Gold prices dip as hawkish Fed minutes weigh ahead of Jackson Hole

Telefonica (BME:TEF) SA ADR (NYSE:TEF) presented its second quarter 2025 results on July 30, showing organic revenue growth despite reported declines, as the company continues to execute its strategic transformation with a focus on Europe and Brazil while accelerating its exit from Hispam markets.

Executive Summary

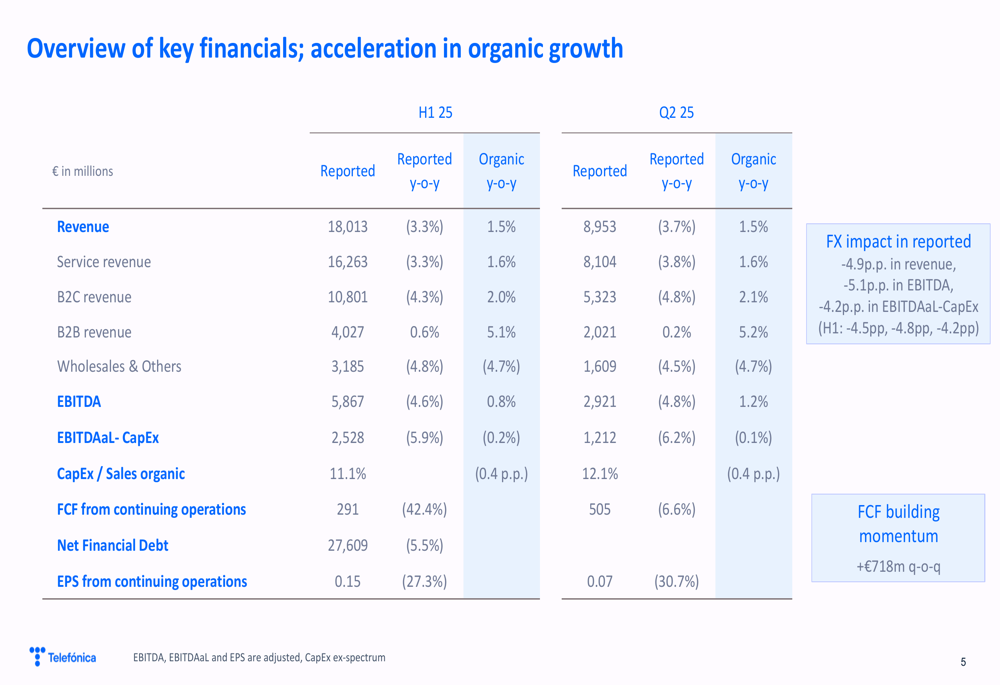

Telefonica reported Q2 2025 revenue of €8,953 million, representing a 3.7% year-over-year decline in reported terms but a 1.5% increase on an organic basis. Similarly, EBITDA reached €2,921 million, down 4.8% as reported but up 1.2% organically. The company maintained its full-year 2025 guidance and confirmed its €0.30 dividend per share.

"We are delivering another solid quarter and building Telefónica’s next chapter," said Marc Murtra, Chairman & CEO, highlighting the company’s dual focus on executing today while building for tomorrow.

The telecommunications giant continues to make progress on its strategic transformation, guided by four key principles: customer focus, technological excellence, disciplined industrial approach, and value creation for all stakeholders. A strategic review is on track for unveiling in the second half of 2025.

Quarterly Performance Highlights

Telefonica’s customer base grew to 348.6 million, adding 1.9 million customers quarter-over-quarter. The company expanded its fiber network to 81.4 million premises passed (adding 1.5 million in the quarter) and increased 5G coverage to 77% in core markets.

