S&P 500 slips, but losses kept in check as Nvidia climbs ahead of results

Introduction & Market Context

Taylor Morrison Home Corp (NYSE:TMHC) released its second quarter 2025 investor presentation on July 23, showing modest revenue growth but declining margins and sales orders. The homebuilder’s stock declined 2.6% to $65.08 during trading, suggesting investors were concerned about the mixed results despite the company maintaining its full-year guidance.

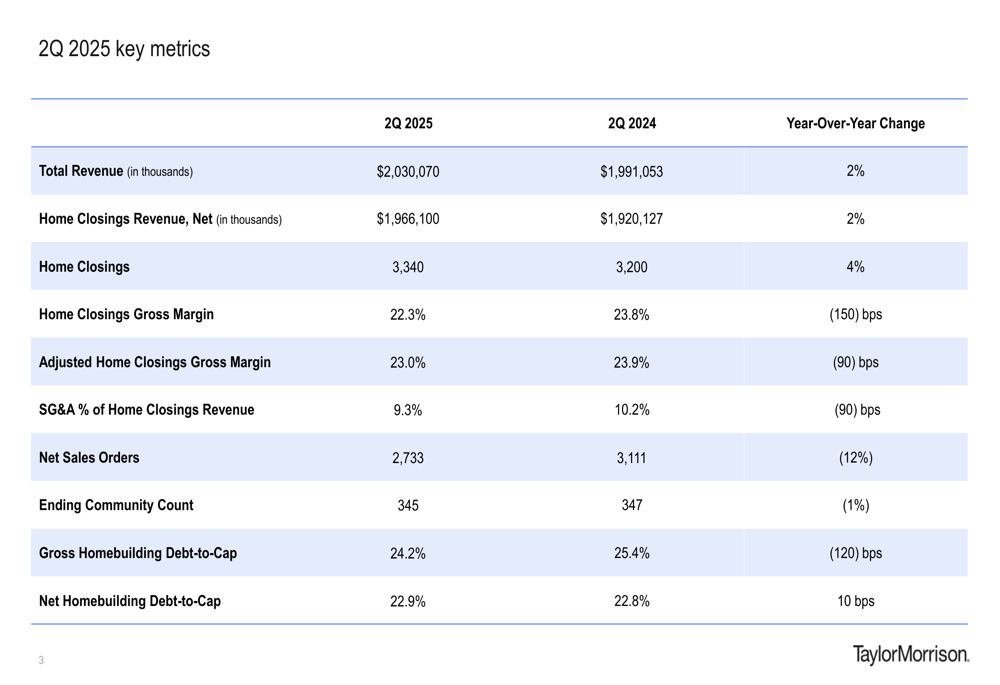

The presentation revealed total revenue of $2.03 billion, a 2% increase year-over-year, while home closings increased 4% to 3,340 units. However, net sales orders decreased 12% compared to the same period last year, indicating potential headwinds in the housing market.

As shown in the following comprehensive overview of Taylor Morrison’s current performance metrics:

Quarterly Performance Highlights

Taylor Morrison’s second quarter results showed resilience in some areas but pressure in others. Home closings revenue reached $1.97 billion, up 2% from Q2 2024, with an average closing price of $589,000. However, profitability metrics declined year-over-year, with home closings gross margin falling 150 basis points to 22.3% and adjusted home closings gross margin decreasing 90 basis points to 23.0%.

The company did show improvement in operational efficiency, with SG&A as a percentage of home closings revenue improving 90 basis points to 9.3%. The company maintained a strong financial position with total liquidity of $1.1 billion and a net homebuilding debt-to-capital ratio of 22.9%.

The detailed year-over-year comparison reveals both strengths and challenges in the company’s performance:

This performance represents a notable shift from Q1 2025, when Taylor Morrison reported a 25% year-over-year increase in adjusted EPS and an adjusted home closings gross margin of 24.8%, indicating sequential margin pressure as the year progresses.

Strategic Initiatives

Taylor Morrison continues to advance its land-lighter investment strategy, with controlled lots now representing 60% of its total homebuilding lot supply, up from 53% in Q4 2023. The company has 85,051 total homebuilding lots, representing 6.4 years of supply, with only 2.6 years of owned lot supply.

