LATAM Airlines pilots in Chile to begin strike at midnight Wednesday

Introduction & Market Context

Swisscom AG (SIX:SCMN) presented its Q1 2025 results on May 8, 2025, marking the first quarter with fully consolidated Vodafone (NASDAQ:VOD) Italia operations. The Swiss telecommunications giant reported a slight revenue decline but confirmed its full-year guidance as it advances with integration efforts in Italy while maintaining its dominant position in Switzerland.

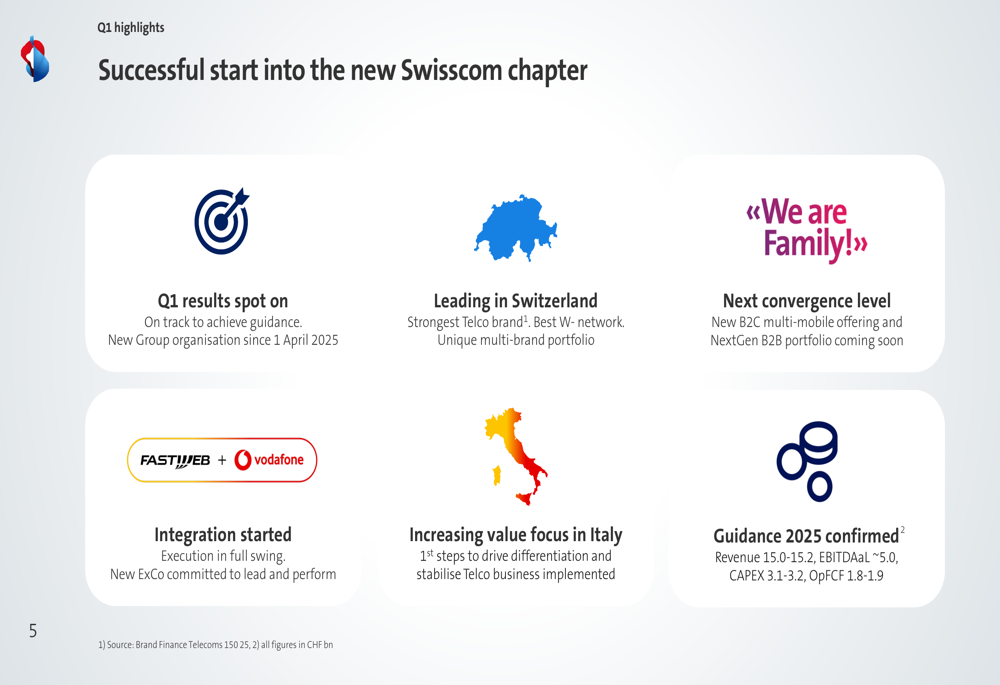

The presentation highlighted Swisscom’s strategic priorities following the significant Vodafone Italia acquisition, which has transformed the company’s footprint in the Italian market. Management characterized Q1 as a "successful start into the new Swisscom chapter," emphasizing that results are on track to achieve 2025 guidance despite transitional challenges.

