Trump-Zelensky meeting ahead, Fed rate outlook in focus - what’s moving markets

Introduction & Market Context

Symbotic Inc. (NASDAQ:SYM) presented its latest investor update on August 6, 2025, showcasing the company’s continued momentum in revolutionizing supply chain automation through artificial intelligence and robotics. The presentation follows Symbotic’s strong Q2 2025 earnings report, where the company exceeded revenue expectations with $550 million, representing a 40% year-over-year increase.

Trading at $63.21 at market close, Symbotic has experienced significant stock appreciation from its 52-week low of $16.32, reflecting growing investor confidence in the company’s execution and market opportunity. The stock saw a minor 0.33% decline in after-hours trading.

The company’s vision to "Reimagine the Supply Chain with Artificial Intelligence and Robotics and Transform the Distribution Network into a Strategic Asset" continues to resonate with major retailers and distributors facing persistent labor challenges, evolving omni-channel demands, and SKU proliferation.

As shown in this vision statement slide:

Quarterly Performance Highlights

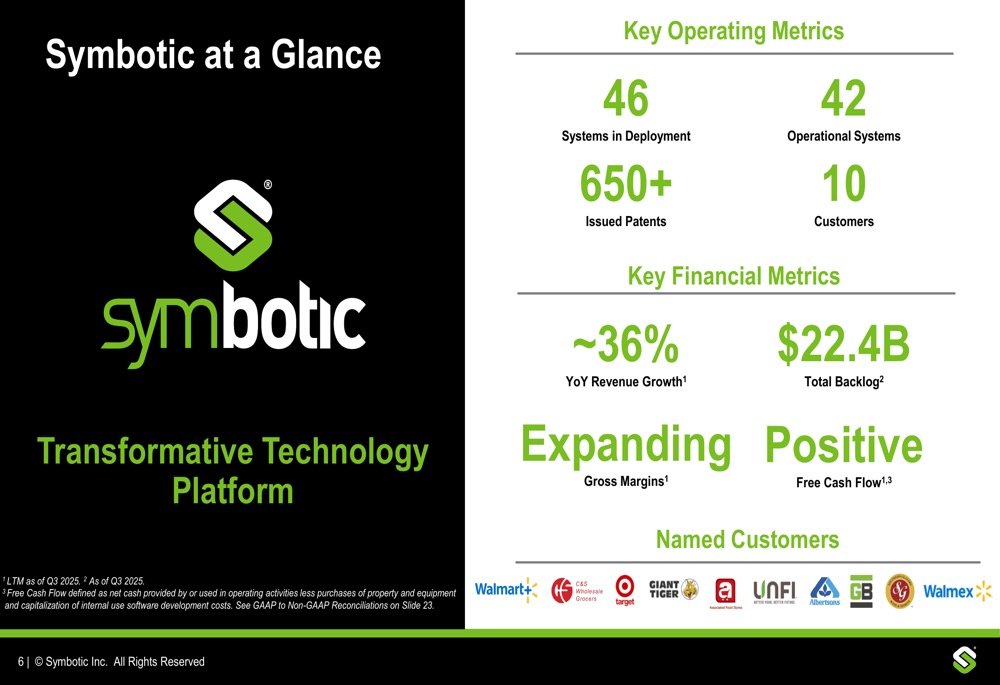

Symbotic’s Q3 2025 presentation highlighted impressive operational and financial metrics that demonstrate the company’s scaling capabilities. The company now has 46 systems in deployment and 42 operational systems, a substantial increase from 44 and 25 respectively at the end of FY2024. This rapid deployment acceleration underscores Symbotic’s improving operational efficiency.

Revenue growth remains robust at approximately 36% year-over-year for the last twelve months ending Q3 2025, consistent with the 40% growth reported in Q2. The company’s total backlog stands at an impressive $22.4 billion, providing exceptional revenue visibility for the coming years.

