Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

Sysco Corporation (NYSE:SYY), the leading food distribution company in North America, presented its fiscal third-quarter 2025 results on April 29, 2025, revealing modest revenue growth but declining profits amid challenging market conditions. The company reported revenue of $19.6 billion, up 1.1% year-over-year, but missed analyst expectations of $20.12 billion. Adjusted earnings per share remained flat at $0.96, falling short of the anticipated $1.03.

Following the earnings release, Sysco’s stock experienced a slight decline in after-hours trading, with the share price dropping to $70.25, reflecting investor concerns about the company’s reduced full-year guidance and ongoing market challenges.

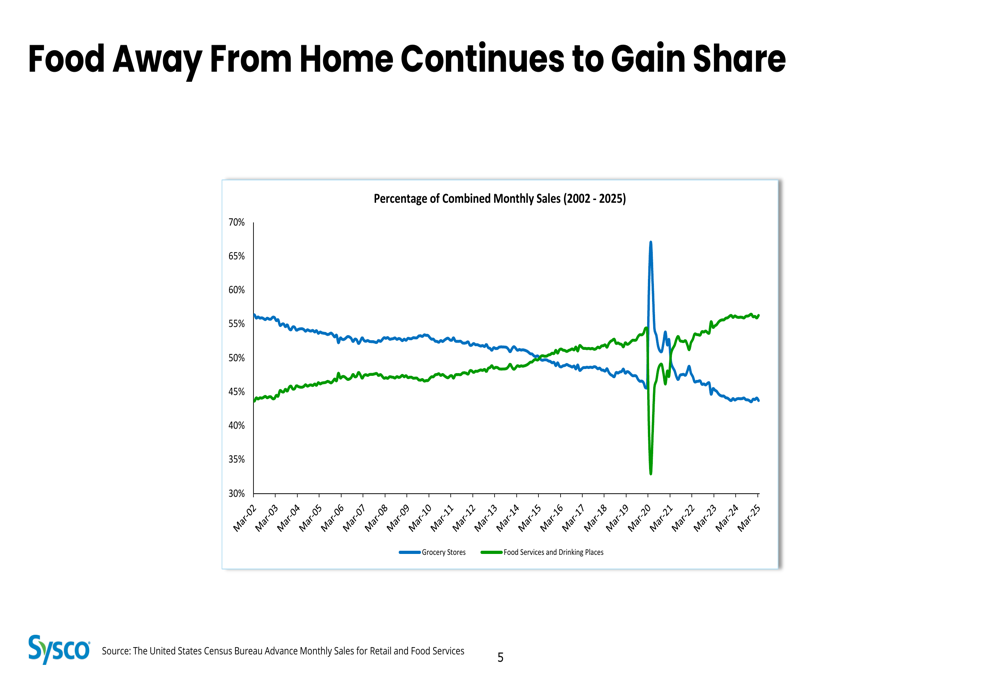

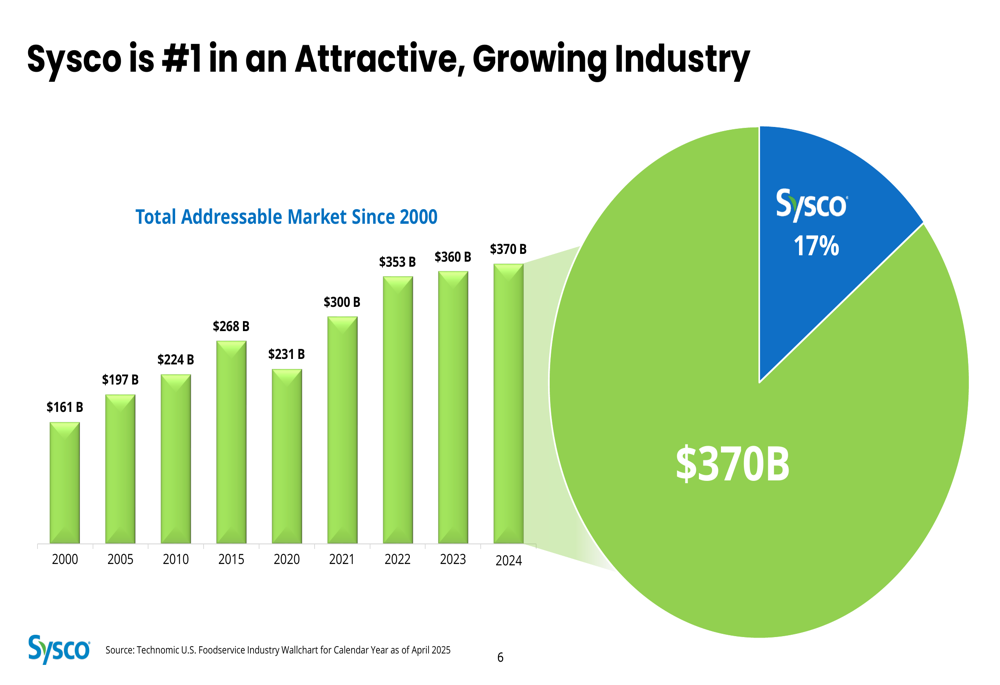