Quarterly Performance Highlights

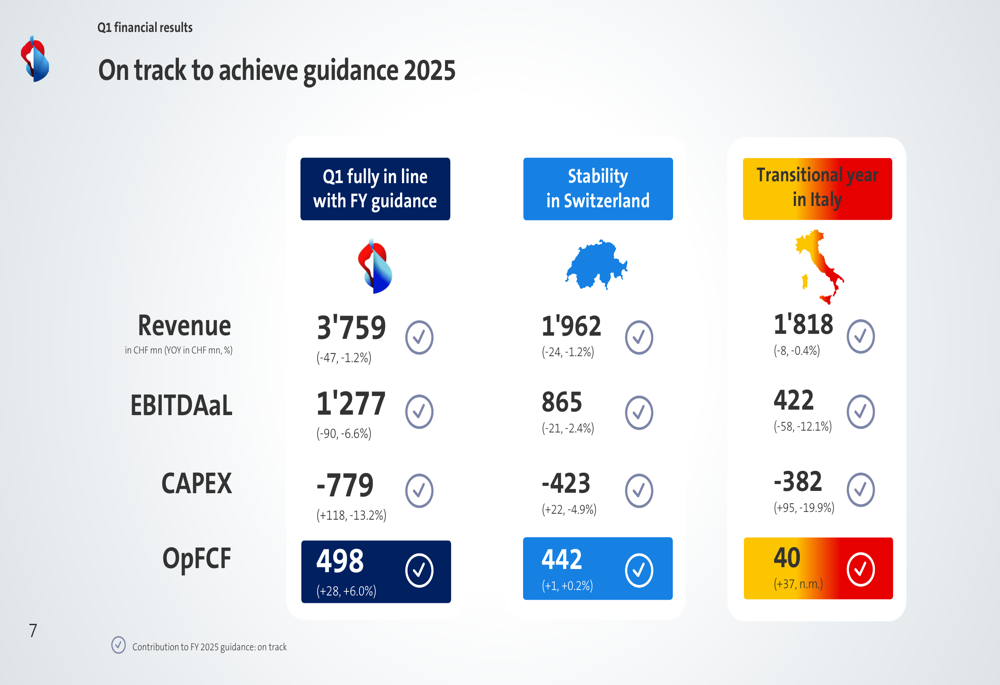

Swisscom reported Q1 2025 revenue of CHF 3,759 million, representing a modest 1.2% year-over-year decline. EBITDAAL (EBITDA after leases) fell more substantially by 6.6% to CHF 1,277 million, while operating free cash flow improved by 6.0% to CHF 498 million. The company emphasized that these results are fully in line with its full-year guidance.

As shown in the following financial results summary:

The performance was characterized by relative stability in Switzerland, where revenue declined 1.2% to CHF 1,962 million and EBITDAAL fell 2.4% to CHF 865 million. Italy, described as being in a "transitional year," saw revenue decrease by 0.4% to CHF 1,818 million, while EBITDAAL dropped more significantly by 12.1% to CHF 422 million.

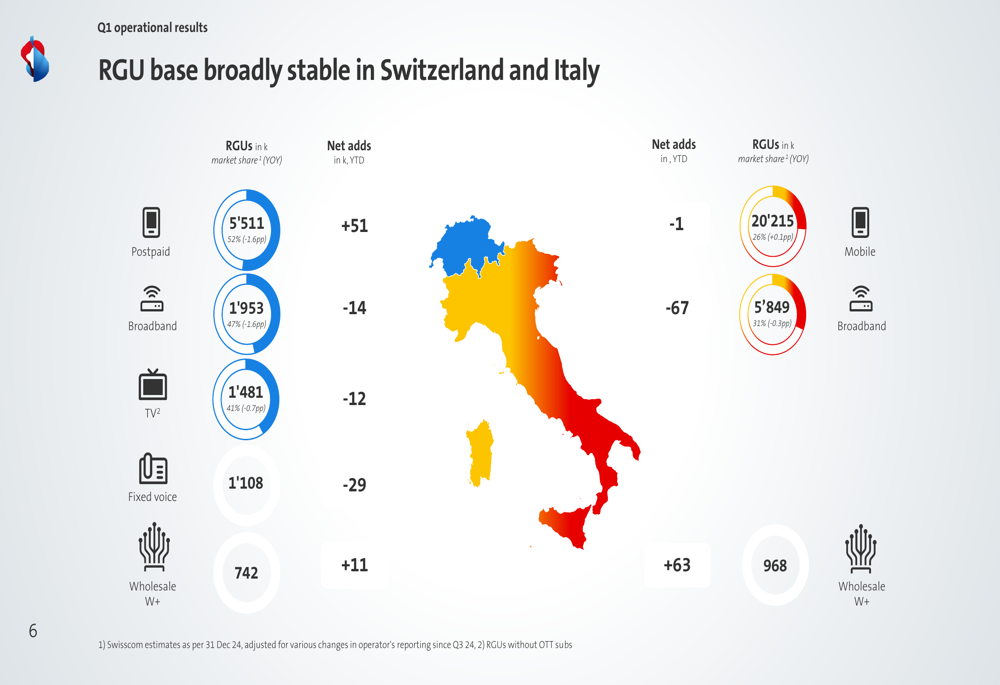

From an operational perspective, Swisscom maintained its market leadership in Switzerland with 5.51 million postpaid mobile customers (52% market share) and 1.95 million broadband customers (47% market share). In Italy, the combined entity now serves 20.22 million mobile customers (26% market share) and 5.85 million broadband customers (31% market share).

The company’s customer base metrics are illustrated in this operational results slide:

Detailed Financial Analysis

Swisscom’s capital expenditures (CAPEX) decreased by 13.2% year-over-year to CHF 779 million, with reductions in both Switzerland (-4.9% to CHF 423 million) and Italy (-19.9% to CHF 382 million). This CAPEX reduction, combined with the EBITDAAL performance, resulted in the 6.0% improvement in operating free cash flow.

The company emphasized that its Q1 results position it well to achieve its full-year 2025 guidance, which remains unchanged: revenue of CHF 15.0-15.2 billion, EBITDAaL of approximately CHF 5.0 billion, CAPEX of CHF 3.1-3.2 billion, and operating free cash flow of CHF 1.8-1.9 billion.