As shown in the following financial performance overview:

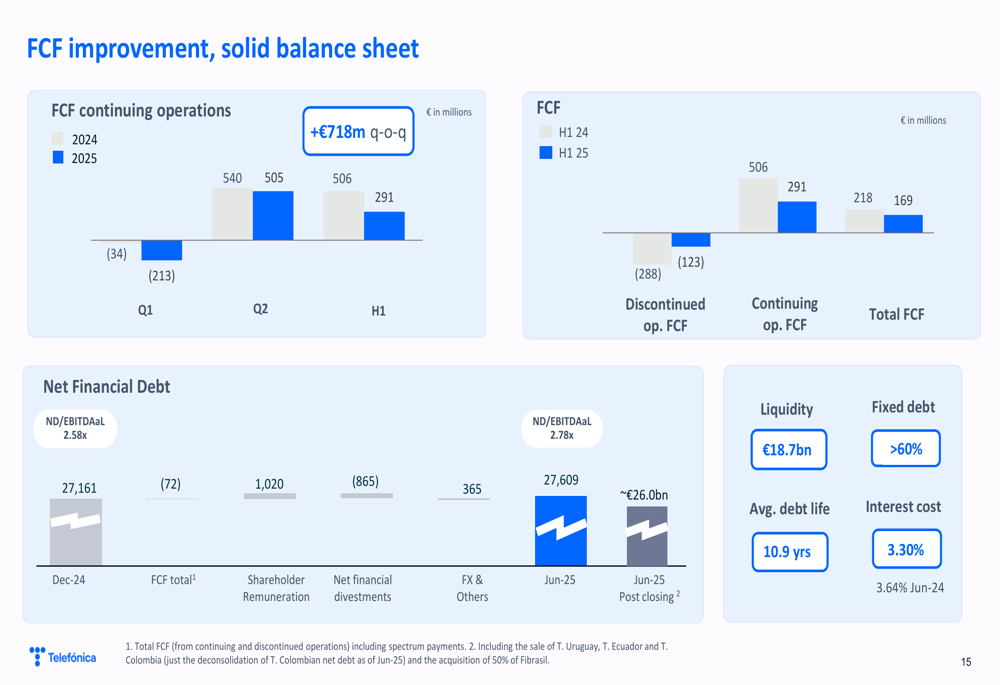

Free cash flow from continuing operations showed significant improvement, increasing by €718 million quarter-over-quarter to reach €505 million in Q2, though this still represents a 6.6% decline year-over-year. The company’s net financial debt stood at €27,609 million, down 5.5%.

"FCF building momentum" was highlighted as a key achievement, with the company maintaining a solid balance sheet featuring €18.7 billion in liquidity, over 60% fixed debt, an average debt life of 10.9 years, and an interest cost of 3.30%.

Strategic Initiatives

The most significant strategic development has been Telefonica’s accelerated portfolio transformation in Hispam, with five transactions totaling approximately €3 billion in firm value. These include:

- Sale of Telefonica Argentina (€1.2 billion), with simultaneous signing and closing executed

- Binding agreement for Telefonica Colombia (~€368 million), pending closing

- Sale of Telefonica Peru, with simultaneous signing and closing executed

- Binding agreement for the sale of Telefonica Uruguay (firm value ~€389 million), pending closing

- Binding agreement for the sale of Telefonica Ecuador (firm value ~€330 million), pending closing

The following slide details the company’s progress in exiting Hispam markets:

These disposals align with Telefonica’s stated strategic priorities of focusing on Europe and leadership in Brazil, while maintaining "strict financial discipline" as the company undergoes its transformation.

Regional Performance

Telefonica’s performance varied significantly across its key markets:

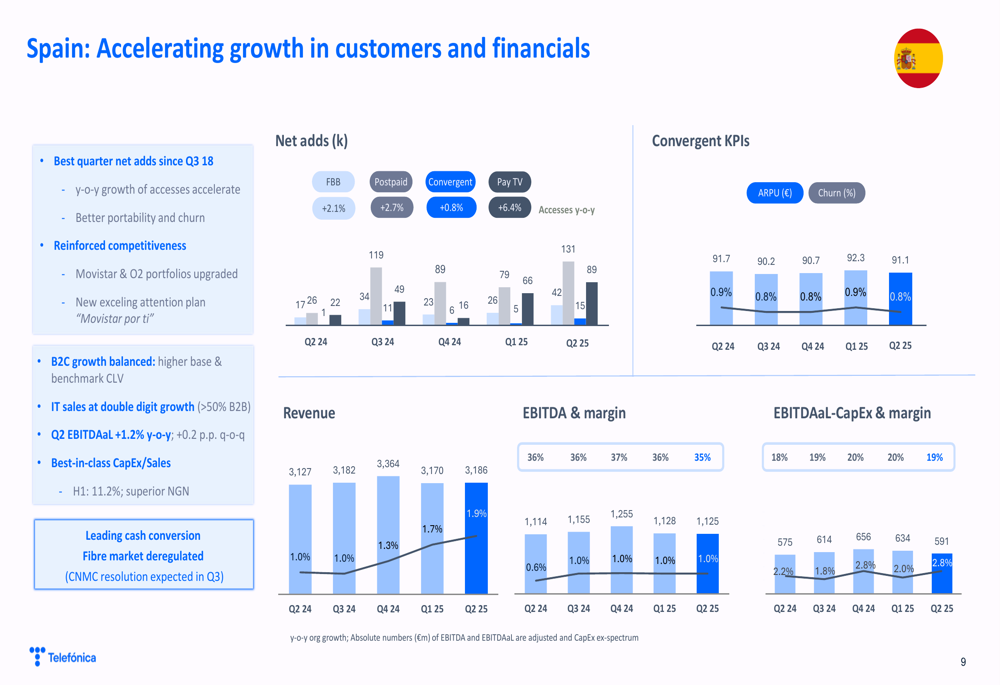

In Spain, the company reported its best quarter for net adds since Q3 2018, with service revenue and EBITDA both growing by 1.0%. EBITDA-CapEx improved by 2.8% year-over-year. IT sales showed double-digit growth, with over 50% coming from B2B segments.

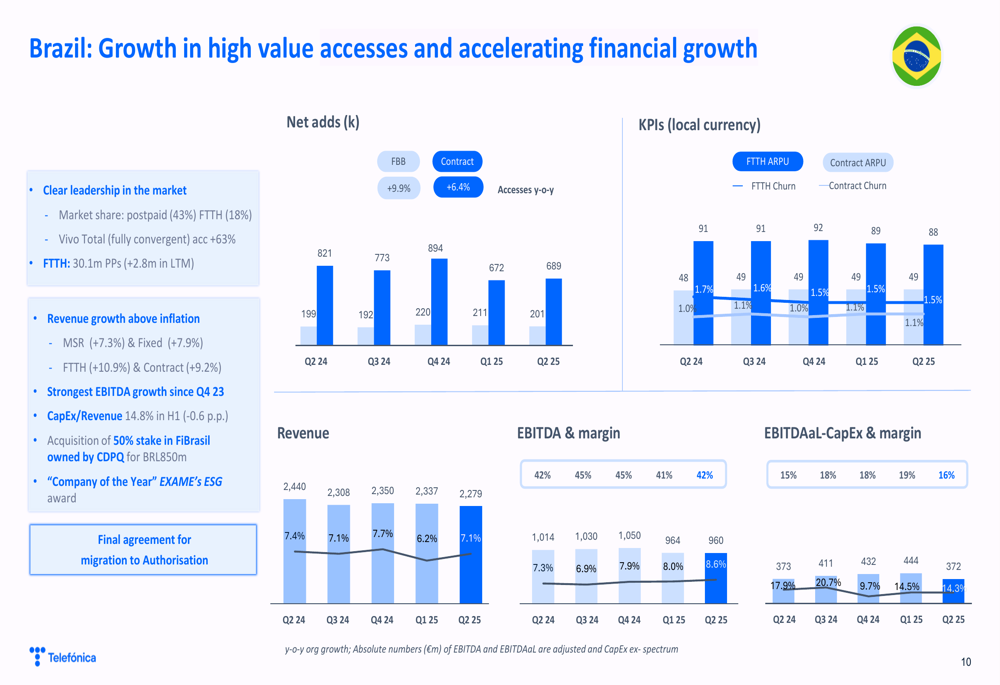

Brazil emerged as a standout performer, with record EBITDA growth of 8.6% since Q4 2023 and a robust EBITDA-CapEx margin of 16.3% (up 1.0 percentage points). The company maintained clear market leadership and expanded its fiber network to 30.1 million premises passed.

