Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

Talgo SA (BME:TLGO) presented its first half 2025 results on September 30, revealing a complex picture of financial challenges alongside significant commercial achievements. The Spanish train manufacturer’s shares closed at €2.76, down 1.44% on the day of the presentation, reflecting investor concerns about the company’s short-term financial performance despite promising long-term prospects.

The presentation highlighted Talgo’s efforts to strengthen its financial position while celebrating a record contract win from FlixTrain worth up to €2.4 billion, the largest in the company’s history. This juxtaposition of financial restructuring needs alongside commercial success characterizes Talgo’s current position in the competitive European rail manufacturing market.

Executive Summary

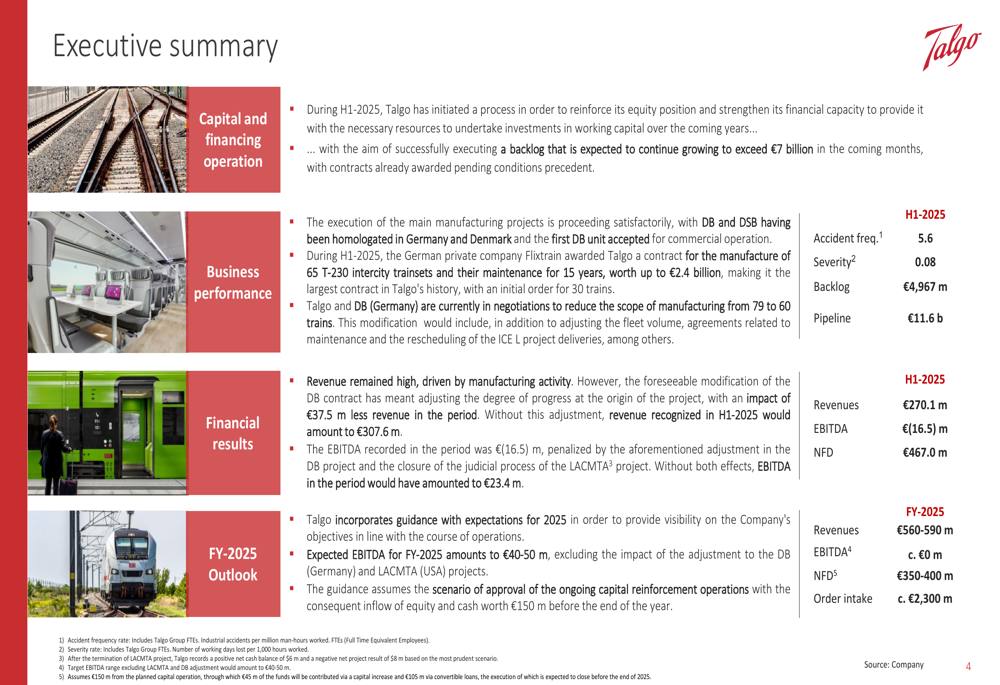

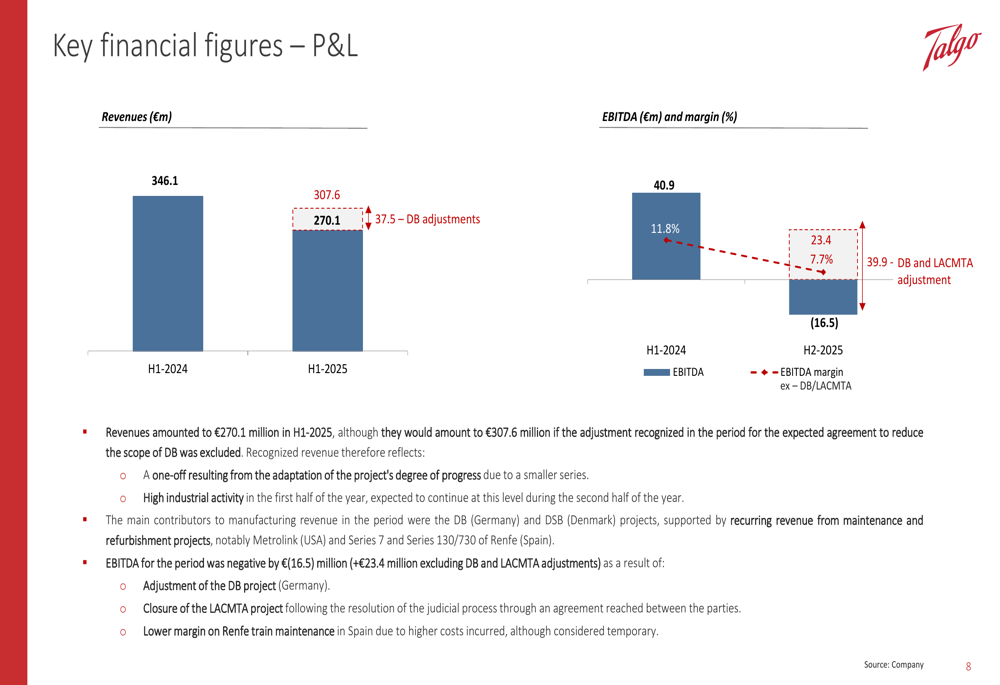

Talgo’s first half 2025 performance showed significant financial challenges, with revenue declining to €270.1 million from €346.1 million in H1 2024, and EBITDA turning negative at €(16.5) million compared to a positive €40.9 million in the prior-year period. The company attributed this decline primarily to adjustments in the Deutsche Bahn (DB) project volume.

