Domino’s Pizza Australia surges on report Bain Capital exploring $2.6 bln buyout

Introduction & Market Context

TGS NOPEC Geophysical Company ASA (OB:TGS) reported a significant quarter-over-quarter improvement in its financial performance during its Q3 2025 earnings presentation on October 23, 2025. Despite ongoing challenges in the energy exploration sector, the company delivered solid results while continuing to reduce debt and maintain its dividend policy.

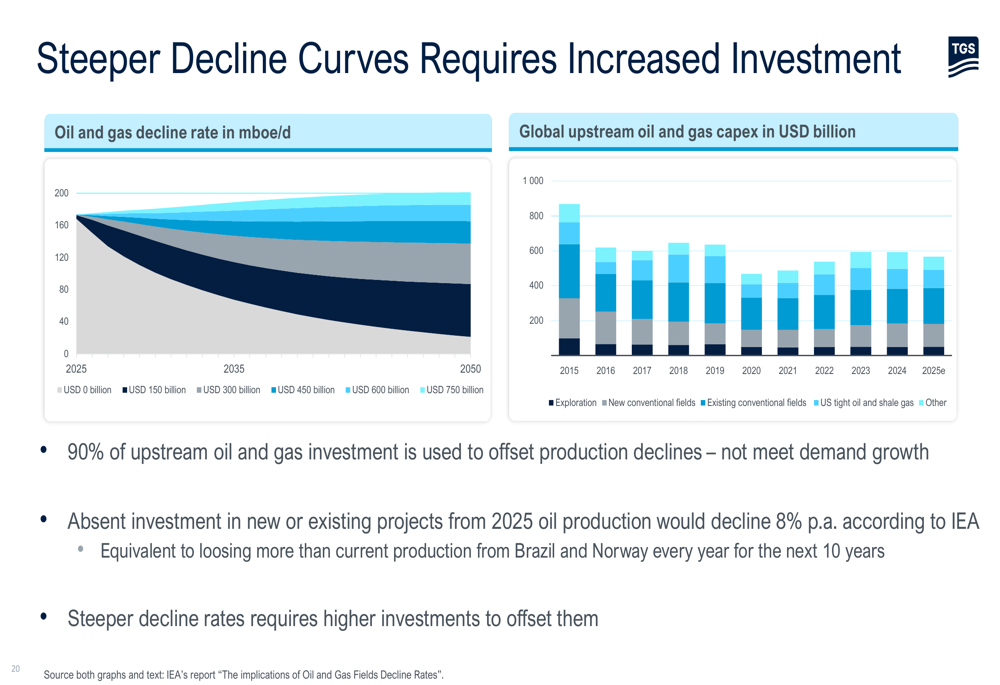

The geophysical services provider operates in an industry facing both short-term volatility and long-term structural challenges. As highlighted in the presentation, oil and gas decline rates require substantial ongoing investment, with 90% of upstream oil and gas investment currently used just to offset production declines.

