Chip stocks fall with Nvidia after data center rev disappointment

Syndax Pharmaceuticals Inc (NASDAQ:SNDX) presented its first quarter 2025 financial results on May 5, revealing strong commercial momentum for its two recently launched products while maintaining a substantial cash position. The oncology-focused company reported significant revenue growth for Revuforj and Niktimvo in their first full quarter of sales, though operating expenses remain high as the company invests in commercialization and pipeline development.

Quarterly Performance Highlights

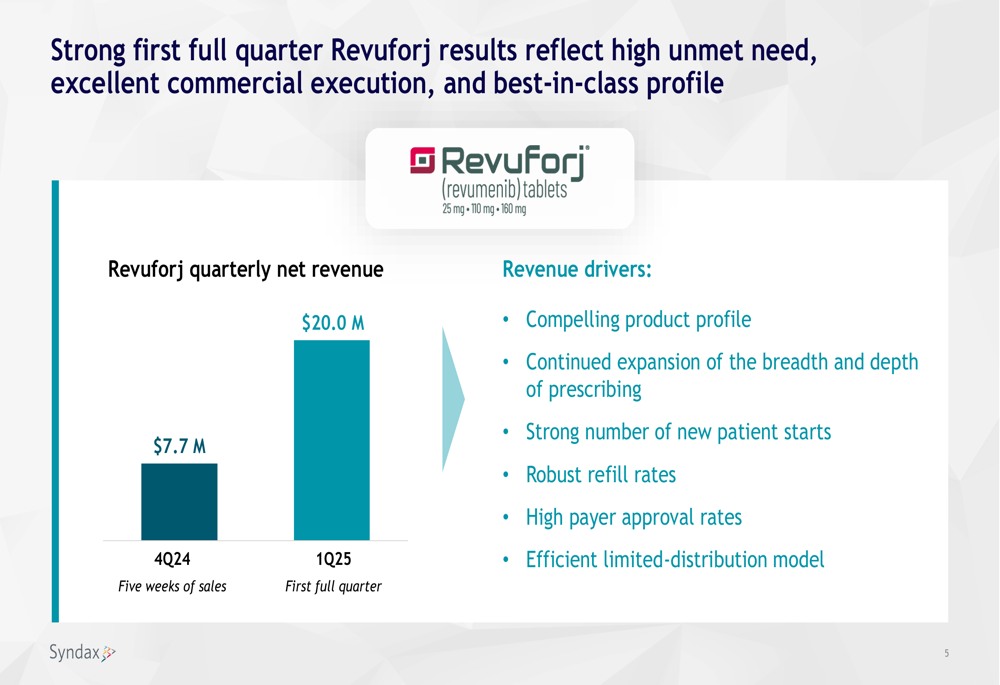

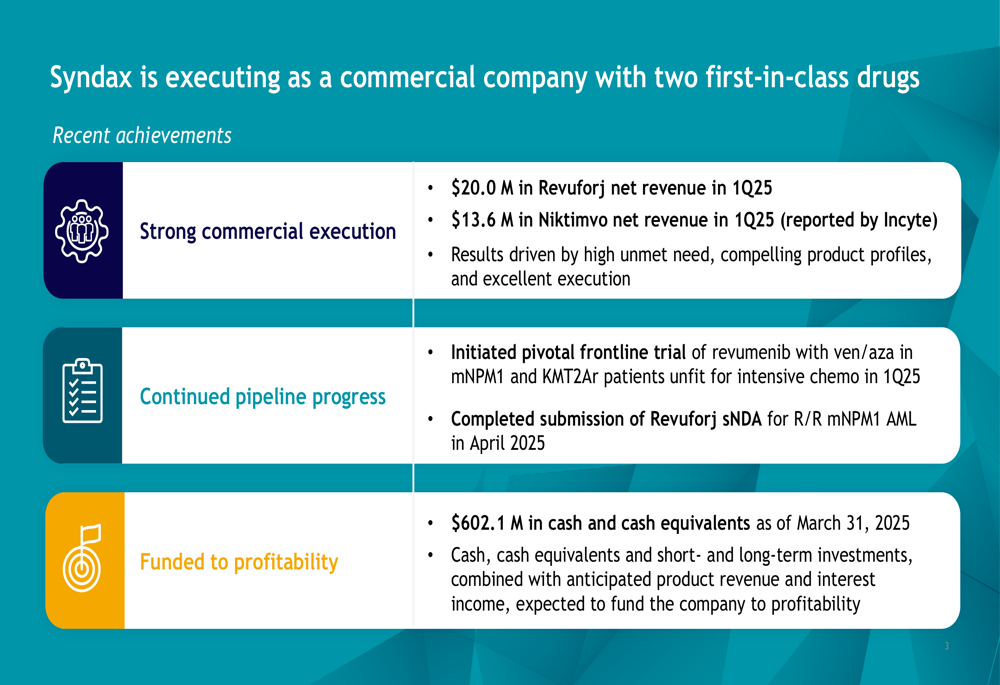

Syndax reported $20.0 million in net revenue from Revuforj for Q1 2025, representing substantial growth from the $7.7 million reported