As shown in the following executive summary from the presentation:

Despite these challenges, Talgo reported substantial commercial progress, including the successful homologation of its Talgo 230 trains in both Germany and Denmark, and most notably, the award of a contract from FlixTrain for up to 65 T-230 trainsets with maintenance for 15 years, valued at up to €2.4 billion.

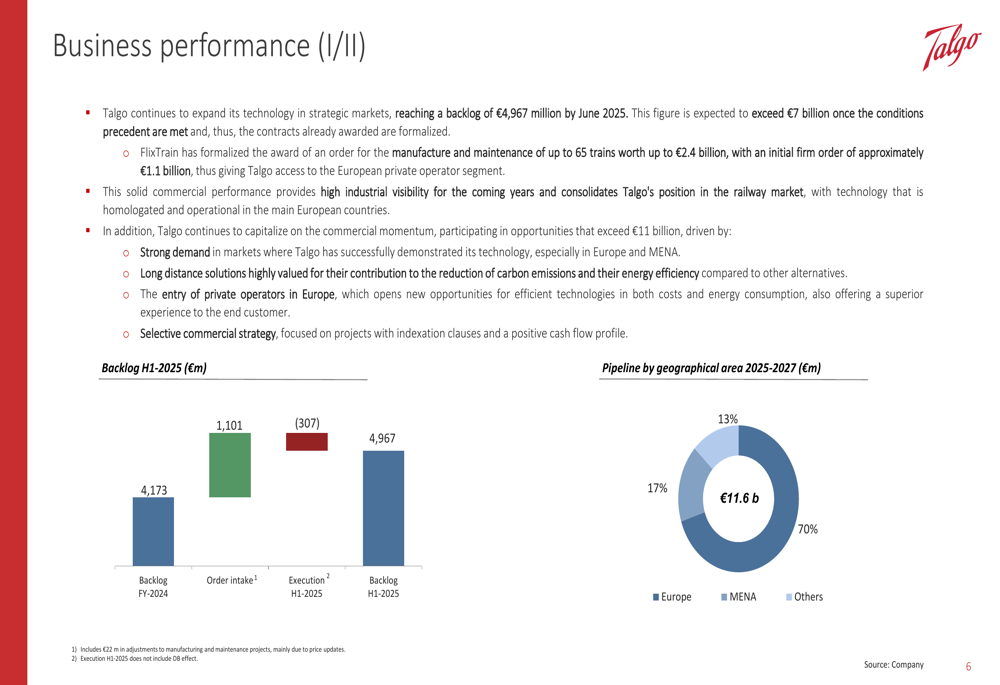

The company’s backlog reached €4,967 million by June 2025, with a pipeline of potential projects valued at €11.6 billion, providing a foundation for future growth despite current financial difficulties.

Financial Performance Analysis

Talgo’s financial performance in H1 2025 showed significant deterioration compared to the same period in 2024. Revenue decreased by 22% to €270.1 million, though the company noted that excluding a €37.5 million adjustment related to the DB project, revenue would have been €307.6 million.

The most concerning metric was EBITDA, which turned negative at €(16.5) million, compared to a positive €40.9 million (11.8% margin) in H1 2024. The company explained that excluding one-off adjustments related to the DB and LACMTA projects, EBITDA would have been €23.4 million with a 7.7% margin.