The company’s disciplined land investment approach is clearly illustrated in the following chart:

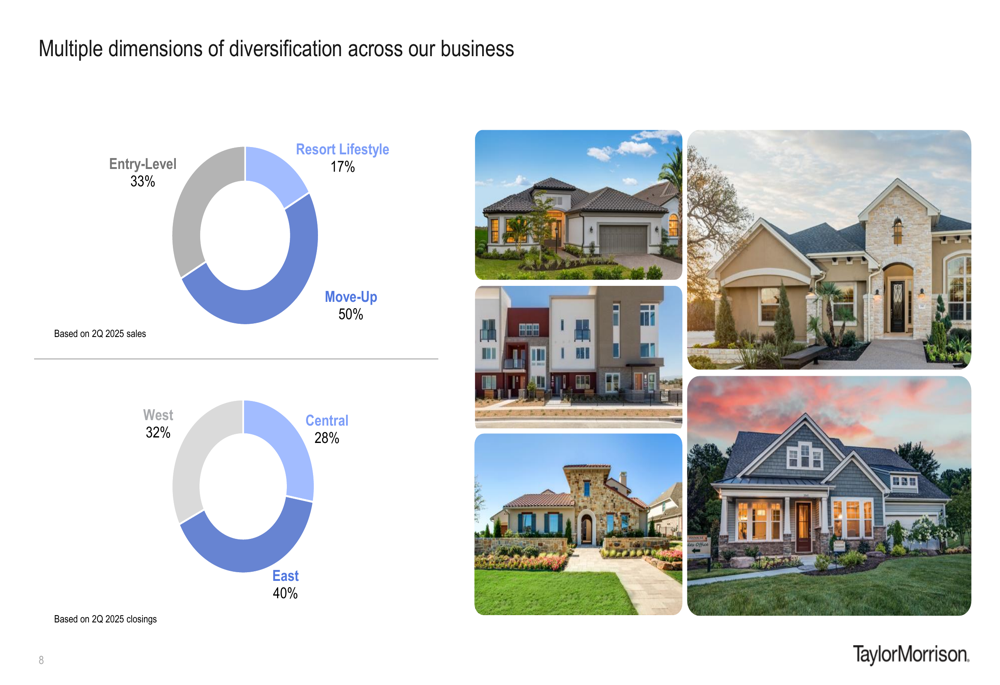

Taylor Morrison maintains a diversified business model across both product types and geography. Entry-level homes represent 33% of sales, while move-up homes account for 50% and resort lifestyle homes make up 17%. Geographically, the East region contributed 40% of closings in Q2 2025, followed by the West at 32% and Central at 28%.

The following chart illustrates this diversification strategy:

The company’s premium Esplanade brand continues to outperform the broader portfolio, with an average sales price of $779,000 (35% higher than other Taylor Morrison homes) and home closings gross margin of 31% (800 basis points higher). The brand also generates significantly higher option and lot premiums per home.

The Esplanade brand’s superior performance metrics are detailed here:

Taylor Morrison is also expanding its build-to-rent business through its Yardly brand, which now operates in 9 markets with approximately 40 owned and controlled communities. This initiative allows the company to diversify its revenue streams while leveraging its core homebuilding expertise.

