Nvidia’s results, Tesla’s European sales, Japan trade - what’s moving markets

Introduction & Market Context

Summit Hotel Properties, Inc. (NYSE:INN) released its first quarter 2025 earnings presentation on April 30, showing mixed results as the hospitality REIT faces operational challenges. Despite achieving modest RevPAR growth, the company reported declines in several key financial metrics compared to the same period last year. The stock closed at $4.07, representing a significant decline from its $6.34 price following the Q4 2024 earnings release, reflecting investor concerns about the company’s performance trajectory.

The presentation reveals a company maintaining a diversified portfolio of 97 hotels with 14,555 rooms across various brands and locations, but struggling to translate occupancy strength into improved financial performance.

Quarterly Performance Highlights

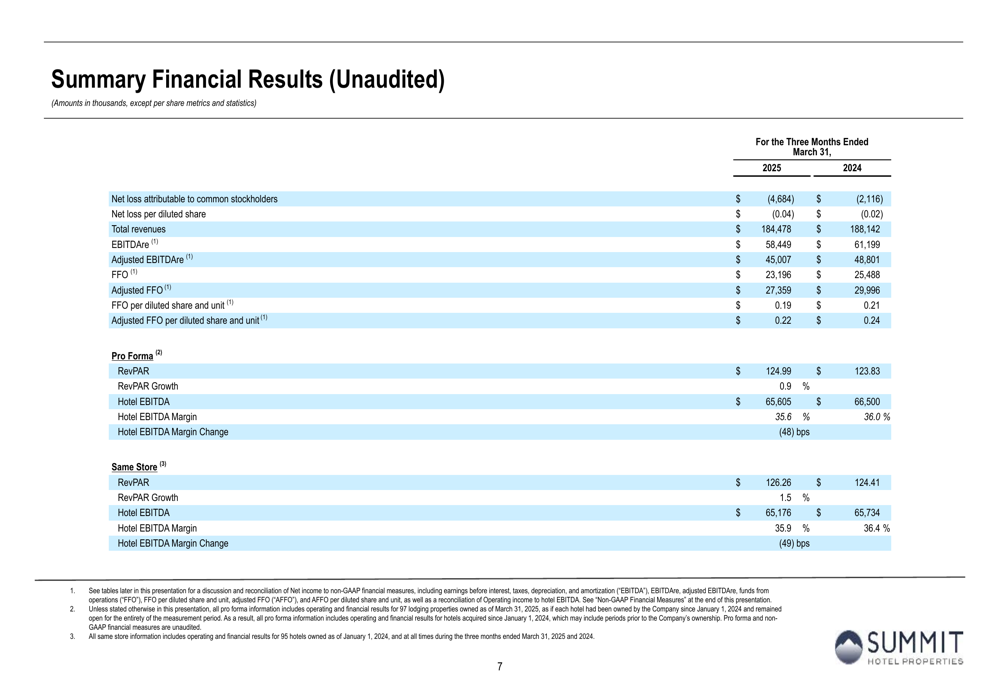

Summit Hotel Properties reported a net loss attributable to common stockholders of $(4,684) thousand for Q1 2025, more than double the $(2,116) thousand loss recorded in Q1 2024. Total (EPA:TTEF) revenues decreased by 1.9% year-over-year to $184,478 thousand from $188,142 thousand.

As shown in the following summary financial results:

Despite the overall revenue decline, the company achieved a modest 0.9% increase in RevPAR to $124.99. However, this growth was insufficient to offset other operational challenges, as evidenced by a 48 basis point decline in Hotel EBITDA Margin to 35.6%.

