Nvidia among investors in xAI’s $20bn capital raise - Bloomberg News

Introduction & Market Context

TopBuild Corp (NYSE:BLD) released its first quarter 2025 financial results on May 6, revealing a 3.6% year-over-year sales decline amid persistent challenges in the residential construction market. The company reported that while commercial and industrial end markets posted solid growth, residential construction continues to face headwinds from affordability challenges, economic uncertainty, and weak consumer confidence.

"We delivered Q1 performance in line with expectations and are confirming our full year 2025 guidance," noted Robert Buck, President and CEO, in the company’s presentation. The company’s stock was trading at $296.72, up 1.62% following the presentation.

The quarterly results mark a significant shift from the company’s performance in late 2024, when TopBuild reported record sales and projected 2025 to be its tenth consecutive year of growth.

Quarterly Performance Highlights

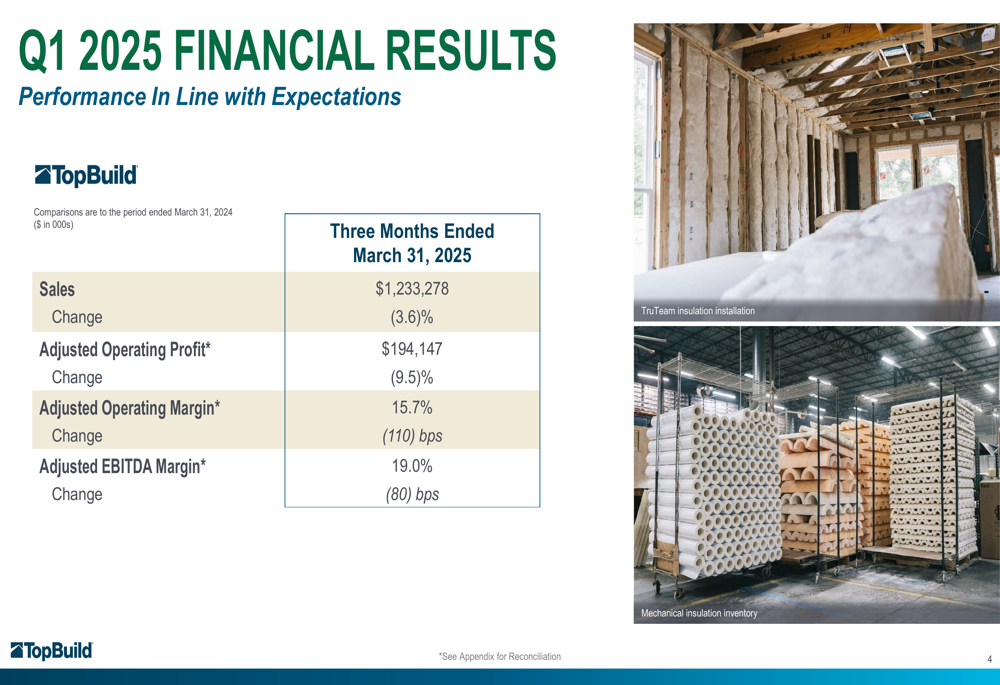

TopBuild reported Q1 2025 sales of $1.23 billion, down 3.6% compared to the same period last year. Adjusted operating profit fell 9.5% to $194.1 million, with adjusted operating margin contracting 110 basis points to 15.7%. Adjusted EBITDA margin decreased 80 basis points to 19.0%.

As shown in the following financial results summary:

