ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

SunCoke Energy Inc (NYSE:SXC) released its third-quarter 2025 results on November 4, revealing a challenging period for the metallurgical coke producer and industrial services provider. Despite beating analyst expectations with earnings per share of $0.26 versus a forecasted $0.17, the company's stock fell 12.26% to close at $8.24, reflecting investor concerns about ongoing operational challenges and reduced guidance.

The quarter was marked by the completion of the Phoenix Global acquisition on August 1, 2025, which has reshaped SunCoke's business mix while adding to its debt load. Meanwhile, a contract breach by a key customer resulted in deferred coke sales, forcing the company to revise its full-year outlook.

Quarterly Performance Highlights

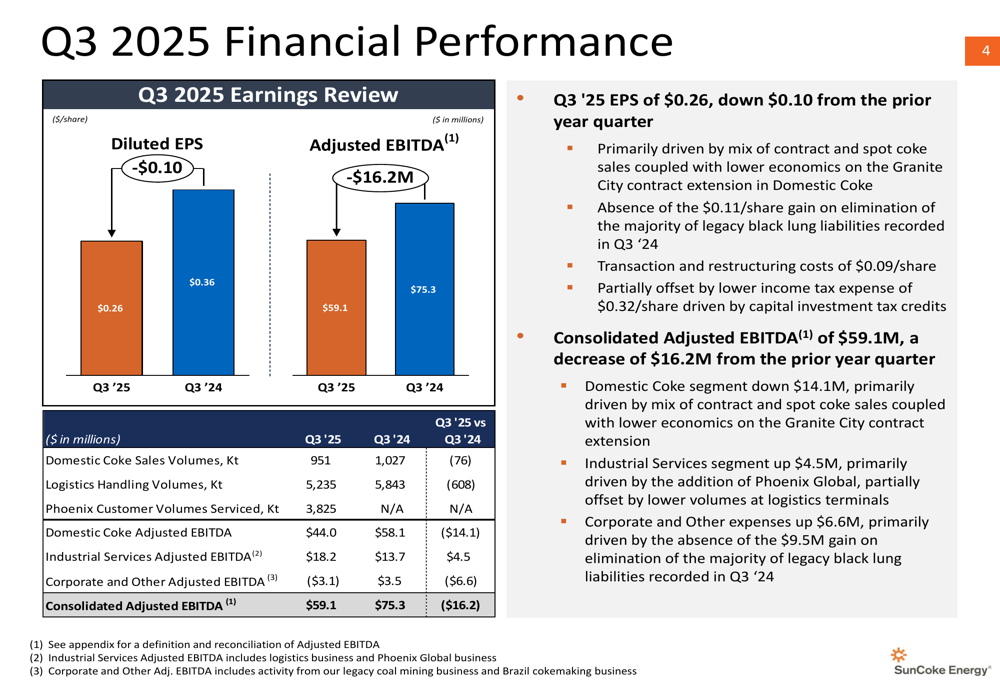

SunCoke reported consolidated adjusted EBITDA of $59.1 million for Q3 2025, a significant decrease from $75.3 million in the same period last year. Diluted earnings per share came in at $0.26, down from $0.36 in Q3 2024, though still exceeding analyst expectations.

The company's performance was impacted by several factors, including lower coke volumes and pricing, less favorable contract terms, and the deferral of approximately 200,000 tons of coke sales due to a customer contract breach. These challenges were partially offset by two months of contribution from the newly acquired Phoenix Global business.

As shown in the following financial performance comparison:

The quarter also marked SunCoke's 25th consecutive quarterly cash dividend of $0.12 per share, payable on December 1, 2025, demonstrating the company's commitment to returning capital to shareholders despite operational headwinds.