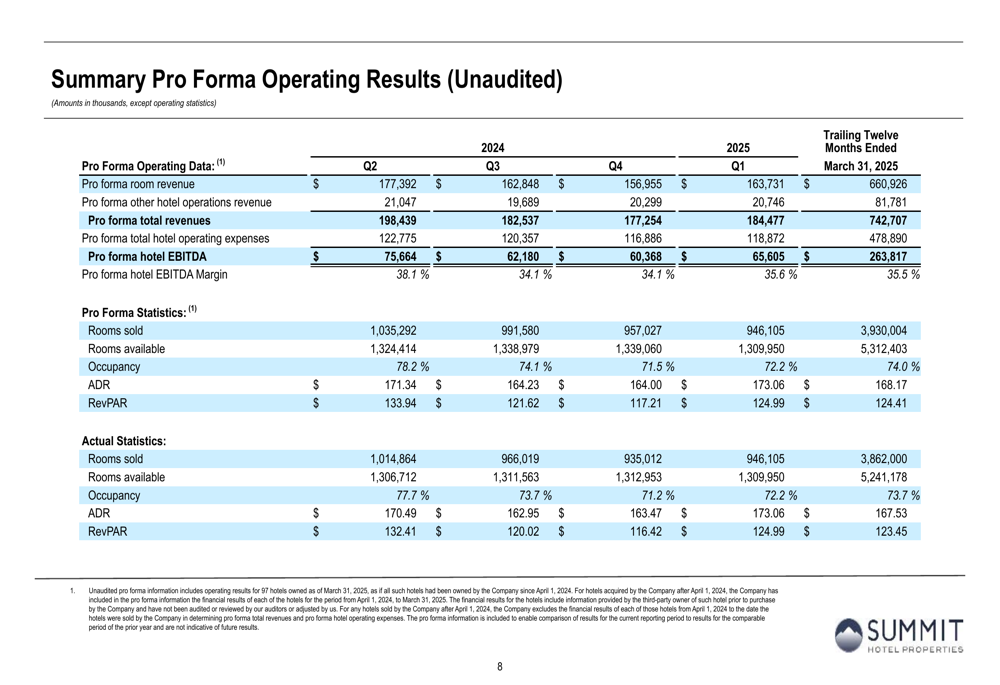

The company’s pro forma operating statistics provide additional context for its performance:

Pro forma occupancy remained relatively strong at 72.2%, with an ADR of $173.06 resulting in the previously mentioned RevPAR of $124.99. The trailing twelve-month data shows total revenues of $742,707 thousand and hotel EBITDA of $263,817 thousand, maintaining a margin of 35.5%.

