EU and US could reach trade deal this weekend - Reuters

Executive Summary

The Timken Company (NYSE:TKR) reported first quarter 2025 results on April 30, showing declining revenue and profitability compared to the prior year, while slightly improving its full-year sales outlook despite ongoing challenges from tariffs and uneven global demand. The company’s stock fell 3.29% to $65.27 following the announcement.

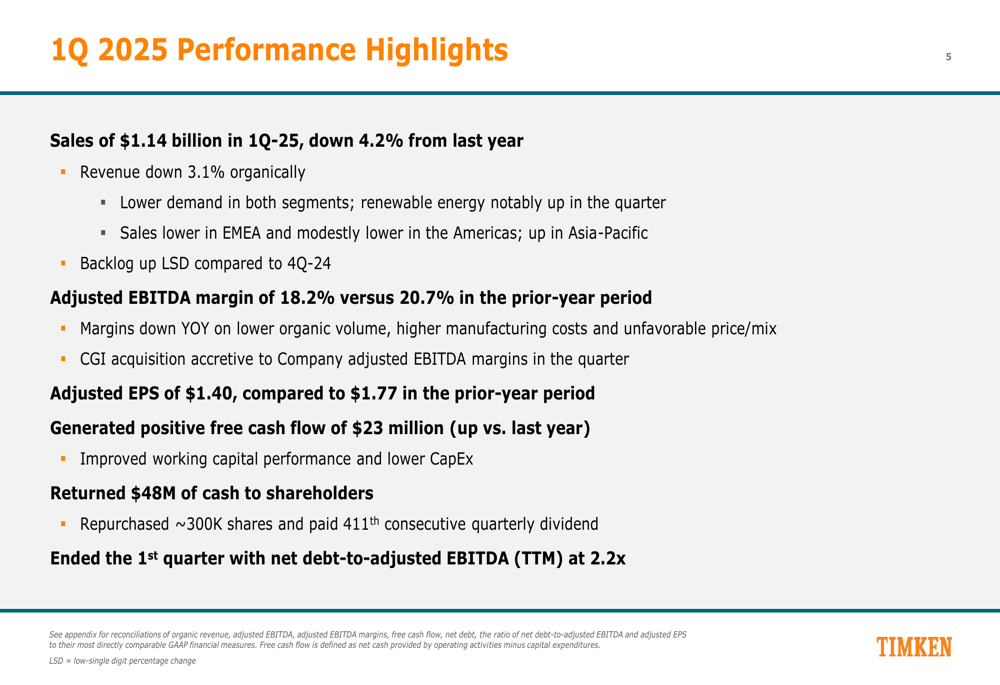

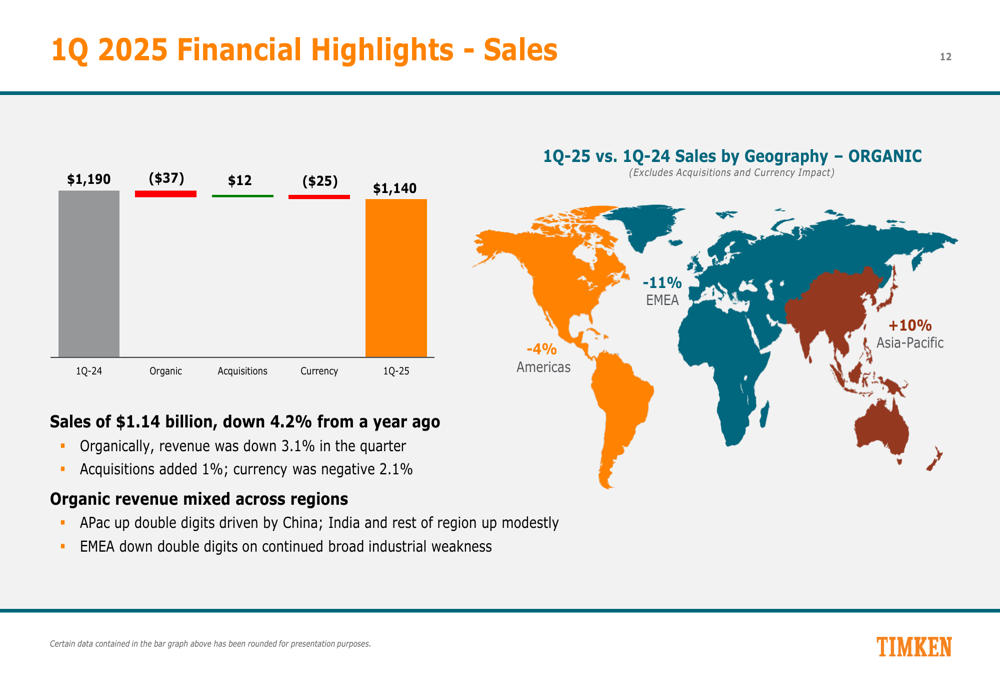

