Trump/Cook, Nissan weakness, more tariffs and gold - what’s moving markets

Introduction & Market Context

ThredUp Inc (NYSE:NASDAQ:TDUP) presented its Q1 2025 investor presentation on May 5, 2025, showcasing improved financial performance and strategic initiatives in the growing secondhand apparel market. The stock responded positively, trading at $4.77 in aftermarket sessions, up 7.43% from the previous close of $4.42.

The company, founded in 2009 and headquartered in Oakland, California, operates as a managed marketplace for secondhand apparel, with a mission to "inspire the world to think secondhand first." ThredUp’s presentation highlighted its position in a secondhand apparel market that grew 14% in 2024, five times faster than the broader retail clothing sector.

As shown in the following slide, ThredUp’s mission is supported by a vast selection of secondhand items:

Quarterly Performance Highlights

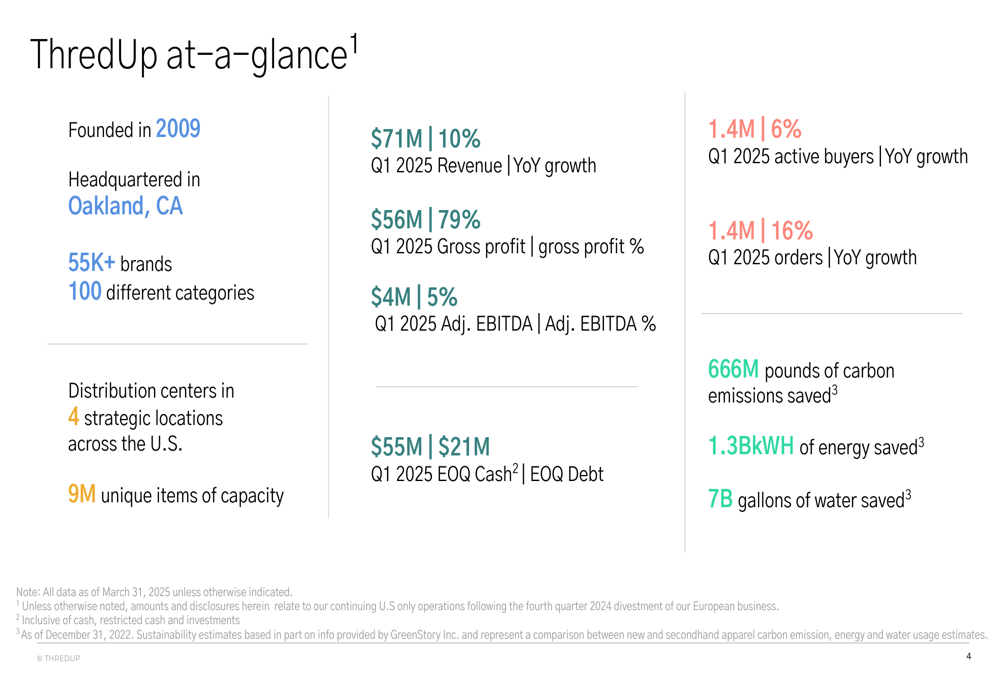

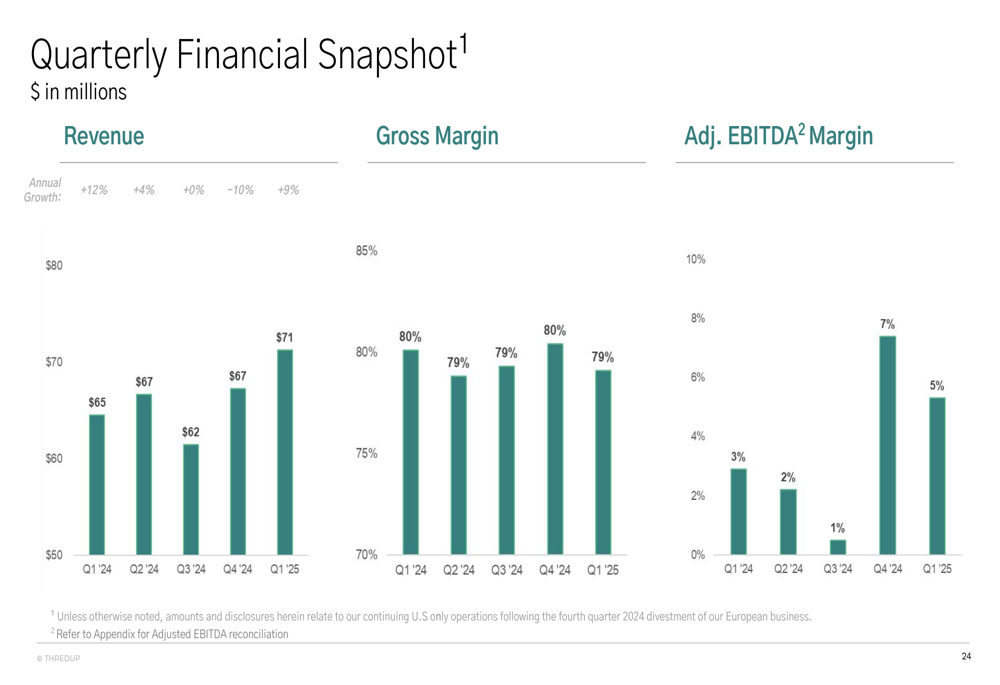

ThredUp reported Q1 2025 revenue of $71 million, representing 10% year-over-year growth. The company achieved a gross profit of $56 million with a robust 79% gross margin, while Adjusted EBITDA reached $4 million, translating to a 5% margin. This marks a significant improvement in profitability compared to previous quarters.

The company’s key metrics as of March 31, 2025, are comprehensively presented in this overview slide:

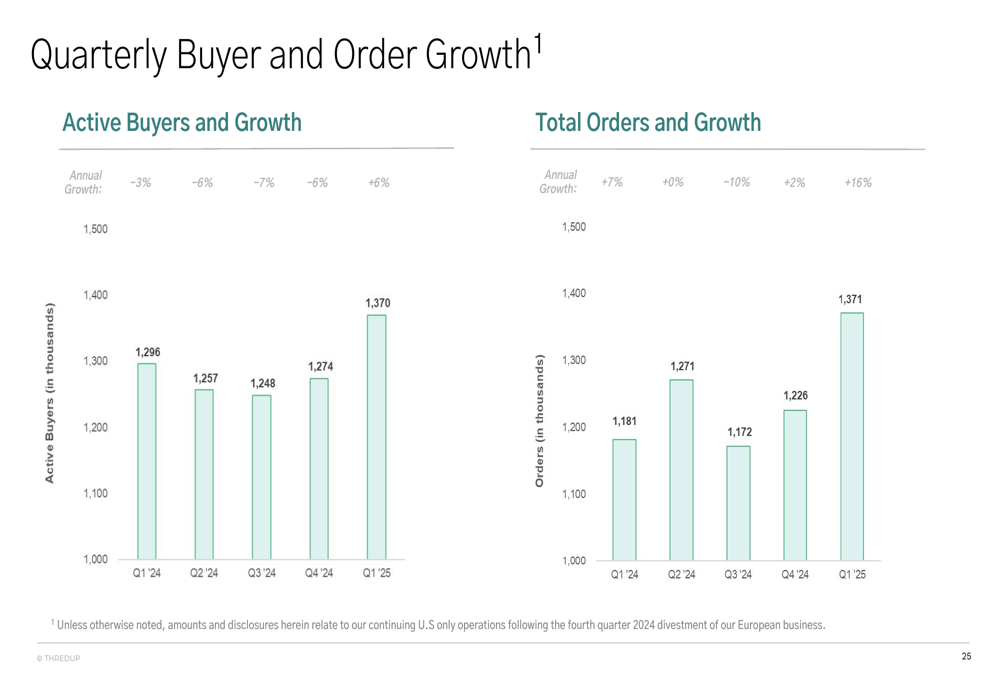

Active buyers increased to 1.4 million, up 6% year-over-year, while orders grew to 1.4 million, representing a 16% year-over-year increase. This growth in buyer and order metrics represents a reversal from the previous quarter’s trends, as the Q4 2024 earnings report had shown a 6% decline in active buyers.