Segment Analysis

Domestic Coke Business

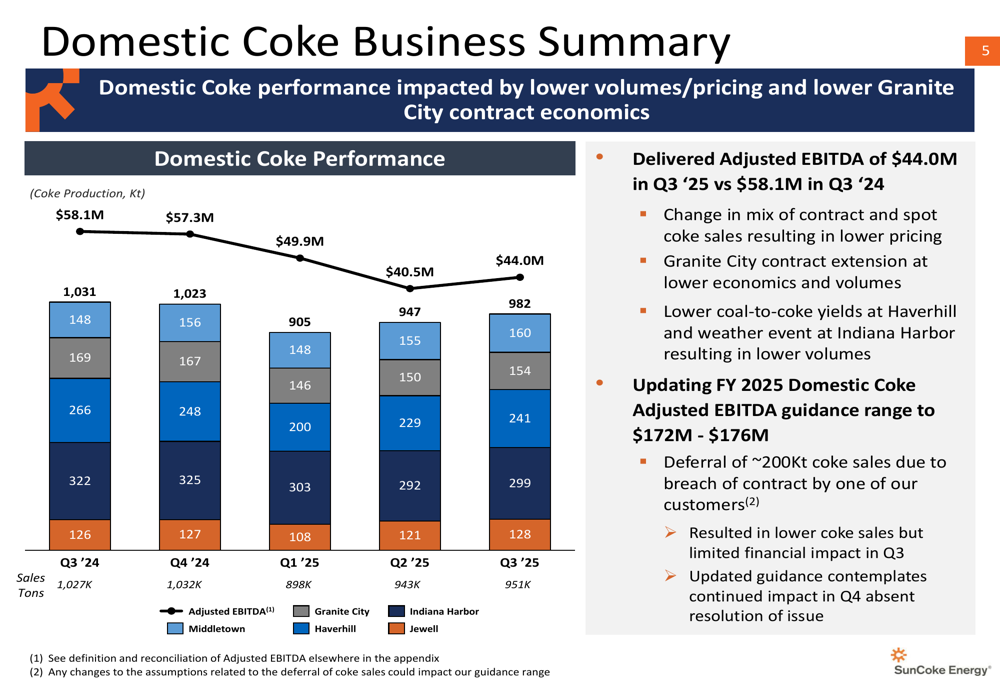

SunCoke's Domestic Coke segment, which remains the company's largest business unit, experienced a significant decline in performance. The segment delivered adjusted EBITDA of $44.0 million in Q3 2025, down from $58.1 million in Q3 2024. This 24.3% decrease was primarily attributed to lower volumes, reduced pricing, and less favorable terms in the extended Granite City contract with U.S. Steel.

The following chart illustrates the downward trend in Domestic Coke performance:

Sales volumes for the segment were 951,000 tons in Q3 2025, compared to 1,027,000 tons in the same period last year. In response to these challenges, SunCoke updated its full-year 2025 Domestic Coke adjusted EBITDA guidance range to $172-$176 million, reflecting the impact of the customer contract breach and market conditions.

Industrial Services Business

The newly expanded Industrial Services segment, which now includes the former Logistics segment and Phoenix Global operations, delivered adjusted EBITDA of $18.2 million in Q3 2025, up from $13.7 million in Q3 2024. This increase was primarily driven by the addition of two months of Phoenix Global results, which contributed 3,825,000 tons of customer volumes serviced.

The segment's performance is detailed in the following chart:

Despite the positive contribution from Phoenix Global, the company noted that lower volumes at its logistics terminals, driven by challenging market conditions, partially offset these gains. SunCoke has established a full-year 2025 Industrial Services adjusted EBITDA guidance range of $63-$67 million.