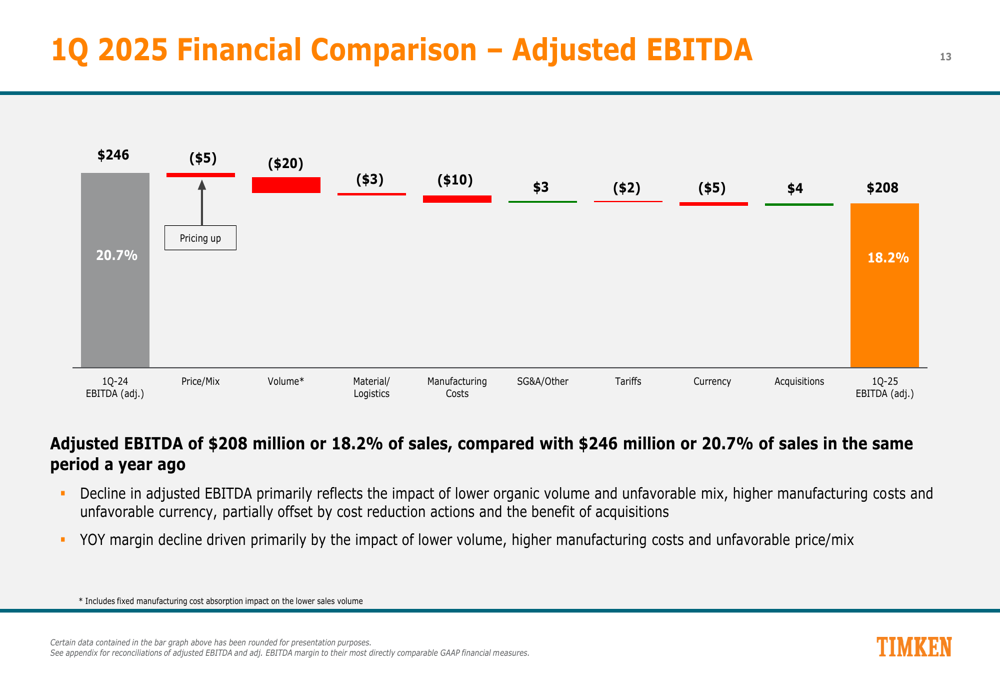

Timken posted sales of $1.14 billion in the first quarter, down 4.2% year-over-year, with organic revenue declining 3.1%. Adjusted earnings per share fell to $1.40 from $1.77 in the prior-year period, while adjusted EBITDA margin contracted to 18.2% from 20.7%.

"We’re focused on delivering resilient performance in 2025 while maintaining a cautious view due to international trade volatility," said Rich Kyle, President and Chief Executive Officer, during the presentation.