Forward-Looking Statements

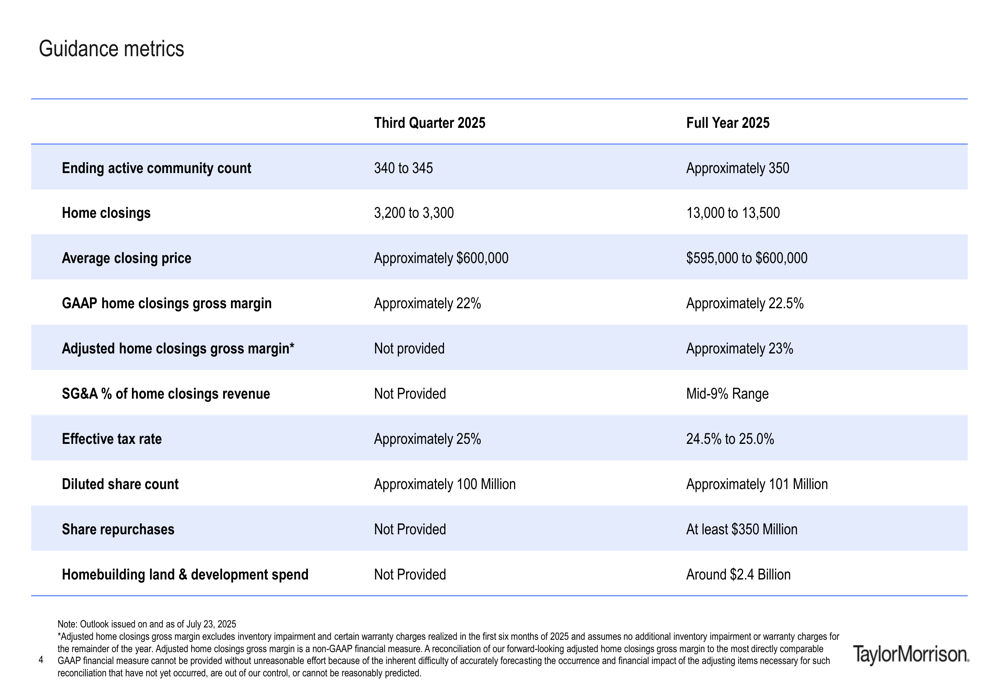

Despite the mixed Q2 results, Taylor Morrison maintained its full-year 2025 guidance, projecting 13,000 to 13,500 home closings with an average closing price of $595,000 to $600,000. For the third quarter, the company expects 3,200 to 3,300 home closings with an average closing price of approximately $600,000.

The company anticipates full-year GAAP home closings gross margin of approximately 22.5% and adjusted home closings gross margin of approximately 23%. SG&A as a percentage of home closings revenue is expected to remain in the mid-9% range for the full year.

Taylor Morrison also reaffirmed its commitment to return capital to shareholders, with plans to repurchase at least $350 million of common stock in 2025, of which $235 million was completed in the first half of the year.

The detailed guidance metrics for both Q3 and full-year 2025 are presented here:

Competitive Industry Position

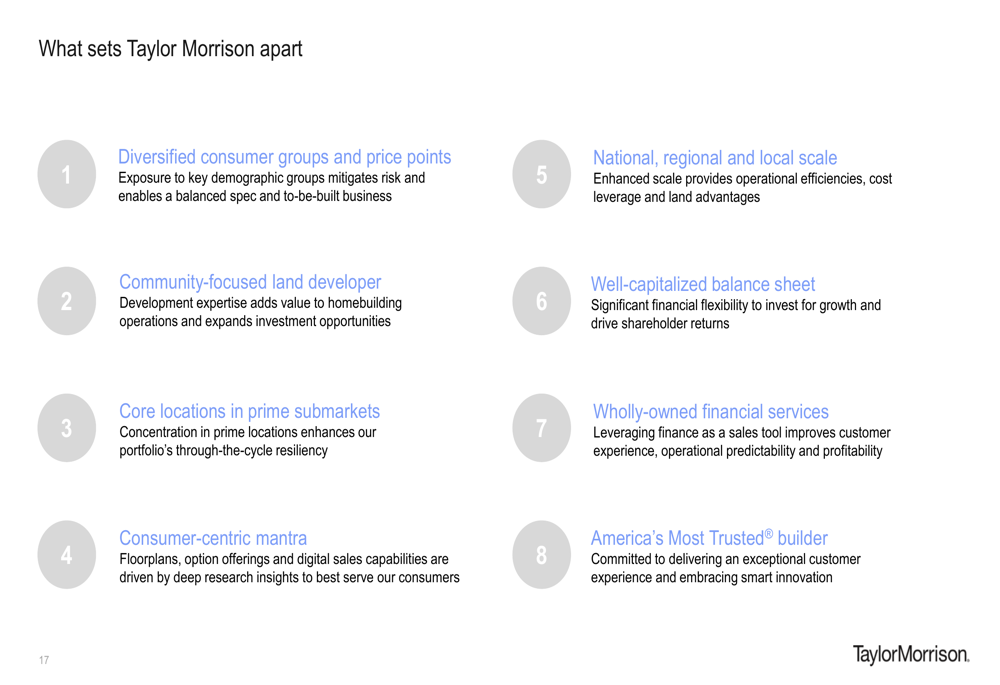

Taylor Morrison highlights several key differentiators that position it competitively in the homebuilding industry. These include its diversified consumer groups and price points, community-focused land development expertise, prime location strategy, consumer-centric approach, and scale advantages.

