Gevo shares jump as Q3 results top estimates, posts positive EBITDA

Introduction & Market Context

Telefónica SA (NYSE:TEF) presented its Q2 2025 results on July 30, showcasing organic growth acceleration despite reported revenue declines affected by foreign exchange impacts. The Spanish telecommunications giant highlighted its strategic transformation, particularly the accelerated disposal of Hispam assets, while emphasizing strong performance in its core markets of Spain and Brazil.

The company’s stock has been under pressure, falling 1.56% in regular trading to $5.13, with aftermarket activity showing further declines of 2.92% to $4.98, suggesting investors may have concerns despite the company’s positive framing of results.

Executive Summary

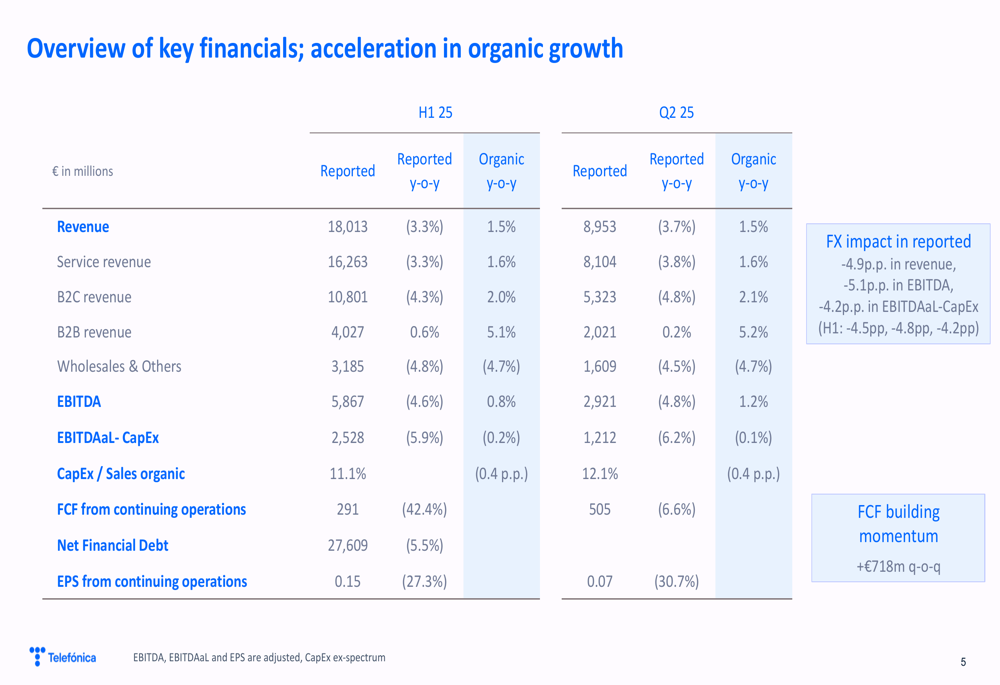

Telefónica reported Q2 2025 revenue of €8.95 billion, representing a 3.7% decline in reported terms but a 1.5% increase in organic terms when adjusting for currency effects. EBITDA followed a similar pattern, declining 4.8% as reported but growing 1.2% organically. The company maintained its full-year guidance across all metrics and confirmed its €0.30 dividend per share commitment.

The quarter was marked by accelerated portfolio transformation in Hispam, with five transactions totaling approximately €3 billion in firm value. Spain and Brazil emerged as standout performers, together contributing 72% to group EBITDA growth, while Germany faced challenges from the migration of 1&1 customers.

As shown in the following overview of Telefónica’s key financials, the company achieved organic growth across major metrics despite negative reported figures:

Quarterly Performance Highlights

Telefónica’s customer base grew to 348.6 million, adding 1.9 million customers quarter-over-quarter. The company continued to expand its next-generation networks, with fiber reaching 81.4 million premises passed (up 1.5 million quarter-over-quarter) and 5G coverage expanding to 77% in core markets.