For proper comparison, Swisscom provided pro forma figures that treat the Vodafone Italia acquisition as if it had been consolidated from January 1, 2024. This approach allows for meaningful year-over-year analysis despite the significant change in corporate structure.

Strategic Initiatives

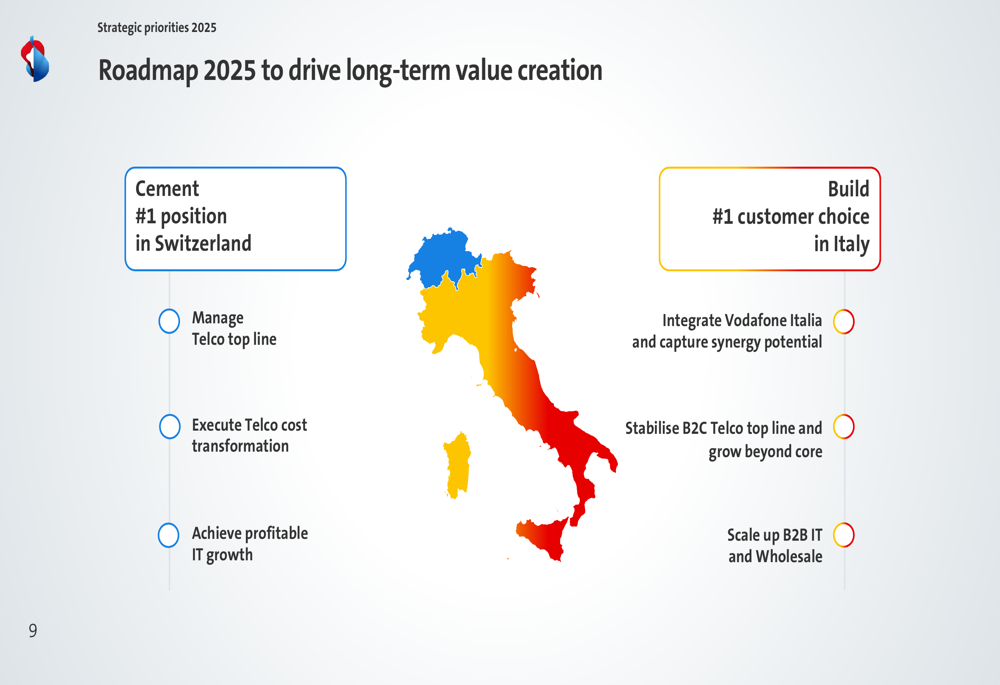

Swisscom outlined its strategic roadmap for 2025, focusing on cementing its #1 position in Switzerland while building the #1 customer choice in Italy. The strategy emphasizes managing telecom revenue, executing cost transformation, and achieving profitable IT growth in Switzerland, while in Italy the focus is on integration, stabilizing consumer telecom revenue, and scaling up business IT and wholesale operations.

The strategic priorities are visualized in this slide:

In Switzerland, Swisscom is emphasizing convergence offerings and household penetration through its multi-brand strategy. The company highlighted the successful launch of its "We are Family" multi-mobile convergence offering and new Blue Kids subscriptions targeting families. The company is also strengthening its secondary brands, with Wingo positioning as a full-service provider, M-Budget Mobile offering promotions in over 250 supermarkets, and Coop Mobile running promotion weeks.

The consumer strategy for Switzerland is detailed in this slide:

For Italy, Swisscom emphasized that integration efforts are "in full swing" with a new executive committee committed to leading the combined entity. The company has implemented initial steps to drive differentiation and stabilize the telecom business in Italy, though specific details were limited in the presentation.

Forward-Looking Statements

Swisscom’s Q1 2025 highlights slide summarizes the company’s key achievements and outlook:

The company confirmed its 2025 guidance across all key financial metrics, expressing confidence in its ability to execute its strategic priorities despite the complexity of integrating Vodafone Italia. Management emphasized the strength of Swisscom’s brand in Switzerland, its network quality, and unique multi-brand portfolio as competitive advantages.

Looking ahead, Swisscom plans to launch new B2C multi-mobile offerings and a "NextGen B2B portfolio" soon, aiming to take convergence to the "next level." The company also highlighted its increasing value focus in Italy, where it has implemented initial steps to drive differentiation and stabilize the telecom business.

The integration of Vodafone Italia remains a central focus, with execution described as "in full swing" and a new executive committee in place to lead the combined entity. This integration is expected to deliver significant synergies over time, though specific targets were not detailed in the Q1 presentation.

As Swisscom navigates this transformative period, the company appears focused on balancing the stability of its Swiss operations with the growth potential and integration challenges of its expanded Italian business.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.