in Q4 2024, which only included five weeks of sales following FDA approval. The company highlighted several factors driving this performance, including a compelling product profile, expanding prescriber base, strong new patient starts, robust refill rates, and high payer approval rates.

As shown in the following revenue performance chart:

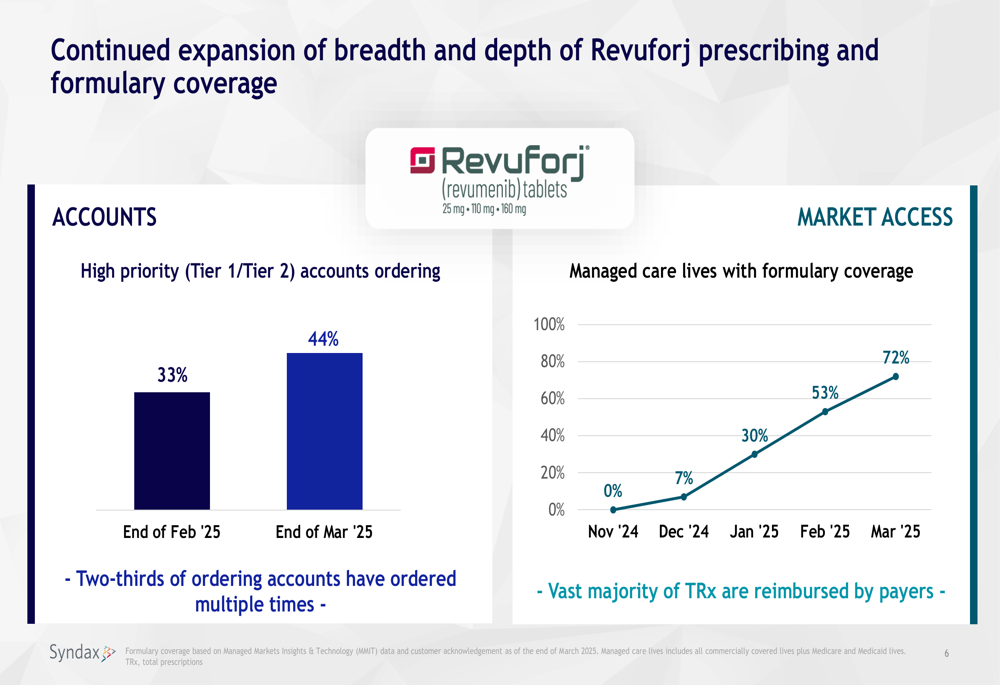

Market access for Revuforj has improved dramatically since launch, with 72% of managed care lives having formulary coverage by March 2025, up from 0% in November 2024. The company also reported that 44% of high-priority (Tier 1/Tier 2) accounts were ordering the product by the end of March, compared to 33% at the end of February.

The following chart illustrates this market access improvement:

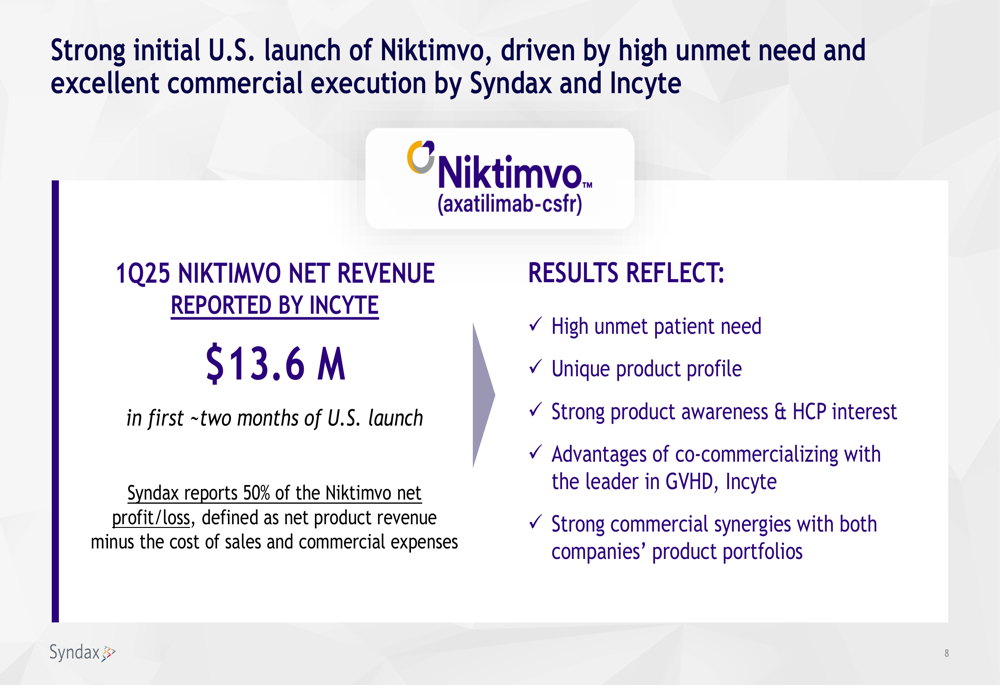

Syndax’s partner Incyte (NASDAQ:INCY) reported $13.6 million in net revenue for Niktimvo in Q1 2025, representing approximately two months of U.S. sales. Syndax receives 50% of the net profit/loss from Niktimvo sales. The company noted strong early adoption, with over 1,250 infusions year-to-date and approximately 95% of top accounts having placed orders.

The following slide details Niktimvo’s early commercial performance:

Detailed Financial Analysis

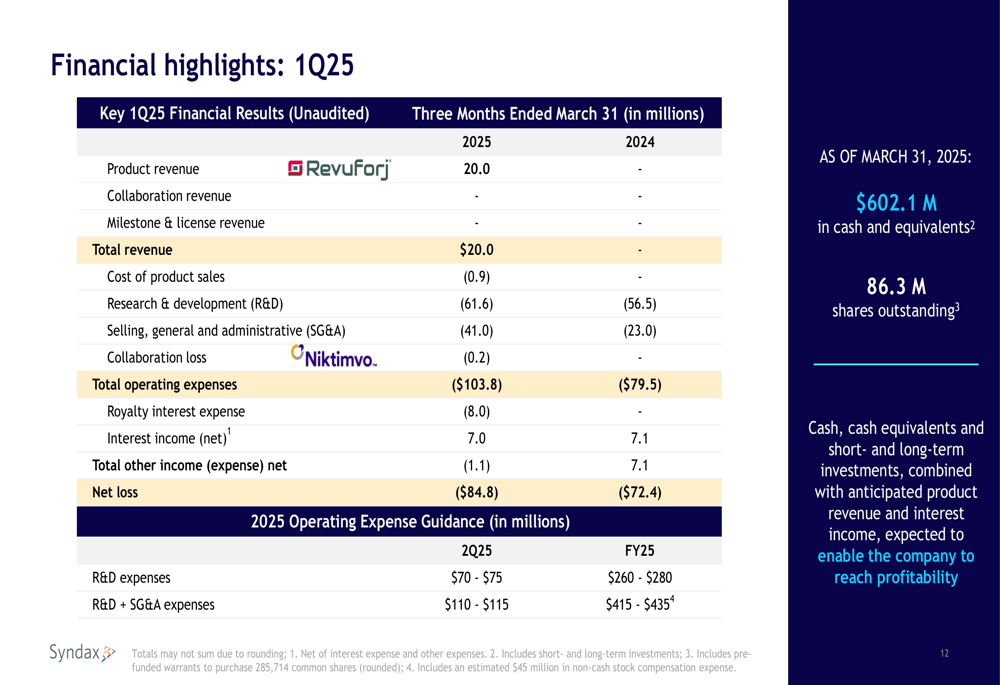

Syndax ended the quarter with $602.1 million in cash and cash equivalents as of March 31, 2025, a decrease from the $692.4 million reported at the end of Q4 2024, reflecting continued investment in commercial infrastructure and R&D. The company believes this cash position, combined with product revenue and interest income, will be sufficient to fund operations to profitability.

For Q1 2025, Syndax reported:

- Total (EPA:TTEF) revenue: $20.0 million

- Total operating expenses: $(103.8) million

- Net loss: $(84.8) million

- Shares outstanding: 86.3 million

The company provided 2025 operating expense guidance of $260-280 million for R&D expenses and total R&D plus SG&A expenses of $415-435 million.