Quarterly Performance Highlights

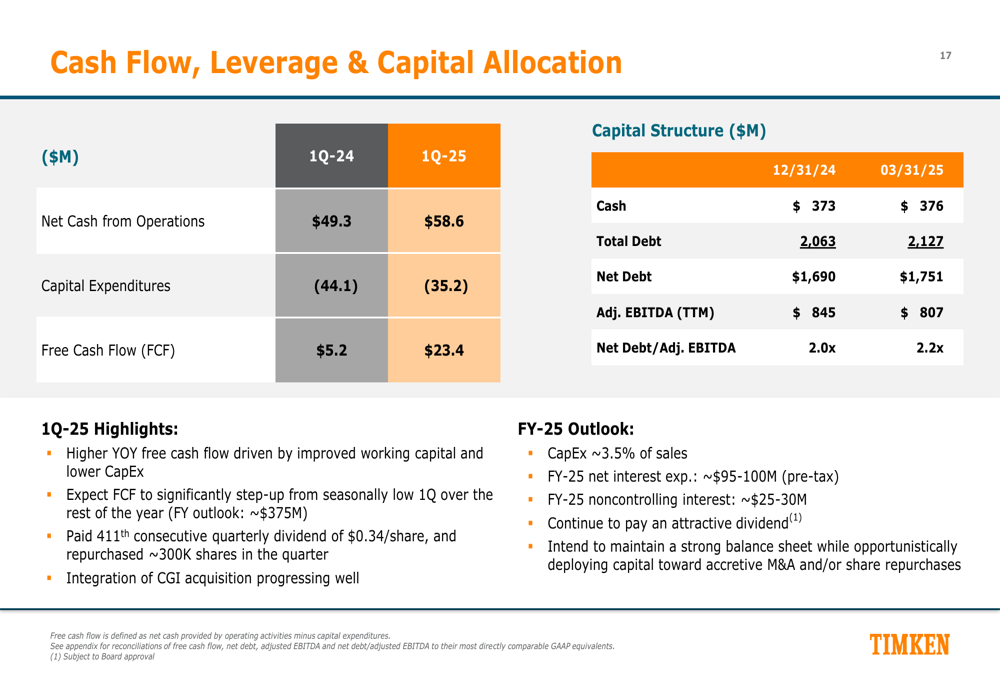

Timken’s first quarter results reflected challenging market conditions across several sectors, though the company managed to generate positive free cash flow of $23 million, an improvement from the same period last year.

The company returned $48 million to shareholders during the quarter through share repurchases (~300,000 shares) and dividends, notably paying its 411th consecutive quarterly dividend. Timken ended the quarter with a net debt-to-adjusted EBITDA ratio of 2.2x.

Regional performance varied significantly, with Asia-Pacific showing double-digit organic growth driven by China, while Europe, Middle East and Africa (EMEA) experienced double-digit declines amid continued broad industrial weakness.

The decline in adjusted EBITDA to $208 million was primarily attributed to lower organic volume, unfavorable mix, higher manufacturing costs, and currency headwinds. These negative factors were partially offset by cost reduction actions and the benefit of acquisitions.

Segment Analysis

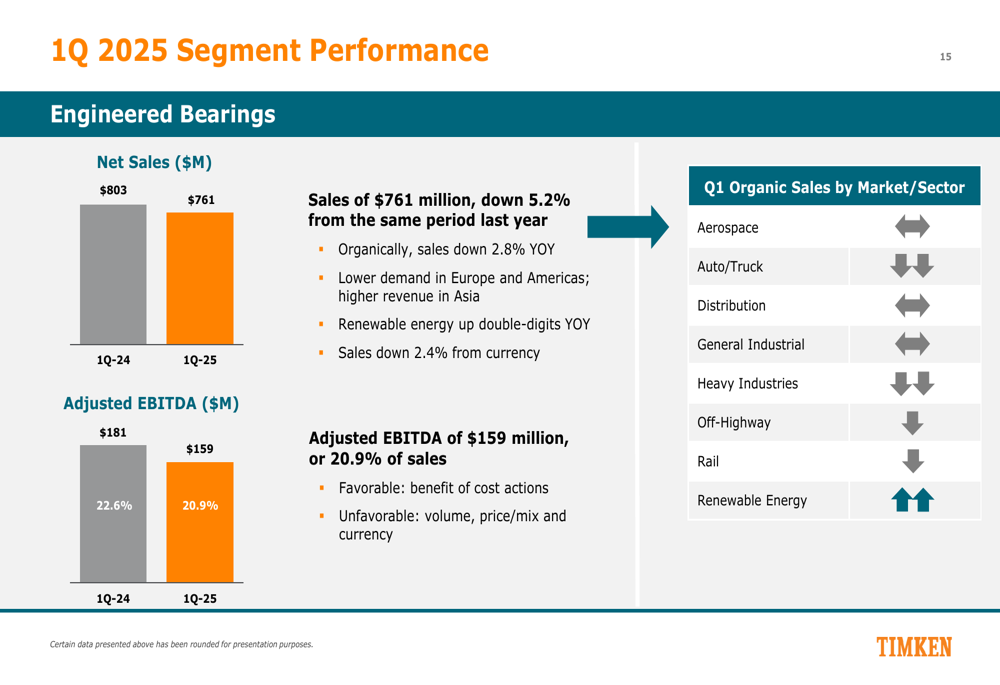

Timken’s Engineered Bearings segment, which represents approximately two-thirds of total revenue, reported sales of $761 million, down 5.2% year-over-year. Organic sales declined 2.8%, with adjusted EBITDA of $159 million representing a margin of 20.9%.

