September looms as a risk month for stocks, Yardeni says

Introduction & Market Context

The Timken Company (NYSE:TKR) released its second-quarter 2025 earnings presentation on July 30, revealing a 0.8% year-over-year decline in sales to $1.17 billion, with organic revenue down 2.5%. The industrial manufacturer narrowed its full-year adjusted EPS guidance while maintaining its cautious outlook on second-half demand.

The presentation comes as Timken’s stock has shown some recovery from earlier lows, closing at $80.98 on July 29, 2025, down 0.87% for the day. The company’s shares have traded between $56.20 and $90.49 over the past 52 weeks, suggesting volatility amid challenging industrial market conditions.

Quarterly Performance Highlights

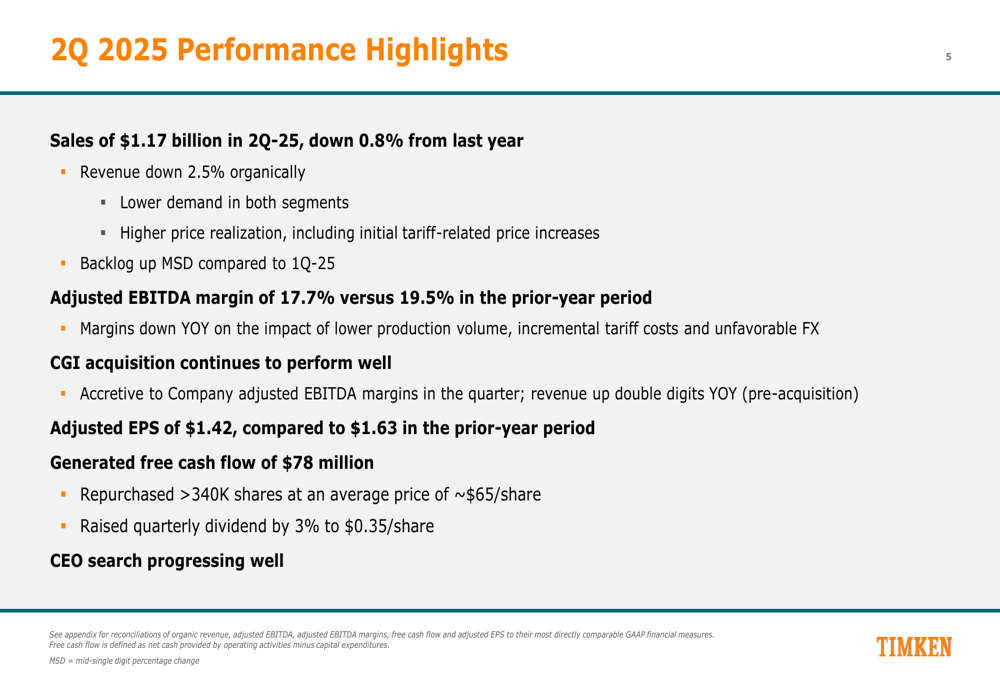

Timken reported adjusted EBITDA of $208 million in Q2 2025, representing a margin of 17.7%, down 180 basis points from 19.5% in the same period last year. Adjusted earnings per share came in at $1.42, compared to $1.63 in Q2 2024, reflecting a 13% decline.

As shown in the following performance highlights slide, the company generated $78 million in free cash flow during the quarter and continued its shareholder return initiatives by repurchasing over 340,000 shares at an average price of approximately $65 per share:

The decline in adjusted EBITDA was primarily attributed to incremental tariff costs ($14 million), lower organic volume, unfavorable mix, manufacturing performance issues, and currency headwinds. These negative factors were partially offset by higher pricing and the benefit of the CGI acquisition.