The following chart illustrates these key financial metrics:

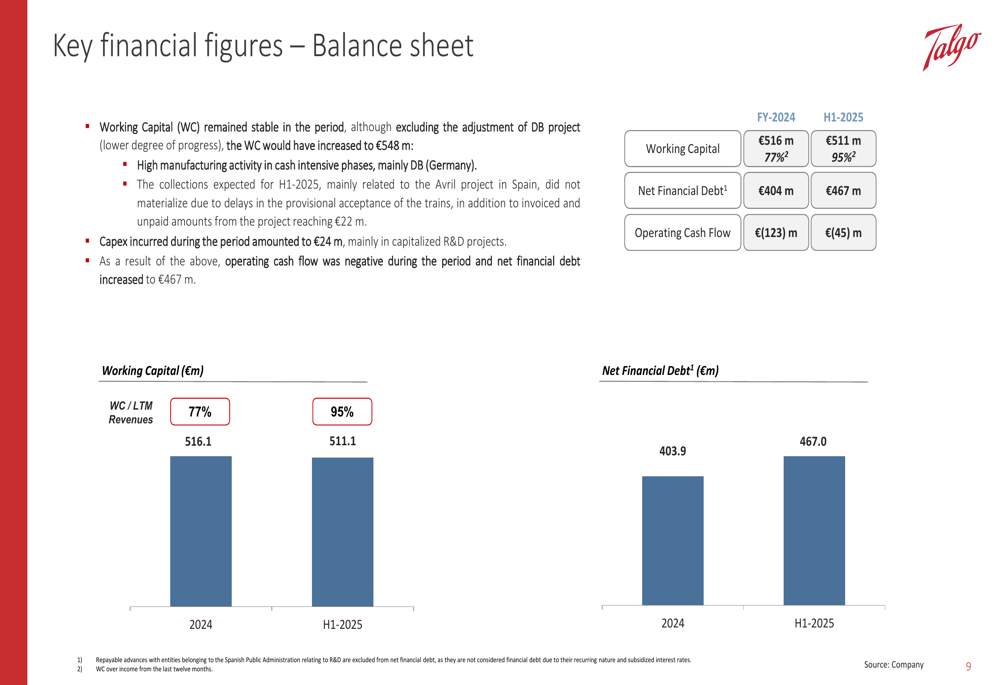

Working capital remained high at €511 million as of H1 2025, representing 95% of last twelve months’ revenue, compared to 77% at the end of 2024. This high working capital ratio reflects the capital-intensive nature of Talgo’s manufacturing projects and puts pressure on the company’s cash flow.

Net financial debt increased to €467 million from €404 million at the end of 2024, driven by negative operating cash flow of €(45) million in H1 2025, though this represented an improvement from €(123) million in 2024.