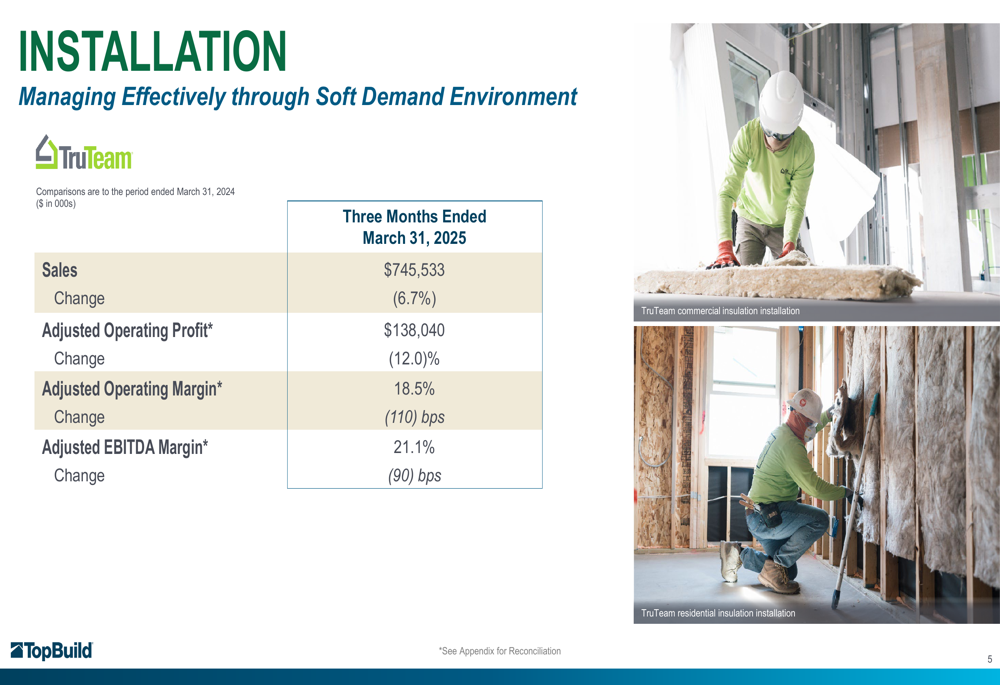

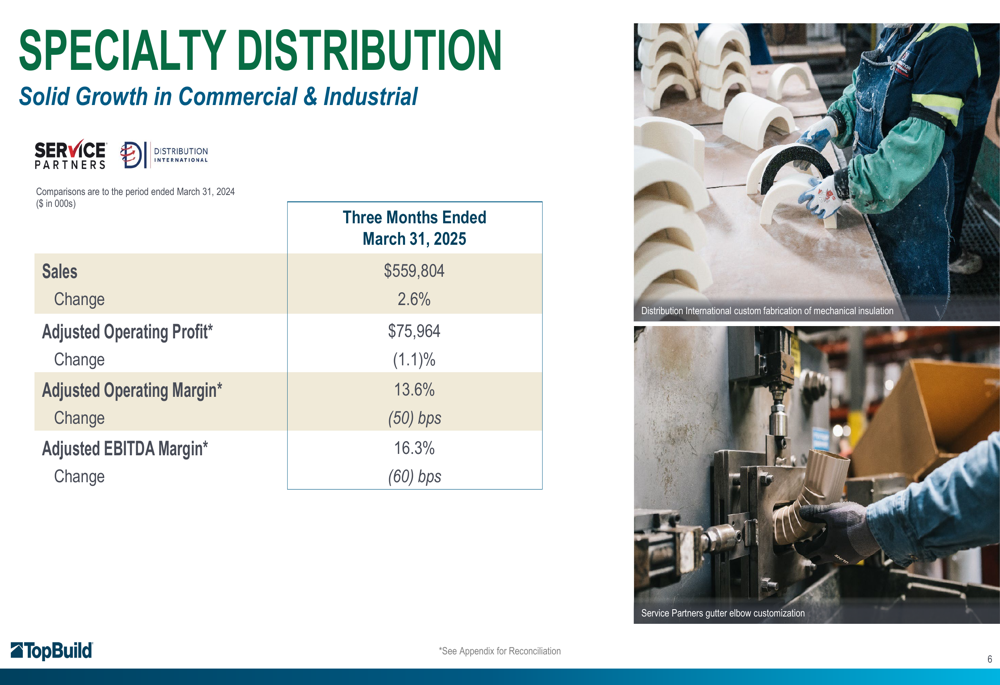

The company’s two business segments showed divergent performance. The Installation segment (TruTeam) reported sales of $745.5 million, down 6.7% year-over-year, with adjusted operating profit declining 12.0% to $138.0 million. Meanwhile, the Specialty Distribution segment demonstrated resilience with sales of $559.8 million, up 2.6% compared to Q1 2024, though adjusted operating profit still declined slightly by 1.1% to $76.0 million.