Detailed Financial Analysis

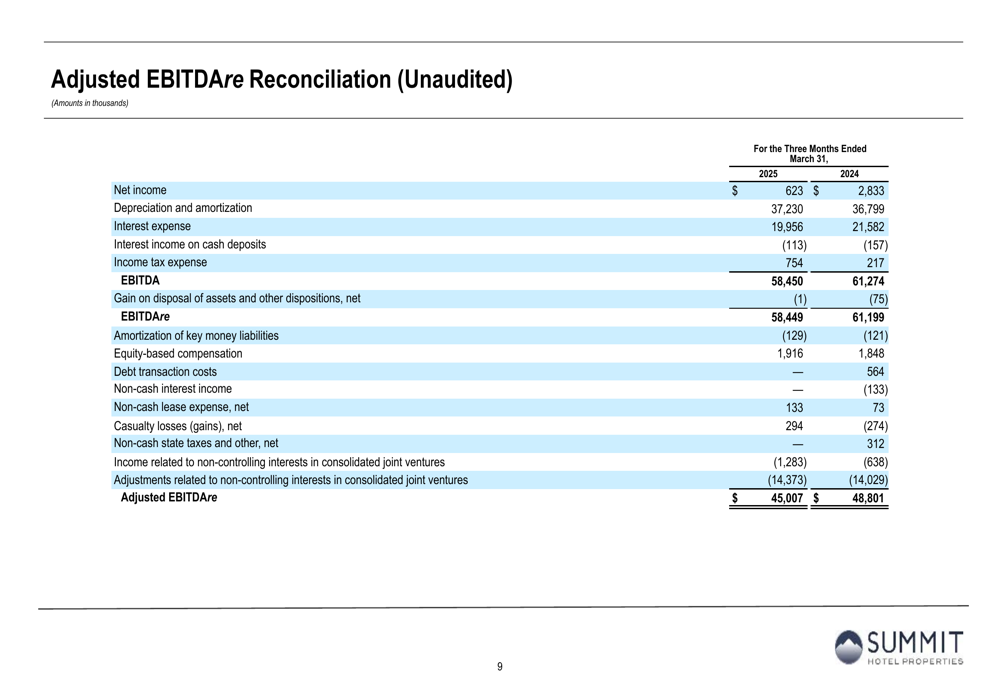

Summit’s adjusted earnings metrics showed consistent declines compared to the prior year. EBITDAre decreased by 4.5% to $58,449 thousand from $61,199 thousand, while Adjusted EBITDAre fell by 7.8% to $45,007 thousand from $48,801 thousand.

The reconciliation to Adjusted EBITDAre provides insight into the components affecting this key metric:

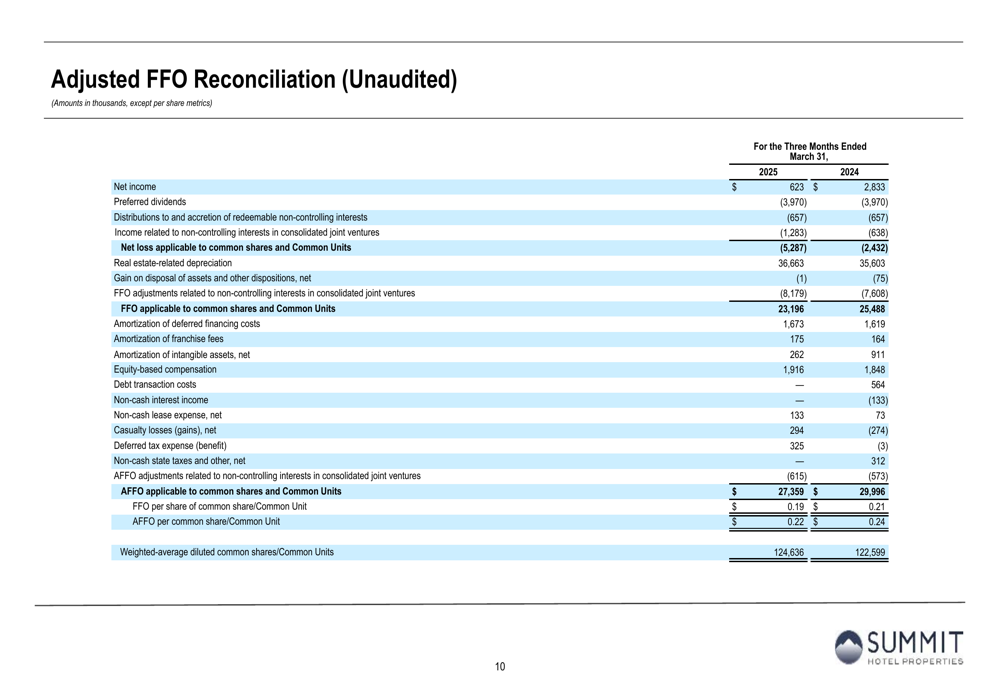

Similarly, Funds From Operations (FFO) declined by 9.0% to $23,196 thousand from $25,488 thousand, and Adjusted FFO decreased by 8.8% to $27,359 thousand from $29,996 thousand. On a per-share basis, FFO was $0.19 and Adjusted FFO was $0.22.

The detailed reconciliation to Adjusted FFO illustrates the impact of various adjustments:

These financial metrics indicate that despite maintaining reasonable occupancy levels, the company is facing challenges in translating room revenue into bottom-line results, suggesting potential cost pressures or inefficiencies in operations.