Despite these headwinds, Sysco maintains its dominant position in the foodservice distribution industry, holding a 17% share of the $370 billion market. The company continues to benefit from the long-term trend of food away from home gaining market share over grocery stores.

As shown in the following chart tracking the percentage of combined monthly sales for Grocery Stores versus Food Services and Drinking Places, the food away from home category has steadily gained market share over time, particularly since recovering from the pandemic:

Quarterly Performance Highlights

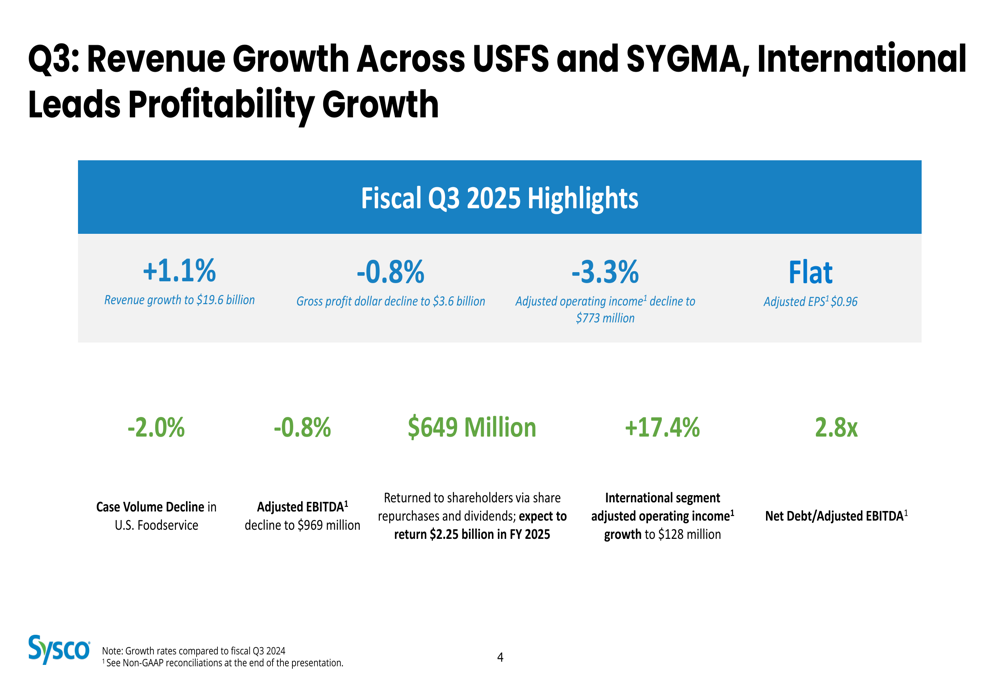

Sysco’s Q3 2025 financial results painted a mixed picture, with top-line growth offset by margin pressures and volume declines. The company delivered sales growth despite negative industry traffic trends, though adjusted EBITDA decreased 0.8% year-over-year to $969 million.

