Intel stock spikes after report of possible US government stake

Introduction & Market Context

Summit Midstream Corporation (NYSE:SMC) presented at Citi’s 2025 Natural Resources Conference on August 12-14, showcasing its strategic positioning across diversified midstream assets. The company, which operates across six resource plays in the United States, emphasized its value-driven approach focused on maximizing free cash flow, deleveraging, and strategic growth initiatives.

With a weighted average contract life of over 7.8 years and more than 85% fixed fee-based gross margin, Summit has built a stable foundation in a sector that continues to face commodity price volatility. The company’s Q1 2025 adjusted EBITDA of $57.5 million demonstrated resilience, though its financial health score remains an area of concern according to recent analyses.

Strategic Positioning and Asset Overview

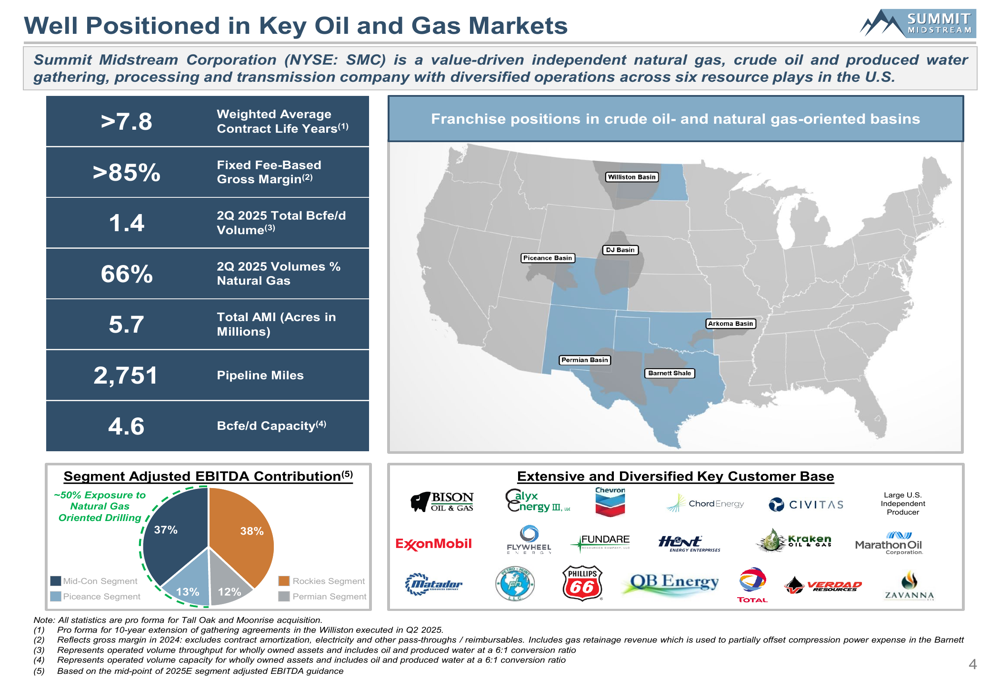

Summit Midstream has established a diversified footprint across key oil and gas basins, including the Permian, Williston, DJ, Barnett, and Arkoma. This geographic diversity provides operational stability and multiple growth avenues as producer activity continues to recover.

As shown in the following map of Summit’s operating footprint, the company has strategically positioned itself in both oil and gas-oriented basins:

The company’s operations span 2,751 pipeline miles with 4.6 Bcfe/d of capacity, currently handling approximately 1.4 Bcfe/d in volume as of Q2 2025. Natural gas represents 66% of current volumes, providing some insulation from crude oil price volatility.