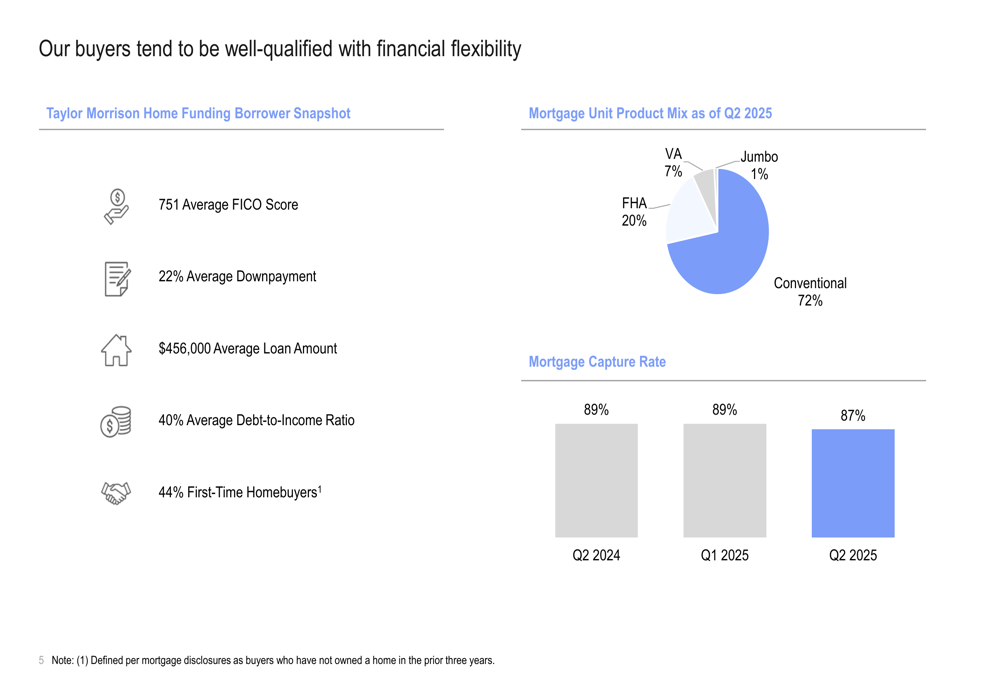

The company’s wholly-owned financial services segment continues to perform well, with a mortgage capture rate of 87% in Q2 2025. The average FICO score of Taylor Morrison Home Funding borrowers was 751, with an average down payment of 22% and an average loan amount of $456,000.

The mortgage data provides insight into the company’s buyer profile:

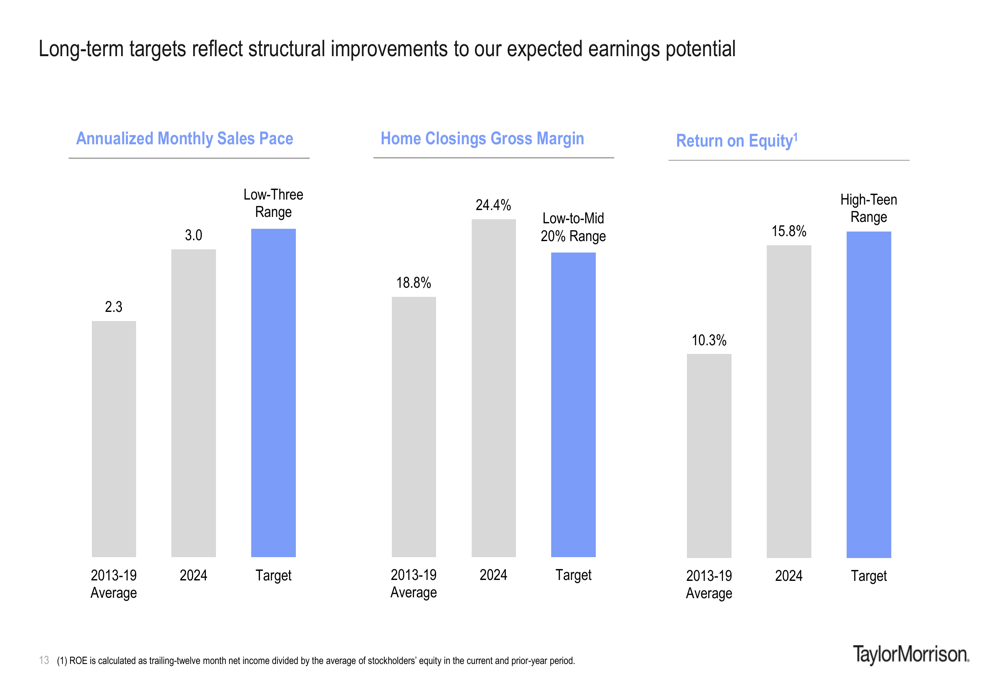

Looking ahead, Taylor Morrison has established ambitious long-term financial targets, aiming for an annualized monthly sales pace in the low-three range, home closings gross margin in the low-to-mid 20% range, and return on equity in the high-teen range. These targets represent significant improvements over the company’s 2013-2019 historical averages.

The company’s long-term financial targets are illustrated in the following chart:

Taylor Morrison’s key competitive differentiators are comprehensively outlined here:

Taylor Morrison’s presentation demonstrates the company’s resilience amid challenging market conditions, with its diversified business model and land-lighter strategy providing flexibility. While Q2 2025 showed some pressure on margins and sales orders, the company remains confident in its full-year outlook and long-term strategic positioning in the homebuilding industry.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.