60%+ returns in 2025: Here’s how AI-powered stock investing has changed the game

Introduction & Market Context

Tobii AB (OTC:TOBII) delivered its first-ever EBIT positive first quarter, according to the company’s Q1 2025 earnings presentation released on May 7, 2025. The eye-tracking technology specialist reported significant year-over-year improvements in profitability and cash flow, driven by successful cost reduction initiatives and strong performance in key business segments.

The company’s stock has recently shown positive momentum, rising 7.84% to $2.20 in the most recent trading session, reflecting growing investor confidence in Tobii’s turnaround strategy. This comes after a challenging period following Q4 2024 results, when the stock experienced a significant decline despite positive financial performance.

Quarterly Performance Highlights

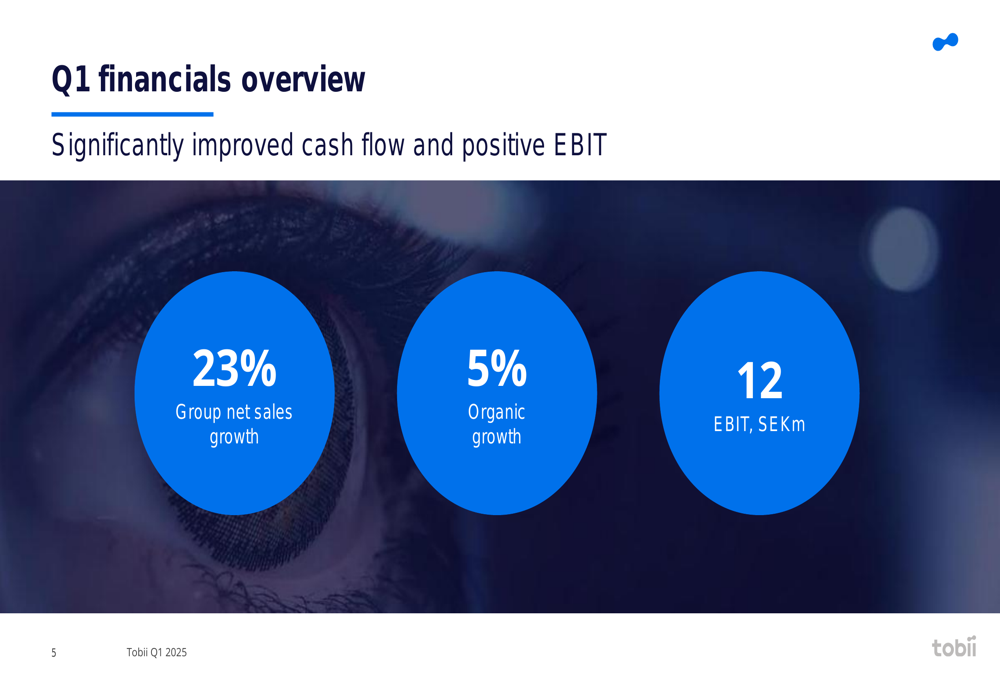

Tobii reported robust top-line growth with group net sales increasing 23% year-over-year, including 5% organic growth. The company achieved an EBIT of 12 million SEK, a substantial improvement from the -65 million SEK reported in Q1 2024.

As shown in the following financial overview:

The company’s gross margin remained strong at 77%, slightly down from 79% in Q1 2024 but still indicating healthy pricing power. Most notably, Tobii achieved an EBIT margin of 6%, compared to -39% in the same period last year, demonstrating significant progress in its path to sustainable profitability.