The following slide summarizes Sysco’s key financial metrics for the quarter:

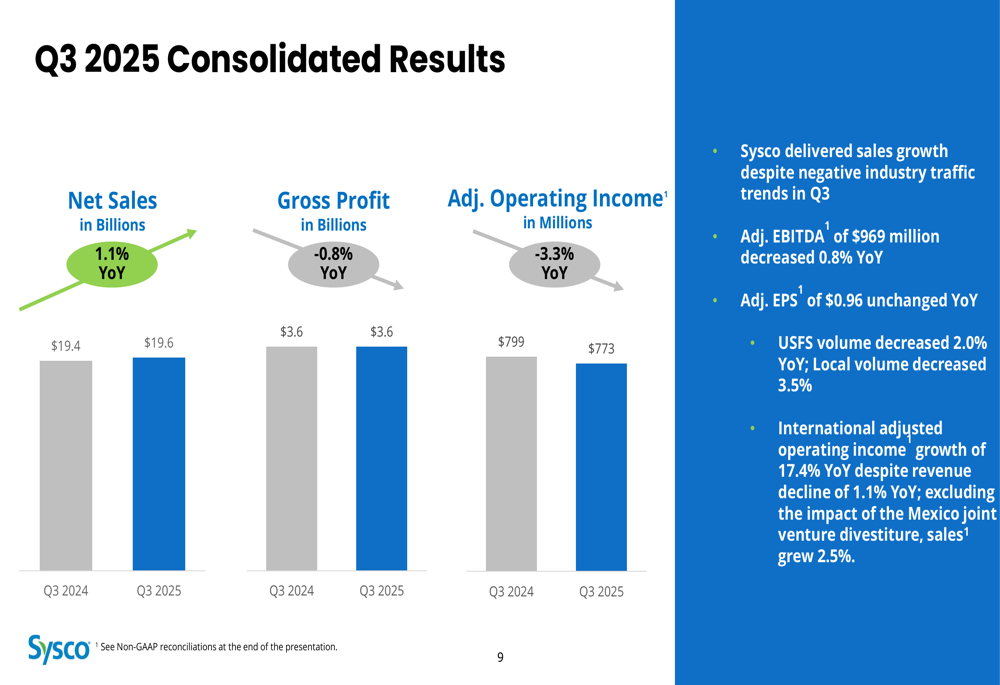

Breaking down the consolidated results further, we can see the specific performance metrics compared to the prior year:

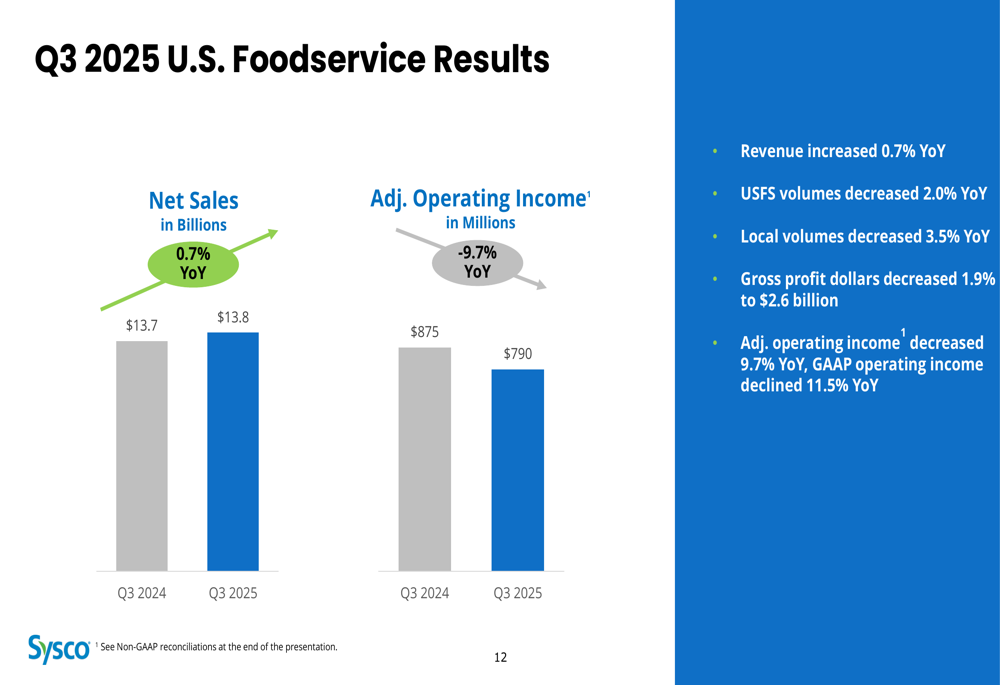

By segment, U.S. Foodservice operations, which represent the largest portion of Sysco’s business, faced significant challenges. While revenue increased 0.7% year-over-year to $13.8 billion, adjusted operating income decreased 9.7% to $790 million. U.S. Foodservice volumes decreased 2.0% year-over-year, with local volumes declining by 3.5%.

