After-hours movers: AMD, Pinterest, CAVA Group, Toast, and more

Introduction & Market Context

Tomra Systems ASA (OB:TOM) presented its first quarter 2025 results on May 7, 2025, revealing a 5% year-over-year revenue increase to €306 million, despite facing headwinds in some business segments. The company’s stock closed at 164.3 on May 6, down 1.85% ahead of the results announcement, reflecting cautious investor sentiment.

The presentation comes after a strong fourth quarter 2024, which saw record revenues of €398 million. The sequential decline from Q4 to Q1 follows typical seasonal patterns, while maintaining year-over-year growth momentum. The Norwegian recycling and food sorting technology company continues to navigate a complex global market environment characterized by regional variations in demand and ongoing macroeconomic uncertainties.

Quarterly Performance Highlights

Tomra reported solid financial performance in Q1 2025, with total revenues reaching €306 million compared to €291 million in Q1 2024. Gross margin improved significantly to 43%, up from 40% in the same period last year, driven by margin improvements in the Collection segment and higher volumes combined with cost savings in the Food segment.

EBITA increased substantially to €26 million from €15 million in Q1 2024 (adjusted for special items), resulting in an EBITA margin improvement to 8% from 5%. The company also demonstrated strong cash generation capabilities, with cash flow from operations reaching €65 million, more than tripling from €19 million in Q1 2024.

As shown in the following financial highlights from the presentation:

Segment Analysis

The company’s performance varied significantly across its three main business segments: Collection, Recycling, and Food.

The Collection segment, which represents the largest portion of Tomra’s business, saw revenues decline slightly to €185 million, down 2% from €189 million in Q1 2024. This decrease was primarily due to a slowdown in Austria following the Deposit Return System (DRS) launch on January 1, 2025. However, the company reported revenue growth in all regions except Europe (excluding Northern Europe) and highlighted record revenues in Romania. The segment also achieved improved gross and EBITA margins compared to the previous year.

The company successfully launched a DRS in Tasmania on May 1, 2025, and has several additional launches scheduled across multiple countries through 2027, including Poland (October 2025), Greece (December 2025), and eventually the United Kingdom (TADAWUL:4280) (October 2027).

The Collection business update illustrates these developments:

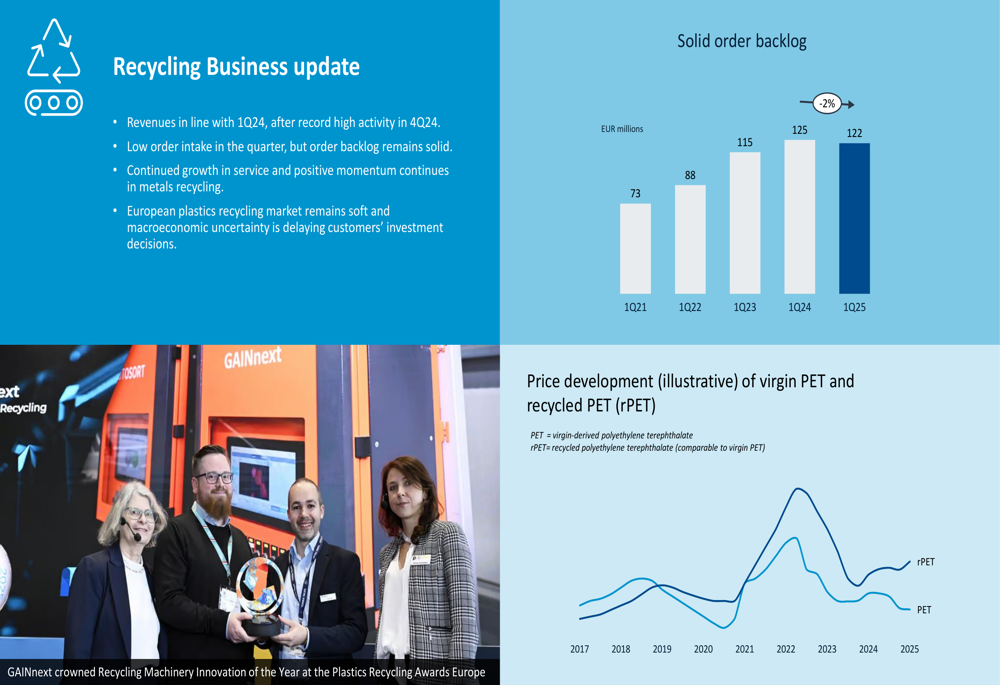

The Recycling segment maintained stable revenues at €46 million, unchanged from Q1 2024, following record high activity in Q4 2024. However, order intake was lower at €61 million compared to €73 million in Q1 2024, though the order backlog remained solid at €122 million. The European plastics recycling market continues to face challenges, with macroeconomic uncertainty delaying customers’ investment decisions.

The following chart illustrates the recycling business performance and market dynamics:

The Food segment emerged as the growth driver for Tomra in Q1 2025, with revenues increasing by 16% to €70 million from €60 million in Q1 2024. The segment saw strong growth in Europe and South America, with profitability improving according to plan. Order intake grew by 13% to €87 million, driven by vegetables and potatoes, and the order backlog increased to €125 million from €118 million in Q1 2024.

The Food segment’s performance is illustrated in this business update:

Strategic Initiatives and New Developments

Tomra continues to advance its strategic initiatives across multiple fronts. The company’s Horizon business, which focuses on new growth areas, reported progress in several key projects. TOMRA Feedstock’s Norwegian plant, named "Områ," is now in its commissioning phase. TOMRA Reuse continues with piloting, product development, and business development activities. Additionally, C-trace signed a contract with OLO Bratislava to enhance waste collection digitalization through integrated RFID tracking, fleet management, and automated route planning.

The company also addressed the potential impact of tariffs on its business, noting that approximately 15% of Tomra Group revenues are exposed to imports of goods to the United States. While first-order effects are limited to potential gross margin shortfalls, second-order effects include growth risks due to lower investments, FX risks, and opportunities to focus on supply security.

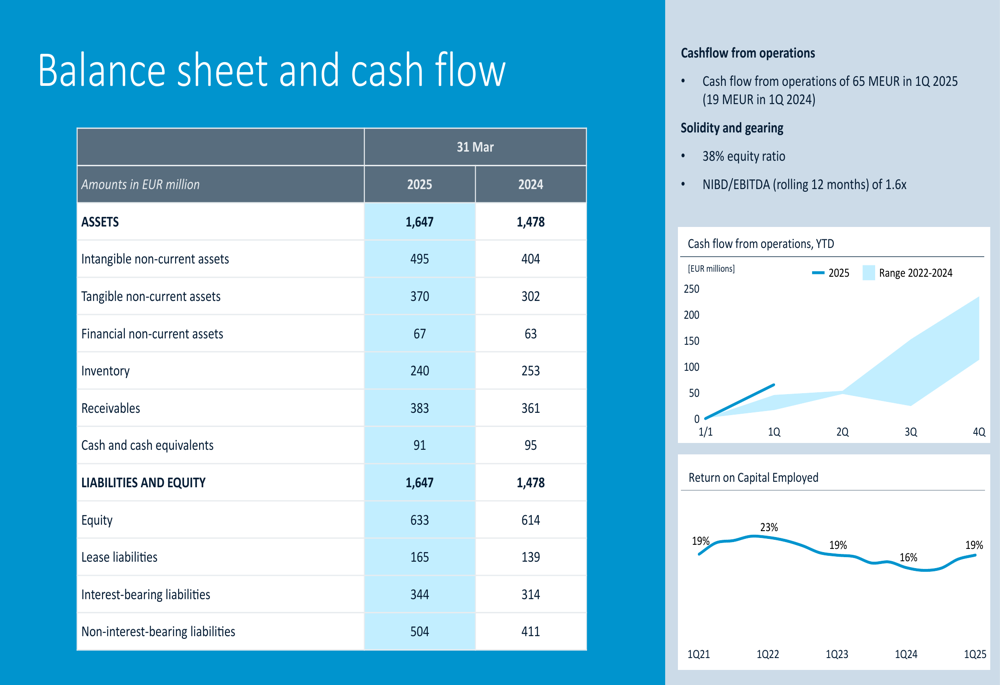

Financial Position and Balance Sheet

Tomra maintained a strong financial position in Q1 2025, with total assets of €1,647 million compared to €1,478 million in Q1 2024. The company’s equity stood at €633 million, representing an equity ratio well above the minimum 30% required by its financial covenant related to bank debt.