Regional and Segment Performance

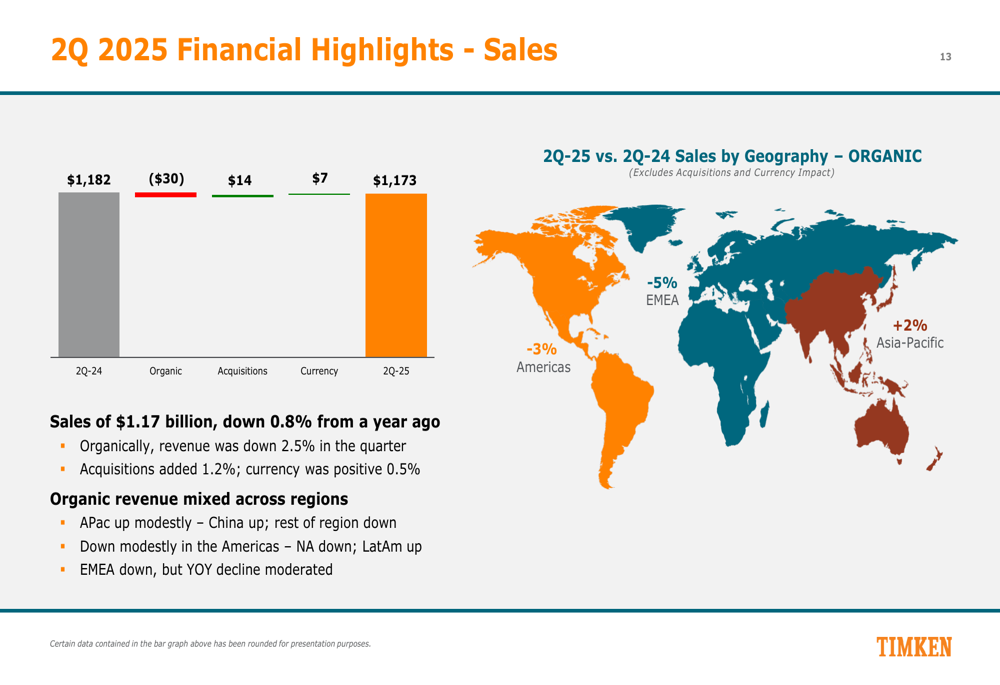

Timken’s organic revenue performance varied by region, with Asia-Pacific showing modest growth (+2%), while the Americas declined slightly (-3%) and EMEA experienced a more significant drop (-5%), though the company noted the year-over-year decline in Europe had moderated. The following slide illustrates this regional performance:

In the Engineered Bearings segment, sales decreased slightly to $777 million from $783 million in Q2 2024, with organic sales down 0.8%. Adjusted EBITDA for this segment fell to $153 million (19.7% margin) from $166 million (21.2% margin) in the prior year.

The Industrial Motion segment reported sales of $396 million, down from $399 million in Q2 2024, with a more pronounced organic sales decline of 5.9%. Adjusted EBITDA for this segment decreased to $73 million (18.3% margin) from $80 million (20.0% margin) in the prior year.

Strategic Focus on Automation

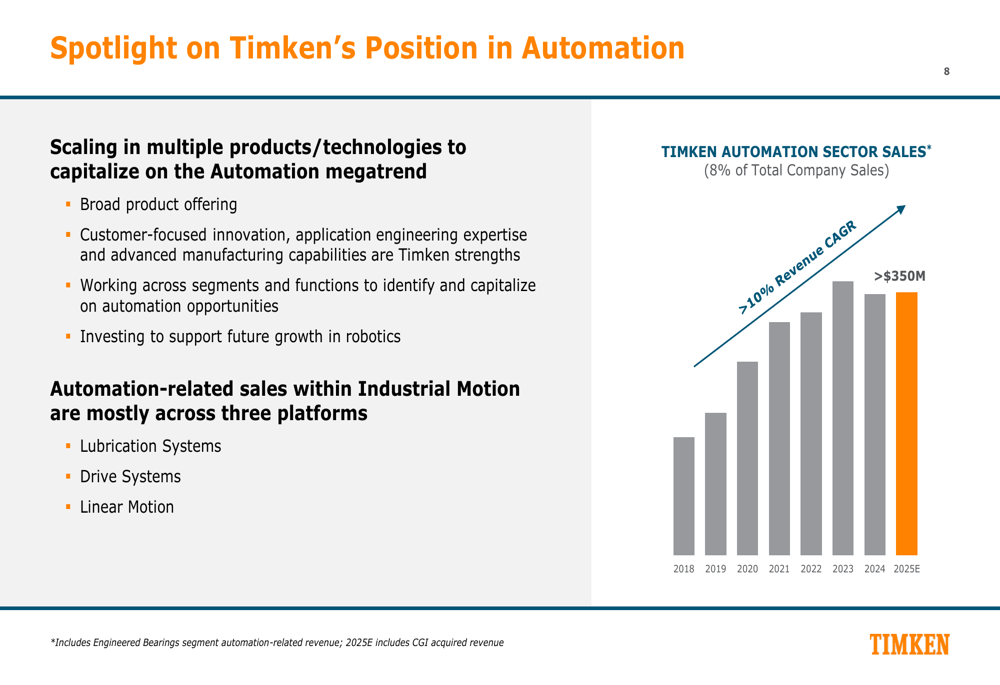

Despite the overall revenue challenges, Timken highlighted its growing position in the automation sector, which represents a strategic growth opportunity. The company is scaling multiple products and technologies to capitalize on this megatrend, leveraging its broad product offering, customer-focused innovation, and application engineering expertise.