The following chart illustrates the U.S. Foodservice segment’s performance:

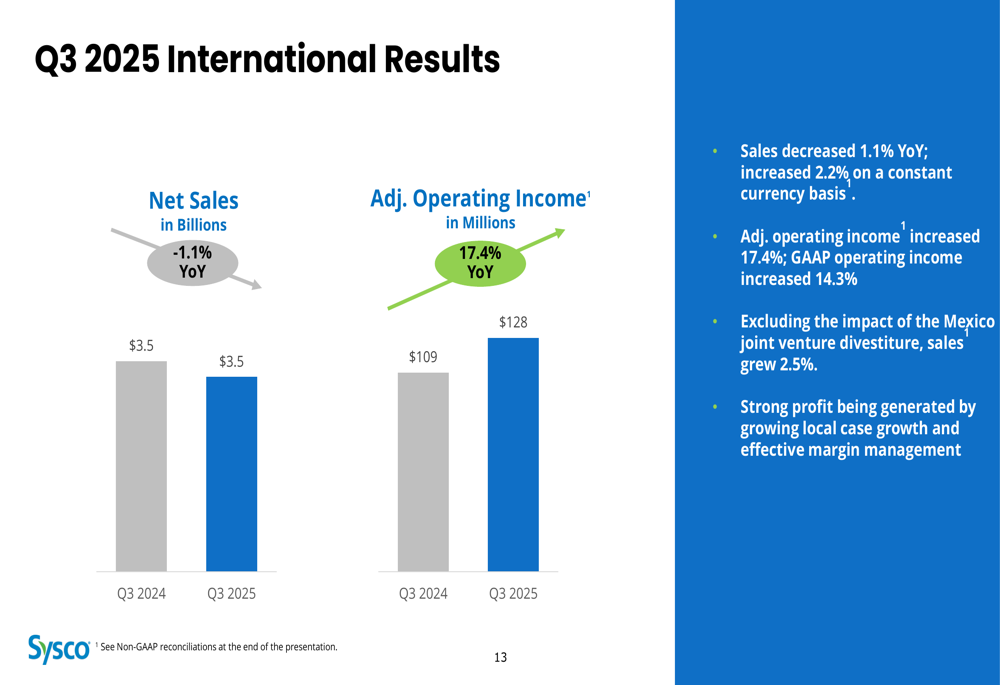

In contrast, Sysco’s International segment delivered strong profit growth despite a slight revenue decline. Adjusted operating income increased 17.4% year-over-year to $128 million, while sales decreased 1.1% to $3.5 billion. Excluding the impact of the Mexico joint venture divestiture, international sales grew 2.5%.

The company’s international performance is detailed in this slide:

The SYGMA segment, which focuses on chain restaurant customers, showed positive momentum with sales increasing 9.5% year-over-year to $2.1 billion, while operating income remained flat at $17 million. Management noted continued segment sales and volume growth after shifting the customer base to a more favorable mix.

Strategic Initiatives

Despite near-term challenges, Sysco continues to advance its long-term strategic initiatives. The company’s "Recipe for Growth" strategy focuses on five key areas: digital tools, products and solutions, supply chain efficiency, customer teams, and future horizons.