Summit’s recent strategic initiatives have focused on simplifying its organizational structure and strengthening its balance sheet, as illustrated in this progress timeline:

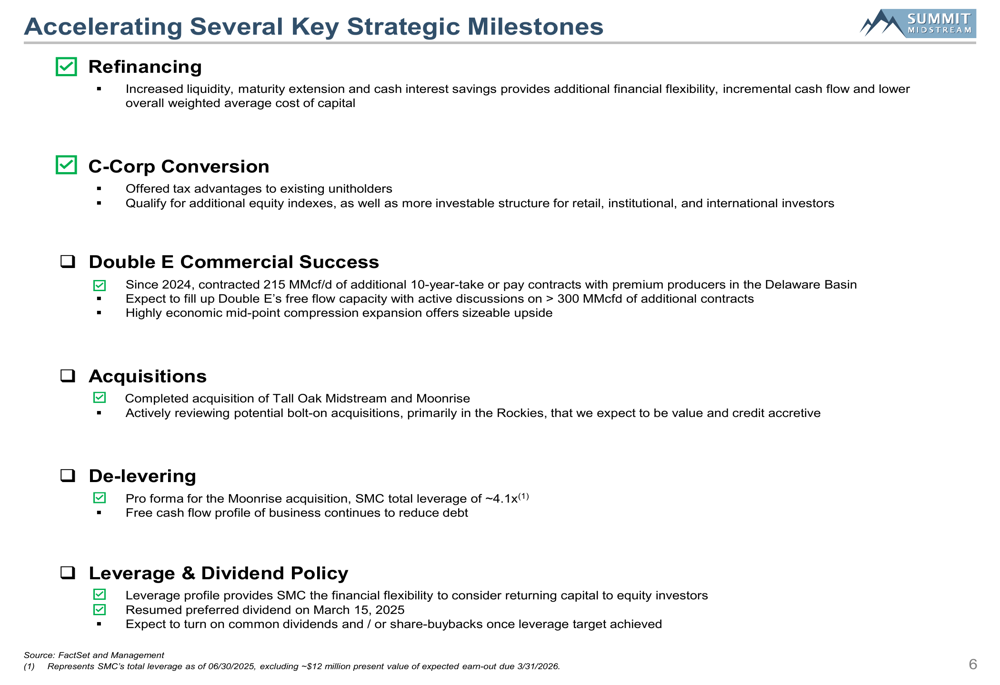

The company has made substantial progress in executing its corporate strategy, including cost control initiatives resulting in approximately $20 million in annual expense savings, liability management through debt repayments and refinancing, and strategic acquisitions and divestitures. Notable achievements include retiring over $850 million in debt and refinancing approximately $1.0 billion of debt with extended maturities and a "covenant-lite" structure.

Financial Performance and Outlook

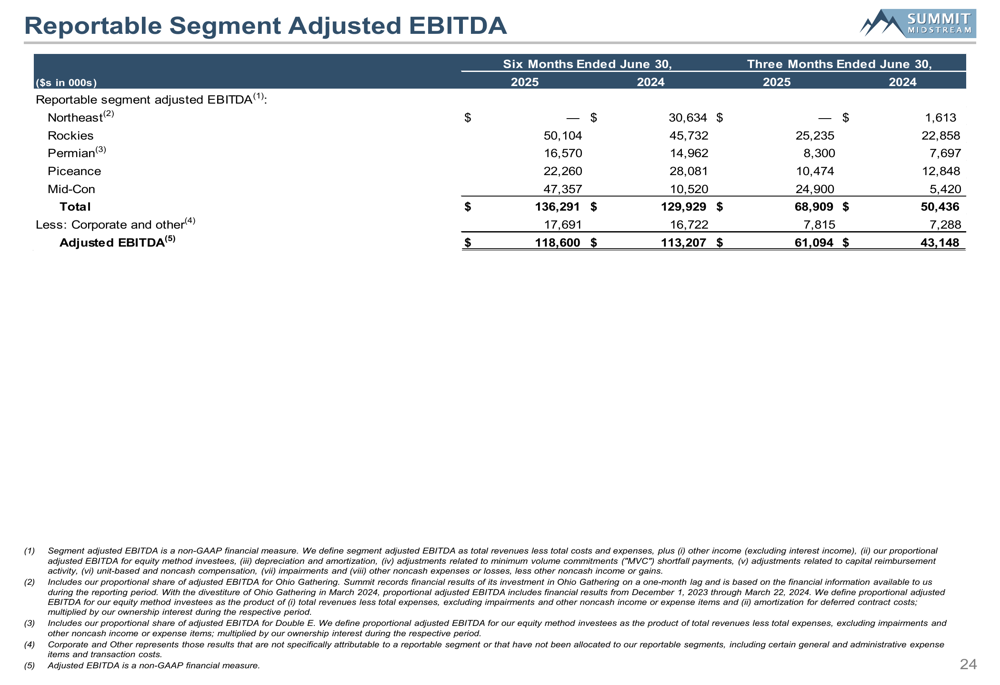

Summit Midstream’s Q2 2025 segment adjusted EBITDA breakdown shows the contribution from each of its operating regions:

For the three months ended June 30, 2025, the Rockies segment contributed $25.2 million, the Permian segment $8.3 million, the Mid-Con segment $24.9 million, and the Piceance segment $10.5 million. The Northeast segment, which contributed $1.6 million in Q2 2024, no longer appears in the 2025 results following strategic divestitures.

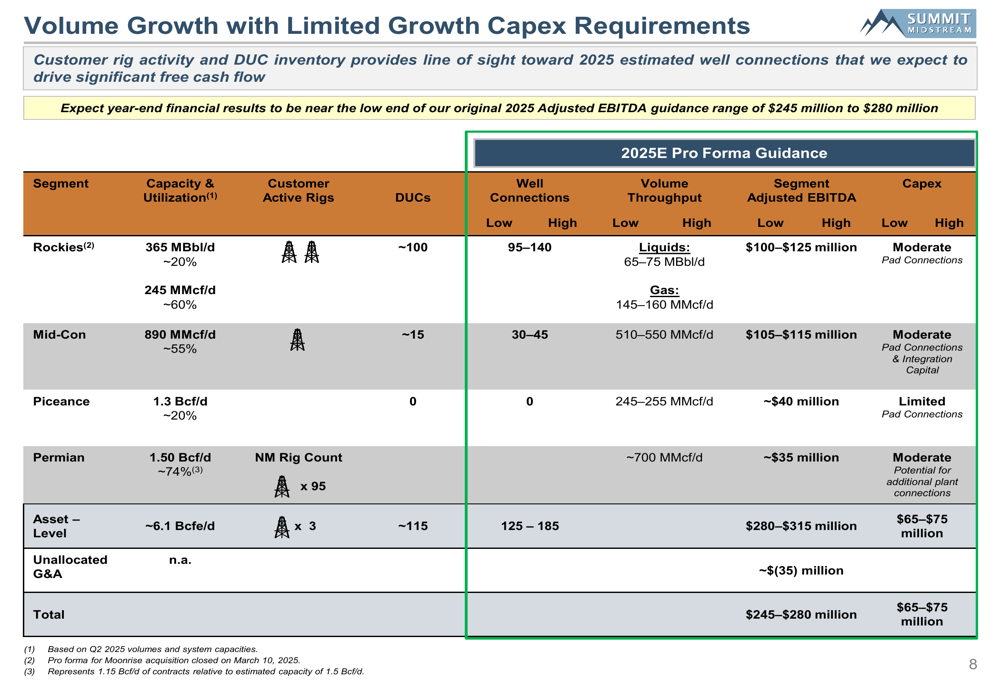

The company expects its year-end financial results to be near the low end of its original 2025 Adjusted EBITDA guidance range of $245 million to $280 million. This aligns with commentary from the Q1 earnings call, where management indicated potential headwinds if well completions are deferred.

Summit’s volume growth projections are supported by limited capital expenditure requirements, as illustrated in this guidance table:

The company’s ample system capacity across its operating regions limits the need for significant growth capital expenditures, allowing more free cash flow to be directed toward debt reduction. Customer rig activity and DUC (drilled but uncompleted wells) inventory provide visibility toward 2025 estimated well connections.