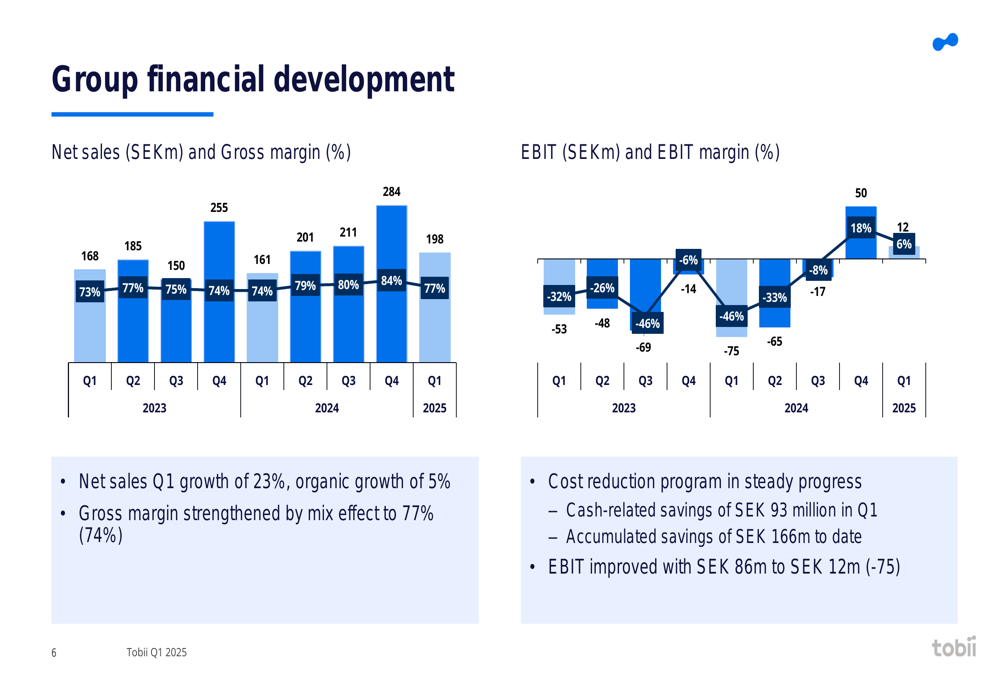

The detailed financial development chart further illustrates this positive trajectory:

Detailed Financial Analysis

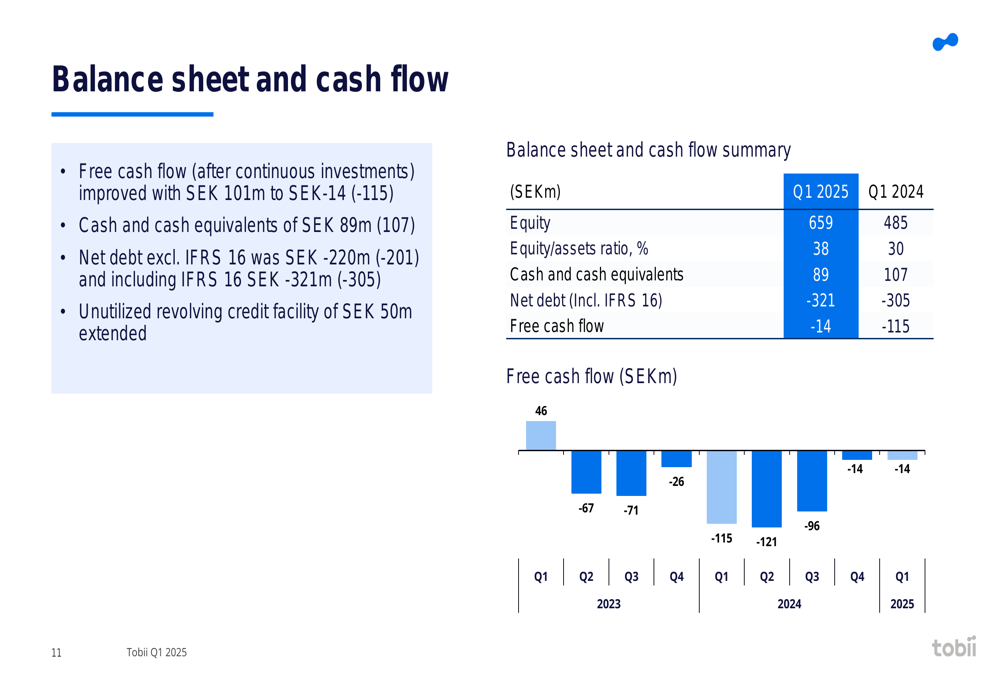

Tobii’s financial transformation is particularly evident in its cash flow performance. Free cash flow improved by 101 million SEK year-over-year to -14 million SEK, compared to -115 million SEK in Q1 2024. This improvement reflects both better operational performance and disciplined capital management.

The company reported cash and cash equivalents of 89 million SEK, down from 107 million SEK in Q1 2024. Net debt including IFRS 16 stood at -321 million SEK compared to -305 million SEK a year earlier. The equity/assets ratio improved to 38% from 30% in Q1 2024, indicating a strengthening balance sheet.

As shown in the balance sheet and cash flow summary:

The company has also secured an extension of its unutilized revolving credit facility of 50 million SEK, providing additional financial flexibility as it continues its transformation journey.