The following slide demonstrates Timken’s automation strategy, showing a revenue CAGR exceeding 10% to reach over $350 million by 2025:

Timken is focusing on higher-growth applications within automation, including industrial robotics, factory/warehouse automation, autonomous guided vehicles, medical robotics, and humanoids. The company’s diverse portfolio of brands positions it well to address these growing markets:

Financial Outlook

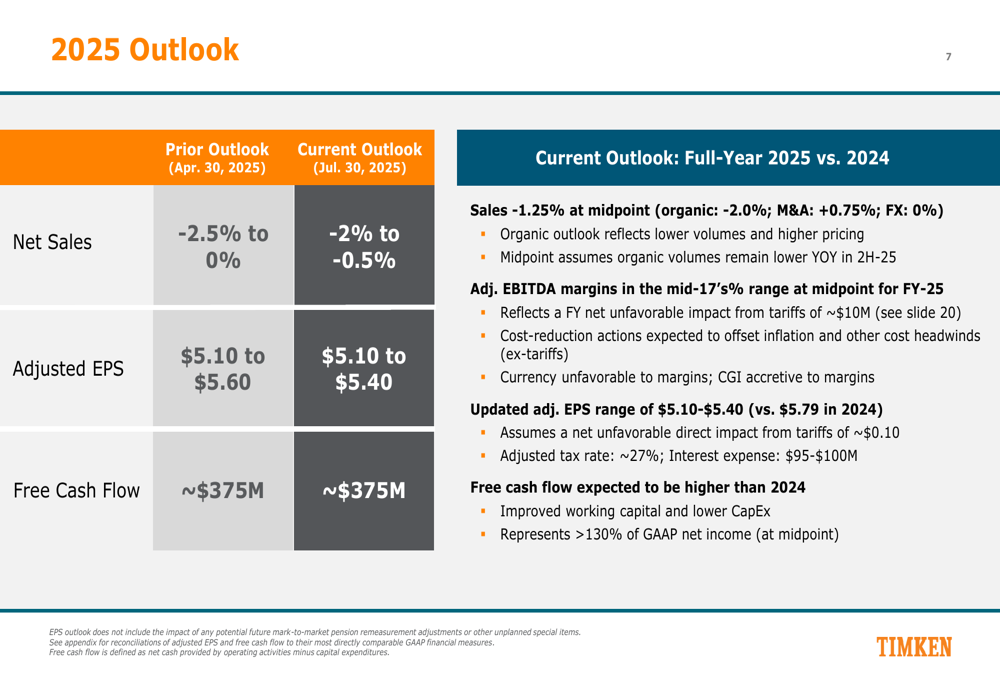

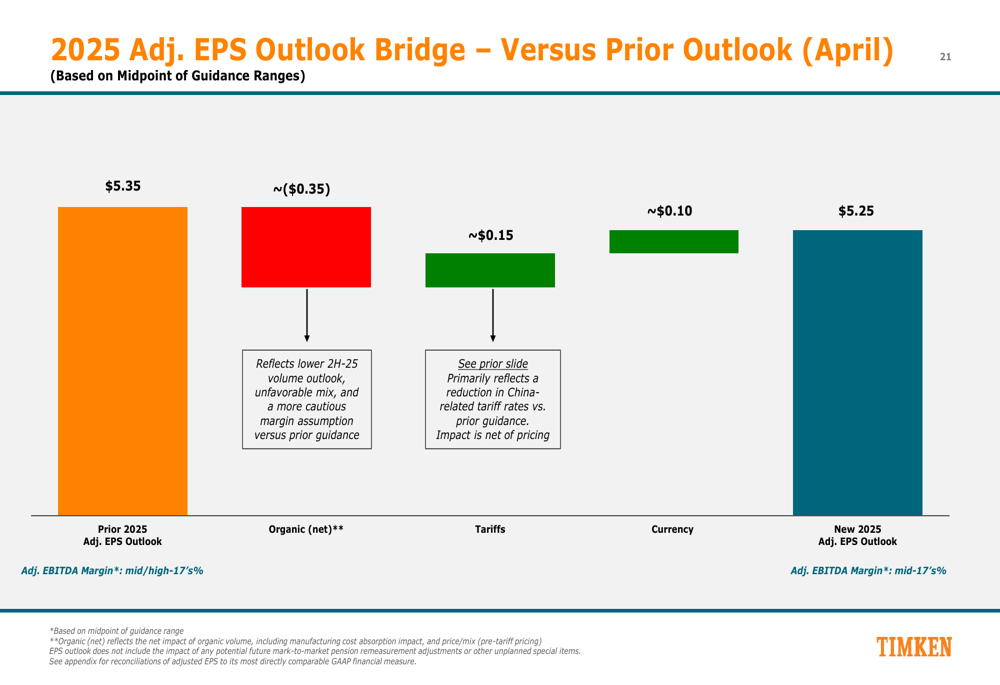

Timken updated its full-year 2025 guidance, narrowing its adjusted EPS range to $5.10-$5.40 from the previous $5.10-$5.60. The company now expects net sales to decline between 2% and 0.5% for the year, a slight improvement from its prior guidance of -2.5% to 0%.