The segment performance breakdown illustrates this divergence:

Balance Sheet and Liquidity

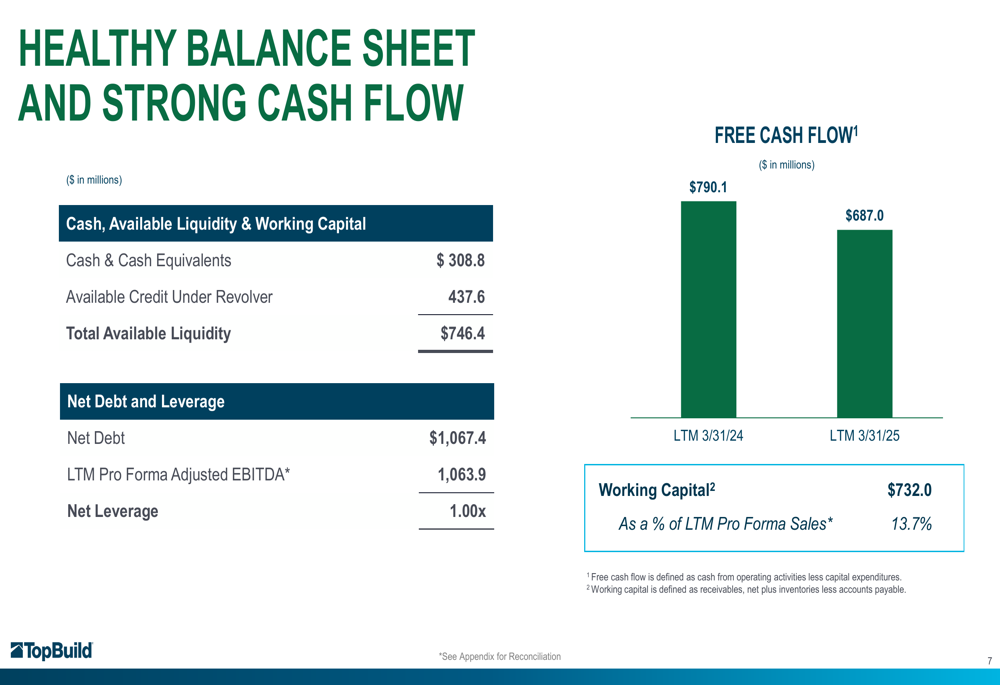

Despite challenging market conditions, TopBuild maintained a strong financial position. The company reported cash and cash equivalents of $308.8 million and total available liquidity of $746.4 million as of March 31, 2025. Net debt stood at $1.07 billion, representing a net leverage ratio of 1.00x, indicating conservative financial management.

Free cash flow for the trailing twelve months ended March 31, 2025, was $687.0 million, supporting the company’s capital allocation priorities. Working capital was $732.0 million, representing 13.7% of trailing twelve-month pro forma sales.

The following slide highlights the company’s financial strength:

Strategic Initiatives

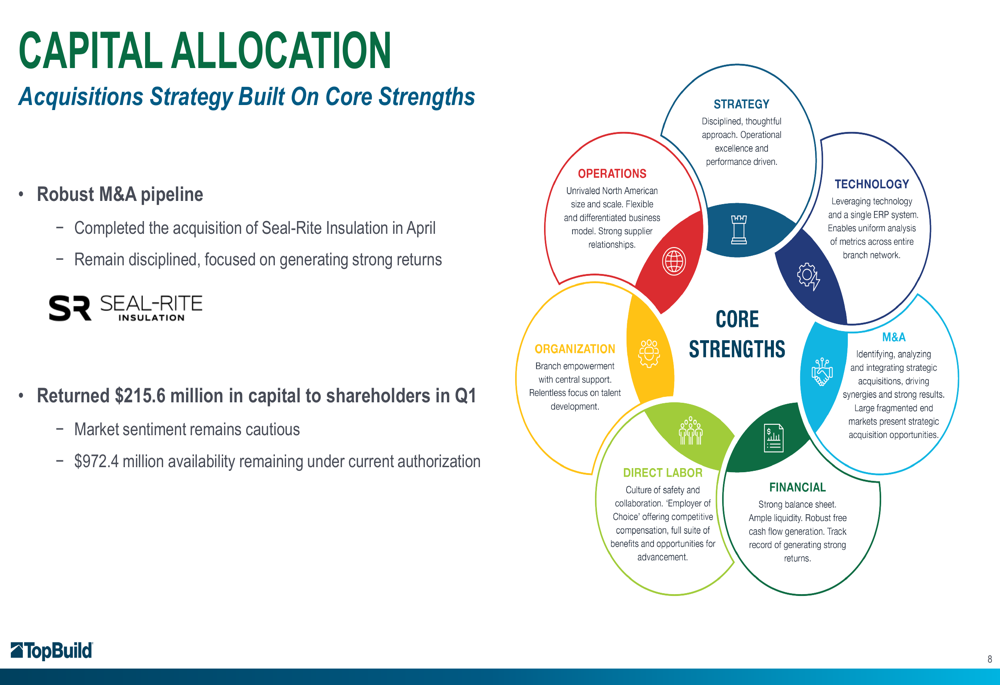

TopBuild emphasized its ongoing efforts to drive operational excellence, including optimization of its network footprint and headcount reduction to align with the current demand environment. The company continues to execute its disciplined capital allocation strategy, with M&A remaining the top priority.

In Q1, TopBuild returned $215.6 million to shareholders through its share repurchase program, demonstrating confidence in its long-term prospects despite near-term market challenges. The company also completed the acquisition of Seal-Rite Insulation in April 2025, adding to its robust M&A pipeline.

The company’s capital allocation strategy is built on core strengths as illustrated below:

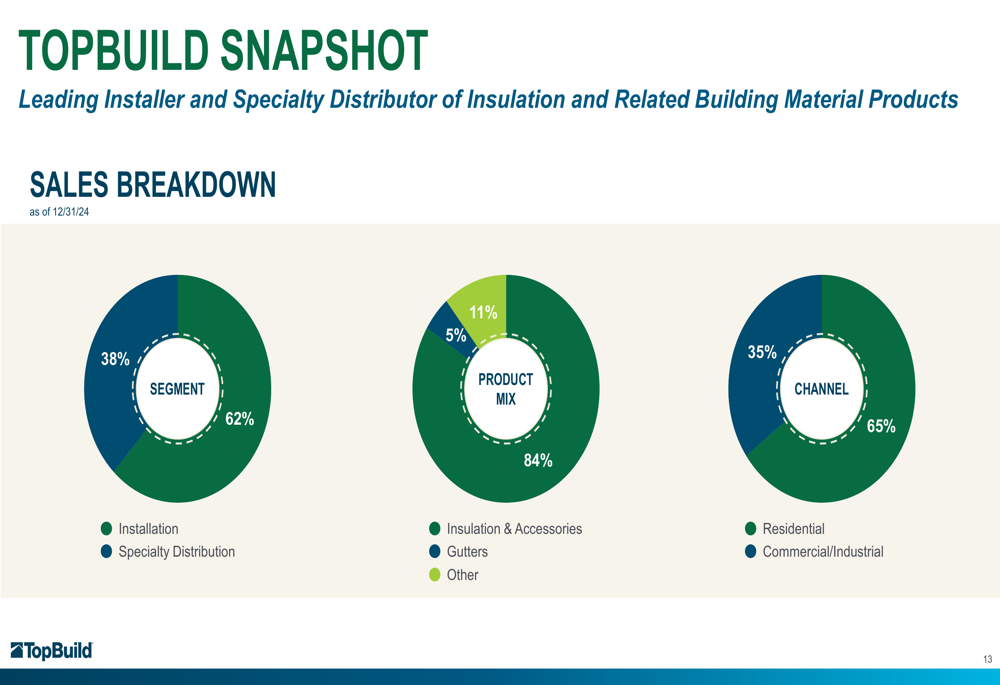

TopBuild’s diversified business model provides some insulation from residential market weakness. According to the company’s sales breakdown, 65% of revenue now comes from commercial and industrial channels, with 35% from residential. By segment, 38% of sales are from Installation and 62% from Specialty Distribution.