Segment Performance Analysis

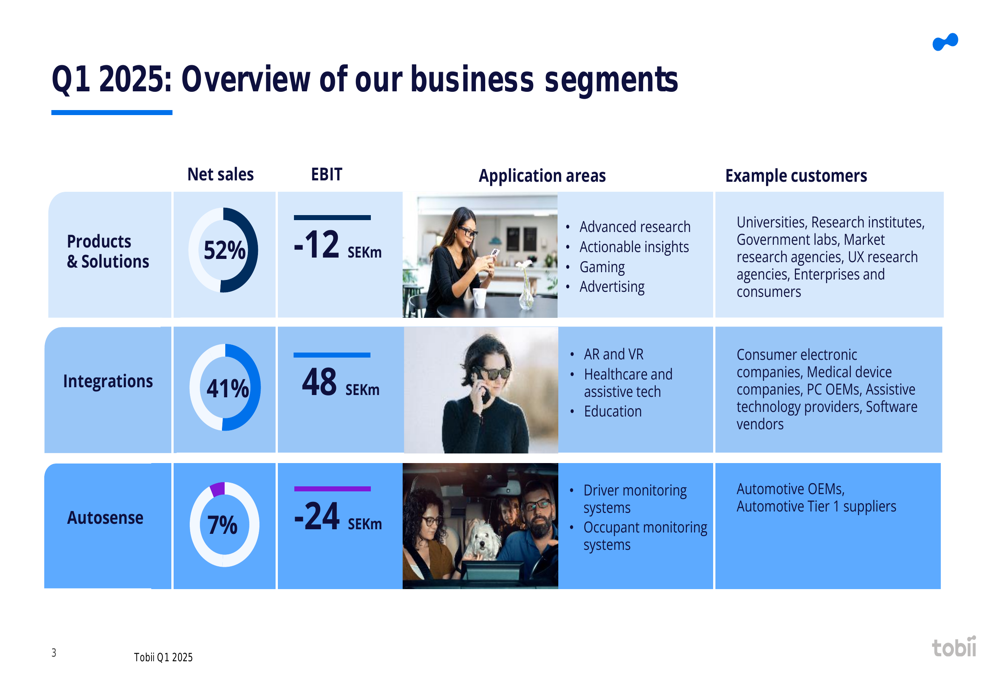

Tobii’s business is divided into three segments, each showing distinctly different performance trajectories:

The Integrations segment emerged as the star performer, contributing 41% of net sales with 23% organic growth and generating an EBIT of 48 million SEK. This segment benefited from non-recurring imaging-related revenue, which contributed 65% of its growth. The segment maintained an impressive gross margin of 91%, though slightly down from 96% in the previous year.

The Autosense segment, while still the smallest at 7% of net sales, showed remarkable growth with organic sales increasing 114% year-over-year. Despite this growth, the segment remained EBIT negative at -24 million SEK, though this represents a significant improvement from -38 million SEK in Q1 2024.

In contrast, the Products & Solutions segment, which accounts for 52% of net sales, experienced an 8% organic decline and posted an EBIT of -12 million SEK. While still negative, this represents an improvement from -23 million SEK in Q1 2024.