Quarterly Performance Highlights

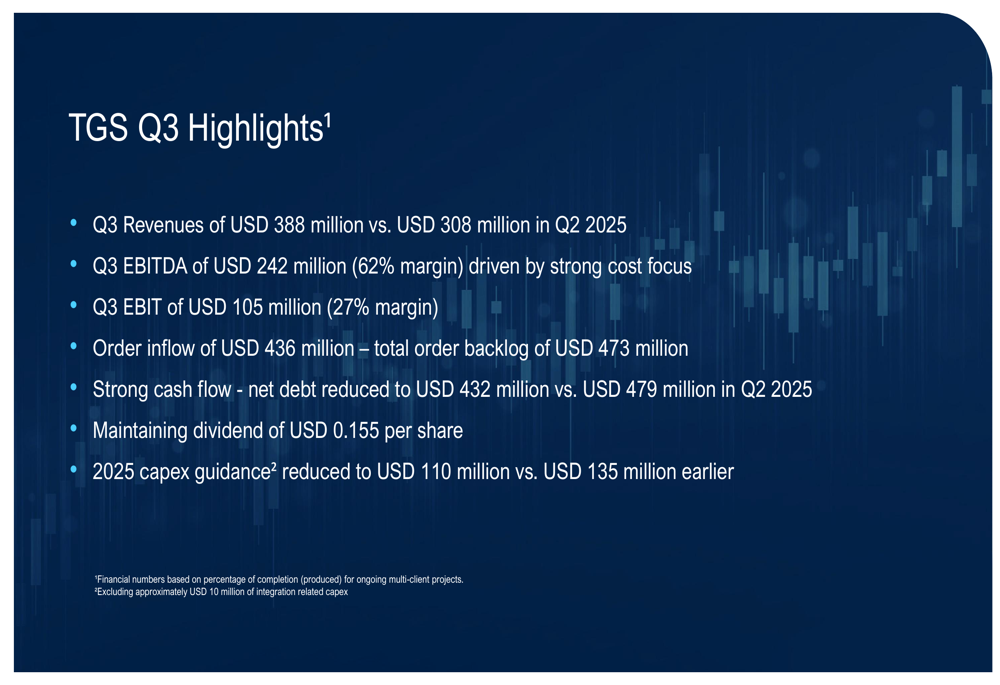

TGS reported Q3 2025 revenues of $388 million, representing a 26% increase from the $308 million recorded in Q2 2025, though remaining flat compared to the same quarter last year. The company achieved an impressive EBITDA of $242 million, translating to a robust 62% margin, while EBIT reached $105 million with a 27% margin.

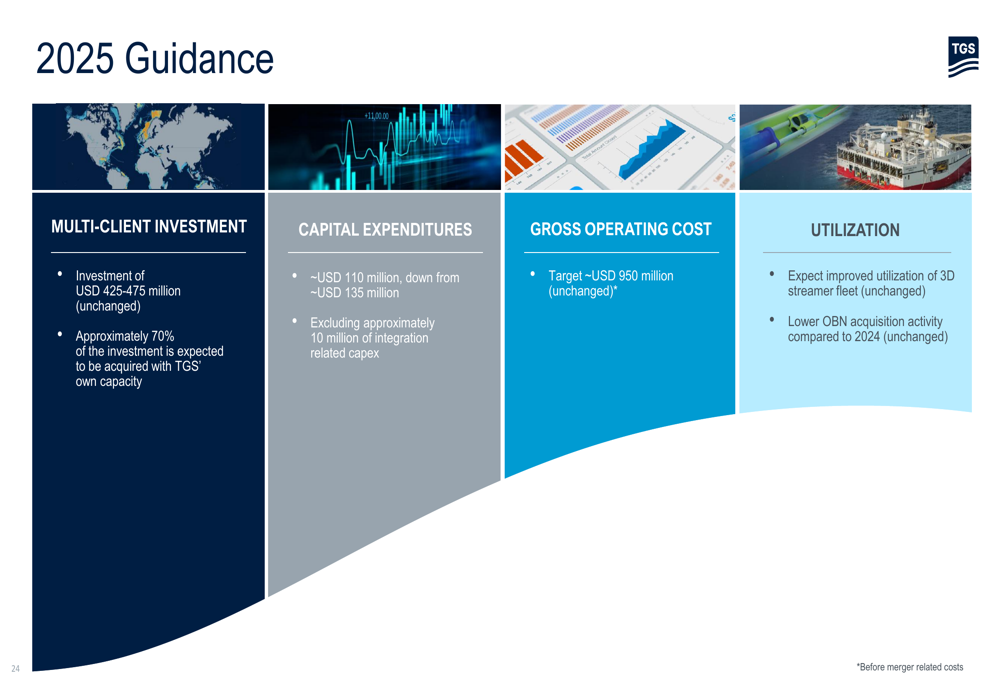

As shown in the following quarterly highlights slide, TGS maintained its quarterly dividend of $0.155 per share while reducing its 2025 capital expenditure guidance to $110 million:

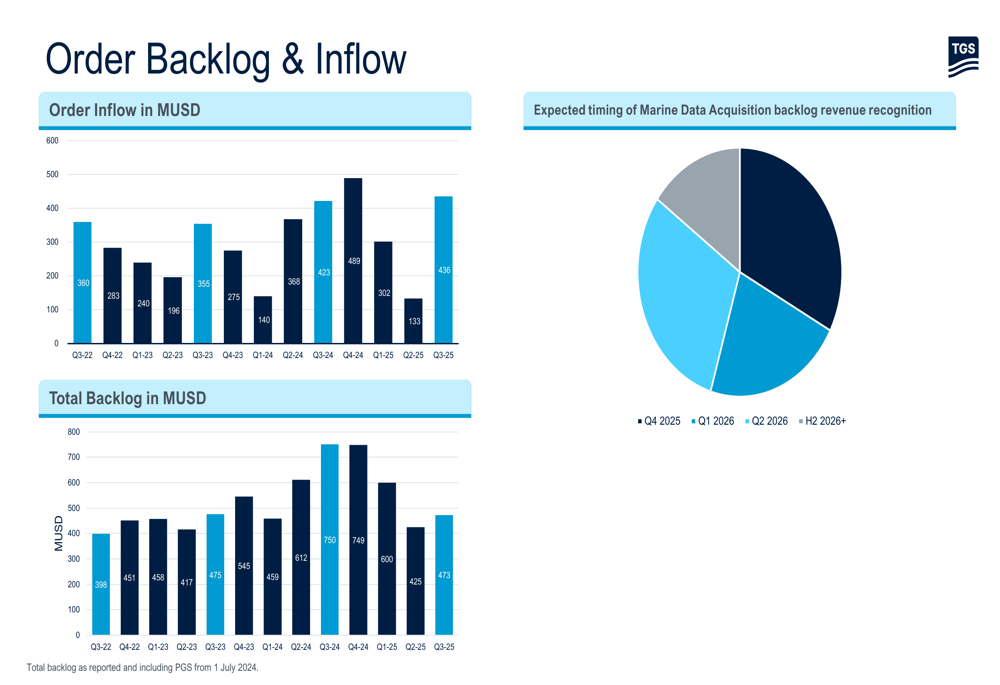

Order inflow remained strong at $436 million, supporting a total order backlog of $473 million. The company also made progress on its debt reduction strategy, bringing net debt down to $432 million from $479 million in the previous quarter, moving closer to its target range of $250-350 million.