As illustrated in this strategic framework:

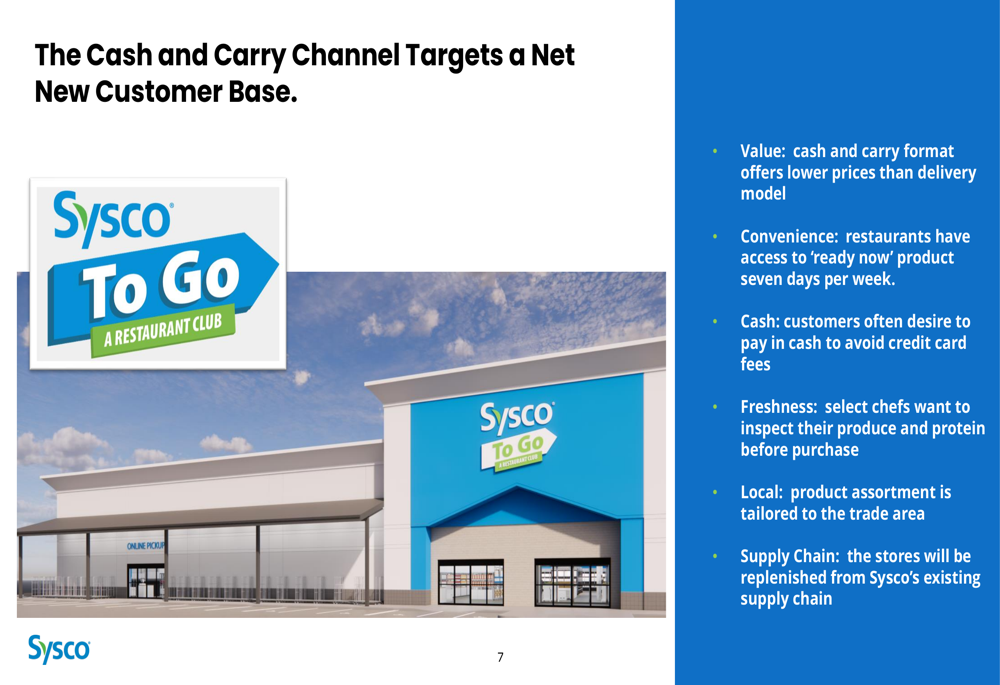

One of Sysco’s notable strategic initiatives is its expansion into the Cash and Carry channel with "Sysco To Go," which targets a new customer base. This format offers lower prices than the traditional delivery model and provides restaurants with convenient access to products seven days a week.

The following slide details this initiative:

Competitive Industry Position

Sysco maintains its leadership position in an attractive and growing industry. The company’s total addressable market has expanded significantly over the past two decades, growing from $161 billion in 2000 to $370 billion in 2024, despite a temporary setback during the pandemic.

This growth trajectory and Sysco’s market position are illustrated in the following chart:

The company’s strong balance sheet and investment-grade credit rating provide financial flexibility to navigate market challenges while continuing to invest in growth initiatives. Sysco ended the quarter with a net debt to adjusted EBITDA ratio of 2.8x, slightly above its target range of 2.5-2.75x.