The complete financial summary is shown in the following slide:

Despite the revenue growth, Syndax’s stock closed at $13.73 on May 5, 2025, down 1.46% for the day, though it gained 2.43% in after-hours trading to reach $13.90. This represents a significant discount from the 52-week high of $25.07, reflecting investor concerns about the path to profitability despite commercial progress.

Strategic Initiatives & Pipeline

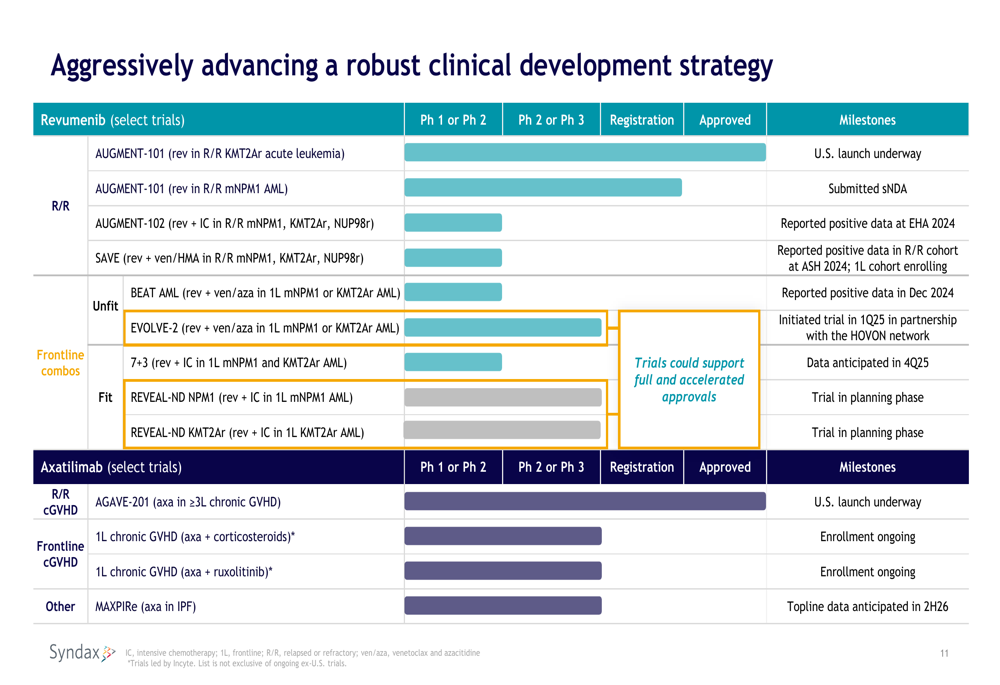

Syndax emphasized its "first mover" advantage with Revuforj as the first and only FDA-approved menin inhibitor. The company outlined a robust clinical development strategy for both products, with multiple trials underway or planned.

As shown in the comprehensive pipeline overview:

For Revuforj, Syndax completed submission of a supplemental New Drug Application (sNDA) for relapsed/refractory mNPM1 AML in April 2025 and initiated a pivotal frontline trial of revumenib with venetoclax/azacitidine in mNPM1 and KMT2Ar patients unfit for intensive chemotherapy in Q1 2025.

The company estimates the initial indication for Revuforj represents a ~$750 million U.S. market opportunity, addressing approximately 2,000 R/R acute leukemia patients with a KMT2A translocation. For Niktimvo, the initial indication represents a $1.5-$2.0 billion U.S. market opportunity, potentially addressing the ~6,500 currently treated 3L+ patients.

Forward-Looking Statements

Syndax outlined several key upcoming milestones for both products:

For Revuforj:

- Publication of pivotal R/R mNPM1 AML data

- Anticipated approval of sNDA for R/R mNPM1 AML

- Phase 1 data from frontline trial expected in Q4 2025

- Multiple frontline trials starting in 2H 2025

For Niktimvo:

- Continued U.S. adoption expansion

- Completion of enrollment in MAXPIRE Phase 2 IPF trial in 2025, with topline data expected in 2H 2026

The company highlighted its key achievements from Q1 2025 in this comprehensive summary:

While Syndax shows strong commercial execution with its dual product launches, the company continues to invest heavily in R&D and commercial infrastructure, resulting in substantial operating losses. Investors will be watching closely to see if revenue growth accelerates sufficiently to offset these expenses and move the company toward its stated goal of profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.