Capital Reinforcement Plans

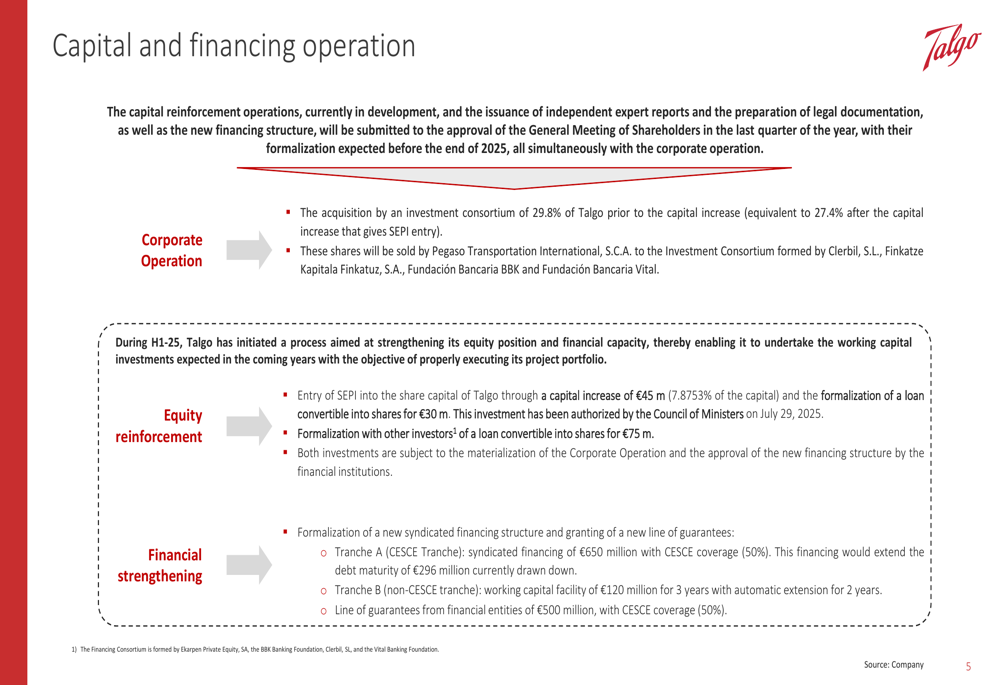

In response to these financial challenges, Talgo has initiated a comprehensive capital reinforcement plan. The company is structuring a significant financial operation involving both equity investment and debt restructuring.

The plan includes the acquisition of a 29.8% stake in Talgo by an investment consortium, followed by a capital increase. Additionally, SEPI (Spain’s state industrial holding company) will enter Talgo’s share capital with a €45 million investment and provide a €30 million loan convertible into shares, as authorized by the Spanish Council of Ministers on July 29, 2025.

As detailed in the following slide, the company is also formalizing a €75 million convertible loan with other investors and establishing a new syndicated financing structure:

The new financing structure includes a €650 million syndicated facility with 50% CESCE coverage (Spain’s export credit agency), a €120 million working capital facility, and a €500 million line of guarantees with 50% CESCE coverage. This comprehensive refinancing aims to provide Talgo with the financial stability needed to execute its growing backlog.

Order Intake and Backlog

Despite financial challenges, Talgo’s commercial performance has been robust. The company’s backlog reached €4,967 million by June 2025, up from €4,173 million at the end of 2024, driven by significant new orders.

The most notable commercial achievement was securing a contract from FlixTrain for the manufacture and maintenance of up to 65 trains worth up to €2.4 billion, with an initial firm order of approximately €1.1 billion. This represents the largest contract in Talgo’s history and significantly bolsters the company’s long-term outlook.

The following slide illustrates the evolution of Talgo’s backlog and its pipeline by geographical area:

Talgo’s pipeline of potential projects exceeds €11 billion, with 70% concentrated in Europe (€8.1 billion), 17% in the Middle East and North Africa (€2.0 billion), and 13% in other regions (€1.5 billion).

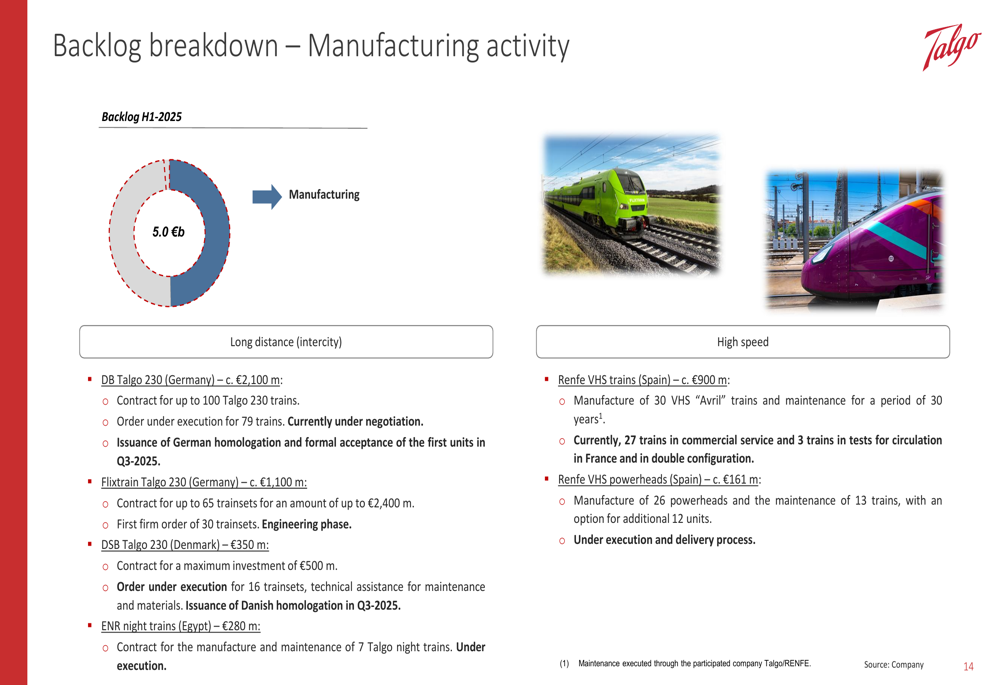

The company’s manufacturing portfolio consists primarily of projects based on the Talgo 230 platform, which received official certification to operate in both Germany and Denmark during the first half of 2025, marking an important milestone for Talgo’s European expansion strategy.