The quarterly financial snapshot demonstrates the company’s improving performance trajectory:

Similarly, the buyer and order growth metrics show encouraging momentum:

Strategic Initiatives

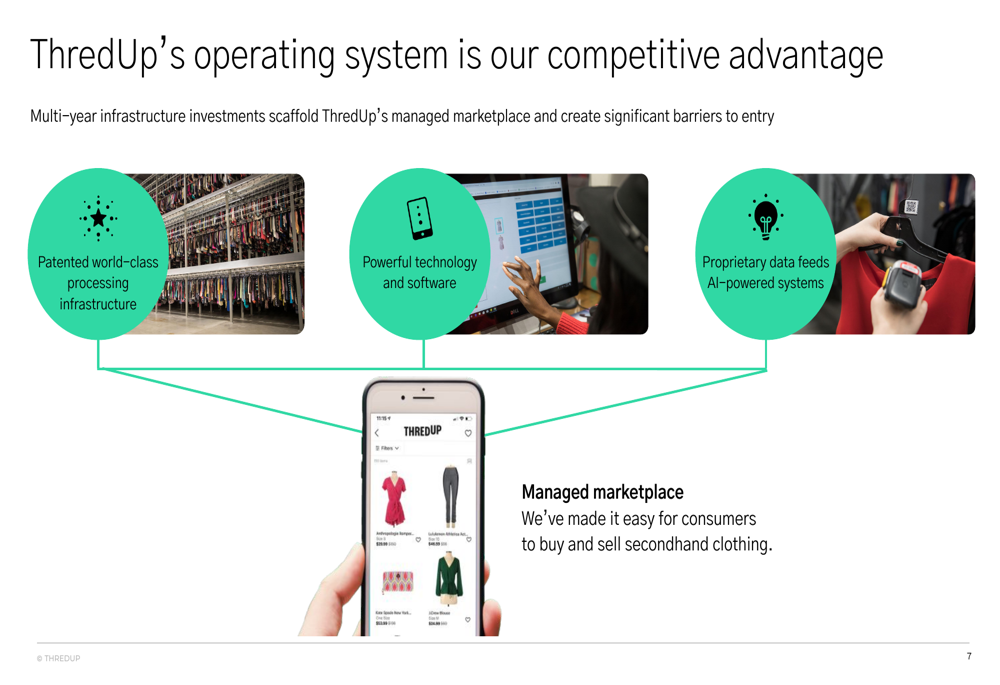

ThredUp’s presentation emphasized several strategic initiatives driving its marketplace growth. The company’s operating system, built on multi-year infrastructure investments, creates significant barriers to entry through patented processing infrastructure, powerful technology, and proprietary data and AI systems.

The following slide illustrates ThredUp’s operating system as a key competitive advantage:

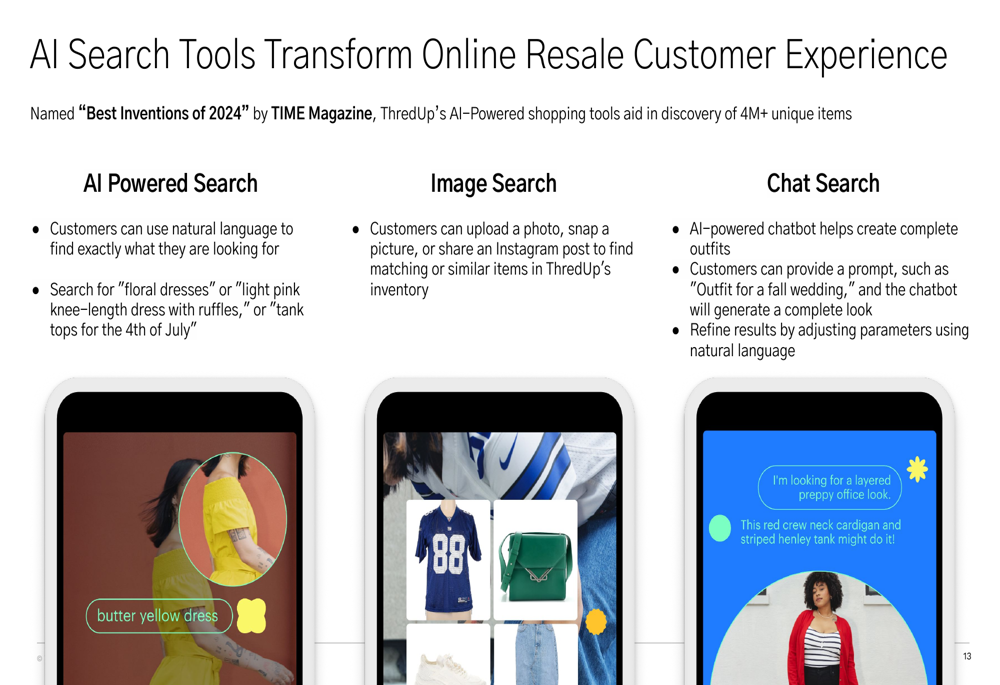

A standout innovation highlighted in the presentation is ThredUp’s AI-powered search tools, which were named among TIME Magazine’s "Best Inventions of 2024." These tools include natural language search, image search, and chat search capabilities that help customers navigate the platform’s millions of unique items.

As shown in this slide, these AI tools transform the online resale customer experience:

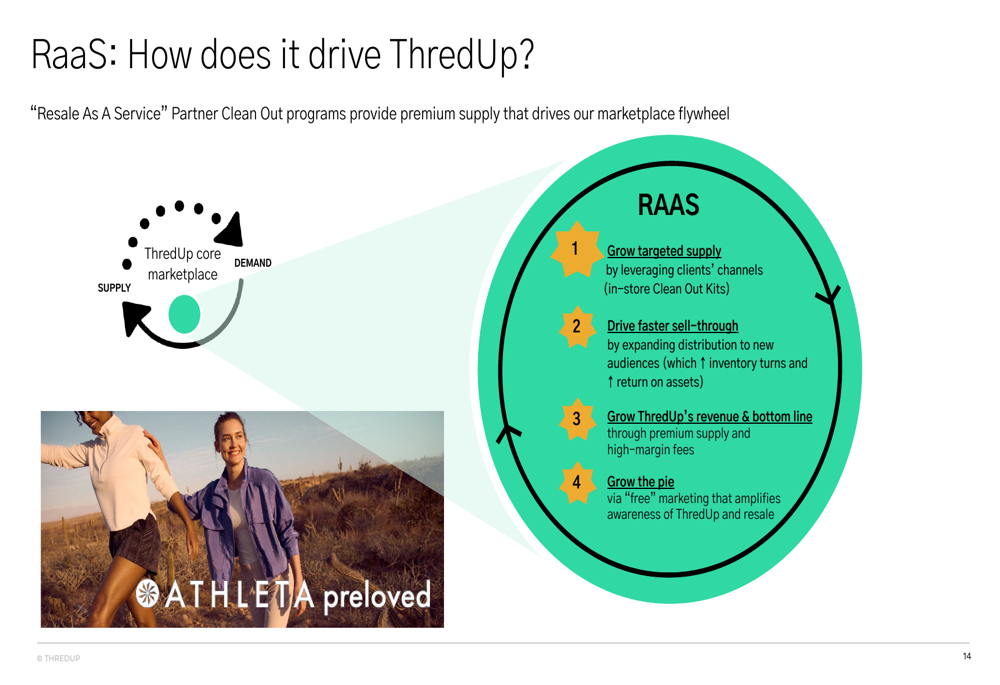

Another key strategic initiative is ThredUp’s Resale-as-a-Service (RaaS) program, which partners with retail brands to provide clean-out programs that supply premium inventory to ThredUp’s marketplace:

Competitive Industry Position

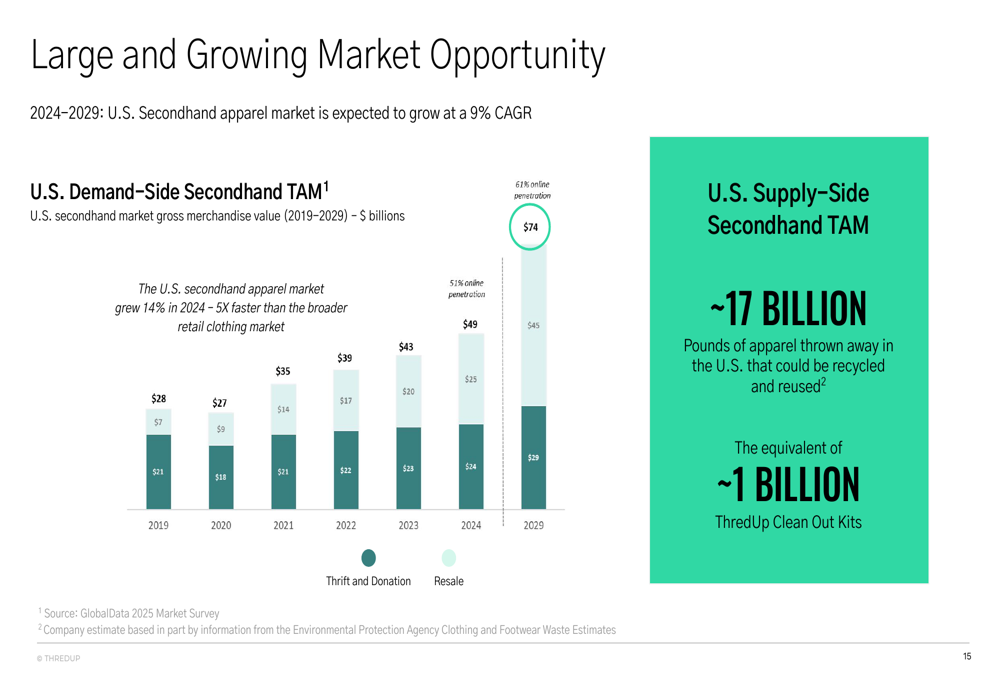

ThredUp operates in a rapidly growing market. According to the presentation, the U.S. secondhand apparel market is expected to grow at a 9% CAGR from 2024 to 2029, with the total addressable market projected to reach $73 billion by 2029.

The market opportunity is visualized in this growth chart:

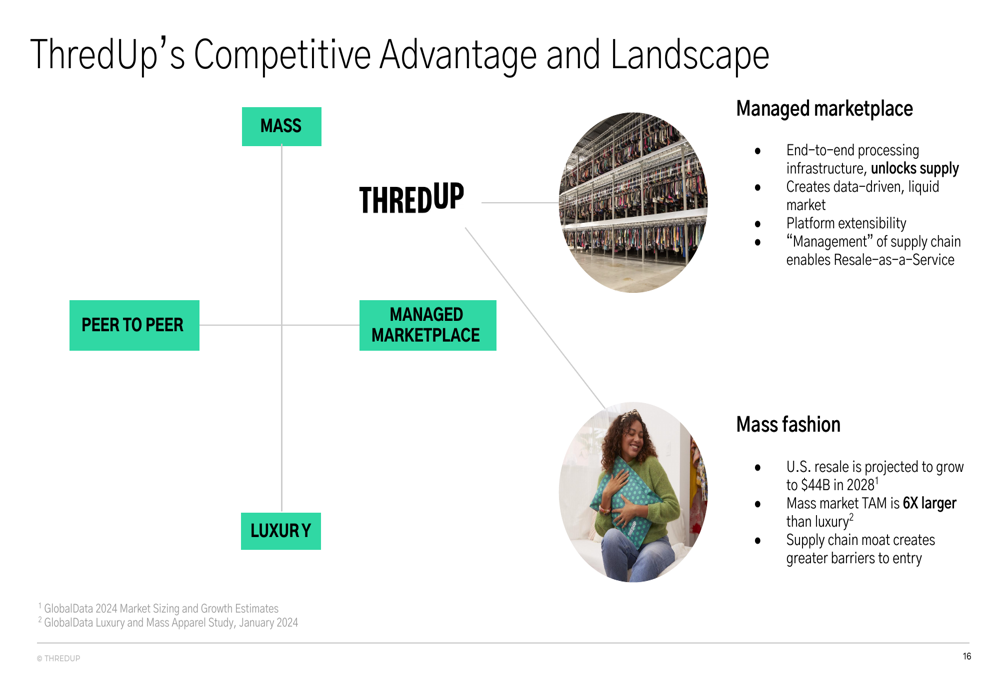

ThredUp positions itself in the "Mass Managed Marketplace" segment, emphasizing that the mass market TAM is six times larger than the luxury segment. The company’s competitive advantages include its end-to-end processing infrastructure, data-driven marketplace, platform extensibility, and RaaS capabilities.

The competitive landscape is illustrated in this positioning slide:

Forward-Looking Statements

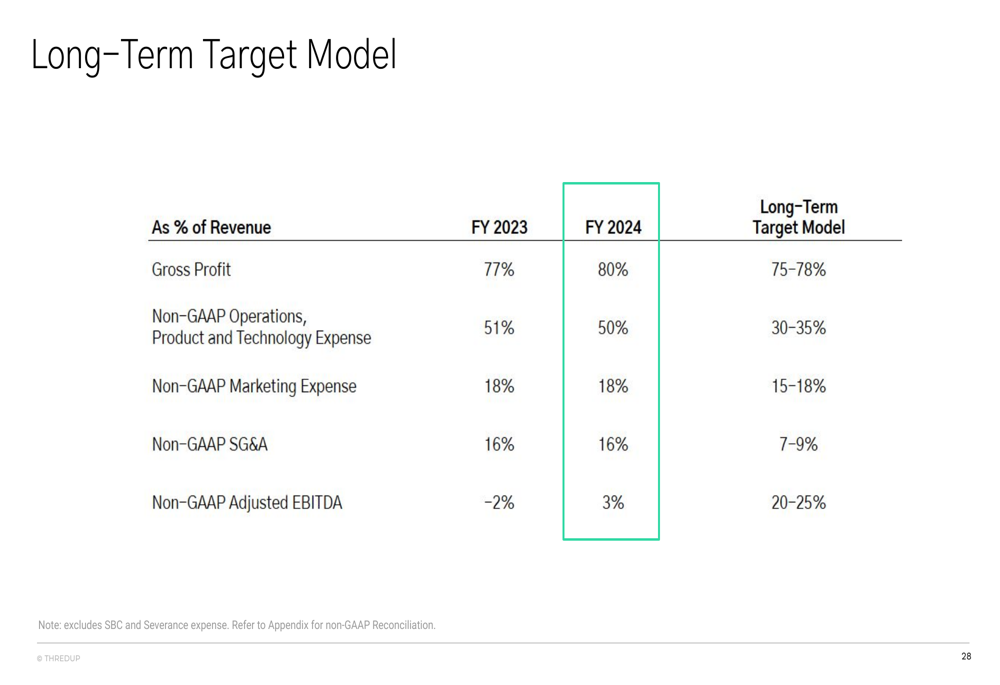

ThredUp’s long-term financial targets suggest substantial margin expansion as the company leverages its infrastructure investments. The presentation outlined a target model with gross profit margins of 75-78% and Adjusted EBITDA margins of 20-25%, compared to the current 5% Adjusted EBITDA margin in Q1 2025.