Strategic Positioning

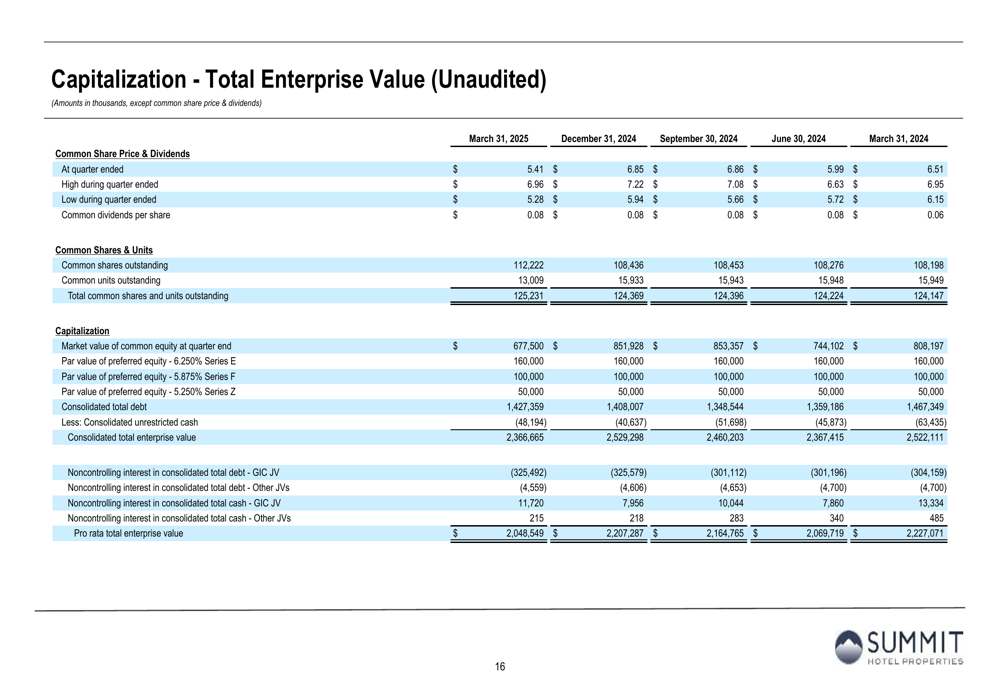

Summit Hotel Properties maintains a diversified capital structure with a total enterprise value of $2,366.665 million as of March 31, 2025. The company’s capitalization breakdown provides insight into its financial structure:

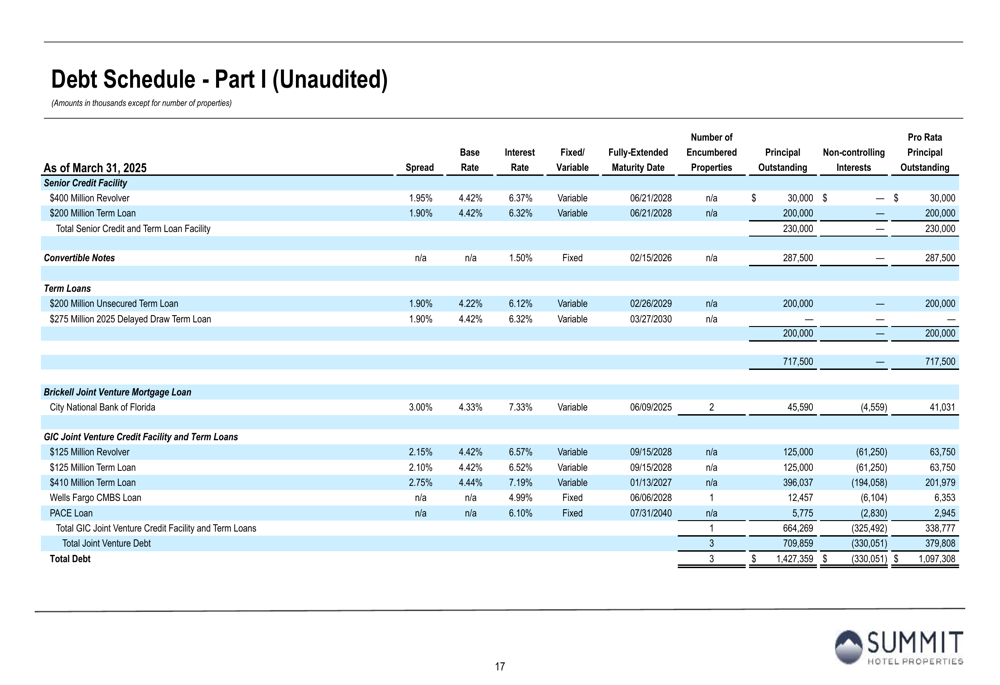

The company’s debt profile includes a mix of revolving credit facilities, term loans, convertible notes, and mortgage debt. The weighted average interest rate on the company’s debt was not explicitly stated, but the presentation details the various debt instruments and their respective terms:

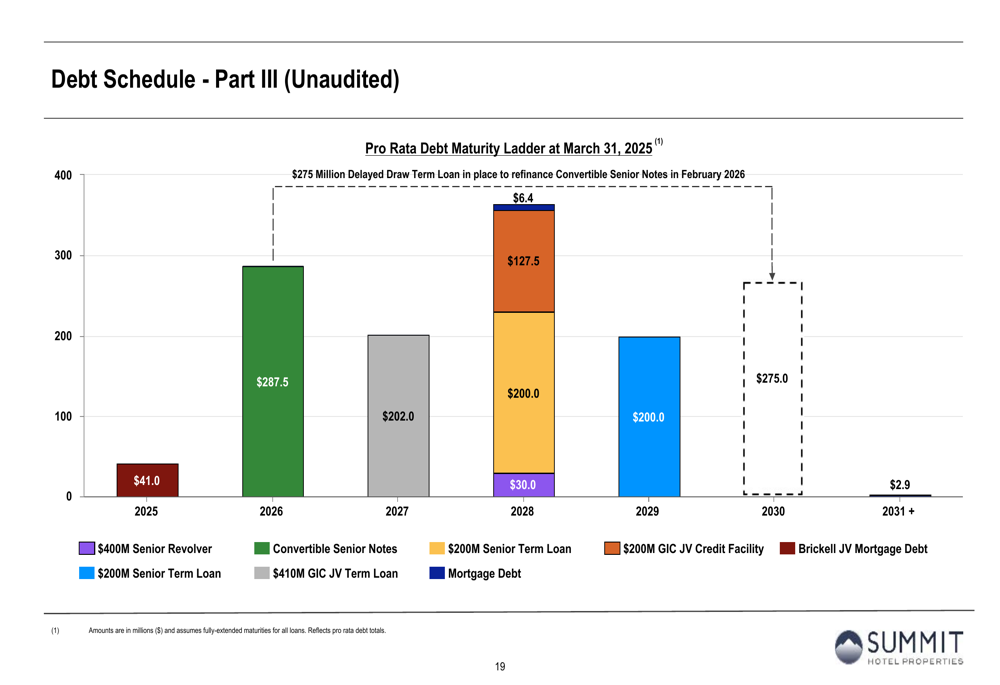

Summit’s debt maturity ladder shows a relatively well-distributed schedule of maturities, which helps mitigate refinancing risk:

The company’s portfolio remains diversified across ownership structures, with 51% ownership in a joint venture with GIC, 100% ownership of numerous properties, and 90% ownership in other joint ventures. This diversification strategy provides some insulation against market-specific downturns, though the overall financial results suggest broader operational challenges.

Forward-Looking Statements

The Q1 2025 results represent a departure from the positive momentum reported in Q4 2024, when the company exceeded earnings expectations with an EPS of $0.01 versus a forecasted loss of $0.08. The current results suggest that Summit Hotel Properties is facing headwinds in maintaining operational efficiency and profitability.

While the presentation did not provide explicit forward guidance, the declining financial metrics despite RevPAR growth indicate potential challenges ahead. The company’s ability to reverse the margin compression and return to profitability will likely depend on implementing effective cost controls and capitalizing on its relatively strong occupancy rates.

The significant stock price decline since the Q4 2024 earnings release suggests that investors remain cautious about Summit’s near-term prospects. However, the company’s diversified portfolio and structured debt profile provide some stability as it navigates the current operational challenges.

For investors in the hospitality REIT sector, Summit’s results may signal broader industry pressures, particularly related to cost management and the ability to translate occupancy into improved financial performance. As the company moves forward in 2025, its ability to address these challenges will be crucial for restoring investor confidence and improving shareholder returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.