Gold futures surpass $4,000 for the first time amid global political uncertainty

Introduction & Market Context

The Andersons , Inc. (NASDAQ:ANDE) reported second-quarter 2025 results that significantly missed earnings expectations despite revenue growth, according to the company’s August 5 earnings presentation. The agricultural and renewables company posted adjusted earnings per share of $0.24, falling well short of the $0.53 analyst forecast and representing a 79% decline from the $1.15 reported in the same quarter last year.

The earnings miss triggered a 2.11% decline in ANDE’s stock price to $34.65 in post-market trading, bringing it closer to its 52-week low of $31.03. Despite the disappointing results, the company highlighted strategic initiatives including a major acquisition in its renewables segment.

Quarterly Performance Highlights

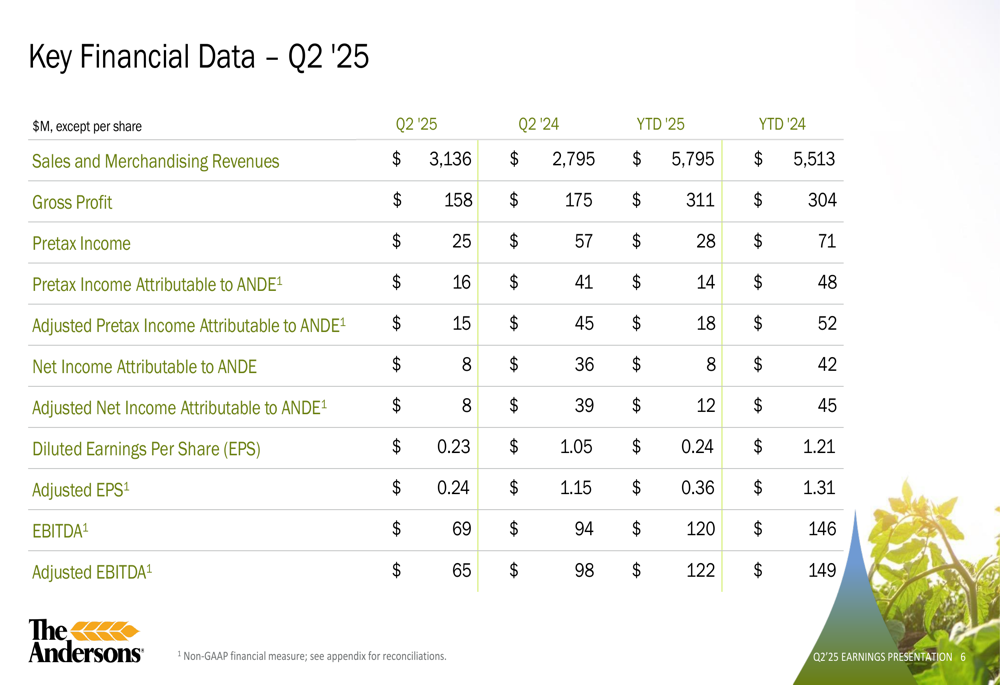

The Andersons reported mixed financial results for the second quarter of 2025. While sales and merchandising revenues increased to $3.14 billion from $2.80 billion in Q2 2024, profitability metrics declined across the board.

As shown in the following comprehensive financial data table:

Gross profit decreased to $158 million from $175 million in the prior-year quarter, while adjusted EBITDA fell to $65 million from $98 million. The company’s adjusted pretax income attributable to The Andersons dropped to $15 million from $45 million a year earlier.

CEO Bill Krueger expressed optimism despite the challenges, stating during the earnings call: "We are positive about the last half of the year. We’re prepared for the fall harvest and are excited about the opportunities ahead of us."