Financial Analysis

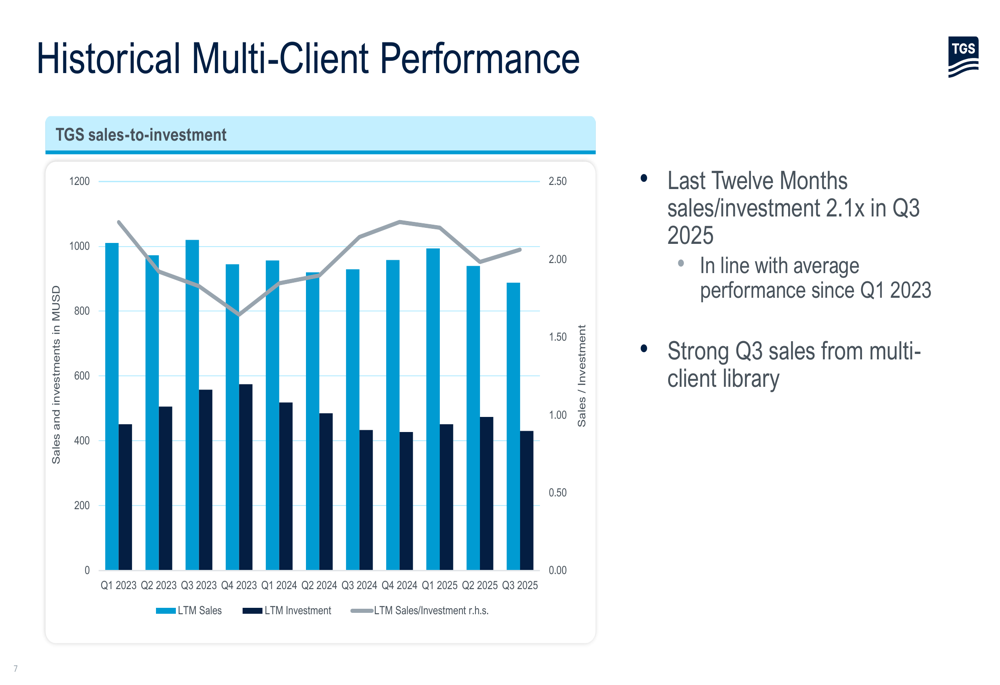

TGS’s multi-client segment continues to be a key revenue driver, generating $226 million in Q3 2025. While this represents a decrease from $277 million in Q3 2024, the company maintained a healthy sales-to-investment ratio of 2.1x over the last twelve months, in line with its historical performance.

The following chart illustrates TGS’s consistent multi-client performance over time:

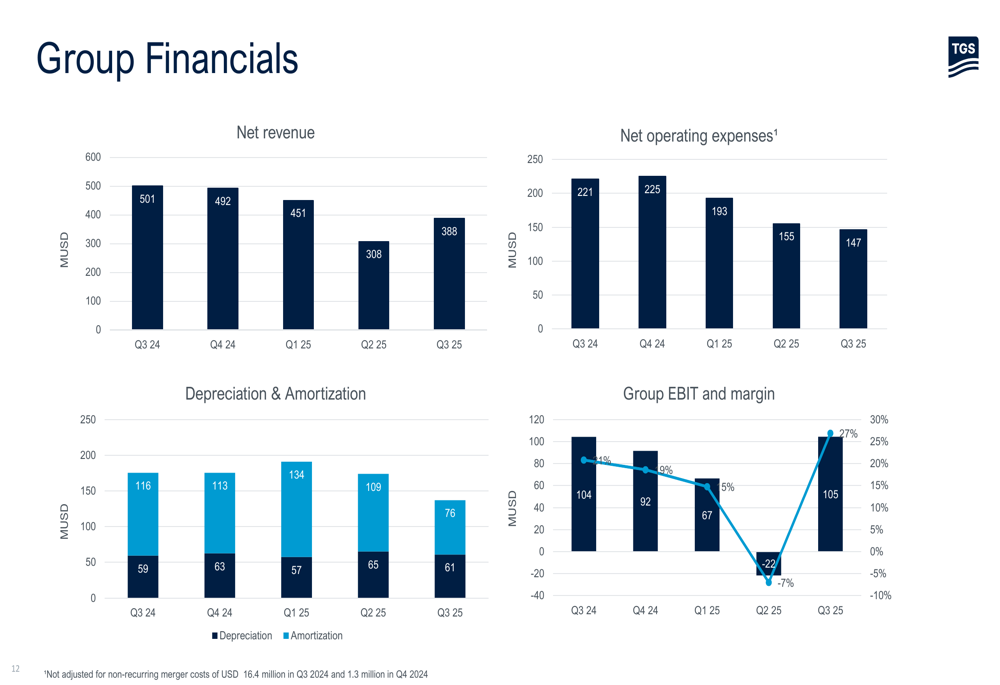

The company’s group financials show a recovery from Q2 2025, when it reported a negative EBIT margin. The Q3 2025 EBIT of $105 million and 27% margin demonstrate a significant improvement in profitability:

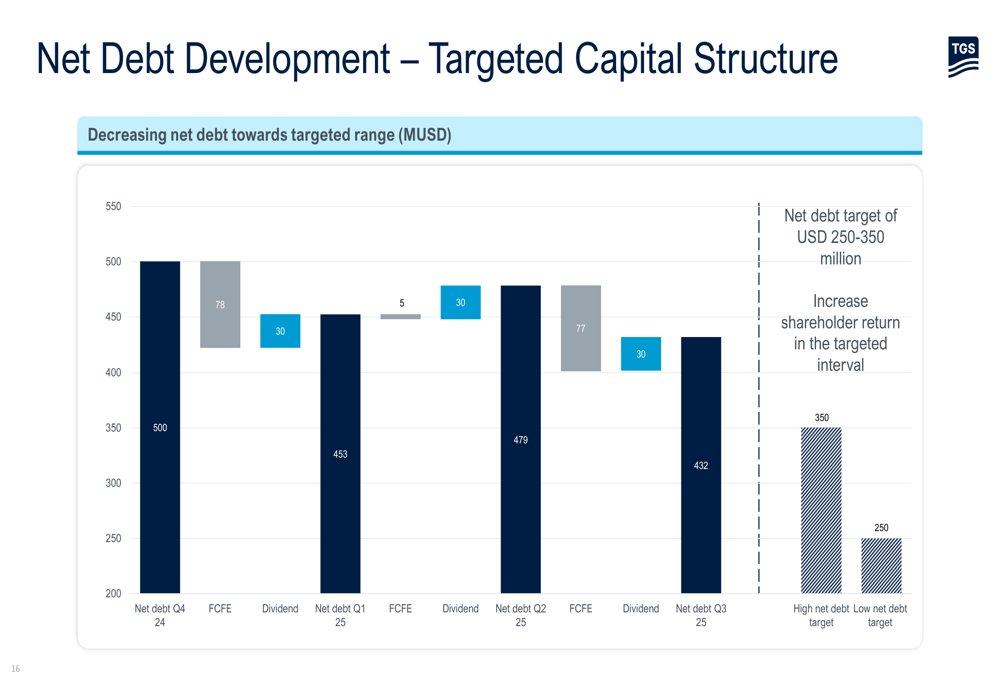

TGS continues to make progress on its debt reduction strategy, with net debt decreasing to $432 million in Q3 2025, down from $500 million at the end of 2024. This moves the company closer to its targeted capital structure with net debt in the $250-350 million range:

Strategic Initiatives & Cost Optimization

A key focus for TGS has been cost optimization across the organization. The company has reduced its 2025 guidance for gross operating expenses from approximately $1,050 million to around $950 million. This disciplined approach to costs, combined with strategic investments in high-return projects, has helped maintain strong margins despite market challenges.

TGS’s integrated business model provides flexibility to shift between contract and multi-client projects based on market conditions. CEO Kristian Johansen emphasized this advantage during the earnings call, stating: "We’re the only company in our space that can claim that we have the flexibility at any point of time to switch between contracts and multi-client."

The company’s data acquisition activity spans multiple regions globally, with significant operations in Brazil, the Gulf of Mexico, and other key exploration areas. This geographic diversification helps mitigate regional market risks.

Industry Outlook & Guidance

TGS highlighted the structural challenges facing the energy exploration industry, with steeper decline curves requiring increased investment. Without continued investment, oil production would decline by approximately 8% annually from 2025, according to the company’s presentation:

For 2025, TGS provided updated guidance reflecting its strategic priorities and market outlook:

The company expects multi-client investments of $425-475 million for the full year, with 70% to be acquired using its own capacity. Capital expenditures are projected at approximately $110 million, reduced from the previous guidance of around $135 million, reflecting the company’s focus on capital discipline.

TGS’s order backlog provides visibility into future revenues, with a significant portion expected to be recognized in the coming quarters:

In summary, TGS delivered a solid quarter with strong financial metrics despite industry challenges. The company’s focus on cost optimization, debt reduction, and strategic investments positions it well for the future, though it remains exposed to volatility in oil prices and exploration spending. Management maintains a cautious but positive outlook, noting that while short-term market development remains sensitive to oil prices, the long-term market outlook remains positive.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.