The following slide summarizes Symbotic’s key metrics:

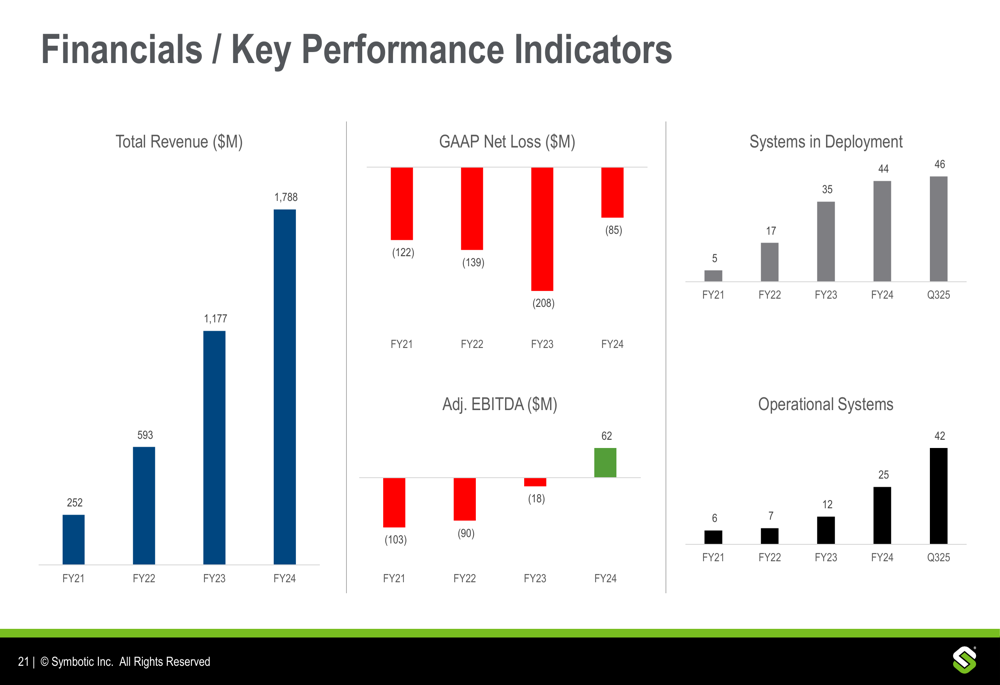

Financial performance continues to improve, with expanding gross margins and positive free cash flow. This represents significant progress from the company’s historical losses, as Symbotic has steadily reduced its GAAP net loss from $122 million in FY2021 to $85 million in FY2024. In the most recent Q2 2025 earnings report, the net loss was further reduced to $21 million, compared to $55 million in the same quarter last year.

Adjusted EBITDA has shown remarkable improvement, turning positive at $61.7 million for FY2024 compared to a loss of $103.4 million in FY2021. This positive trend continued in Q2 2025, with adjusted EBITDA of $35 million, more than triple the $9 million reported in Q2 2024.

The financial progression is clearly illustrated in this performance indicators slide:

Strategic Initiatives

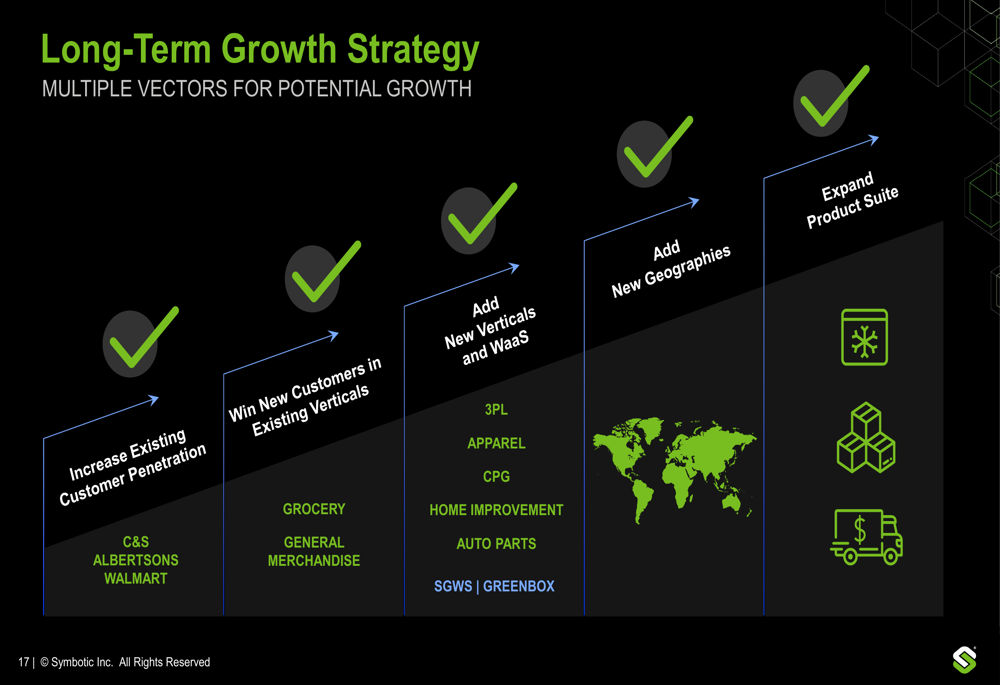

Symbotic outlined multiple growth vectors in its presentation, focusing on both expanding relationships with existing customers and capturing new market opportunities. The company’s strategic initiatives include increasing penetration with current blue-chip customers like Walmart (NYSE:WMT), Albertsons (NYSE:ACI), and C&S Wholesale Grocers, while simultaneously targeting new customers in existing verticals and expanding into additional sectors.

A key strategic development is Symbotic’s joint venture with SoftBank (TYO:9984) to acquire GreenBox, which has an $11 billion contract and unlocks a $500 billion annual total addressable market through a Warehouse-as-a-Service (WaaS) model. This partnership, with Symbotic maintaining 35% ownership, represents a significant expansion opportunity beyond the company’s traditional business model.

The company’s long-term growth strategy is visualized in this comprehensive slide:

Product innovation remains central to Symbotic’s strategy. In August 2025, the company announced its Next (LON:NXT) Gen Storage Structure Design, featuring higher density storage, rapid assembly capabilities, and enhanced safety features including integrated fire suppression and improved seismic adaptability. Additionally, Symbotic continues to develop its BreakPack solution, which enables the efficient handling of individual items (eaches) alongside cases, addressing a critical need in the evolving e-commerce landscape.

Symbotic’s business model combines capital asset sales with recurring revenue streams from software licensing and maintenance services over 15-year contracts. This approach creates long-term revenue visibility while allowing the company to continuously improve margins as the installed base grows.