Strategic Initiatives

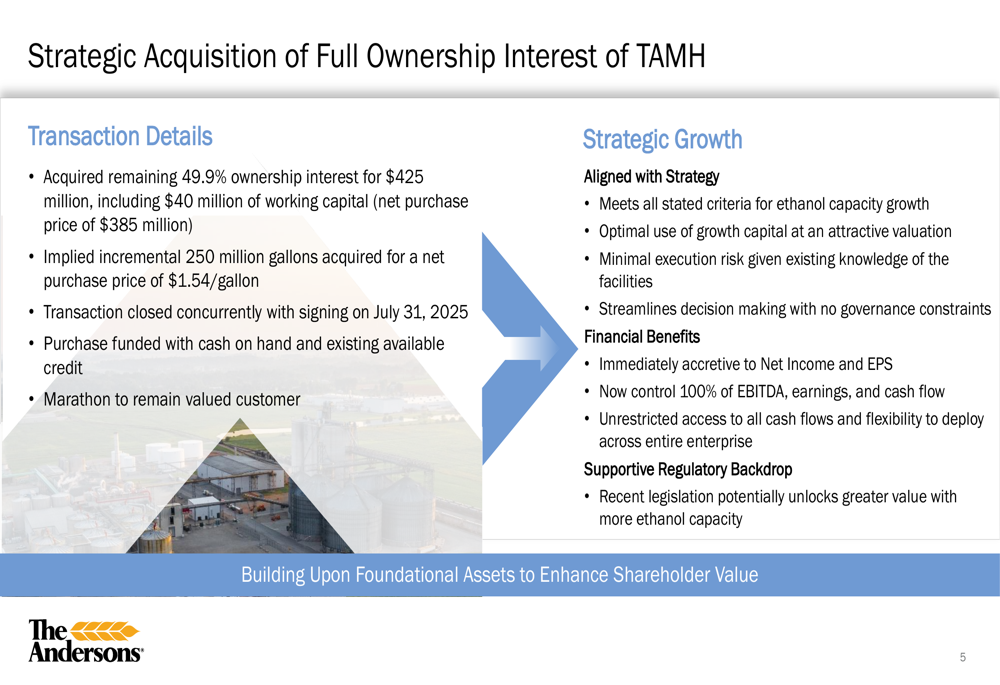

The most significant strategic development announced was the acquisition of the remaining 49.9% ownership interest in TAMH (The Andersons Marathon Holdings), a key component of the company’s renewables business. The transaction, which closed on July 31, 2025, was valued at $425 million including $40 million of working capital.

The following slide details the strategic rationale and financial impact of this major acquisition:

The company emphasized that the acquisition aligns with its strategy for ethanol capacity growth at an attractive valuation of $1.54 per gallon. Management expects the transaction to be immediately accretive to net income and EPS, while providing full control of TAMH’s EBITDA, earnings, and cash flow. Marathon will remain a valued customer despite the ownership change.

Segment Analysis

The Andersons’ performance varied across its two primary business segments: Agribusiness and Renewables.