Deleveraging Strategy and Balance Sheet Strength

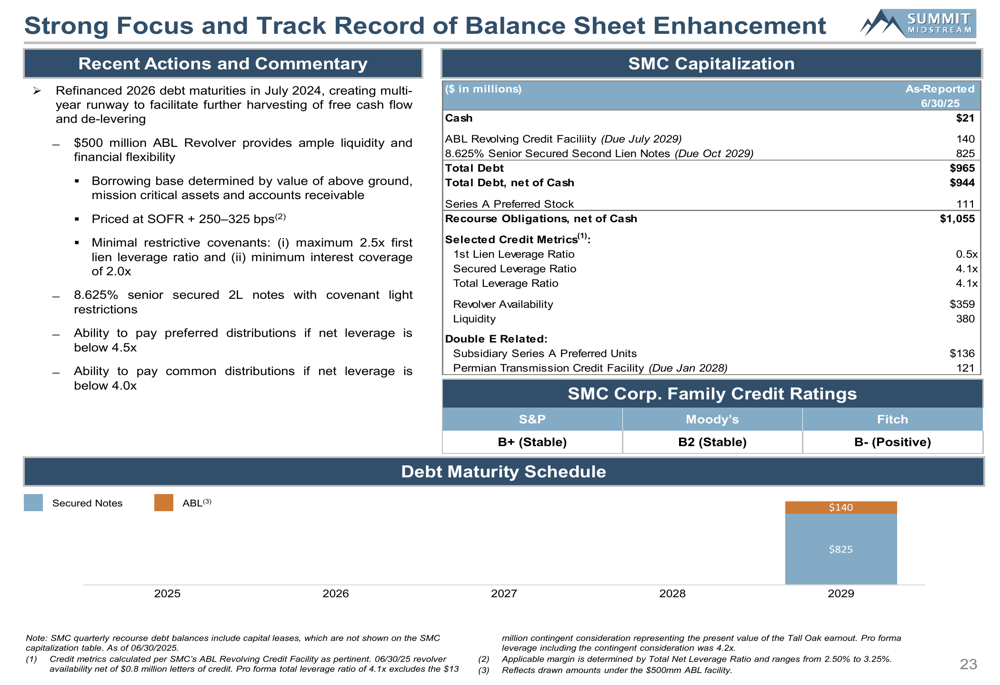

A key focus of Summit’s presentation was its commitment to deleveraging and strengthening its balance sheet. The company has made significant progress in this area, as shown in the following slide:

Summit refinanced its 2026 debt maturities in July 2024, creating a multi-year runway to facilitate further free cash flow generation and deleveraging. As of June 30, 2025, the company had $21 million in cash, $140 million drawn on its ABL revolving credit facility, and $825 million in 8.625% senior secured second lien notes, resulting in total debt of $965 million and net debt of $944 million.

The company’s pro forma leverage ratio stands at approximately 4.1x following the Moonrise acquisition, with a long-term target of 3.5x. Summit resumed its preferred dividend on March 15, 2025, and expects to consider common dividends and/or share buybacks once its leverage target is achieved.

Valuation Analysis and Growth Catalysts

Summit Midstream’s presentation highlighted its attractive relative valuation compared to peers, suggesting potential upside as the company executes its strategy:

Trading at an enterprise value to 2025 estimated EBITDA multiple of 7.2x for its base business, Summit trades at a discount to the peer average of 9.8x. The company attributes this discount to its higher leverage and historical MLP structure, which it has addressed through its C-Corp conversion and ongoing deleveraging efforts.

A significant growth catalyst for Summit is its Double E pipeline in the Permian Basin, which connects New Mexico natural gas to the Waha Hub. The company has executed 215 MMcf/d of incremental 10-year take-or-pay contracts since 2024, and is actively discussing over 300 MMcf/d of additional contracts. This asset is valued at a higher multiple than the company’s gathering and processing assets, potentially providing additional value as utilization increases.

The company’s key investment highlights summarize its value proposition:

Summit’s strategic milestones include its refinancing, C-Corp conversion, Double E commercial success, strategic acquisitions, and deleveraging efforts:

Conclusion

Summit Midstream’s Q2 2025 presentation outlines a clear strategy focused on maximizing shareholder value through financial discipline, strategic growth, and operational excellence. The company’s diversified asset base, long-term contracts, and limited capital expenditure requirements position it to generate significant free cash flow for debt reduction and eventual shareholder returns.

While the company expects to be at the lower end of its 2025 EBITDA guidance, its stable business model and strategic initiatives provide a foundation for long-term value creation. The valuation discount relative to peers offers potential upside as Summit continues to execute on its deleveraging strategy and increases utilization across its asset base.

Investors will be watching closely for continued progress on debt reduction, increased utilization of the Double E pipeline, and the company’s ability to capitalize on producer activity in its key operating regions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.