Competitive Industry Position

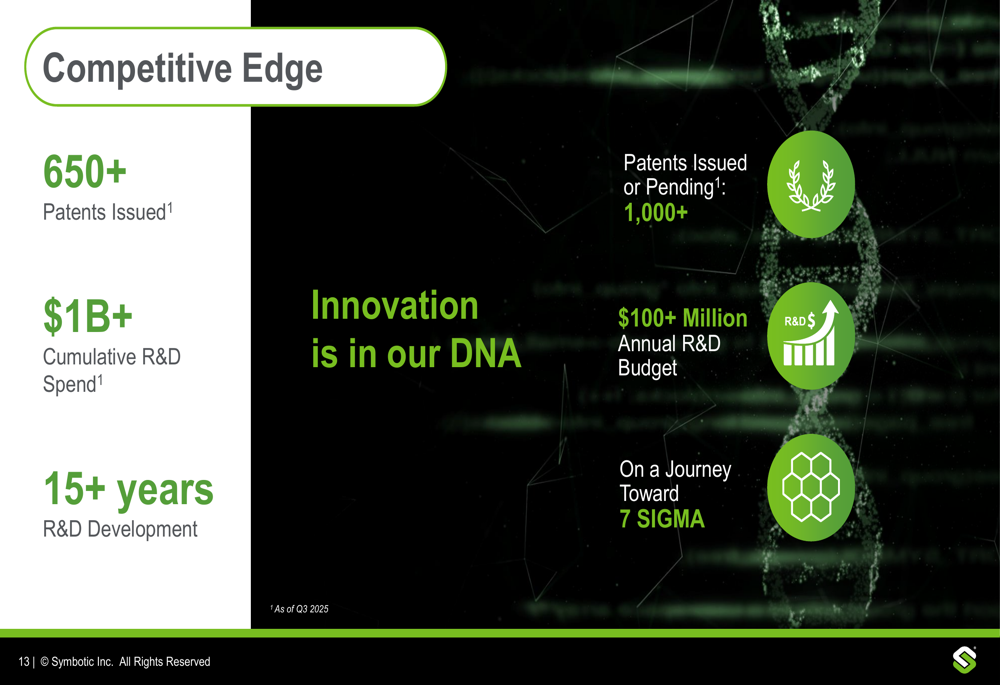

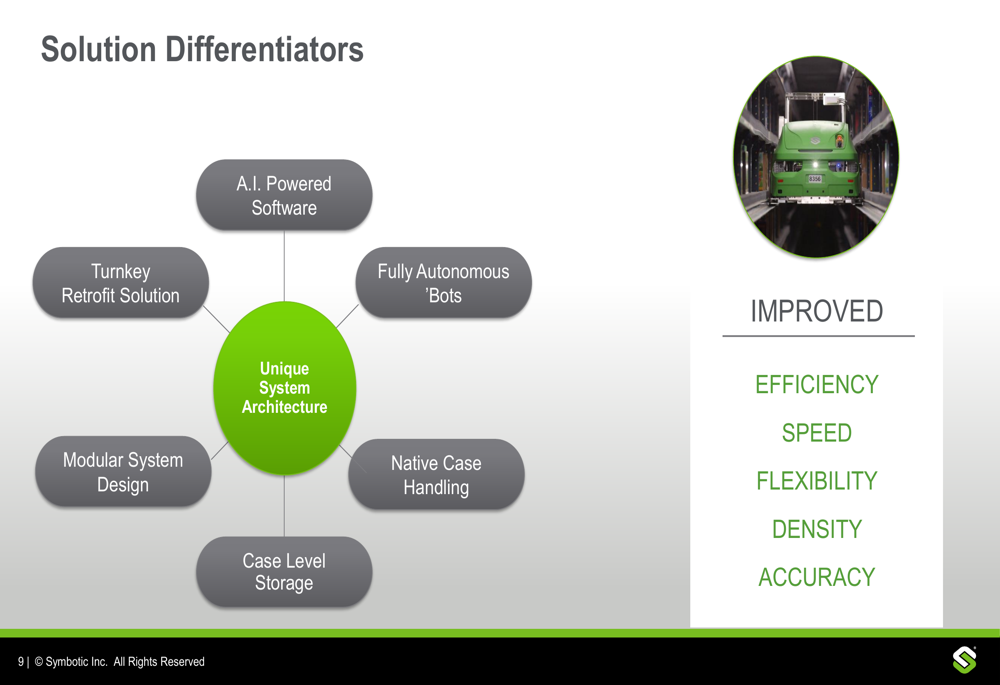

Symbotic positions itself as having significant competitive advantages in the supply chain automation market, backed by over 650 issued patents and more than $1 billion in cumulative R&D investment over 15+ years. This intellectual property foundation provides substantial barriers to entry and technological differentiation.

The company’s competitive edge is clearly illustrated in this slide:

The company differentiates itself through several key technological advantages, including AI-powered software, fully autonomous robots, native case handling capabilities, and a unique system architecture that enables greater efficiency, speed, flexibility, density, and accuracy compared to traditional solutions.