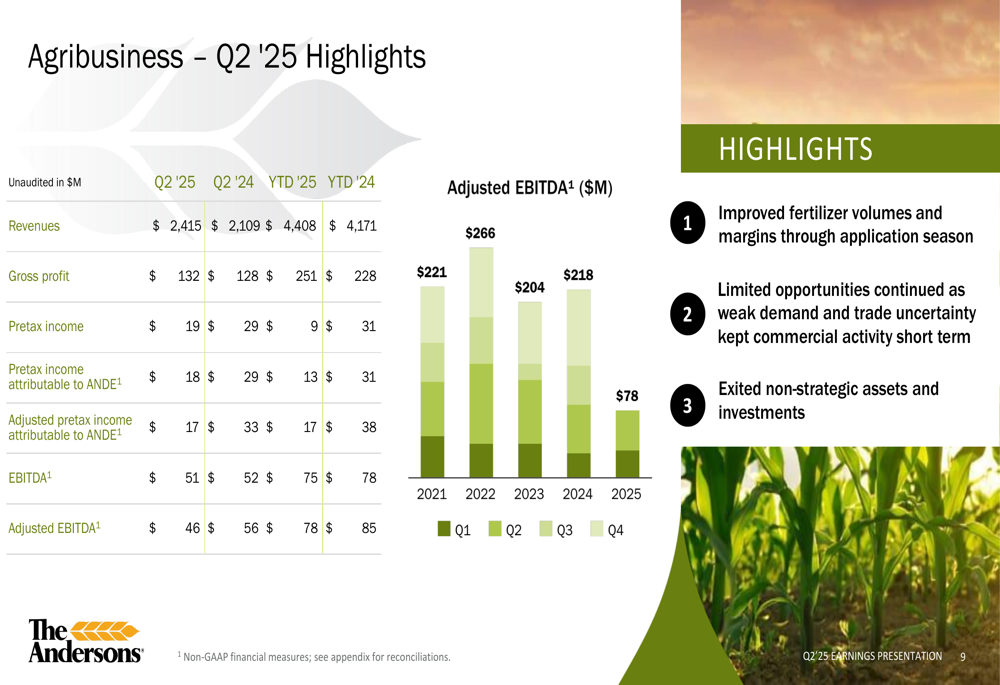

The Agribusiness segment showed mixed results with improved fertilizer volumes and margins, but faced challenges from weak demand and trade uncertainty. The segment’s pretax income attributable to The Andersons fell to $18 million from $29 million in Q2 2024, while adjusted EBITDA declined to $46 million from $56 million.

As illustrated in the detailed Agribusiness performance metrics:

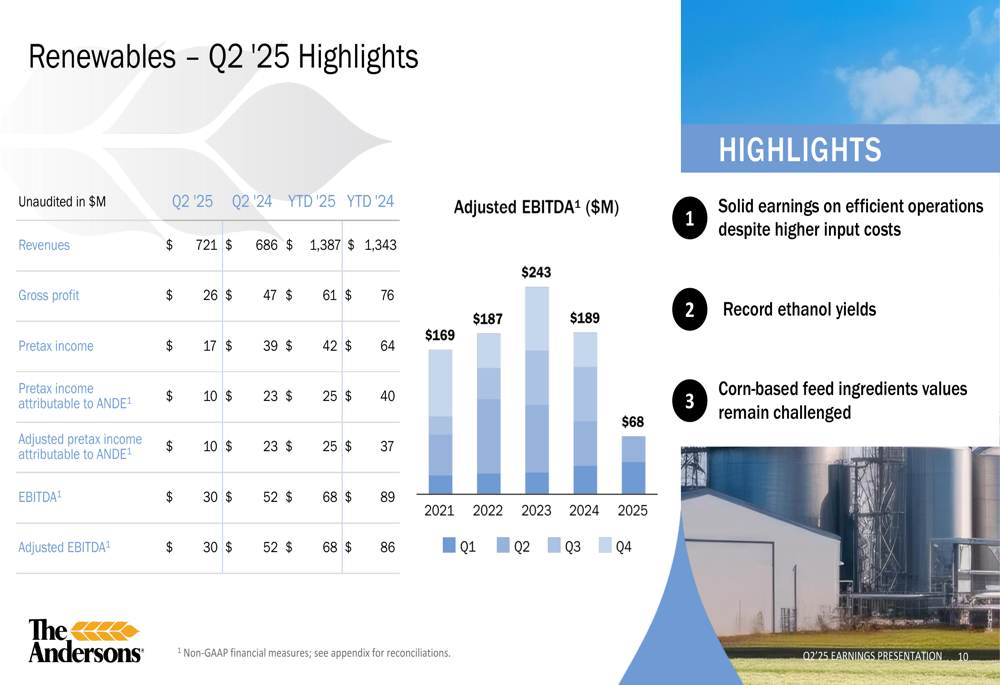

The Renewables segment, which includes ethanol production, reported "solid earnings on efficient operations" despite higher input costs. The segment achieved record ethanol yields but faced challenges with corn-based feed ingredient values. Pretax income attributable to The Andersons decreased to $10 million from $23 million in Q2 2024, with adjusted EBITDA falling to $30 million from $52 million.