The company’s financial position is supported by a revolving credit facility of €150 million running until December 2027, with €143 million undrawn. Tomra’s weighted average debt maturity is 4.1 years, and its financial position is rated A- by Scope Ratings.

The following chart provides a detailed overview of the company’s balance sheet and cash flow:

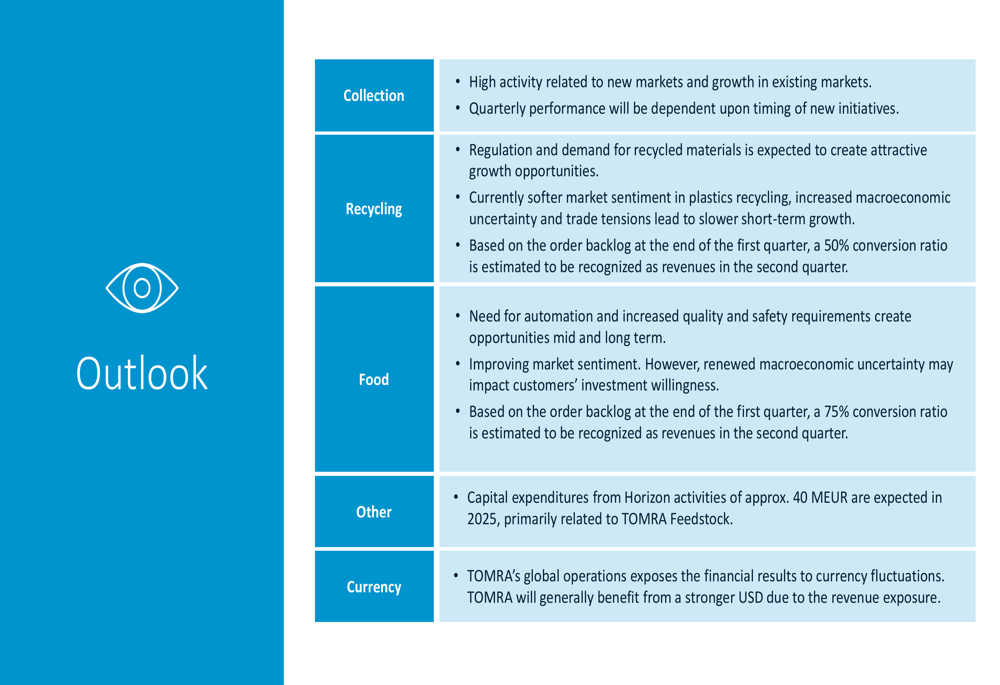

Outlook and Guidance

Looking ahead, Tomra provided a segment-specific outlook for the remainder of 2025. For the Collection segment, the company expects high activity related to new markets and continued growth in existing markets, though quarterly performance will depend on the timing of new initiatives.

In the Recycling segment, regulation and demand for recycled materials are expected to create attractive growth opportunities, though softer market sentiment and macroeconomic uncertainty may lead to slower short-term growth. Approximately 50% of the current order backlog is expected to be recognized as revenue in Q2 2025.

For the Food segment, automation and increased quality and safety requirements are creating mid and long-term opportunities. Market sentiment is improving, though macroeconomic uncertainty may impact customers’ willingness to invest. About 75% of the current order backlog is expected to be recognized as revenue in Q2 2025.

The company also noted that capital expenditures from Horizon activities are expected to be approximately €40 million in 2025, primarily related to TOMRA Feedstock. Currency fluctuations remain a factor, with a stronger USD generally benefiting Tomra due to its revenue exposure.

As shown in the company’s detailed outlook:

Tomra’s Q1 2025 results demonstrate the company’s ability to deliver growth and improved profitability despite mixed market conditions. With the Food segment emerging as a key growth driver and multiple DRS launches on the horizon, Tomra appears well-positioned to navigate current market challenges while pursuing long-term strategic initiatives in recycling, food sorting, and new business areas.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.