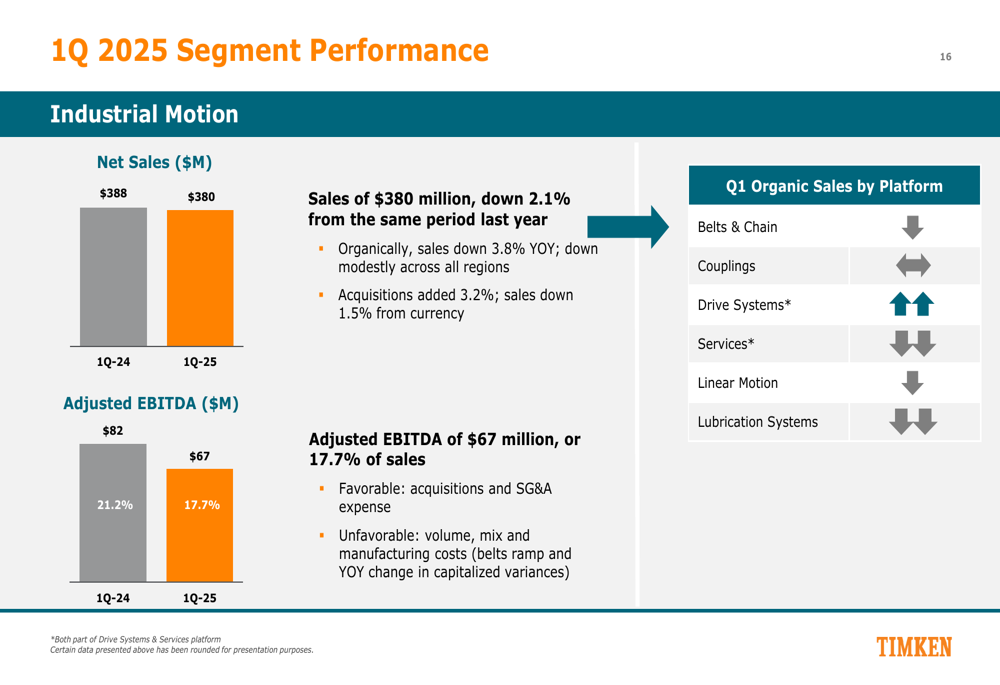

The Industrial Motion segment fared slightly better with sales of $380 million, down 2.1% from the prior year. Organic sales decreased 3.8%, while adjusted EBITDA came in at $67 million with a margin of 17.7%.