Financial Position and Liquidity

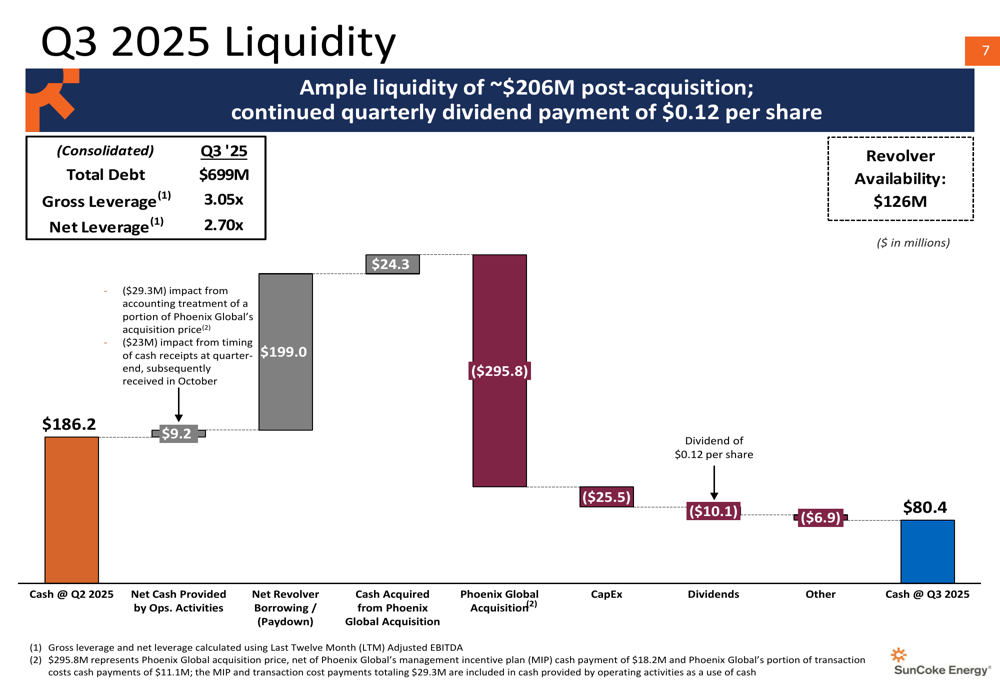

The acquisition of Phoenix Global has significantly impacted SunCoke's balance sheet and liquidity position. As of September 30, 2025, the company reported total liquidity of approximately $206 million, down from $540 million at the end of 2024. Total debt increased to $699 million from $500 million during the same period.

The following chart details the company's liquidity position:

SunCoke's gross leverage ratio stood at 3.05x and net leverage at 2.70x at the end of Q3 2025. While management characterized this as "ample liquidity," the significant reduction in financial flexibility following the acquisition raises questions about the company's ability to navigate ongoing challenges in its core business while managing increased debt obligations.

Updated Guidance and Outlook

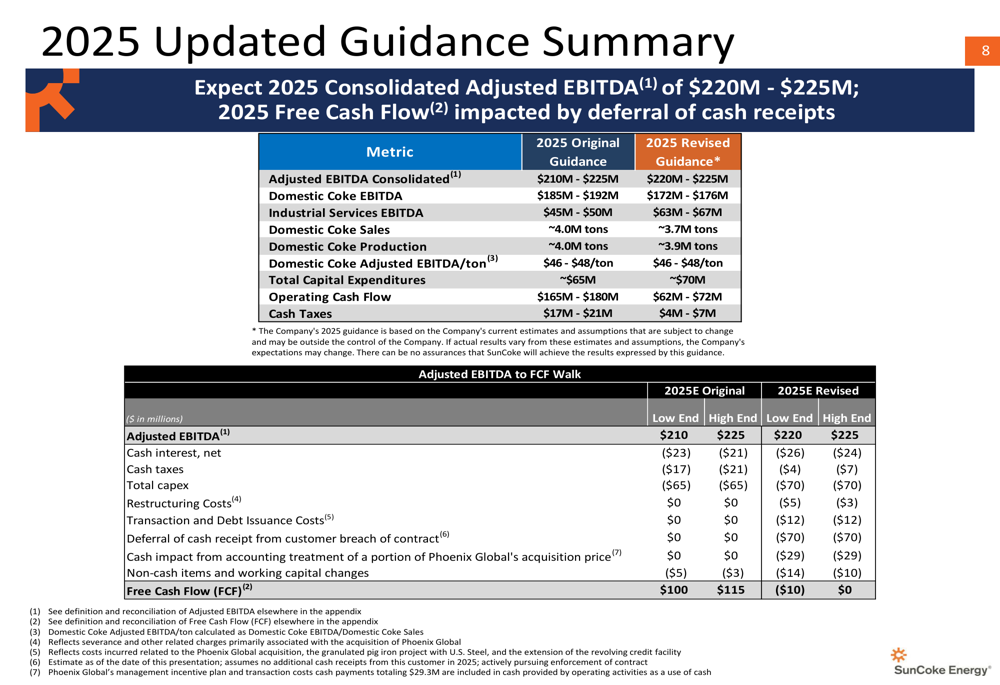

In light of the Phoenix Global acquisition and operational challenges, SunCoke has updated its full-year 2025 guidance. The company now expects consolidated adjusted EBITDA of $220-$225 million, compared to its original guidance of $210-$225 million. However, this revised range includes five months of Phoenix Global results, masking underlying weakness in the core Domestic Coke business.