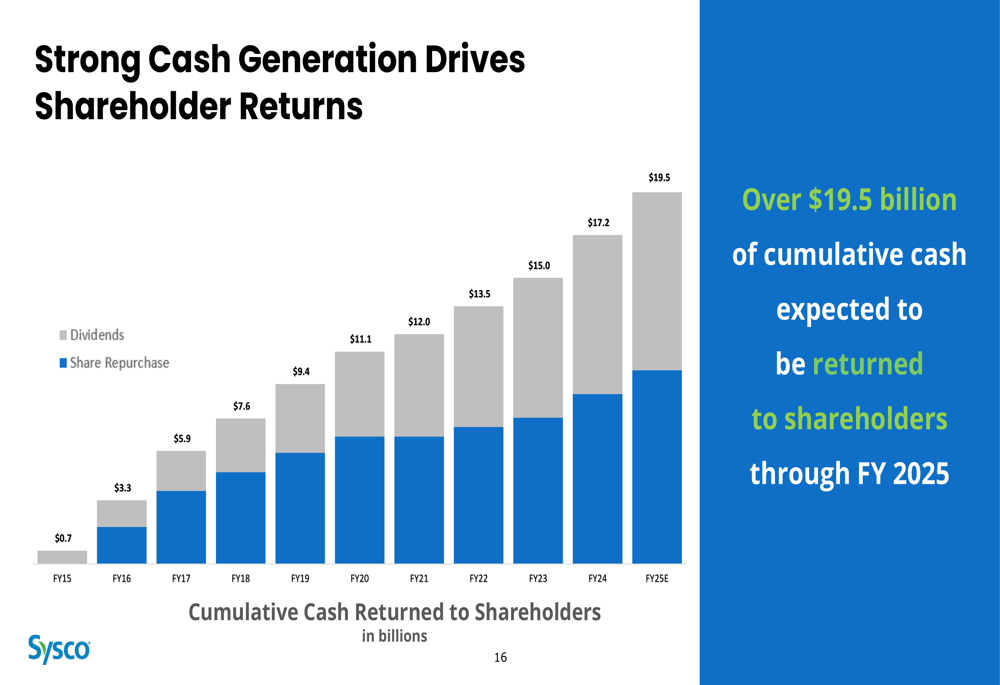

Sysco’s commitment to shareholder returns remains robust, with plans to return $2.25 billion to shareholders in fiscal year 2025 through dividends and share repurchases. The company has built an impressive track record of returning cash to shareholders, as shown in this cumulative chart:

Forward-Looking Statements

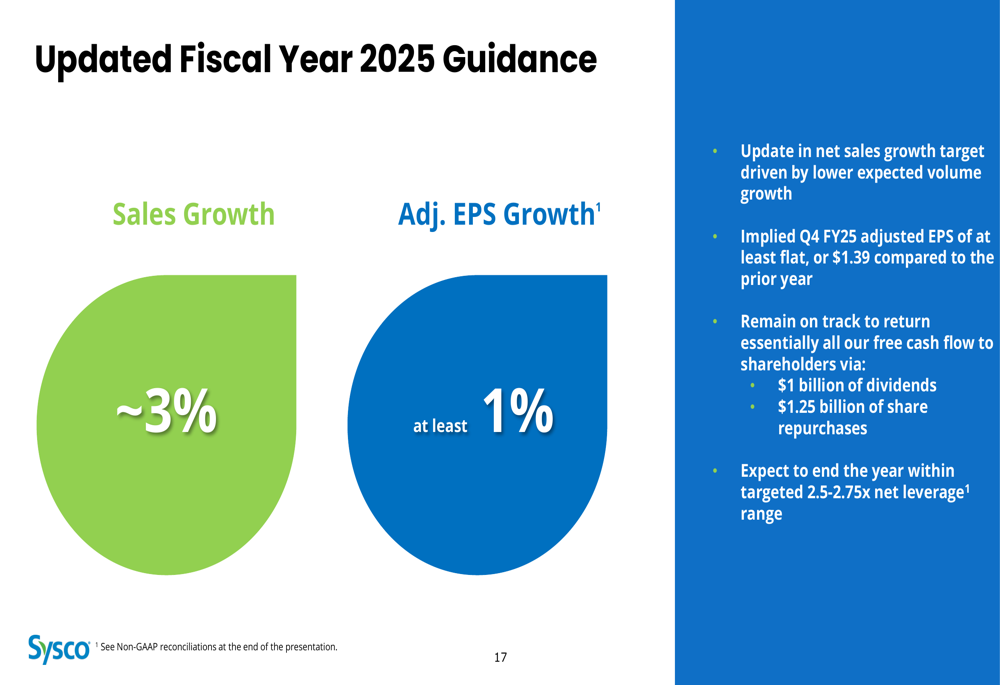

In response to the challenging operating environment, Sysco has revised its fiscal year 2025 guidance. The company now expects sales growth of approximately 3%, down from its previous target of 4-5%, driven by lower expected volume growth. Adjusted EPS growth is projected to be at least 1%.

The updated guidance is detailed in this slide:

For the fourth quarter of fiscal 2025, Sysco expects adjusted EPS to be at least flat compared to the prior year at $1.39. The company remains on track to return essentially all its free cash flow to shareholders via $1 billion of dividends and $1.25 billion of share repurchases.

During the earnings call, CEO Kevin Hourican acknowledged that "Q3 did not live up to our expectations on the top or bottom line," while expressing caution about tariff uncertainties and market volatility. However, he emphasized the company’s strong balance sheet and potential to return value to shareholders even in difficult times.

Despite the near-term challenges, Sysco’s management remains confident in the company’s long-term prospects, supported by its market leadership position, strategic initiatives, and the ongoing shift toward food away from home. The company expects to end the fiscal year within its targeted 2.5-2.75x net leverage range, maintaining financial flexibility for future growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.