Revised 2025 Outlook

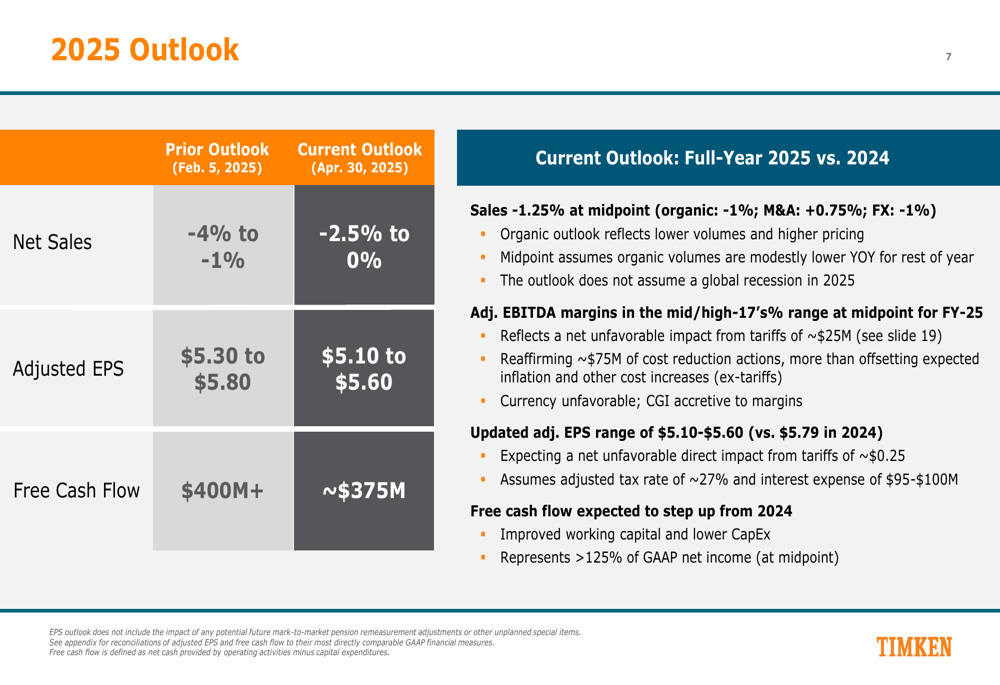

Timken revised its full-year 2025 outlook, slightly improving its sales forecast while reducing earnings and free cash flow expectations. The company now projects net sales to decline between 2.5% and 0%, compared to its previous guidance of -4% to -1%. However, adjusted EPS guidance was lowered to $5.10-$5.60 from $5.30-$5.80, and free cash flow is now expected to be approximately $375 million, down from the previous target of $400+ million.

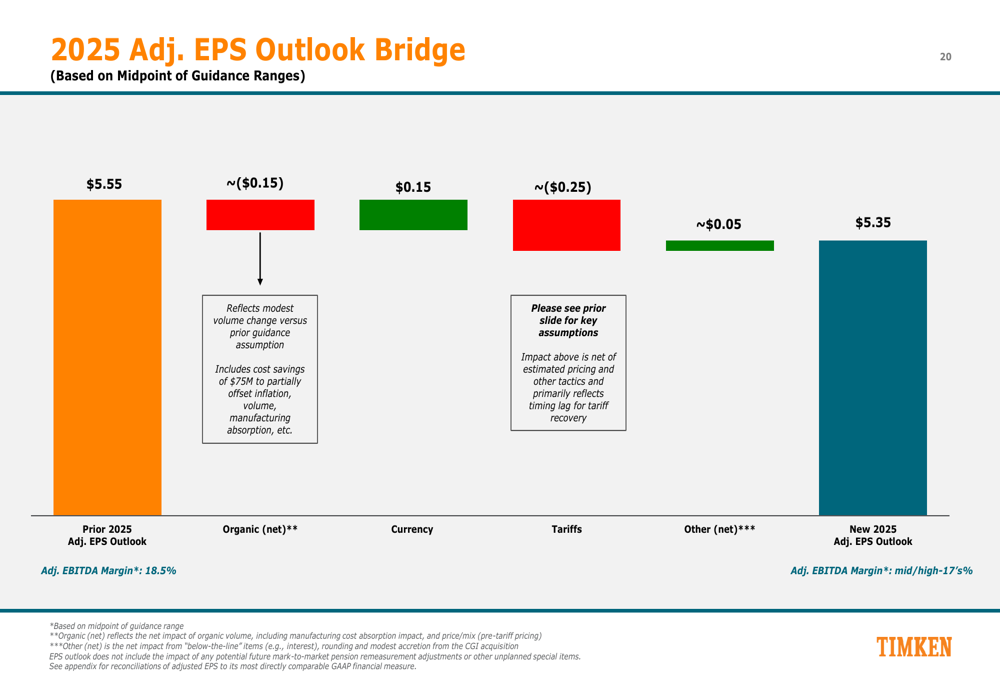

The company provided a detailed bridge analysis explaining the $0.20 reduction in its midpoint adjusted EPS outlook. Organic factors resulted in approximately $0.15 of negative impact, while tariffs are expected to create a $0.25 headwind. These negative factors are partially offset by favorable currency impacts of $0.15 and other net positive factors of $0.05.

