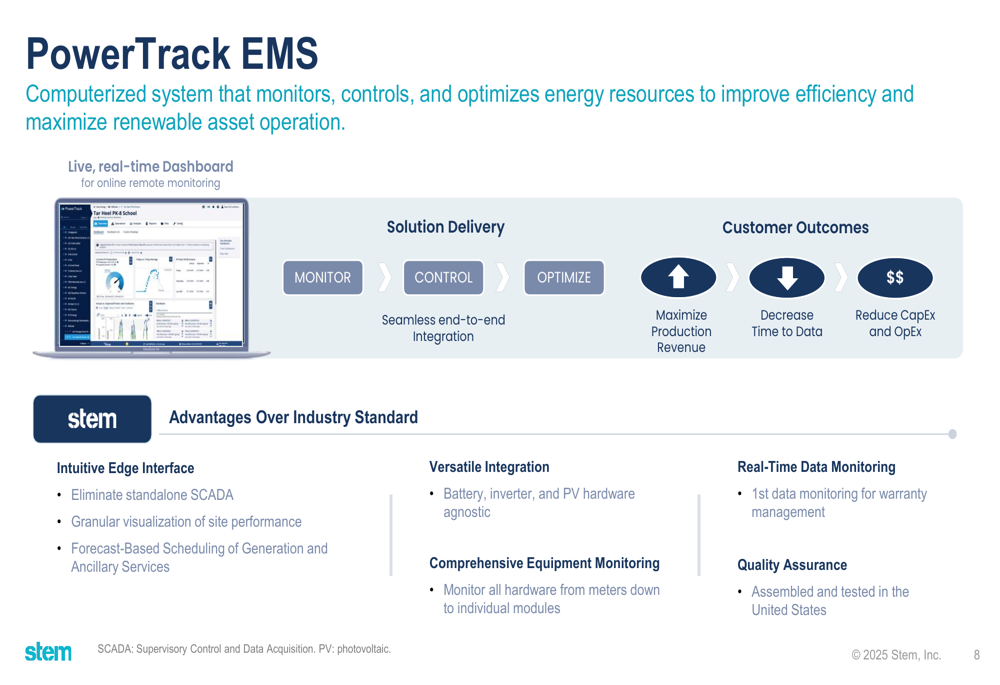

On the product front, Stem highlighted its PowerTrack Energy Management System (EMS), which offers monitoring, control, and optimization capabilities for renewable energy assets. The company announced multiple significant PowerTrack engagements during the quarter, including with Avangrid (NYSE:AGR) and Norbut Solar Farms.

The PowerTrack platform offers several advantages over industry standard solutions:

Forward-Looking Statements

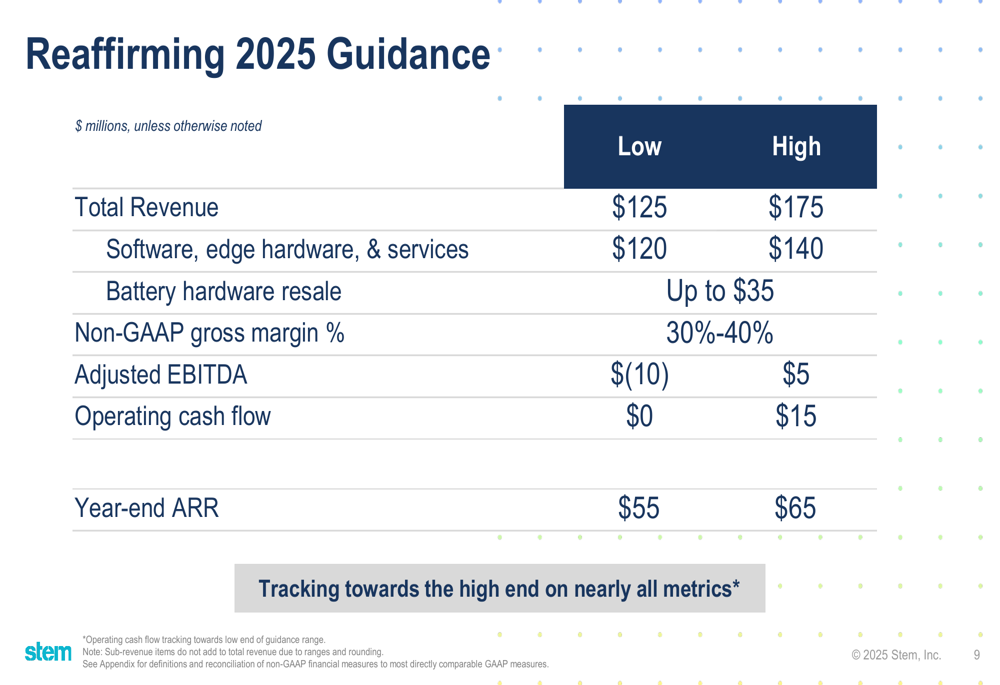

Stem reaffirmed its full-year 2025 guidance across all metrics, noting that it is tracking toward the high end on nearly all metrics, with the exception of operating cash flow which is tracking toward the low end of the projected range.

The company’s guidance projects:

The guidance suggests continued confidence in Stem’s software-focused strategy, despite the operating cash flow challenges in Q2. The company expects total revenue between $125-$175 million for the full year, with software, edge hardware, and services accounting for $120-$140 million of that total.

Non-GAAP gross margin is projected to be between 30-40%, while adjusted EBITDA is expected to range from $(10) million to $5 million. Year-end ARR is forecasted to be between $55-$65 million, with the company currently at $58.5 million as of Q2.

Stem’s Q2 results demonstrate progress in its transition toward a software-focused business model, with improved margins and a strengthened balance sheet. However, the negative operating cash flow remains a challenge that investors will likely monitor closely in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.