The breakdown of Talgo’s manufacturing backlog includes several major projects:

Forward-Looking Statements

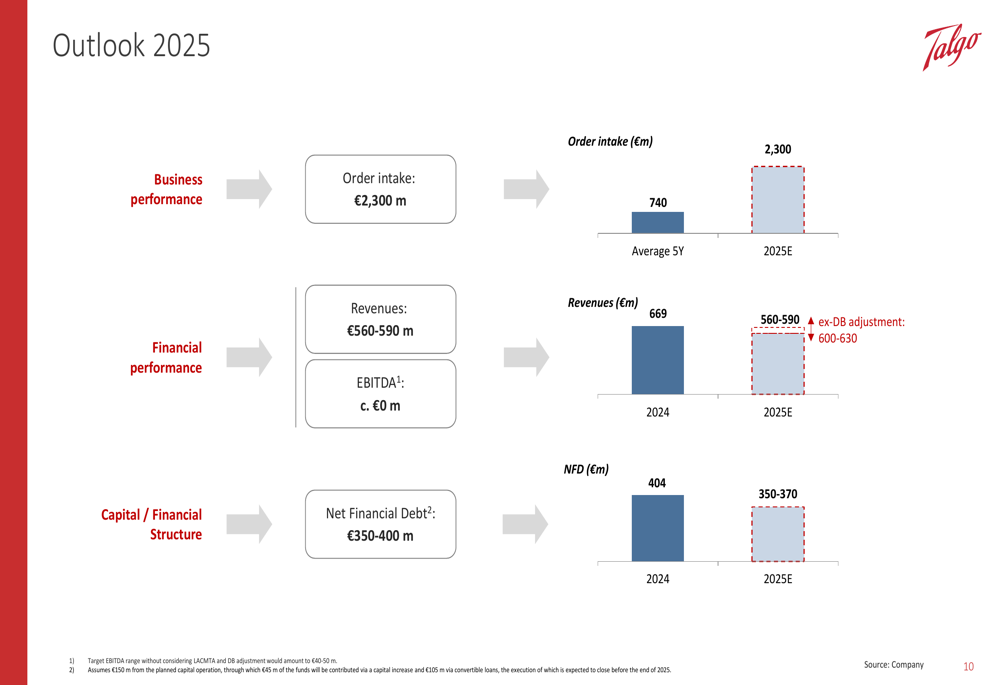

Looking ahead to the full year 2025, Talgo provided guidance that reflects both its current challenges and expected gradual recovery. The company expects revenue to reach €560-590 million for the full year, with EBITDA projected to break even at around €0 million.

Order intake is expected to be approximately €2,300 million for 2025, significantly above the five-year average of €740 million, driven by the FlixTrain contract. Net financial debt is projected to improve to €350-370 million by year-end, down from €467 million at the half-year mark.

The following outlook summary illustrates these projections:

Talgo’s management emphasized that the company is in a transition year, with financial performance expected to improve as the capital reinforcement plan is implemented and as execution of the growing backlog progresses. The successful homologation of the Talgo 230 platform in key European markets is expected to support future growth opportunities.

Conclusion

Talgo’s H1 2025 results presentation reveals a company at a pivotal juncture, facing significant short-term financial challenges while securing record orders that strengthen its long-term prospects. The capital reinforcement plan, including SEPI’s investment and the new syndicated financing structure, aims to provide the financial stability needed to execute on the company’s €5 billion backlog.

The record FlixTrain contract demonstrates market confidence in Talgo’s technology despite current financial difficulties. Investors will be closely watching whether the company can successfully implement its financial restructuring and return to profitability by the end of 2025 as projected.

With a substantial pipeline of potential projects and newly secured certifications for its Talgo 230 platform in key European markets, the company has laid the groundwork for potential recovery, though execution risks remain significant given the current negative EBITDA and high working capital requirements.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.