Strategic Initiatives

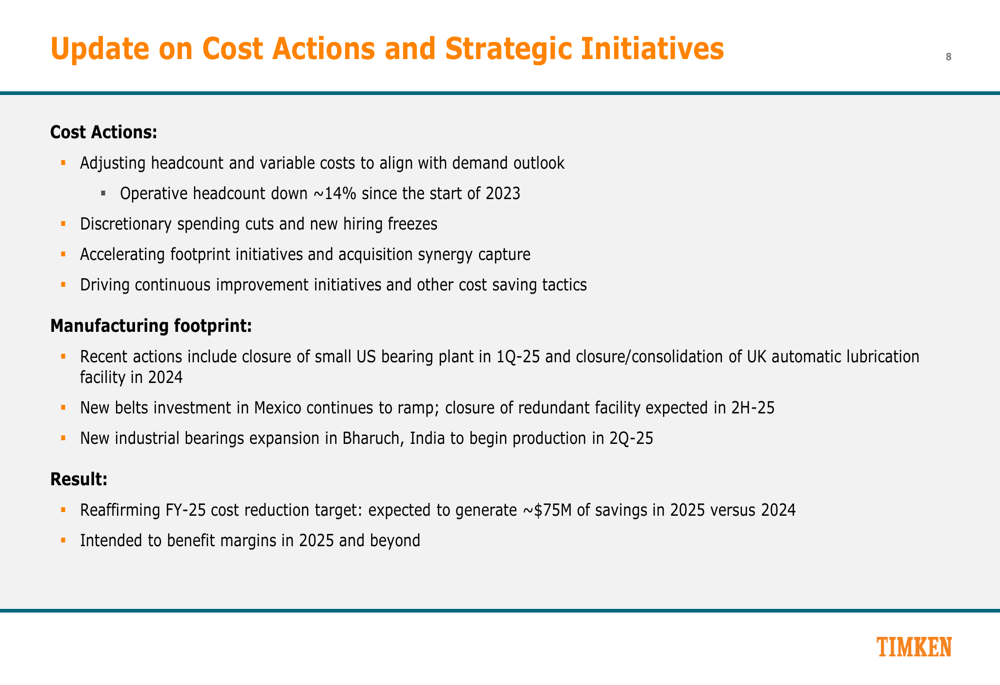

Timken is implementing significant cost actions to improve profitability in the challenging environment. The company has reduced operative headcount by approximately 14% since the start of 2023 and is accelerating footprint initiatives.

Key manufacturing footprint actions include the closure of a small U.S. bearing plant, consolidation of a UK lubrication facility, new belts investment in Mexico, and expansion in Bharuch, India. Through these initiatives, Timken reaffirmed its fiscal year 2025 cost reduction target of approximately $75 million in savings versus 2024.