Free cash flow from continuing operations reached €505 million in Q2, representing a significant improvement of €718 million compared to Q1, although it declined 6.6% year-over-year. Net financial debt stood at €27.6 billion, down 5.5% compared to the previous year.

The following chart illustrates Telefónica’s accelerated transformation of its Hispam portfolio, with completed sales in Argentina and Peru, and signed agreements for Colombia, Uruguay, and Ecuador:

The company’s underlying performance varied significantly across markets, with Spain and Brazil showing strong results while Germany and VMO2 faced more challenging conditions:

Market-by-Market Analysis

Spain

Telefónica’s home market delivered its best quarter for net additions since Q3 2018, with year-over-year growth accelerating across all access types. The company reinforced its competitive position by upgrading its Movistar and O2 portfolios and implementing a new customer attention plan called "Movistar por ti." EBITDAAL grew 1.2% year-over-year, improving 0.2 percentage points quarter-over-quarter.

The following slide details Spain’s performance, highlighting growth in customers and financial metrics:

Brazil

Brazil emerged as a standout performer with the strongest EBITDA growth since Q4 2023 at 8.6%. The operation maintained clear market leadership with 43% share in postpaid and 18% in FTTH. Revenue growth exceeded inflation, with mobile service revenue up 7.3% and fixed revenue increasing 7.9%. The company also announced the acquisition of CDPQ’s 50% stake in FiBrasil for BRL850 million.

The following chart shows Brazil’s impressive growth in high-value accesses and accelerating financial performance:

Germany

Telefónica Deutschland faced challenges from the migration of 1&1 customers but reported robust mobile trading with contract net adds increasing 12.1% quarter-over-quarter. The operation achieved approximately 98% 5G coverage and maintained stable O₂ churn at 0.9%. However, partner business transformation negatively impacted financial results.

The following slide illustrates Germany’s focus on mitigating the effect of 1&1 migration:

VMO2

The UK joint venture VMO2 showed improved contract churn at 1.1% and consumer fixed ARPU growth of £1.5 quarter-over-quarter. Revenue decline was impacted by price rise phasing, handset softness, and lower nexfibre construction. However, EBITDA trends improved due to cost efficiencies. The company also acquired spectrum to strengthen its mobile position, pending regulatory approval.

The following chart details VMO2’s focus on value over volume:

Financial Position and Outlook

Telefónica maintained a solid balance sheet with liquidity of €18.7 billion and an average debt life of 10.9 years. The company reduced its interest cost to 3.30% from 3.64% in June 2024. While net financial debt increased slightly to €27.6 billion, the company expects this to decrease to approximately €26 billion following the closing of pending transactions.

The following slide illustrates Telefónica’s FCF improvement and balance sheet position:

For 2025, Telefónica confirmed its guidance of organic revenue growth, EBITDA growth, and a CapEx to sales ratio below 12.5%. The company also reiterated its dividend commitment of €0.30 per share, to be paid in two installments of €0.15 each in December 2025 and June 2026.

Strategic Initiatives

Telefónica emphasized four guiding principles for its transformation: putting customers at the core, focusing on technology and operational excellence, maintaining disciplined industrial rationale, and creating value for all stakeholders. The company also highlighted its strategic priorities of Europe and leadership in Brazil.

A strategic review is progressing on schedule and is expected to be unveiled in the second half of 2025. This review will likely provide further clarity on the company’s long-term vision and strategic direction.

In sustainability, Telefónica was named the second Most Sustainable Company of 2025 by TIME and Statista, reflecting its commitment to environmental, social, and governance initiatives. The company published an updated Climate Action Plan and was recognized as a CDP Supplier Engagement Leader for the sixth consecutive year.

As Telefónica navigates its transformation journey, the company faces both opportunities and challenges. While core markets like Spain and Brazil continue to deliver strong results, the company must address ongoing challenges in Germany and the UK while completing its strategic exit from Hispam. The upcoming strategic review will be crucial in defining Telefónica’s path forward in an increasingly competitive telecommunications landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.