Symbotic’s impressive customer roster includes the world’s largest retailer by revenue (Walmart), the second-largest U.S. supermarket chain (Albertsons), and the largest U.S. wholesale grocery distributor (C&S Wholesale Grocers), demonstrating the solution’s appeal to industry leaders. These relationships provide powerful validation in a competitive landscape that includes established players like Honeywell (NASDAQ:HON) Intelligrated, Dematic, and Vanderlande in distribution centers, and Amazon (NASDAQ:AMZN), Ocado (LON:OCDO), and AutoStore in order fulfillment.

The comprehensive solution differentiators are showcased in this slide:

Forward-Looking Statements

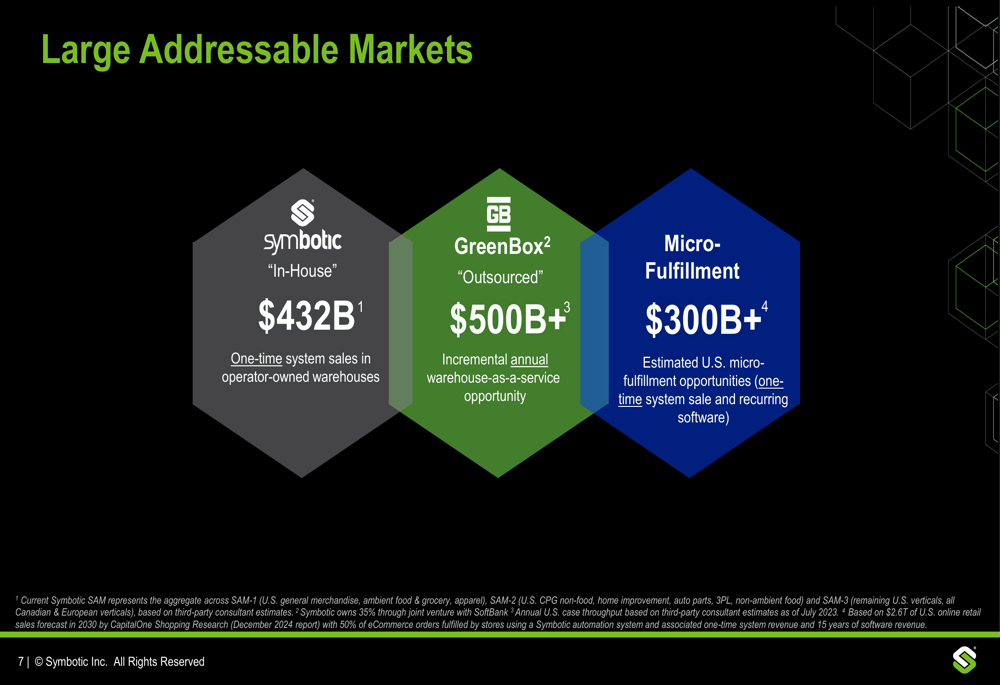

Symbotic’s presentation highlights massive addressable markets totaling over $1.2 trillion across in-house operations ($432 billion), outsourced logistics ($500+ billion), and micro-fulfillment ($300+ billion). This extensive opportunity provides multiple avenues for sustained long-term growth.

The large addressable markets are visualized in this slide:

While specific guidance for Q4 2025 wasn’t detailed in the presentation, the company previously provided Q3 revenue guidance of $520-540 million and adjusted EBITDA of $26-30 million during its Q2 earnings call. The consistent execution against the $22.4 billion backlog suggests Symbotic remains on track with its growth trajectory.

Management has emphasized the company’s focus on improving deployment efficiency and exploring new market opportunities. CEO Rick Cohen previously highlighted the "strong multiyear opportunity with nearly $23 billion of backlog," while CFO Carol Hibbert noted that "execution has improved resulting in improved gross margin performance."

With continued operational improvements, expanding margins, and a massive contracted backlog, Symbotic appears well-positioned to maintain its growth momentum while progressing toward sustainable profitability. The company’s innovative approach to supply chain automation, combined with strong customer relationships and strategic partnerships, provides a solid foundation for long-term success in a rapidly evolving industry.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.