Strategic Initiatives

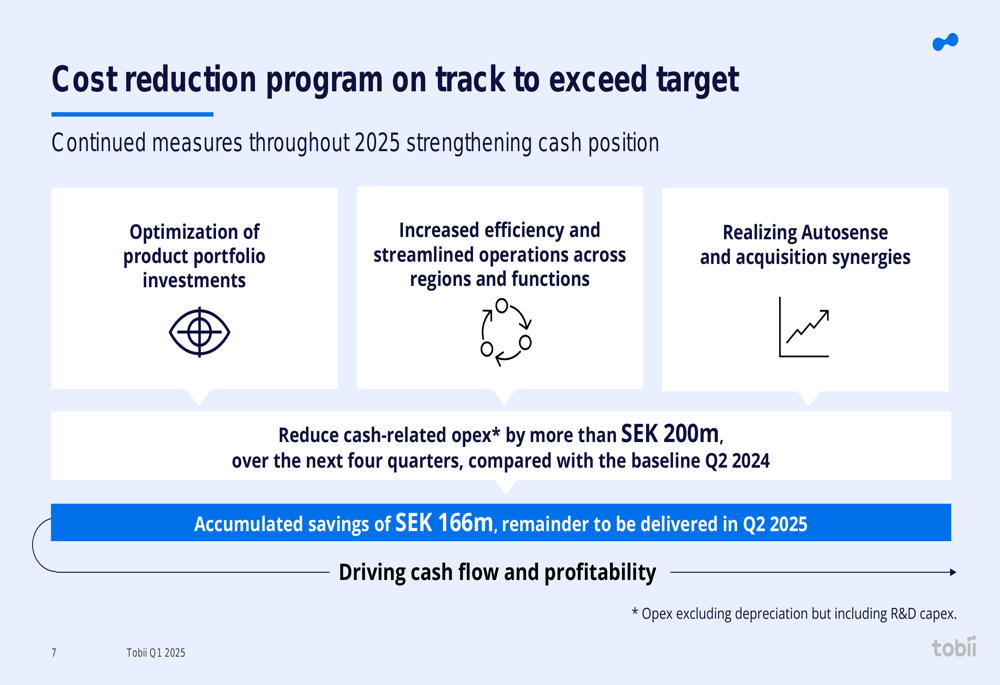

A key driver of Tobii’s improved financial performance is its comprehensive cost reduction program, which has already delivered substantial results:

The program focuses on optimizing product portfolio investments, increasing efficiency across regions and functions, and realizing synergies from Autosense and acquisitions. Tobii reported accumulated savings of 166 million SEK to date, with the remainder of its target of over 200 million SEK expected to be delivered in Q2 2025.

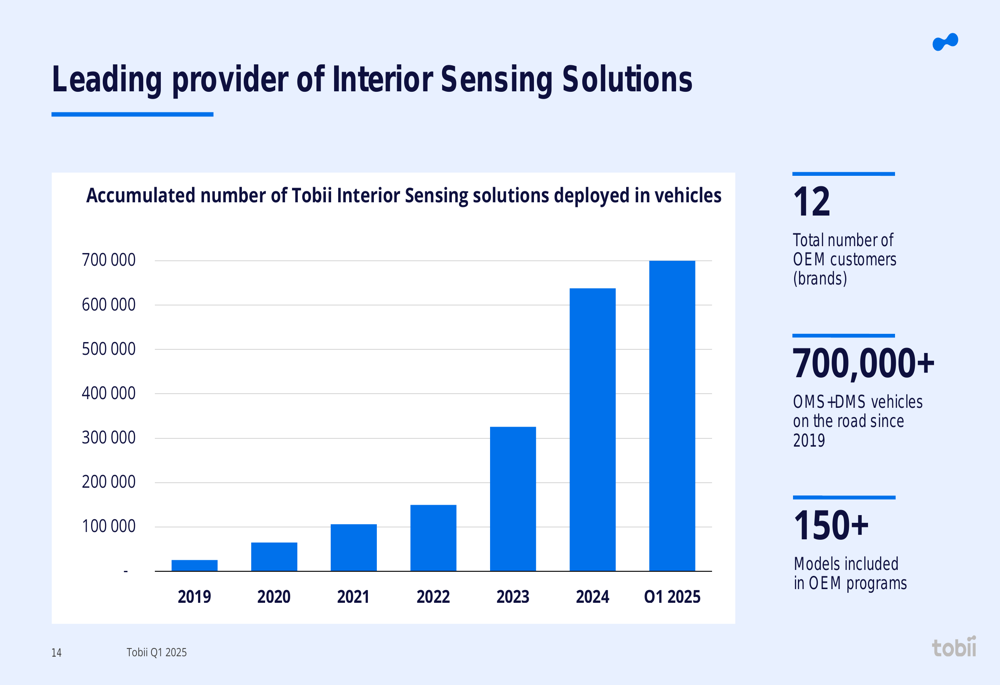

In the Autosense division, Tobii continues to build credibility in the automotive sector:

The company has deployed over 700,000 interior sensing solutions in vehicles since 2019, with more than 150 models included in OEM programs. Tobii now counts 12 OEM customers (brands) among its clients, positioning it as a leading provider in this growing market segment.

Forward-Looking Statements

Looking ahead, Tobii management expressed confidence in the company’s trajectory, noting sustained progress on profitability and liquidity. The company reported limited impact from macroeconomic uncertainties in Q1 and has implemented additional cost reductions for the second half of 2025.

Management expects a strengthened cash position in Q2 to meet near-term liabilities and is pursuing strategic initiatives aimed at improving mid- and long-term financial positioning. The company appears well-positioned to continue its transformation from a growth-focused technology company to one with sustainable profitability.

For the Autosense segment specifically, Tobii highlighted that ongoing OEM programs advanced solidly in Q1 toward Start of Production (SOP). The company received EU homologation for its Driver Monitoring System (DMS) in a commercial vehicle program and achieved ASPICE CL2 validation for a program with a leading German passenger car OEM, further validating its technology and approach in this competitive market.

As Tobii moves through 2025, investors will be watching closely to see if the company can maintain its positive momentum and deliver on its cost reduction and profitability targets while continuing to grow its strategic business segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.