The most significant revision came in operating cash flow guidance, which was reduced from $165-$180 million to $62-$72 million, primarily due to the deferral of cash receipts related to the customer contract breach. As a result, free cash flow is now projected to be between -$10 million and $0 for the year.

The updated guidance is detailed in the following table:

Despite these near-term challenges, management expressed optimism about 2026, expecting to start recognizing synergies from the Phoenix Global acquisition and potentially resolving the contractual dispute that has impacted 2025 performance.

Strategic Initiatives

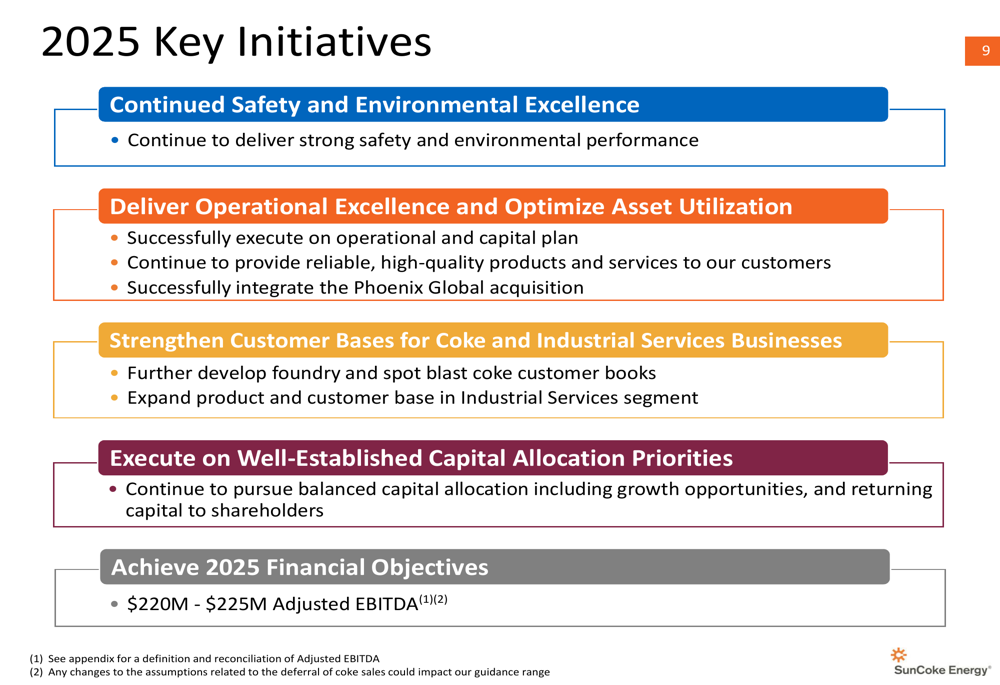

SunCoke outlined several key initiatives for 2025 aimed at strengthening its competitive position and financial performance:

The company emphasized its focus on operational excellence and asset utilization optimization, which will be critical as it integrates the Phoenix Global business and addresses challenges in its Domestic Coke segment. Additionally, SunCoke highlighted its commitment to strengthening customer relationships across both business segments, particularly important given the recent contract breach by a key customer.

Management also noted the extension of the Granite City cokemaking contract with U.S. Steel through December 31, 2025, providing some stability in its customer base. However, the short-term nature of this extension suggests potential uncertainty beyond next year.

As SunCoke navigates these challenges and opportunities, investors will be closely monitoring the company's progress in integrating Phoenix Global, resolving the customer contract dispute, and maintaining financial discipline amid increased leverage and reduced liquidity.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.