The following chart illustrates this diversification:

Forward-Looking Statements

Despite the challenging Q1 results, TopBuild confirmed its full-year 2025 guidance, projecting sales between $5.05 billion and $5.35 billion, and adjusted EBITDA between $925 million and $1.07 billion. The company expects residential markets to experience a high single-digit decline, while commercial and industrial markets are anticipated to deliver low single-digit growth.

The guidance reflects management’s confidence in the company’s ability to navigate the current market environment through operational discipline and strategic initiatives. M&A is expected to contribute approximately $85 million to sales in 2025.

The company’s outlook is summarized in the following slide:

TopBuild’s management emphasized that despite near-term challenges, underlying macro fundamentals support a long-term growth opportunity. The company’s addressable market remains substantial at approximately $18.25 billion, split across residential ($6.25 billion), building envelope ($6.25 billion), and mechanical ($5.75 billion) segments.

Competitive Industry Position

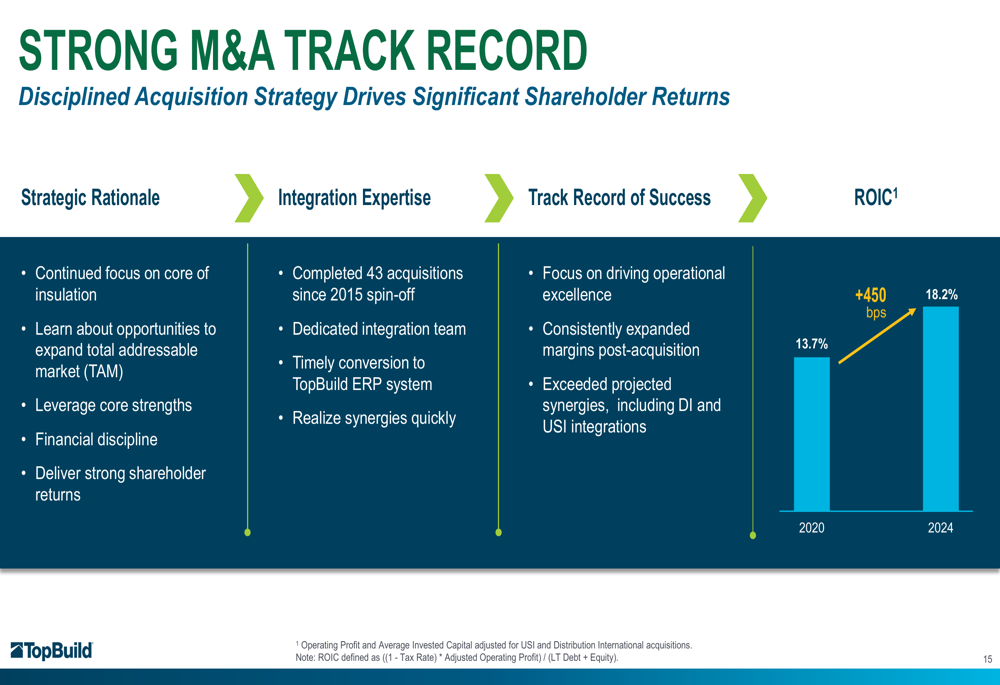

TopBuild has built a strong track record of strategic acquisitions, completing 43 deals since its 2015 spin-off. This M&A strategy has contributed to the company’s growth while maintaining disciplined financial management. The company’s return on invested capital (ROIC) has improved from 13.7% in 2020 to 18.2% in 2024, demonstrating effective capital allocation.

The company’s acquisition strategy and performance is illustrated in the following slide:

TopBuild’s diversified project portfolio across commercial building insulation and commercial/industrial mechanical insulation provides resilience against residential market fluctuations. The company highlighted significant projects including airport expansions, data centers, manufacturing facilities, and energy sector installations, underscoring its broad market reach.

As the residential construction market navigates through affordability and economic challenges, TopBuild’s balanced exposure to commercial and industrial segments positions it to weather the current downturn while maintaining financial strength for future growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.