The updated outlook reflects a cautious view on second-half demand, with organic revenue projected to decline 2.0% at the midpoint for the full year. The company continues to expect free cash flow of approximately $375 million, which would represent an increase from 2024.

As shown in the following outlook slide, Timken expects adjusted EBITDA margins in the mid-17% range for the full year:

The company noted that its updated EPS guidance assumes a net unfavorable direct impact from tariffs of approximately $0.10 per share. Timken provided additional context on the tariff situation, noting that as a U.S.-based global manufacturer with its largest sales and manufacturing base in the U.S., it is well-positioned relative to competitors to manage these challenges.

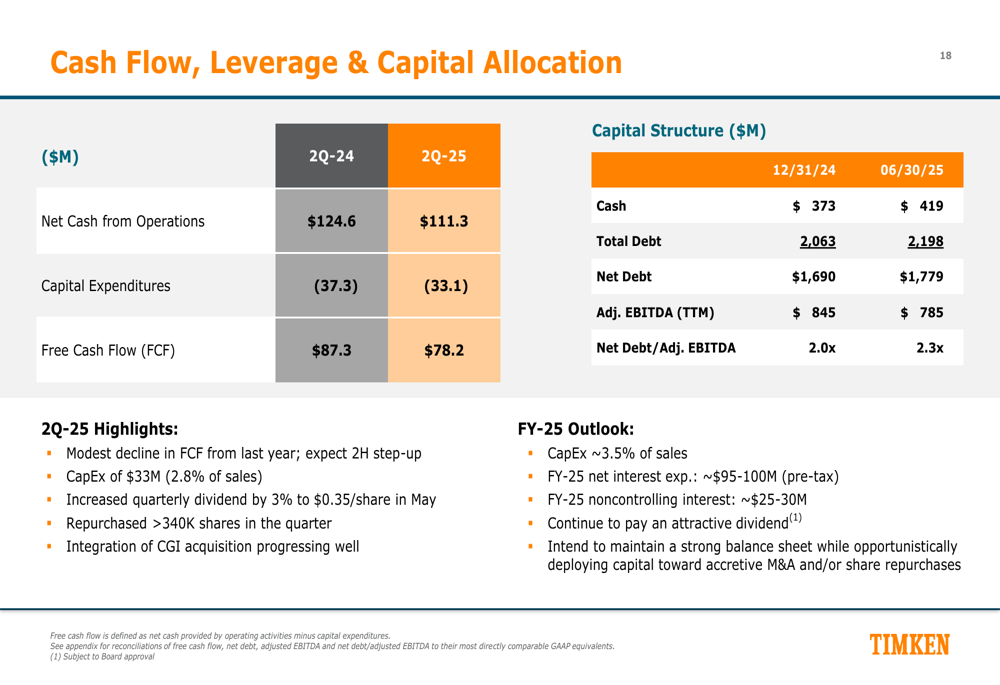

Cash Flow and Capital Allocation

Timken’s balance sheet remains solid with a net debt to adjusted EBITDA ratio of 1.9x as of June 30, 2025. The company generated $78 million in free cash flow during Q2 and expects a stronger second half for cash generation.

The following slide details Timken’s cash flow, leverage, and capital allocation priorities:

During the quarter, Timken raised its quarterly dividend by 3% to $0.35 per share, reflecting confidence in its long-term cash generation capabilities. The company also noted that its CEO search is progressing well, though no specific timeline was provided for naming a successor.

Looking Ahead

Timken’s near-term strategic priorities include driving operational excellence, mitigating tariff impacts, positioning for an anticipated industrial market expansion in 2026, and advancing organic outgrowth initiatives. The company expects to deliver resilient performance in 2025 despite the challenging environment.

The EPS outlook bridge below shows how Timken’s guidance has evolved since its previous outlook in April, with organic factors and tariff impacts contributing to the adjustment:

While facing headwinds in several traditional industrial markets, Timken continues to emphasize its strategic positioning in growth sectors like automation and renewable energy, which could provide momentum as the broader industrial market recovers.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.