The following slide provides a comprehensive view of the Renewables segment performance:

Financial Position & Outlook

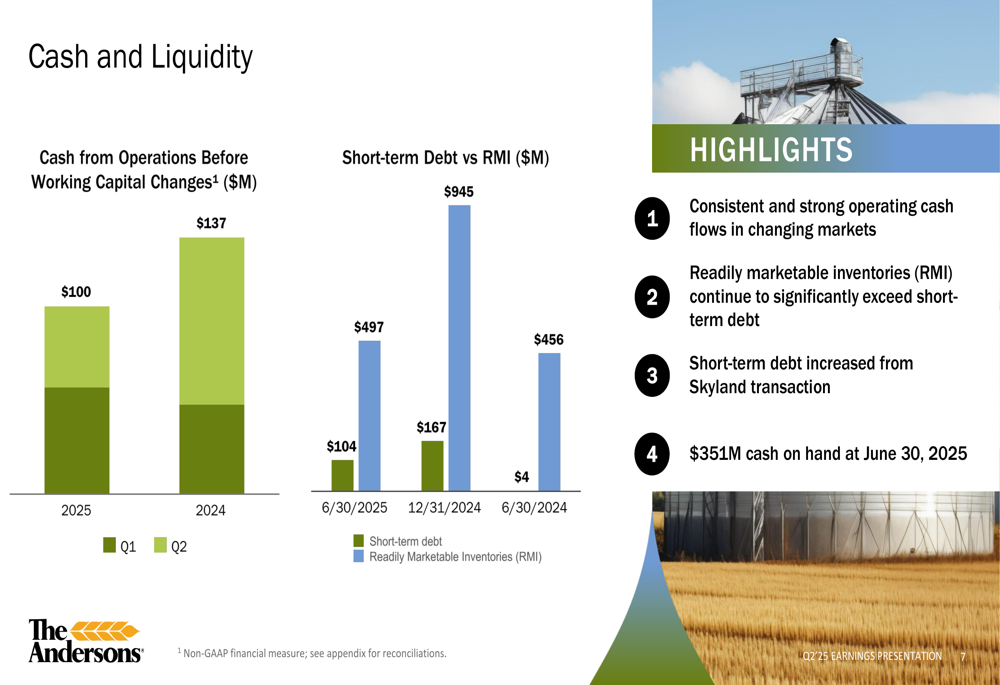

Despite the earnings challenges, The Andersons maintained a strong financial position with $351 million in cash as of June 30, 2025. The company’s readily marketable inventories (RMI) of $497 million significantly exceeded its short-term debt of $104 million, providing substantial liquidity.

The following chart illustrates the company’s cash and liquidity position:

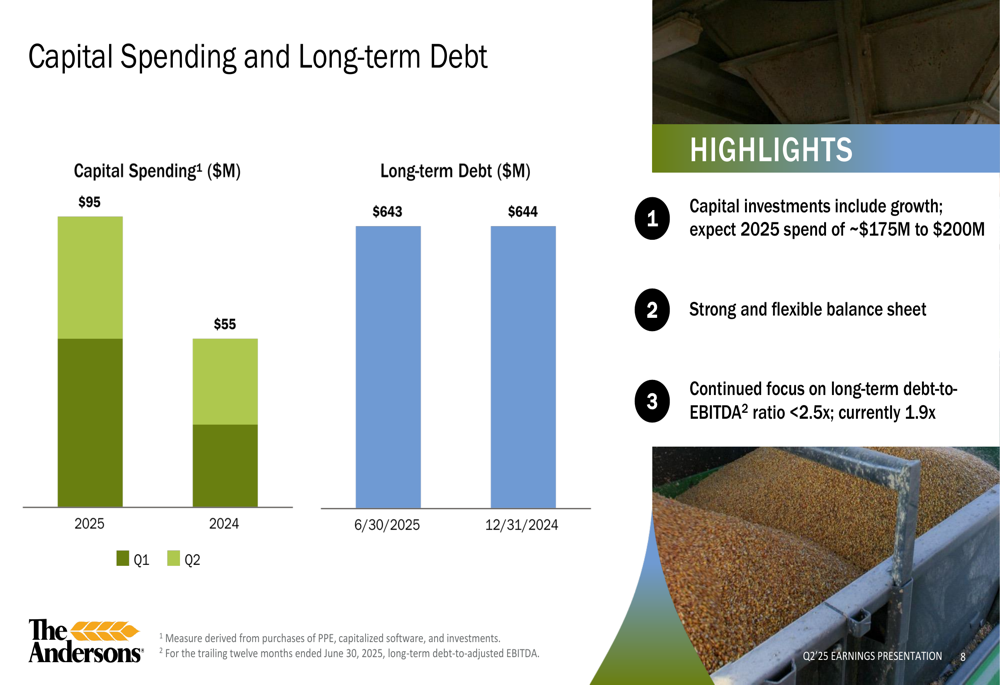

Capital spending increased to $95 million in the first half of 2025 compared to $55 million in the same period of 2024, with full-year 2025 capital expenditures expected to reach $175-200 million. Long-term debt remained stable at $643 million, with a debt-to-EBITDA ratio of 1.9x, well below the company’s target of 2.5x.

As shown in this capital spending and debt overview:

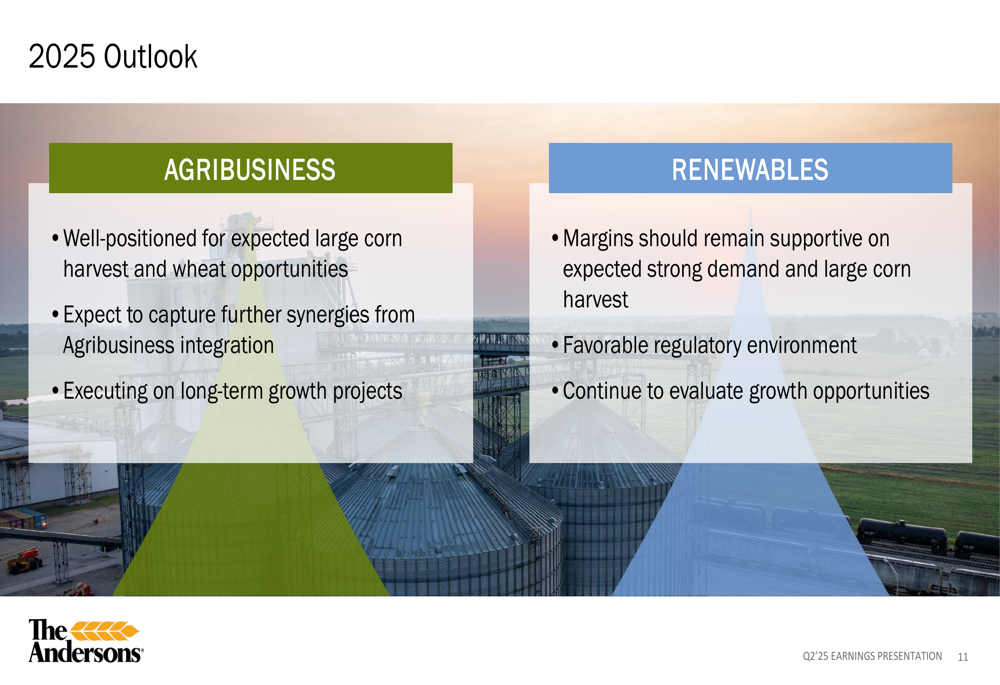

Looking ahead, The Andersons expressed optimism about the second half of 2025, citing expectations for a large corn harvest and wheat opportunities. In the Renewables segment, management anticipates supportive margins due to strong demand and favorable regulatory conditions.

The company’s outlook slide highlights these forward-looking expectations:

Executive Commentary

During the earnings call, management emphasized the strategic importance of the TAMH acquisition and expressed confidence in future performance despite current challenges. CEO Bill Krueger highlighted the company’s strong balance sheet and strategic focus on growth and shareholder value.

The leadership team presenting these results included:

CFO Brian Valentine noted that the company remains committed to its long-term financial targets and continues to evaluate growth opportunities that align with its strategic priorities.

While The Andersons faces near-term profitability challenges, management believes its strategic initiatives, particularly the TAMH acquisition, position the company for improved performance as agricultural markets stabilize and renewable energy demand continues to grow.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.