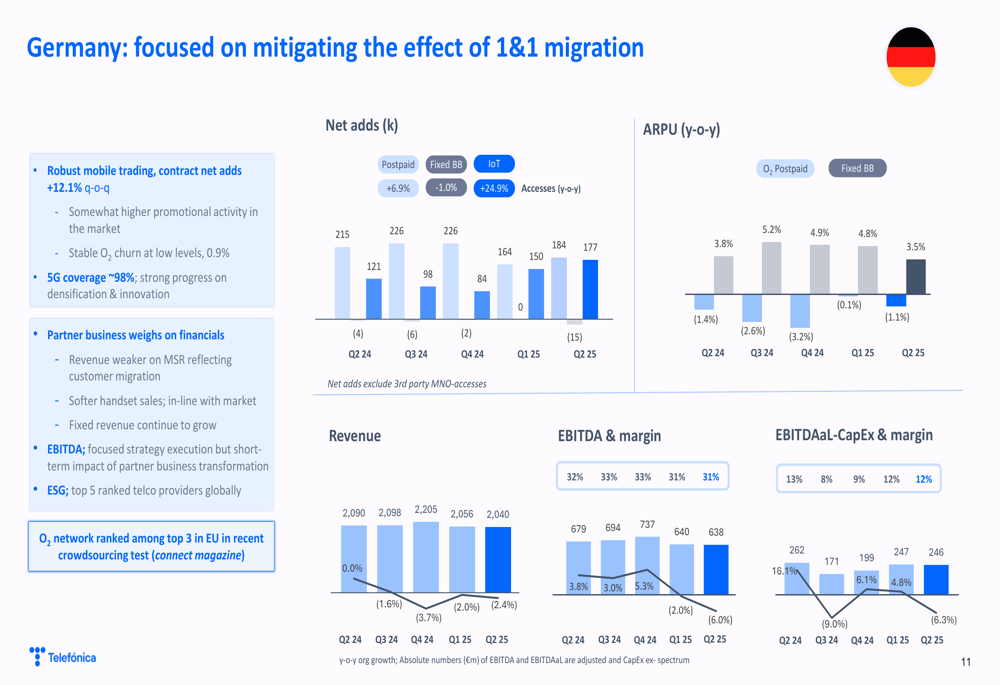

In Germany, Telefonica focused on mitigating the impact of 1&1’s migration away from its network, reporting robust mobile trading with contract net adds up 12.1% quarter-over-quarter. The company achieved approximately 98% 5G coverage in the market.