The long-term target model is detailed in this slide:

This ambitious profitability target represents a significant improvement from the company’s historical performance. For context, ThredUp’s Adjusted EBITDA margin has improved from -18% in 2020 to 3% in 2024, showing consistent progress toward profitability.

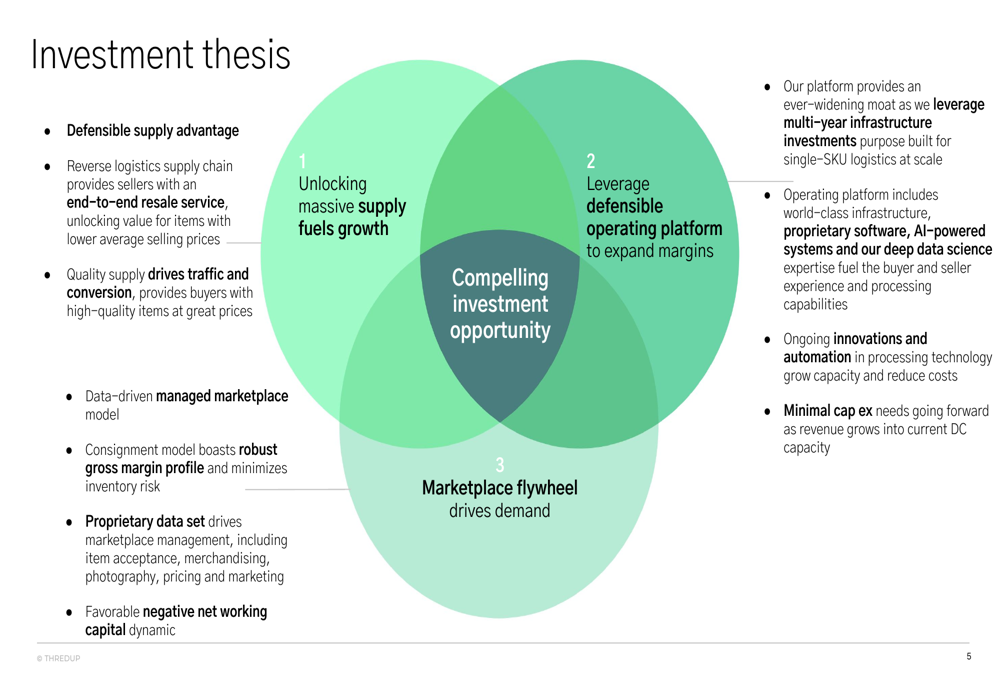

The company’s investment thesis centers around three interconnected pillars: unlocking massive supply to fuel growth, leveraging its defensible operating platform to expand margins, and using its marketplace flywheel to drive demand:

While ThredUp’s Q1 2025 presentation painted an optimistic picture of growth and improving profitability, it’s worth noting that the company’s Q4 2024 results had shown mixed performance, with an EPS miss of -$0.19 versus an expected -$0.13. However, the positive trends in Q1 2025, particularly the return to active buyer growth and the significant improvement in Adjusted EBITDA margin, suggest that ThredUp may be turning a corner in its path to sustainable profitability.

As the secondhand apparel market continues to expand, ThredUp’s investments in AI technology, processing infrastructure, and strategic partnerships position the company to capitalize on the growing consumer interest in sustainable fashion alternatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.