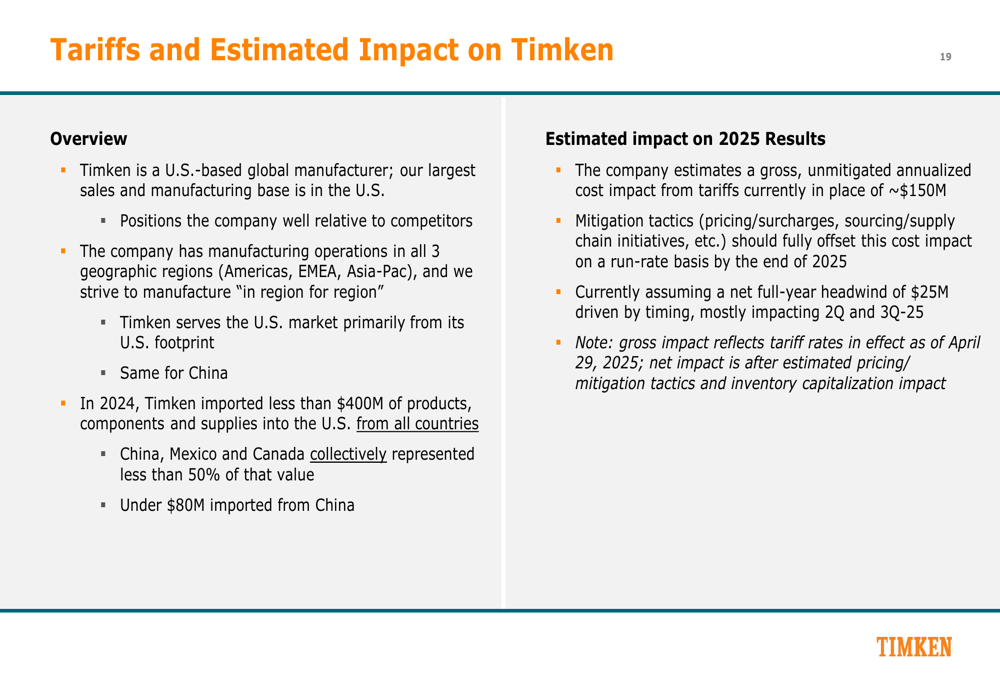

The company is also actively addressing tariff impacts, which represent a significant challenge. Timken estimates a gross annualized cost impact from tariffs of approximately $150 million but expects mitigation tactics to fully offset this on a run-rate basis by the end of 2025. For the current year, the company is assuming a net full-year headwind of $25 million due to timing of implementation.

Capital Allocation and Cash Flow

Despite the challenging environment, Timken demonstrated improved cash flow generation with first quarter free cash flow of $23.4 million, compared to $5.2 million in the prior-year period. This improvement came from higher net cash from operations ($58.6 million vs. $49.3 million) and lower capital expenditures ($35.2 million vs. $44.1 million).

The company continues to maintain a balanced approach to capital allocation, focusing on significant free cash flow generation in 2025, pursuing accretive M&A opportunities, and considering share repurchases as an attractive option.

Market Context

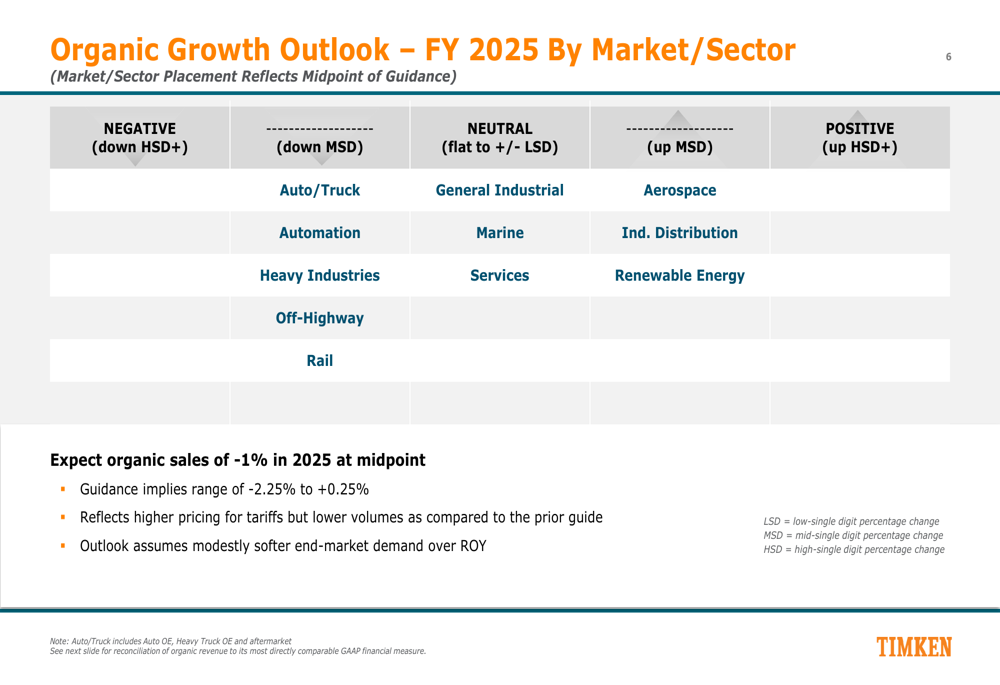

Timken’s organic growth outlook for fiscal year 2025 varies significantly by market sector. The company expects negative growth (down high single digits or more) in several sectors including Auto/Truck, Heavy Industries, Off-Highway, Rail, Automation, Marine, and Services. General Industrial is projected to be neutral (flat to +/- low single digits), while Aerospace, Industrial Distribution, and Renewable Energy are expected to show positive growth (up high single digits or more).

The company’s near-term strategic priorities focus on driving operational excellence, mitigating tariff impacts, advancing organic outgrowth, and integrating acquisitions. These initiatives are designed to help Timken navigate the current challenging environment while positioning for future growth.

This mixed performance and cautious outlook align with trends observed in Timken’s previous quarter, where the company also faced challenges in certain sectors while maintaining strong margins and focusing on cost-saving measures.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.