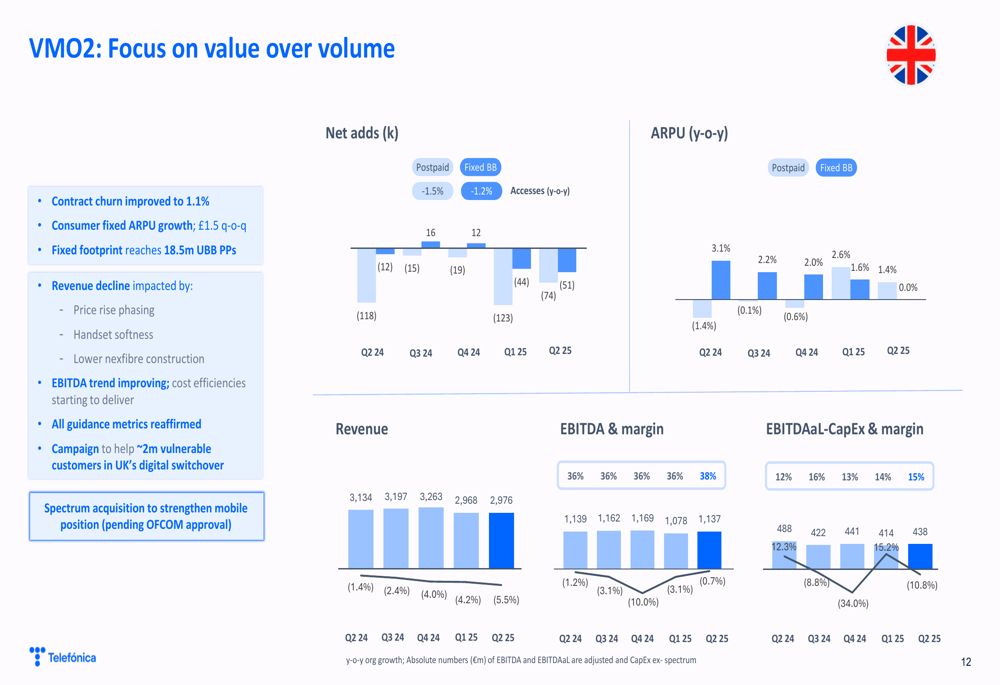

The UK joint venture VMO2 showed improved contract churn at 1.1% and consumer fixed ARPU growth of £1.5 quarter-over-quarter. The fixed footprint reached 18.5 million ultra-broadband premises passed, though EBITDA continued to decline, albeit at an improved rate due to cost efficiencies.

Forward-Looking Statements

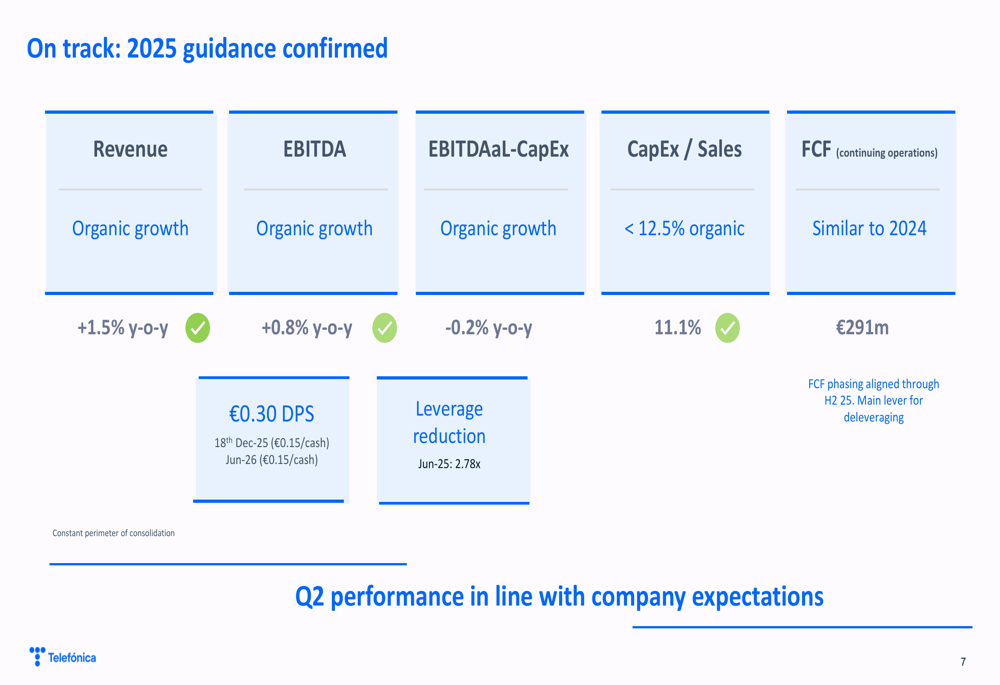

Telefonica confirmed its 2025 guidance across all key metrics:

- Revenue: Organic growth of 1.5% year-over-year

- EBITDA: Organic growth of 0.8% year-over-year

- EBITDA-CapEx: Organic growth of -0.2% year-over-year

- CapEx/Sales ratio: Below 12.5% organic (currently 11.1%)

- Free cash flow from continuing operations: Similar to 2024 (€291 million)

- Dividend: €0.30 per share (€0.15 in cash on December 18, 2025, and €0.15 in cash in June 2026)

- Leverage reduction: 2.78x as of June 2025

The company also highlighted its sustainability achievements, noting that Telefónica was named the 2nd Most Sustainable Company of 2025 by TIME and Statista.

Looking ahead, Telefonica emphasized that its strategic review is "progressing on schedule for H2 unveiling," suggesting potential further changes to the company’s structure or strategic direction in the coming months. The company continues to focus on its customer and infrastructure advantages while maintaining "disciplined industrial rational and financial flexibility" to drive value creation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.